Quick Navigation

- Report Overview

- Key Takeaways

- Service Type Analysis

- Product Type Analysis

- Arrangement Type Analysis

- End User Analysis

- Service Provider Type Analysis

- Distribution Channel Analysis

- Payment Type Analysis

- Death Care Method Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Market Dynamics

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Geopolitical Impact Analysis

- Report Scope

Report Overview

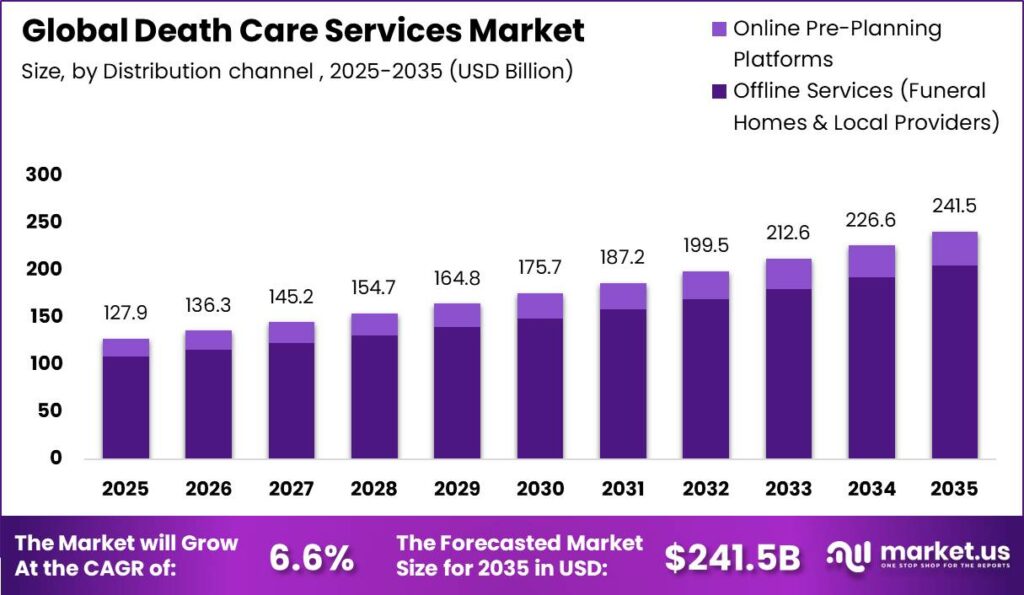

Global Death Care Services Market size is expected to be worth around USD 241.5 Billion by 2035 from USD 127.9 Billion in 2025, growing at a CAGR of 6.6% during the forecast period 2026 to 2035. This steady expansion reflects non-discretionary demand tied to global mortality. Providers gain a stable revenue base regardless of economic cycles.

The Death Care Services Market covers funeral, cremation, burial, memorial, and pre-planning services delivered through funeral homes, crematoriums, and cemeteries. This market structures itself around service providers, product suppliers, and payment models. Therefore buyers, insurers, and operators interact across a fragmented but consolidating value chain, which shapes pricing power and regional service availability.

Key Takeaways

- Global Death Care Services Market reached USD 127.9 Billion in 2025 and will hit USD 241.5 Billion by 2035 at a CAGR of 6.6%.

- Funeral Services led the By Service Type segment with a 41.30% share in 2025.

- Coffins and Caskets dominated the By Product Type segment with a 36.80% share.

- At-Need Services held the By Arrangement Type segment with a 63.20% share.

- Individual Families controlled the By End User segment with a 72.40% share.

- Independent Funeral Homes led the By Service Provider Type segment with a 48.60% share.

- Offline Services captured the By Distribution Channel segment with an 85.10% share.

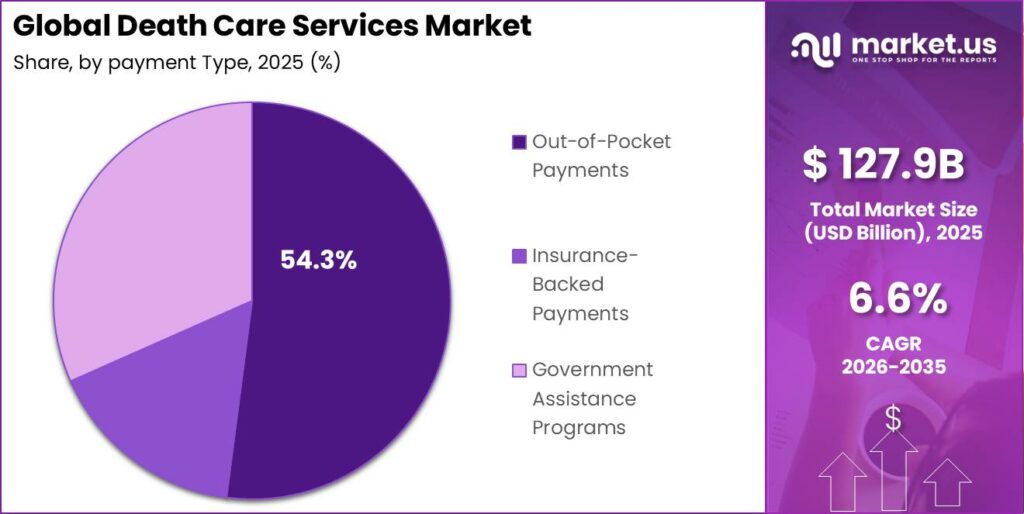

- Out-Of-Pocket Payments led the By Payment Type segment with a 54.30% share.

- Traditional Burial held the By Death Care Method segment with a 49.10% share.

- North America dominated with a 38.40% share, valued at USD 49.11 Billion in 2025.

Government mortality systems and price regulation shape this market directly. The World Health Organization maintains cause-of-death records that let providers forecast demand pools with confidence. As a result, operators plan capacity around predictable death volumes rather than speculative growth, which lowers investment risk across cemetery and crematorium buildouts.

According to WHO data, global mortality exceeds roughly 67 Million deaths annually, forming the base demand pool for death care worldwide. This volume guarantees recurring caseloads for funeral homes. Consequently investors treat the sector as recession-resistant, which supports higher acquisition multiples for well-run regional chains.

As per our research, the average US funeral with burial costs about USD 9,135, while cremation averages USD 6,645. This gap pushes cost-sensitive families toward cremation. Therefore providers that build cremation capacity capture rising volume, even as per-case revenue falls, which reshapes long-term margin strategy. Globally, cremation now accounts for around 50% of dispositions, and in parts of Asia it exceeds 90% of deaths, while UK burial share has fallen to roughly 26%. This structural shift signals where new infrastructure spending should flow.

Service Type Analysis

Funeral Services dominates with 41.30% due to bundled ceremony and logistics demand.

In 2025, Funeral Services held a dominant market position in the By Service Type segment of Death Care Services Market, with a 41.30% share. WHO figures confirm roughly 67 Million deaths occur yearly, sustaining ceremony demand. This scale means full-service homes retain pricing power. Providers that bundle transport, preparation, and ceremony services protect margins as families seek single-point convenience during bereavement.

Families choose Cremation Services increasingly for cost and land reasons, making it the fastest-growing service. NFDA data shows the US cremation rate reached 63.4% in 2025, more than double the burial rate of 31.6%. This shift lowers per-case spend but lifts throughput. Operators adding retort capacity capture volume before competitors, securing early share in a rapidly converting market.

Buyers use Burial Services, Memorial Services, and Pre-Planning Services to address tradition, remembrance, and advance cost control. In the UK, burial has declined to about 26% of funerals, reflecting a structural move toward alternatives. This means burial providers must diversify into memorialization and pre-need contracts. In July 2025, Tukios acquired Batesville’s AI obituary writing services, signaling growing digital memorial demand that reshapes remembrance offerings collectively across these remaining service types.

Product Type Analysis

Coffins and Caskets dominates with 36.80% due to traditional burial merchandise reliance.

In 2025, Coffins and Caskets held a dominant market position in the By Product Type segment of Death Care Services Market, with a 36.80% share. UN Comtrade trade flows record steady casket shipments across North America and Europe. This demand anchors supplier revenue despite cremation growth. Manufacturers that control materials sourcing protect margins as buyers weigh premium wood against economy metal options.

Grieving families select Urns as cremation adoption climbs, making urns the fastest-growing product. CANA reports US cremation reached roughly 62% by the mid-2020s, expanding the urn buyer base rapidly. This trend rewards suppliers offering personalized and biodegradable designs. Vendors that lead on customization capture higher-margin sales as commodity urns face price pressure.

Providers rely on Embalming Products, Grave Markers and Headstones, and Funeral Accessories to complete service delivery. Matthews International expanded its embalming supply operations through the June 2025 Dodge Company acquisition, confirming durable demand for preparation chemicals. This means accessory suppliers hold defensible niches. These remaining product lines together serve traditional burial workflows that resist full displacement by cremation.

Arrangement Type Analysis

At-Need Services dominates with 63.20% due to immediate post-death service urgency.

In 2025, At-Need Services held a dominant market position in the By Arrangement Type segment of Death Care Services Market, with a 63.20% share. WHO mortality records show around 67 Million annual deaths trigger immediate service needs. This urgency limits price comparison by families. Providers therefore capture strong margins on at-need cases, since bereaved buyers rarely negotiate during acute grief.

Households increasingly select Pre-Need and Pre-Planning Services to lock in prices, making this the fastest-growing arrangement. UK data shows the cost of dying reached £9,797 at record levels, pushing families toward advance payment. This shift stabilizes provider cash flow through upfront contracts. Operators building pre-need portfolios secure predictable future revenue and hedge against inflation-driven cost spikes.

End User Analysis

Individual Families dominates with 72.40% due to direct household service purchasing.

In 2025, Individual Families held a dominant market position in the By End User segment of Death Care Services Market, with a 72.40% share. World Bank household data confirms families bear most end-of-life spending directly. This concentration makes consumer trust central to provider success. Firms that build local reputation retain repeat family business across generations, protecting share from new entrants.

Religious and Community Organizations arrange services tied to faith traditions, forming the fastest-growing end-user group. In parts of Asia, cremation exceeds 90% of deaths, shaping community-managed disposition demand. This means providers partnering with religious bodies gain volume access. Operators that respect ritual requirements win contracts that individual marketing cannot reach.

Government and Institutional Clients procure services for indigent care, unclaimed remains, and public health needs. National statistical offices record steady public-sector death care spending across municipalities. This creates stable, tender-based revenue for qualified providers. These institutional buyers hold the remaining share collectively, offering volume contracts that offset consumer-market seasonality for scaled operators.

Service Provider Type Analysis

Independent Funeral Homes dominates with 48.60% due to trusted local community relationships.

In 2025, Independent Funeral Homes held a dominant market position in the By Service Provider Type segment of Death Care Services Market, with a 48.60% share. UNIDO service-sector data shows fragmented ownership across most national markets. This fragmentation preserves local loyalty as a competitive moat. Independents that maintain personal service resist corporate encroachment, though they face capital constraints for facility upgrades.

Corporate Funeral Service Chains scale through acquisition, making them the fastest-growing provider type. Regulatory filings show major chains completed dozens of buyouts across North America during 2025. This consolidation lowers unit costs through shared procurement. Chains that integrate acquired homes efficiently gain pricing advantages that pressure independent competitors on merchandise margins.

Crematorium Operators and Cemeteries and Memorial Parks provide specialized infrastructure across the disposition chain. Customs and land-use records confirm high capital intensity for crematory and cemetery assets. This capital barrier limits new entrants, protecting incumbents. These provider types hold the remaining share collectively, anchoring the physical backbone that funeral homes depend on for service completion.

Distribution Channel Analysis

Offline Services dominates with 85.10% due to in-person arrangement and body handling.

In 2025, Offline Services held a dominant market position in the By Distribution Channel segment of Death Care Services Market, with an 85.10% share. National statistical offices confirm physical funeral homes handle the vast majority of arrangements. This physical requirement stems from body handling and ceremony hosting. Providers with local premises retain control, since core services cannot fully digitize.

Families increasingly use Online Pre-Planning Platforms for advance arrangements, making this the fastest-growing channel. ITU digital-adoption data shows rising internet use for financial and service planning across mature markets. This trend opens low-cost customer acquisition for digital-first providers. Operators that offer online pre-need tools capture younger planners before traditional competitors engage them.

Payment Type Analysis

Out-Of-Pocket Payments dominates with 54.30% due to limited funeral insurance penetration.

In 2025, Out-Of-Pocket Payments held a dominant market position in the By Payment Type segment of Death Care Services Market, with a 54.30% share. World Bank data shows most households fund funerals from savings rather than coverage. This reliance exposes families to sudden financial strain. Providers offering payment plans capture price-sensitive buyers and reduce unpaid-invoice risk.

Families increasingly choose Insurance-Backed Payments to spread rising costs, making this the fastest-growing payment type. IMF economic data links inflation pressure to demand for pre-funded coverage. This shift stabilizes provider collections through guaranteed insurer payouts. Operators partnering with insurers secure reliable revenue and attract cost-conscious pre-need customers.

Government Assistance Programs fund services for low-income and indigent cases across many jurisdictions. Regulatory filings confirm public death-benefit schemes cover a measurable share of funerals. This creates guaranteed but low-margin volume for participating providers. These assistance programs hold the remaining share collectively, offering baseline caseloads that support facility utilization during demand troughs.

Death Care Method Analysis

Traditional Burial dominates with 49.10% due to enduring religious and cultural mandates.

In 2025, Traditional Burial held a dominant market position in the By Death Care Method segment of Death Care Services Market, with a 49.10% share. FAO land-use data confirms cemetery allocation remains substantial across many regions. This persistence reflects deep religious mandates in Middle Eastern and South Asian communities. Providers serving these markets retain stable burial demand that cremation trends cannot quickly erode.

Families adopt Cremation rapidly for lower cost and land efficiency, making it the fastest-growing method. Globally cremation now accounts for around 50% of dispositions, exceeding burial in multiple regions. This shift redirects capital toward crematory infrastructure. Operators expanding retort capacity capture converting volume ahead of slower traditional competitors.

Providers develop Green and Eco-Friendly Burial and Direct Cremation to serve environmental and budget-driven families. National regulatory records show growing approval of aquamation and terramation methods. This trend opens premium and value niches simultaneously. These emerging methods hold the remaining share collectively, letting differentiated providers capture families that reject both conventional burial and standard cremation.

Key Market Segments

By Service Type

- Funeral Services

- Cremation Services

- Burial Services

- Memorial Services

- Pre-Planning Services

By Product Type

- Coffins & Caskets

- Urns

- Embalming Products

- Grave Markers & Headstones

- Funeral Accessories

By Arrangement Type

- At-Need Services

- Pre-Need / Pre-Planning Services

By End User

- Individual Families

- Religious & Community Organizations

- Government & Institutional Clients

By Service Provider Type

- Independent Funeral Homes

- Corporate Funeral Service Chains

- Crematorium Operators

- Cemeteries & Memorial Parks

By Distribution Channel

- Offline Services (Funeral Homes & Local Providers)

- Online Pre-Planning Platforms

By Payment Type

- Out-Of-Pocket Payments

- Insurance-Backed Payments

- Government Assistance Programs

By Death Care Method

- Traditional Burial

- Cremation

- Green / Eco-Friendly Burial

- Direct Cremation (No Ceremony)

Regional Analysis

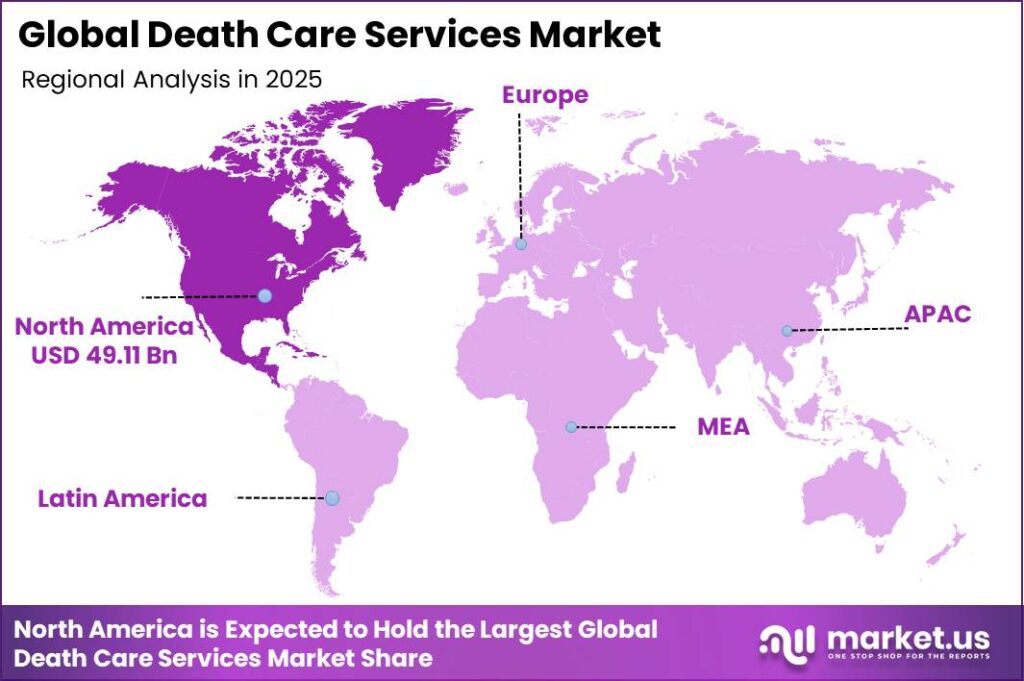

North America Dominates the Death Care Services Market with a Market Share of 38.40%, Valued at USD 49.11 Billion

North America led the Death Care Services Market in 2025 with a 38.40% share worth USD 49.11 Billion. High cremation adoption and organized corporate chains drive this dominance. This means the region sets pricing and consolidation benchmarks. In October 2025, Rumbu Holdings acquired Warren and Son funeral home in Saskatchewan, expanding Canadian death care operations and reinforcing regional consolidation momentum.

Asia Pacific ranks as the fastest-growing region as urbanization lifts demand for professionalized funeral homes. Cremation adoption there exceeds 90% of deaths in several markets, driven by land constraints. This scale rewards operators building high-throughput crematory networks. Providers entering dense metro areas early capture share before organized competition matures.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Underserved eco, digital, and institutional niches offer entry points for new players

Online Pre-Planning Platforms remain underexploited despite Offline Services holding an 85.10% share. This gap means digital-first entrants face little organized competition for younger planners. Therefore new players building intuitive pre-need portals capture a rising customer segment before incumbents digitize. Early movers lock in relationships years before the eventual at-need transaction occurs.

Pre-Need Services stay underpenetrated while At-Need Services command a 63.20% share. This imbalance signals that most families still buy under duress rather than in advance. Consequently providers marketing pre-need contracts unlock predictable, inflation-hedged revenue that competitors overlook. New entrants targeting ageing but healthy households can build portfolios that mature into guaranteed future caseloads.

Green and Eco-Friendly Burial and Direct Cremation hold only the residual share behind Traditional Burial at 49.10%. This means environmentally driven demand outpaces current supply in many regions. Instead of competing on price alone, new players offering aquamation or terramation differentiate on sustainability. Investors backing these niche methods position for outsized share as regulation opens.

Religious and Community Organizations and institutional clients trail Individual Families at 72.40% of the End User segment. This concentration leaves community and public-sector channels comparatively open. Therefore providers partnering with faith bodies and municipalities access volume that consumer marketing cannot reach. New entrants winning tender-based institutional contracts secure stable baseline caseloads that smooth seasonal demand.

Technology and Innovation Landscape - Digital memorials, AI content, and eco-methods redefine competitive edges

Digital memorial platforms reshape remembrance by offering interactive legacy management and online services. In July 2025, Tukios acquired Batesville’s AI obituary writing services, signaling rapid platform consolidation. This means providers can monetize post-funeral engagement beyond the ceremony. Operators adopting these tools build recurring digital revenue that traditional single-event models cannot match.

Livestreamed funeral ceremonies now enable remote participation across dispersed global families. This capability extends service reach beyond the physical venue. Therefore providers offering hybrid ceremonies capture diaspora and migrant demand that competitors cannot serve locally. Firms integrating streaming into standard packages differentiate on accessibility and widen their addressable client base.

AI-generated obituaries and QR-enabled headstones link physical memorials to digital life archives. These innovations create upsell paths tied to personalization. This means providers add high-margin digital products onto conventional merchandise sales. Operators deploying QR memorials and AI content tools convert one-time buyers into ongoing subscribers of legacy services.

Eco-friendly methods such as aquamation and terramation advance as material and process innovations. Regulatory approval in new jurisdictions expands their commercial reach. As a result, providers investing early in low-carbon disposition equipment gain first-mover branding. Firms combining green technology with transparent footprint reporting attract environmentally conscious families willing to pay premiums.

Drivers

Demographic momentum anchors death care demand as ageing cohorts lift annual deaths. The World Health Organization recorded approximately 68 million deaths worldwide in 2021, and US provisional figures show more than 3,070,000 deaths in 2024 at an age-adjusted rate near 722 per 100,000. This means addressable volume grows even as age-specific mortality improves. Providers therefore gain a stable, non-discretionary demand floor contributing an estimated +2.8% to the baseline CAGR of 6.6%.

Rising cremation rates and urbanization reshape where growth concentrates. This means volumes shift toward lower-cost, higher-throughput services while pre-need contracts hedge climbing end-of-life costs. Cultural acceptance of personalized memorials adds further momentum. Consequently operators that expand cremation capacity and pre-need offerings capture converting families ahead of slower traditional competitors across mature and emerging markets alike.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural increase in annual deaths from population ageing and demographic momentum | +2.8% | Global | Long term (≥ 4 years) |

| High and rising cremation rates shifting volumes toward lower-cost but higher-throughput services | +1.6% | North America, Europe | Medium term (2–4 years) |

| Urbanization driving demand for professionalized, full-service funeral homes | +1.1% | Asia-Pacific, Latin America, Africa | Medium term (2–4 years) |

| Growth in pre-need funeral and cremation contracts as households hedge rising end-of-life costs | +0.9% | North America, Europe, Japan | Short term (≤ 2 years) |

| Cultural normalization of non-religious and personalized memorial services | +0.7% | Global | Medium term (2–4 years) |

Restraints

Margin compression pressures providers as cremation displaces higher-spend burial. The Cremation Association of North America reported a US cremation rate near 62.8% and 77.4% in Canada in 2025, up from 57.2% and 74.0% in 2021. Because cremation families buy fewer premium caskets and embalming services, blended revenue per case falls. This pulls an estimated -2.0% off the attainable CAGR of 6.6% unless providers upsell memorialization.

High infrastructure costs further restrain expansion in dense urban zones. Real-estate and maintenance expenses for cemeteries strain provider balance sheets. This means new burial-ground and crematorium development slows where land is scarce. Consequently operators delay capacity additions, limiting growth in the markets with the highest death volumes and strongest latent demand.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin compression from higher cremation penetration and reduced spend on embalming and merchandise | -2.0% | North America, Europe | Medium term (2–4 years) |

| Tightening air-emissions and environmental rules on crematoria and burial grounds | -1.5% | Europe, North America | Medium term (2–4 years) |

| High real-estate and maintenance costs for urban cemeteries | -1.1% | Global cities | Long term (≥ 4 years) |

| Price sensitivity of lower-income households facing rising funeral expenses | -0.9% | Global | Short term (≤ 2 years) |

| Regulatory barriers to introducing new disposition methods in some jurisdictions | -0.7% | Europe, parts of Asia | Long term (≥ 4 years) |

Challenges

Workforce shortages strain funeral homes as licensed directors and embalmers retire faster than new graduates arrive. Smaller firms handle hundreds of cases yearly with only a few licensed professionals, driving burnout. Call volumes swing seasonally by 20–30% while staffing cannot flex at the same rate. This forces owners to cap cases or pay heavy overtime, dragging roughly -1.7% off maximum growth over a 2–4 year horizon.

Operational complexity compounds this labor gap across the sector. Providers must navigate diverse cultural, religious, and legal requirements per case while upgrading capital-intensive facilities. This means capacity to serve rising death volumes is limited by people, not buildings. Consequently firms investing in training, retention bonuses, and workflow automation avoid service failures and convert constrained capacity into a new efficiency-driven revenue stream.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Workforce shortages and burnout among licensed funeral directors and embalmers | -1.7% | North America, Europe | Medium term (2–4 years) |

| Complexity of navigating diverse cultural, religious, and legal requirements per case | -1.3% | Global | Long term (≥ 4 years) |

| Capital intensity of upgrading cremation and refrigeration facilities | -1.1% | Global | Medium term (2–4 years) |

| Digitalization gaps in case management, pre-need sales, and family communications | -0.9% | Global | Medium term (2–4 years) |

| Reputational risk and regulatory scrutiny following incidents of mishandled remains | -0.8% | Global | Short term (≤ 2 years) |

Opportunities

Eco-friendly disposition opens premium revenue as families reject high-footprint methods. One French study estimated a single conventional burial generates around 833 kg of CO2 equivalent, while US cremation emits roughly 360,000 tons of CO2 annually. As jurisdictions legalize aquamation and terramation, even 10–20% of families shifting to eco-alternatives lets providers charge a premium. This adds an estimated +2.1% to the baseline CAGR of 6.6%.

Digital planning and integrated advisory services widen the revenue base further. End-to-end platforms enable remote arrangements and hybrid memorials, while grief-care and pre-need bundles lift spend per family. This means early movers build recurring relationships beyond the single funeral event. Therefore providers combining eco-options with digital and advisory services position themselves to capture the fastest-expanding margins in competitive urban markets.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Eco-friendly disposition options (aquamation, terramation, green burial) capturing environmentally conscious families | +2.1% | North America, Europe, Oceania | Long term (≥ 4 years) |

| End-to-end digital planning platforms for remote arrangements and hybrid memorials | +1.6% | Global | Medium term (2–4 years) |

| Integrated grief-care, estate, and pre-need advisory services increasing revenue per family served | +1.4% | North America, Europe | Medium term (2–4 years) |

| Partnerships with healthcare and senior-living providers for coordinated end-of-life pathways | +1.2% | Global | Long term (≥ 4 years) |

| Operational decarbonization and transparent footprint reporting as differentiators in competitive urban markets | +1.0% | Europe, North America | Long term (≥ 4 years) |

Key Company Insights

Service Corporation International holds a structural advantage through the largest funeral and cemetery network in North America. WHO maintains a global mortality database from 1950 onward, and this scale lets the company forecast demand precisely across markets. The US cremation services market alone was worth about USD 2.8 Billion in 2023. This means its combined funeral and cemetery model captures both burial and cremation revenue, though heavy cremation exposure pressures merchandise margins.

Stonemor Inc. positions itself around cemetery and memorial-park assets that generate recurring pre-need income. UK funeral costs rose more than 134% over 21 years, and the cost of dying reached £9,797, showing why families pre-fund. In June 2025, Matthews International expanded embalming supply through the Dodge acquisition, signaling durable product demand that supports memorial-park operators. This land-heavy model creates a defensible moat but ties up capital, limiting rapid geographic expansion.

Key Players

- Service Corporation International

- Stonemor Inc.

- Carriage Services, Inc.

- Park Lawn Corporation

- Nirvana Asia Ltd.

- Invocare Limited

- Dignity Plc

- Fu Shou Yuan International Group

- San Holdings, Inc.

- Hillenbrand, Inc.

- Matthews International Corporation

- Carriage Funeral Holdings (Carriage Services Segment Brands)

- Keystone Group

- Northstar Memorial Group

- Lifemark Group

Recent Developments

- December 2025: Anthem Partners completed multiple strategic acquisitions and divestitures across the United States to expand its funeral home and cemetery portfolio while streamlining underperforming assets.

- April 2025: Propel Funeral Partners acquired Richmond Funeral Home Limited in Canada as part of its ongoing expansion strategy in cremation and funeral service operations.

- October 2025: Park Lawn Corporation acquired multiple funeral home and crematory assets in Georgia, strengthening its North American funeral service footprint.

- September 2025: Carriage Services expanded its US operations by acquiring Faith Chapel Funeral Homes and Crematory in Florida to increase regional market penetration.

Geopolitical Impact Analysis

According to the World Trade Organization, tariff escalation has raised import costs for caskets, urns, and embalming inputs sourced across borders. The WTO recorded average applied tariffs near 9% on some manufactured goods, while global merchandise trade volume growth slowed to about 2.7% recently. This means death care suppliers relying on imported hardwood caskets and metal fittings face higher landed costs. Providers therefore reshore procurement or accept thinner merchandise margins.

As reported by UNCTAD, shipping disruptions and Red Sea rerouting added roughly 10 to 14 days of transit delay on some Asia-to-Europe routes, while container freight rates rose over 150% during peak disruption. This means casket and urn importers face longer lead times and volatile logistics costs. Consequently death care operators build larger safety stock or shift toward regional suppliers to protect service reliability during volatile geopolitical periods.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 127.9 Billion |

| Forecast Revenue (2035) | USD 241.5 Billion |

| CAGR (2026-2035) | 6.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Funeral Services, Cremation Services, Burial Services, Memorial Services, Pre-Planning Services), By Product Type (Coffins & Caskets, Urns, Embalming Products, Grave Markers & Headstones, Funeral Accessories), By Arrangement Type (At-Need Services, Pre-Need / Pre-Planning Services), By End User (Individual Families, Religious & Community Organizations, Government & Institutional Clients), By Service Provider Type (Independent Funeral Homes, Corporate Funeral Service Chains, Crematorium Operators, Cemeteries & Memorial Parks), By Distribution Channel (Offline Services, Online Pre-Planning Platforms), By Payment Type (Out-Of-Pocket Payments, Insurance-Backed Payments, Government Assistance Programs), By Death Care Method (Traditional Burial, Cremation, Green / Eco-Friendly Burial, Direct Cremation) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Service Corporation International, Stonemor Inc., Carriage Services Inc., Park Lawn Corporation, Nirvana Asia Ltd., Invocare Limited, Dignity Plc, Fu Shou Yuan International Group, San Holdings Inc., Hillenbrand Inc., Matthews International Corporation, Carriage Funeral Holdings, Keystone Group, Northstar Memorial Group, Lifemark Group |

| Customization Scope | Customization for segments, region / country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License | Multi-User License (Up to 5 Users) | Corporate Use License (Unlimited User and Printable PDF) |