Quick Navigation

Report Overview

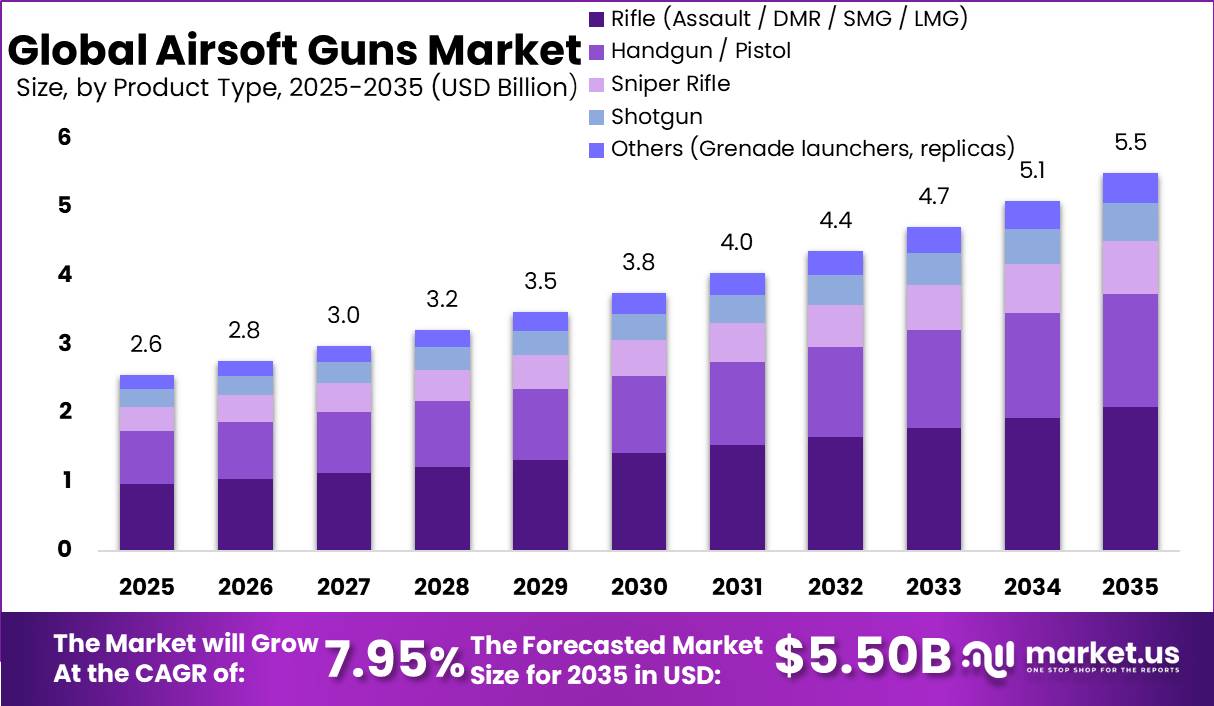

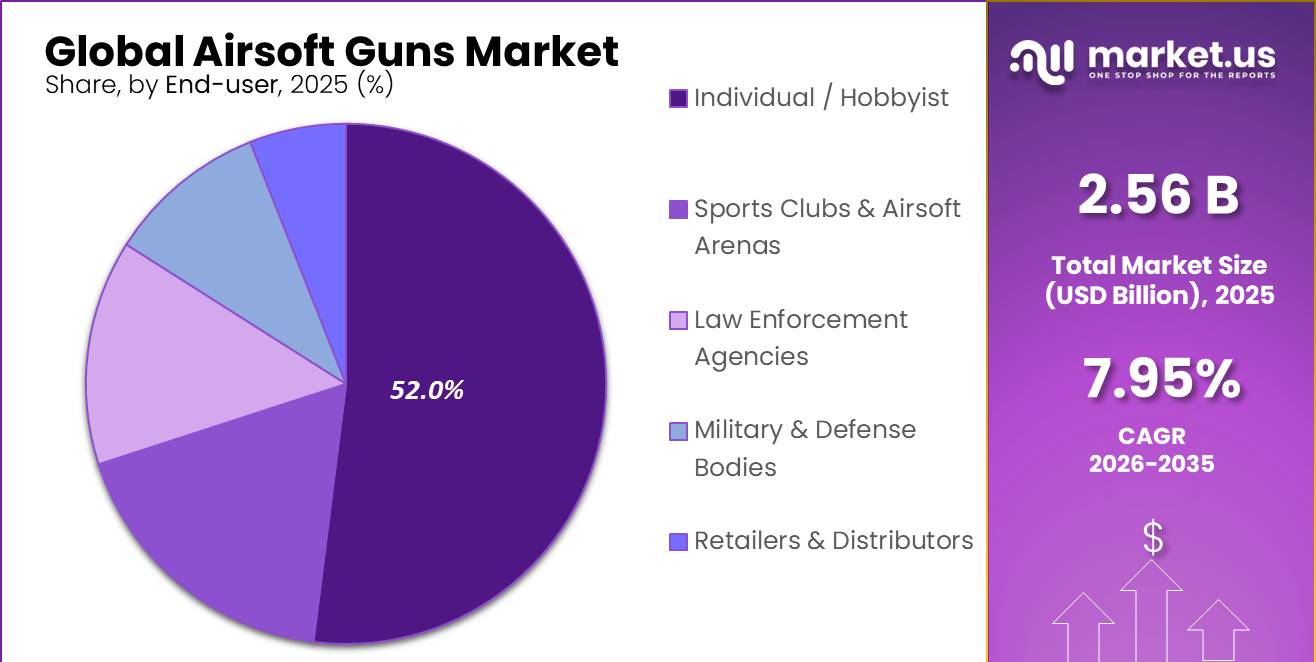

Global Airsoft Guns Market size is expected to be worth around USD 5.50 Billion by 2035 from USD 2.56 Billion in 2025, growing at a CAGR of 7.95% during the forecast period 2026 to 2035. This trajectory reflects steady consumer conversion from entry-level spring platforms to higher-value electric and gas systems across core recreational and training segments.

The airsoft guns market covers battery-powered, spring-driven, and gas-operated replica firearms used across recreational skirmish, military simulation, sport shooting, and training applications. Product categories span rifles, handguns, sniper replicas, and shotguns, distributed through specialty retail, sporting goods chains, and direct-to-consumer online platforms. End users range from individual hobbyists to organized sports clubs and law enforcement agencies.

Key Takeaways

- Global Airsoft Guns Market was valued at USD 2.56 Billion in 2025 and is forecast to reach USD 5.50 Billion by 2035.

- The market grows at a CAGR of 7.95% from 2026 to 2035.

- North America dominates with a 35% market share, valued at USD 0.89 Billion in 2025.

- By Product Type, Rifle (Assault/DMR/SMG/LMG) holds the dominant share at 38.00%.

- By Mechanism, Spring-Powered (Manual) leads with a 50.00% share.

- By End User, Individual/Hobbyist accounts for the largest segment at 52.00%.

- By Price Range, Mid-Range (USD 100–500) holds a 45.00% share.

- By Distribution Channel, Offline channels command 74.70% of sales.

Regulatory structures shape participation and product design across major markets. According to ukara data, UKARA requires players to be over 18 years old and complete 3 games across more than 56 days at a registered site before obtaining a retail verification status. This requirement creates a measurable conversion lag between new field participants and licensed buyers.

As reported by ukara, UKARA-registered game sites must maintain more than 20 registered eligible players and accurate member records. This structure formalizes skirmish-field participation and creates traceable demand data for retailers and distributors planning inventory deployment. By contrast, Canada classifies any airsoft gun firing below 111.6 m/s or 366 fps that closely resembles a real firearm as a prohibited replica, per rcmp data, directly restricting the importable product range for that market.

Product Type Analysis

Rifle (Assault/DMR/SMG/LMG) dominates with 38.00% due to versatility across skirmish and mil-sim formats.

In 2025, Rifle (Assault/DMR/SMG/LMG) held a dominant market position in the By Product Type segment of the Airsoft Guns Market, with a 38.00% share. Rifle platforms support the widest range of gameplay styles, from close-quarters combat to long-range mil-sim, making them the default first purchase for new and returning players. This breadth of application keeps rifle SKUs at the center of retailer assortment planning.

Handgun/Pistol platforms capture 30.00% of the product type segment, functioning primarily as sidearms in mil-sim loadouts and as standalone training tools for law enforcement and competitive players. Their lower price points and compact form factor support high unit turnover at retail. This segment also benefits from gas-blowback technology adoption, which increases average selling price among realism-focused buyers.

Sniper Rifle holds a 14.00% share, anchored by a dedicated player segment willing to pay premium prices for precision-engineered spring and gas platforms. Sniper users typically invest in aftermarket upgrades including hop-up assemblies and tightbore barrels, generating sustained aftermarket revenue for suppliers. This segment rewards brands with strong licensing agreements and consistent engineering tolerances.

Shotgun accounts for 10.00% of the segment, serving niche skirmish scenarios and collector use cases. Remaining product types including grenade launchers and specialty replicas collectively hold 8.00%. In August 2025, KRYTAC unveiled a 40 mm gas grenade shell and modular grenade launcher, signaling that even niche accessory-linked product lines attract investment from established brands.

Mechanism / Power Type Analysis

Spring-Powered (Manual) dominates with 50.00% due to low cost and zero battery dependency.

In 2025, Spring-Powered (Manual) held a dominant market position in the By Mechanism / Power Type segment of the Airsoft Guns Market, with a 50.00% share. Spring platforms serve as the entry point for most new players due to their affordability, mechanical simplicity, and compliance ease across regulated markets. Retailers rely on spring-gun volume to drive foot traffic and first-purchase conversions that later migrate to higher-margin electric platforms.

Electric-Powered (AEG) holds a 30.00% share and represents the primary upgrade destination for players moving beyond spring platforms. AEG systems support semi-automatic and fully automatic fire modes, MOSFET trigger upgrades, and LiPo battery compatibility, creating a multi-year accessory revenue stream per user. As per our research, Desert Fox Airsoft Events enforces a 400 FPS limit with 0.20 g BBs across pistols, shotguns, and rifles, defining a product-design ceiling that AEG manufacturers engineer to meet precisely.

Gas-Powered platforms account for 18.00% of the mechanism segment, driven by demand for blowback realism in mil-sim and collector applications. Gas-blowback pistols and rifles command the highest average selling prices within their respective product categories, supporting stronger margin profiles for brands. This segment is most sensitive to ambient temperature variation, which affects consistent performance and repeat field use.

Others/Hybrid mechanisms hold the remaining 2.00%. This sub-segment includes dual-power and experimental platforms that serve niche testing and development audiences rather than mainstream retail channels. Consequently, hybrid platforms carry limited near-term volume impact but signal ongoing engineering experimentation within the broader market.

End User Analysis

Individual/Hobbyist dominates with 52.00% due to discretionary recreational spending patterns.

In 2025, Individual/Hobbyist held a dominant market position in the By End User segment of the Airsoft Guns Market, with a 52.00% share. Individual buyers drive the widest retail distribution requirement, purchasing across specialty airsoft stores, sporting goods chains, and e-commerce platforms. This segment’s behavior sets the demand baseline that field operators, distributors, and brands build their inventory strategies around.

Sports Clubs and Airsoft Arenas represent the organized participation layer, purchasing rental fleets, consumables, and venue-grade equipment in bulk. Club-level procurement differs structurally from individual buying, favoring durable AEG platforms with replaceable internal components over premium collector replicas. This creates a distinct B2B sales channel that rewards suppliers offering after-sales service and parts availability alongside hardware.

Law Enforcement Agencies and Military and Defense Bodies purchase airsoft systems specifically for force-on-force scenario training and close-quarters tactics rehearsal. As per our research, Canada treats air guns exceeding both 152.4 m/s or 500 fps and 5.7 joules as firearms under the Firearms Act, setting a hard product-specification ceiling that training-use suppliers must design around when shipping to Canadian defense clients.

Price Range Analysis

Mid-Range (USD 100–500) dominates with 45.00% due to balance of performance and accessibility.

In 2025, Mid-Range (USD 100–500) held a dominant market position in the By Price Range segment of the Airsoft Guns Market, with a 45.00% share. This band captures the primary upgrade path for players moving from entry spring platforms to entry and mid-tier AEG and gas systems. Brands positioned in this tier benefit from the largest active buyer pool and the highest reorder frequency among hobbyist users.

Distribution Channel Analysis

Offline dominates with 74.70% due to tactile evaluation needs and in-store regulatory compliance support.

In 2025, Offline held a dominant market position in the By Distribution Channel segment of the Airsoft Guns Market, with a 74.70% share. Specialty airsoft and tactical stores, sporting goods retailers, gun shops, and hobby stores collectively anchor offline sales by offering hands-on product evaluation, age verification, and in-person compliance guidance that online channels cannot replicate. This structural dependence on physical retail protects established brick-and-mortar operators from pure e-commerce displacement.

Online distribution including brand-owned D2C websites, e-commerce marketplaces such as Amazon, eBay, and Evike.com, and social commerce platforms captures the remaining share. As per our research, Canada Border Services Agency confirms that both the velocity threshold of 152.4 m/s or 500 fps and the energy threshold of 5.7 joules must be exceeded together for a product to be regulated as a firearm, providing online importers with a precise product-specification target for cross-border shipment compliance.

Key Market Segments

By Product Type

- Rifle (Assault / DMR / SMG / LMG)

- Handgun / Pistol

- Sniper Rifle

- Shotgun

- Others (Grenade launchers, replicas)

By Mechanism / Power Type

- Spring-Powered (Manual)

- Electric-Powered (AEG – Automatic Electric Gun)

- Gas-Powered

- Others / Hybrid

By End User

- Individual / Hobbyist

- Sports Clubs and Airsoft Arenas

- Law Enforcement Agencies

- Military and Defense Bodies

- Retailers and Distributors

By Price Range

- Low / Entry-Level (Below USD 100)

- Mid-Range (USD 100–500)

- High / Premium (Above USD 500)

By Distribution Channel

- Offline

- Specialty airsoft and tactical stores

- Sporting goods and outdoor retailers

- Gun shops and hobby stores

- Airsoft arenas and rental outlets

- Online

- Brand-owned D2C websites

- E-commerce marketplaces (Amazon, eBay, Evike.com)

- Social commerce and community forums

Regional Analysis

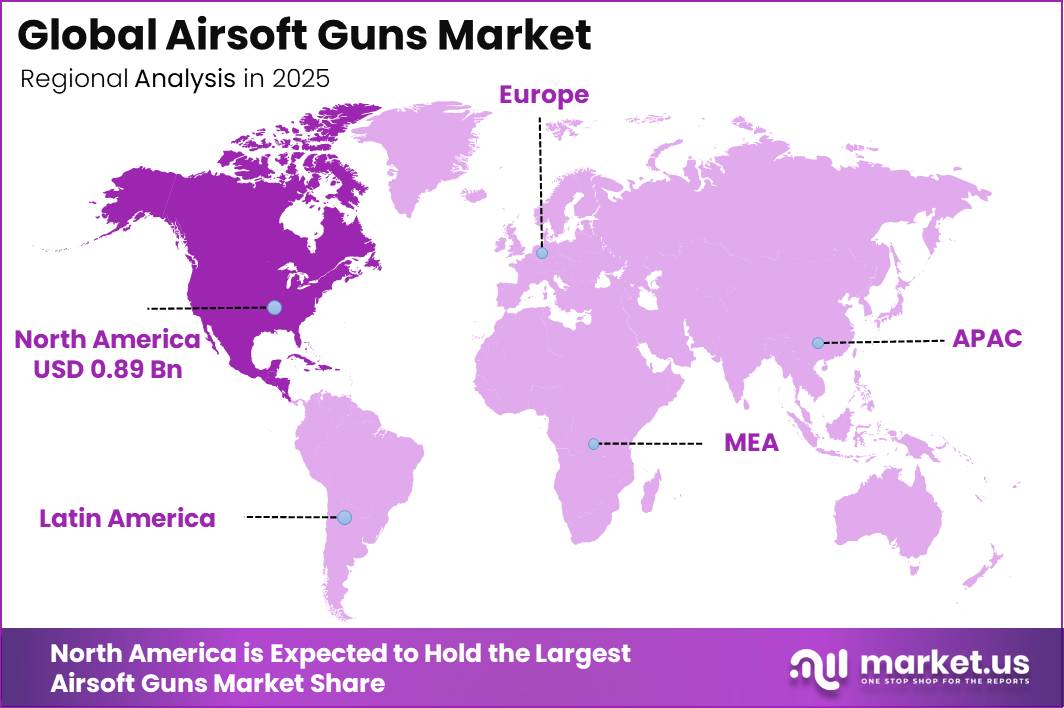

North America Dominates the Airsoft Guns Market with a Market Share of 35%, Valued at USD 0.89 Billion

North America holds a 35% share valued at USD 0.89 Billion in 2025, supported by a large organized field network, strong specialty retail infrastructure, and consistent consumer spending on tactical recreational products. U.S. federal imitation-firearm marking rules, requiring a blaze-orange plug recessed no more than 6 mm per ecfr data, define a product-design standard that all market entrants must meet to access this dominant region.

Europe represents the second-largest regional market, driven by a dense network of registered skirmish fields operating under national replica-firearm regulations and joule-based FPS limits. The UK’s structured UKARA verification system and the broader EU’s varied national rules create compliance complexity that favors established importers with dedicated legal and logistics teams. This regulatory density raises entry barriers and supports premium brand positioning across Western European markets.

Asia Pacific functions as both the primary manufacturing base and a fast-expanding consumer region, with Japan anchoring the premium engineering segment and Southeast Asian markets growing participation at the hobby level. Taiwan and China supply the majority of global AEG and spring-platform production, giving APAC manufacturers structural cost advantages in export-oriented sales. This dual role as producer and consumer creates vertically integrated opportunities unavailable to purely import-dependent Western brands.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

The primary driver is the steady shift from low-cost spring units toward electric-powered and gas-blowback systems that replicate recoil feel, magazine logic, and accessory compatibility. This product mix upgrade allows the market to grow revenue faster than unit volume alone. Premium internals, MOSFET trigger systems, hop-up assemblies, and LiPo batteries raise average revenue per user and support high aftermarket attach rates over a 24 to 36 month ownership cycle.

In Japan, legal energy limits below 0.98 joules and adult-only ownership rules push manufacturers to compete through precision engineering and collector-grade finish quality rather than raw power output. This regulation-induced emphasis on quality structurally favors premium brands over commodity sellers. Market.us estimates this driver contributes an estimated +1.4 percentage-point uplift to CAGR, particularly across North America, Japan, and the EU where serious players over-index on accessories and replacement parts.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organized airsoft participation and field expansion | +1.8% | North America core, Western Europe, Japan, South Korea | Short term (≤ 2 years) |

| Mil-sim realism and training-grade platform premiumization | +1.4% | North America core, Japan, EU, select APAC corridors | Medium term (2-4 years) |

| E-commerce-led assortment reach and direct-to-consumer conversion | +1.2% | North America, EU, Southeast Asia, cross-border APAC | Short term (≤ 2 years) |

| Compliance-driven product refresh under safety and replica rules | +0.9% | US, EU, Japan | Medium term (2-4 years) |

| Asia-centric sourcing scale with export redistribution | +0.8% | China-Hong Kong-Taiwan manufacturing base, US/EU import markets | Medium term (2-4 years) |

| Leisure spending recovery and tourism-linked hobby purchases | +0.7% | EU, Japan, North America urban hobby clusters | Short term (≤ 2 years) |

Restraints

Airsoft purchases are non-essential and hobby-led, bundled with ancillary spend on BBs, gas, batteries, optics, protective gear, and field fees, so consumer stress compounds across the full participation wallet. As per our research, U.S. sporting-goods spending fell 9% year over year in the three months ended January 2026, signaling softness in the broader discretionary recreation basket that directly affects airsoft sell-through rates.

A player facing a 10% to 15% rise in total hobby cost can delay primary-gun upgrades by 6 to 12 months, trade down from gas-blowback to spring or entry AEG platforms, or shift to second-hand channels. This behavior causes retailers to face slower premium mix, higher promotion intensity, and inventory aging. Market.us estimates this restraint supports an estimated 100 basis-point reduction to near-term CAGR across the US, Western Europe, and affluent APAC urban markets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replica regulation tightening | -1.4% | North America core, EU, UK, Japan | Short term (≤ 2 years) |

| Tariff-led retail inflation | -1.1% | US core, EU import channels | Short term (≤ 2 years) |

| Compliance cost escalation | -0.9% | EU, UK, North America core | Medium term (2-4 years) |

| Discretionary spend weakness | -1.0% | US, Western Europe, urban APAC | Short term (≤ 2 years) |

| Cross-border fulfillment friction | -0.8% | APAC export corridors, EU, North America | Medium term (2-4 years) |

| Channel liability and platform controls | -0.7% | US, EU, UK, major online marketplaces | Medium term (2-4 years) |

Challenges

The most persistent friction in the airsoft market is not outright prohibition but high-variance customs handling of look-alike products across ports, parcel gateways, and retailer intake systems. Compliance depends on exact conformity with blaze-orange marking rules, barrel-depth specifications, product descriptions, and importer standing. This creates recurring relabeling, split-shipment, and detention risk rather than a single one-time regulatory adjustment for affected brands.

For mid-market importers, an estimated 4% to 7% shipment-inspection incidence applies to higher-realism SKUs, with average dwell-time penalties of 6 to 14 days for secondary review, documentation rework costs of roughly 0.8% to 1.4% of landed value, and assortment pruning of 8% to 12% in channels unwilling to carry seizure-prone models. This means brands must invest in pre-export compliance cells, SKU-level customs coding, and port diversification as permanent operating costs rather than temporary fixes.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Customs Classification Volatility | -1.3% | North America core, EU border nodes, APAC export hubs | Medium term (2-4 years) |

| Battery Logistics Compliance Burden | -0.9% | APAC export corridors, North America imports, EU distributors | Medium term (2-4 years) |

| Fragmented Youth Access Controls | -0.8% | UK retail chain, EU regulatory hubs, North America e-commerce | Short term (≤ 2 years) |

| Tariff Cost Pass-Through Stress | -1.1% | US import channel, China/Taiwan factories, ASEAN rerouting lanes | Long term (≥ 4 years) |

| Insurance And Venue Cost Creep | -0.7% | North America field networks, UK site operators, EU urban sites | Medium term (2-4 years) |

| Quality Variance In Multi-Sourcing | -1.0% | China-Taiwan production base, Southeast Asia backup supply, global brands | Long term (≥ 4 years) |

Opportunities

A major untapped opportunity is the creation of a field-and-retail roll-up model that acquires or franchises fragmented arena operators and converts them into standardized Field-as-a-Service nodes with integrated rentals, consumables, memberships, and e-commerce fulfillment. U.S. shooting and target-sport participation exceeds 52.7 million people, while the U.S. outdoor recreation economy generated USD 696.7 Billion in value added in 2024. Airsoft currently captures only a small share of this adjacent recreation wallet.

Even modest venue economics scale effectively. A single indoor arena model in India cites entry fees of ₹300 to ₹500 per player, implying a 15,000 annual-player venue generates roughly USD 90,000 to USD 180,000 equivalent ticket revenue before rentals and accessories. Multi-site standardization can add 600 to 900 basis points to EBITDA through centralized procurement, private-label BBs, and shared digital customer acquisition systems.

A 20 to 40 site regional platform could expand total addressable monetization per active player by 18% to 25%, lift repeat visit frequency by 1.3 to 1.6 times through memberships, and support a +2.4 percentage-point CAGR uplift over baseline. This means investors willing to consolidate fragmented field operators in North America, the EU, India, and Southeast Asia hold a first-mover structural advantage before institutional capital formalizes the channel.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Field-as-a-Service roll-up | +2.4% | North America core, EU, India, SEA | Short term |

| Corporate events monetization | +1.6% | North America, Western EU, India metros | Short term |

| Licensed collector premiumization | +1.9% | US, Japan, France, Germany, GCC | Medium term |

| Safety-tech compliance stack | +1.3% | US, Canada, EU, Australia | Medium term |

| India indoor micro-arena scaling | +2.1% | India tier 1/2 cities, GCC spillover | Medium term |

| DTC consumables subscription | +1.1% | US, EU, Japan, South Korea | Short term |

Key Company Insights

Tokyo Marui Co., Ltd. holds a structural advantage in the global airsoft market through its precision-engineered platforms designed within Japan’s strict sub-0.98 joule energy limit. This engineering discipline positions Tokyo Marui as the benchmark brand for quality-focused buyers worldwide. In May 2026, the company launched the Electric Gun EVOLT RS FPR MK 4, reinforcing its strategy of continuous product refresh to retain premium segment share.

Umarex GmbH and Co. KG operates through its Elite Force brand, leveraging licensed manufacturer agreements to deliver officially branded replicas across the mid-range and premium price bands. This approach reduces product development cost while capturing buyer trust from established firearm brand recognition. In February 2025, Umarex USA expanded its 2025 airsoft lineup with optics-ready GLOCK MOS airsoft versions and a new E&L AK-based AEG distribution partnership, widening its accessible SKU range without expanding its own manufacturing base.

Key Players

- Tokyo Marui Co., Ltd.

- Umarex GmbH & Co. KG

- G&G Armament Taiwan Ltd.

- Vega Force Company (VFC)

- Valken Sports (Valken Inc.)

- ICS Airsoft, Inc.

- Krytac (Kriss USA)

- Colt’s Manufacturing Company LLC

- Cybergun SA

- Crosman Corporation

- Classic Army

- ARES Airsoft

- WE Tech (WE Airsoft)

- Lancer Tactical Inc.

- CYMA International Ltd.

Recent Developments

- May 2026 – G&G Armament announced the TR16 GMS MK1 9” America’s 250th Edition commemorative airsoft rifle, limited to 2,000 units worldwide with unique serial numbering.

- October 2025 – ICS Airsoft announced it would unveil its officially licensed Taran Tactical Innovations series, authorized through EMG, at the 2025 MOA Exhibition in Taipei.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.56 Billion |

| Forecast Revenue (2035) | USD 5.50 Billion |

| CAGR (2026-2035) | 7.95% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Rifle, Handgun/Pistol, Sniper Rifle, Shotgun, Others); By Mechanism/Power Type (Spring-Powered, Electric-Powered AEG, Gas-Powered, Others/Hybrid); By End User (Individual/Hobbyist, Sports Clubs and Airsoft Arenas, Law Enforcement Agencies, Military and Defense Bodies, Retailers and Distributors); By Price Range (Low/Entry-Level, Mid-Range, High/Premium); By Distribution Channel (Offline, Online) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Tokyo Marui Co., Ltd., Umarex GmbH & Co. KG, G&G Armament Taiwan Ltd., Vega Force Company (VFC), Valken Sports (Valken Inc.), ICS Airsoft Inc., Krytac (Kriss USA), Colt’s Manufacturing Company LLC, Cybergun SA, Crosman Corporation, Classic Army, ARES Airsoft, WE Tech (WE Airsoft), Lancer Tactical Inc., CYMA International Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |