Quick Navigation

Report Overview

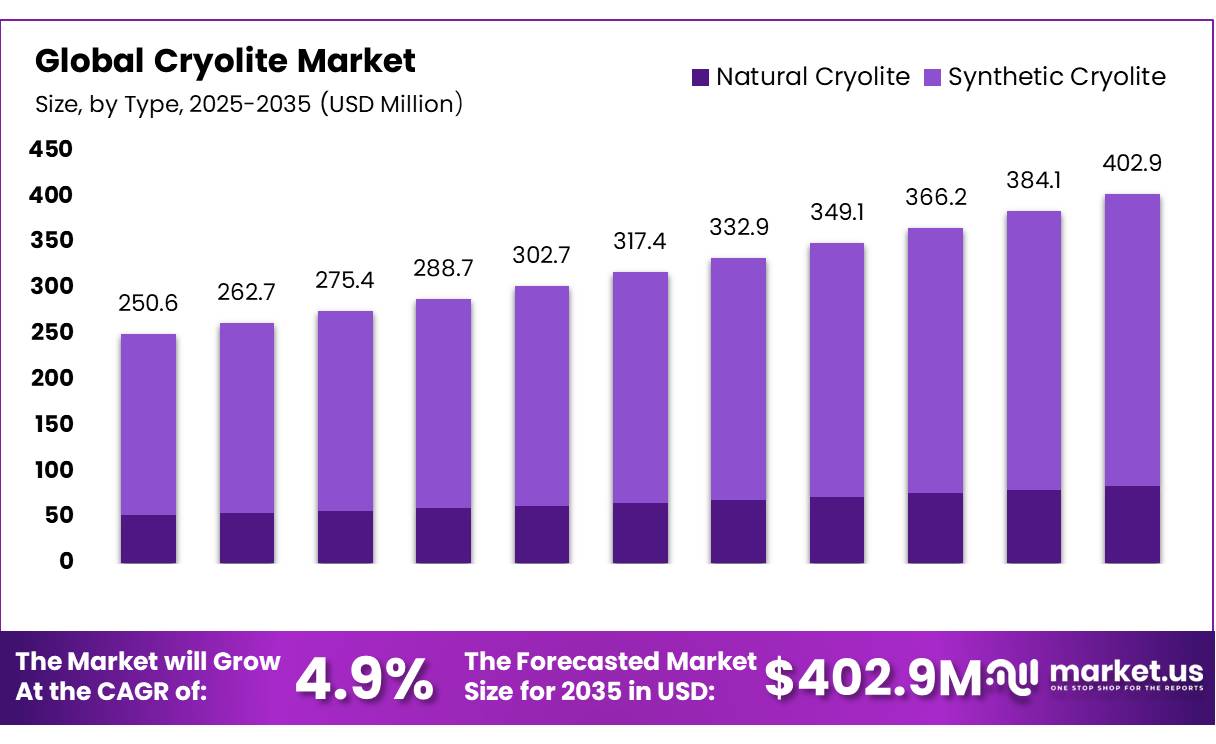

In 2025, the Global Cryolite Market was valued at US$250.6 million, and between 2026 and 2035, this market is estimated to register a CAGR of 4.9 %, reaching about US$402.9 million by 2035.

Cryolite is an inorganic fluoride compound, chemically identified as sodium hexafluoroaluminate, with the formula Na3AlF6, CAS (Chemical Abstracts Service Registry Number) number 15096-52-3, and molecular weight of 209.94 g/mol. Natural cryolite is rare, so industrial demand is mainly served by synthetic grades manufactured for controlled purity, particle size, and flux performance.

- The U.S. Geological Survey estimated global primary aluminium production at 74 million metric tons in 2025, compared with 72.8 million metric tons in 2024. In the United States, transportation represented 36% of aluminium consumption, followed by packaging at 24%, building at 13%, electrical uses at 9%, and consumer durables and machinery at 8% each. This broad downstream structure supports continued demand for smelting fluxes and processing chemicals.

- The International Aluminium Institute expects total aluminium demand to rise from 86.2 million metric tons in 2020 to 119.5 million metric tons by 2030, requiring 33.3 million additional metric tons.

Key Takeaways

- The global cryolite market was valued at USD 250.6 million in 2025.

- The global market is projected to grow at a CAGR of 4.9% and is estimated to reach USD 402.9 million by 2035.

- Based on the type, the synthetic dominated the cryolite market, with a substantial market share of around 79.2%.

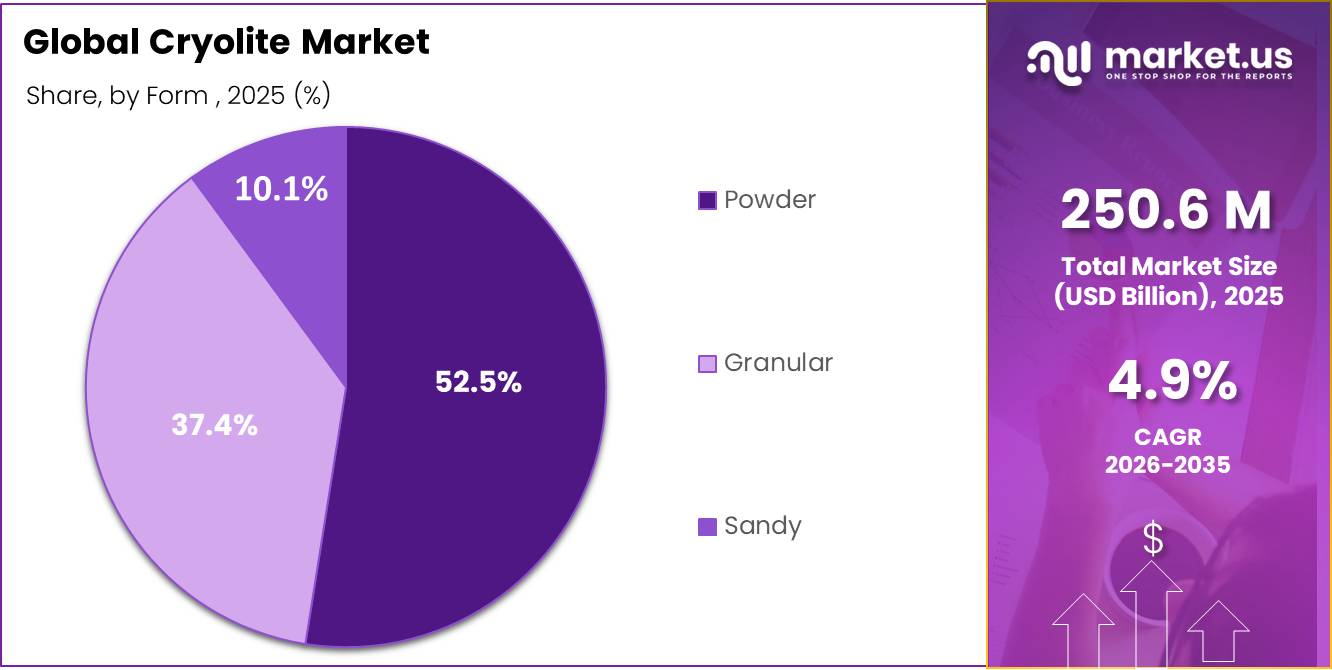

- Based on the form, powder form led the market, comprising 52.5% of the total market.

- Among the application, the aluminium smelting held a major share in the cryolite market, 75.3% of the market share.

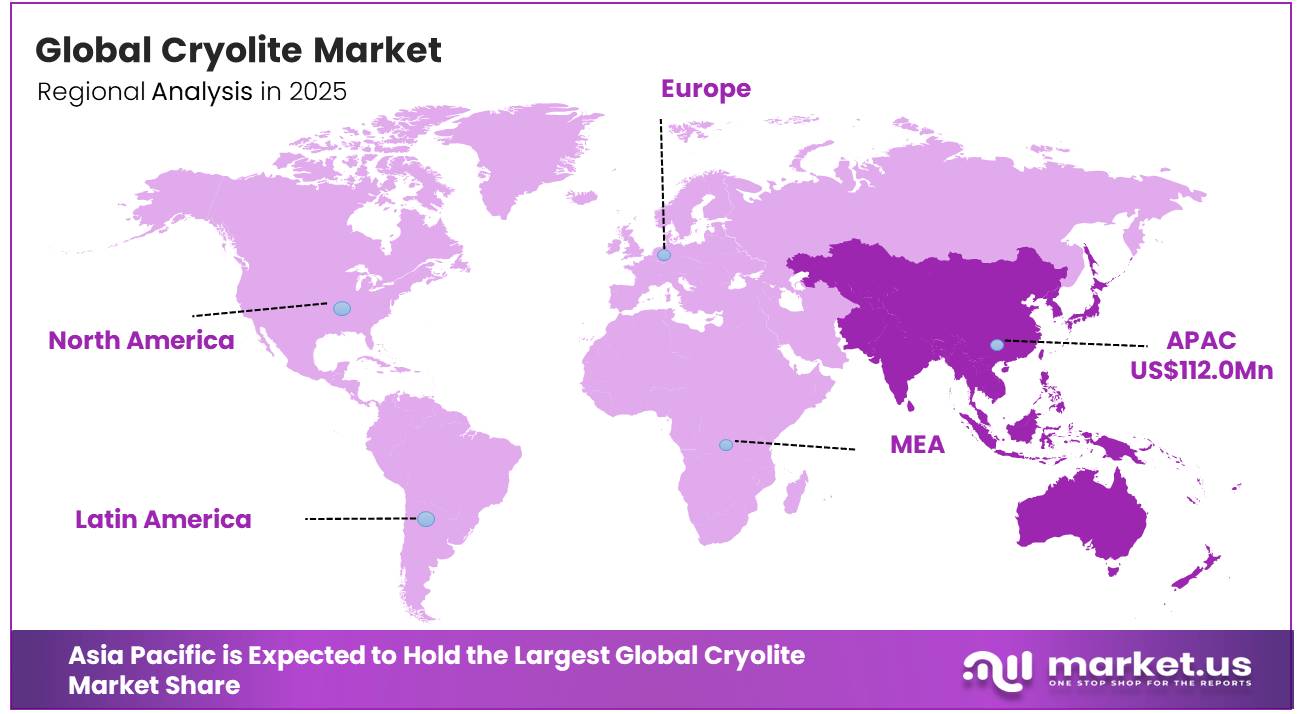

- In 2025, the Asia Pacific was the most dominant region in the cryolite market, accounting for 44.7% of the total global consumption.

Future opportunities will emerge from low-carbon smelting, improved electrolyte management, recycling-compatible flux systems, and higher-purity synthetic cryolite. In January 2025, the U.S. Department of Energy awarded USD 10 million for Phase 1 of a green aluminium smelter project, with federal support potentially reaching USD 500 million. Such investments can stimulate modern smelting capacity and create demand for efficient, lower-emission cryolite formulations worldwide. Suppliers offering stable chemistry, technical support, and consistent delivery are positioned to benefit from modernization programs.

Cryolite Market Segmentation

Type Analysis

Synthetic Cryolite leads the market due to reliable quality and broad industrial use.

In 2025, Synthetic Cryolite held a dominant market position, capturing more than a 79.2% share. In June 2025, the segment remained widely preferred across aluminium smelting, abrasives, welding materials, glass, and enamel production. Manufacturers rely on synthetic cryolite because it offers controlled purity, stable composition, and consistent performance in high-temperature processes. Its dependable availability also supports large-scale industrial operations where uniform quality is essential.

Natural Cryolite is gaining limited interest in specialised mineral, research, and niche industrial applications. Its rarity restricts large-scale availability, but demand may continue where naturally sourced mineral characteristics are preferred for selected uses by certain specialist industrial buyers.

Form Analysis

Powder leads the Cryolite Market because it supports easy blending and uniform processing.

In 2025,Powder held a dominant market position, capturing more than a 52.5% share. In June 2025, the segment remained used in aluminium smelting, abrasives, glass, enamel, welding materials, and metal treatment. Its fine particle structure allows faster mixing, even dispersion, and controlled dosing during industrial processing. Manufacturers prefer powder cryolite because it can be handled efficiently in production batches and supports consistent performance at high temperatures.

Granular cryolite is gaining attention because it produces less dust during handling, storage, and transportation. Its larger particle size supports cleaner workplace conditions and controlled feeding into industrial equipment. Growing preference for safer material handling and reduced product loss is supporting its wider adoption.

Application Analysis

Aluminium Smelting leads the Cryolite Market due to its essential role in metal production.

In 2025, Aluminium Smelting held a dominant market position, capturing more than a 75.3% share. In June 2025, the segment remained the leading application because cryolite acts as a flux and electrolyte during aluminium production. It helps dissolve alumina, lowers the operating temperature, improves electrical conductivity, and supports smoother metal extraction. Smelters prefer cryolite because it improves process control and maintains stable performance in high-temperature production systems.

Abrasive Production is gaining attention as cryolite improves cutting performance, heat resistance, and surface quality in grinding products. Manufacturers use it in bonded and coated abrasives where controlled friction and cleaner finishing are important. Machining and metalworking activity supports this segment’s expansion.

Key Market Segments

By Type

- Natural Cryolite

- Synthetic Cryolite

By Form

- Powder

- Granular

- Sandy

By Application

- Aluminum Smelting

- Abrasive Production

- Metal Surface Treatment

- Enamel and Glass Frits

- Welding Flux

- Others

Drivers

EV & Energy Transition Aluminium Pull-Through

The International Aluminium Institute forecast, updated in its landmark demand report, projects global aluminium demand to increase by approximately 40% by 2030 from 2020 levels rising from 86.2 million to 119.5 million tonnes with the electrical sector alone requiring an additional 5.2 million tonnes by 2030, driven by solar panel substrate demand, copper-to-aluminium cable substitution in grid infrastructure, and EV drivetrain components.

In the automotive sector specifically, each battery electric vehicle contains 250–500 kg of aluminium for battery enclosures, structural frames, heat management systems, and body panels meaning that the IAI’s forecast of 31.7 million EV units by 2030 translates into an incremental aluminium demand of approximately 30–50 million additional tonnes of primary and secondary aluminium, directly expanding the Hall–Héroult melt throughput and associated cryolite consumption.

The World Bank published in June 2026 that demand from data centres, electric vehicles, and renewable energy is pushing aluminium prices to multi-year highs, while aluminium prices hit a 4-year high in May 2026 on fears of Chinese smelter shutdowns and Middle East supply disruptions a price signal that incentivises capacity expansion in new-energy-smelting hubs and the associated cryolite procurement contracts.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Primary Aluminium Smelting & China’s 45 Mt Cap Structural Tightness | +1.8% | China (55%+ demand), GCC, India, Southeast Asia | Short–Medium (≤ 3 years) |

| EV & Energy Transition Aluminium Pull-Through | +1.4% | North America, EU, China primary; APAC corridors | Medium term (2–4 years) |

| Bonded Abrasives Growth: Cryolite as Flux Filler | +1.0% | Asia-Pacific (55% share), North America aerospace, EU | Medium term (2–4 years) |

| US Section 301 Tariffs Forcing Supply Chain Diversification | +0.7% | North America primary; EU secondary reshoring | Short term (≤ 2 years) |

| Sodium-Ion Battery Emerging Application | +0.5% | China primary; EU, North America early-stage | Long term (≥ 4 years) |

| Agricultural Pesticide & Organic Certification Expansion | +0.4% | North America (California), EU, Australia, South America | Short–Medium (≤ 3 years) |

Restraint

Fluorspar Supply Concentration & Critical Mineral Deficit

The U.S. Department of Energy, in a forecast confirmed as recently as 2024–2025, projects that global demand for fluorspar will exceed current supply by 1–4% by 2025 and by a structurally alarming 40–70% by 2035 a demand-supply gap that is being driven simultaneously by fluorine demand in lithium-ion battery electrolytes, fluoropolymers, refrigerants, and semiconductor etchants competing directly with the synthetic cryolite value chain for the same acidspar feedstock.

The USGS Mineral Commodity Summaries 2026 confirms that the United States is 100% import-dependent for fluorspar, with no domestic fluorspar mine in commercial operation and with approximately 70–75% of imported fluorspar directed toward HF production the upstream precursor in every synthetic cryolite manufacturing route, including both the HF-alumina hydrate-soda ash route and the sodium fluorosilicate-soda ash route.

For cryolite producers in North America and Europe, this feedstock deficit creates structural long-lead-time supply insecurity: new fluorspar mining projects in Canada, Kenya, and Namibia carry 5–10 year development timelines, meaning that no material supply diversification will materialise before 2030 at the earliest, and the projected 40–70% demand-supply gap by 2035 will maintain a structural pricing premium on HF the immediate precursor to synthetic cryolite that cannot be passed through entirely to aluminium smelter buyers operating under their own cost pressure from LME aluminium price ceilings.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluorspar Supply Concentration & Critical Mineral Deficit | -1.5% | North America, EU primary; APAC secondary | Long term (≥ 4 years) |

| HF Price Volatility & Pass-Through Margin Compression | -1.3% | EU, North America primary; APAC secondary | Short–Medium (≤ 3 years) |

| China Demand Concentration & Geopolitical Single-Point Risk | -1.0% | China core; global demand correlation risk | Medium term (2–4 years) |

| Environmental & Fluoride Emission Compliance Escalation | -0.8% | North America, EU regulatory hubs; Australia | Medium term (2–4 years) |

| Agricultural MRL Tightening: Fluoride Residue Risk | -0.5% | EU primary; North America secondary | Short–Medium (≤ 3 years) |

| AlF₃ Substitution Pressure in Bath Chemistry | -0.4% | Global; most acute at APAC greenfield smelters | Long term (≥ 4 years) |

Opportunity

Waste Cryolite Closed-Loop Recovery as Commercial Revenue Stream

The scientific validation for commercial recovery has advanced materially in 2025–2026: a January 2025 ACS Sustainable Chemistry & Engineering study, authored by a team including MIT and Nitto Denko researchers, demonstrated a nanofiltration membrane approach that blocks 99.7% of aluminium ions from waste cryolite electrolyte while allowing monovalent sodium, lithium, and potassium ions to permeate — achieving a sodium/aluminium separation factor of 102.02 at optimal pH, with module-scale analysis confirming a viable sodium/aluminium ratio of approximately 2.6 in the retentate stream, ready for upcycling as recovered cryolite electrolyte.

A complementary June 2025 PubMed study by Chinese researchers presents a two-step leaching and alkalisation method achieving 85.6% fluorine recovery and 83.6% lithium recovery from waste cryolite under optimal conditions, producing aluminium fluoride hydroxy hydrate (AFHH) that can be re-injected into electrolytic cells as a bath chemistry supplement — a circular product that closes the loop without requiring new HF synthesis.

The white space being identified here is the commercialisation of these technologies as a licensed service or tolling model offered by speciality fluoride producers to smelters: by acquiring waste bath at near-zero or negative cost, recovering fluoride and aluminium value at processing costs of approximately USD 40–65/tonne, and reselling recovered AlF₃/cryolite to smelters at a 15–20% discount to virgin-grade spot prices, a circular business model generating 40%+ gross margins becomes structurally viable — representing a TAM of USD 80–225 million in waste processing liability-to-revenue conversion across the global smelting base that does not exist in any consensus cryolite market forecast.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Waste Cryolite Closed-Loop Recovery | +1.6% | China (primary smelter base), EU pilot hubs, North America | Medium term (2–4 years) |

| Indonesia Greenfield Smelting: First-Mover Contracting | +1.3% | Indonesia (Kalimantan, Bintan SEZ); Southeast Asia | Short–Medium (≤ 3 years) |

| Upstream Vertical Integration into Fluorspar/HF | +1.1% | North America, EU; GCC FTA partners | Medium–Long (2–5 years) |

| Battery-Grade Ultra-High-Purity Cryolite for Solid-State Na | +0.9% | China (CATL/BYD), EU, North America R&D pipeline | Long term (≥ 4 years) |

| Domestic US Production under Critical Minerals Mandates | +0.7% | North America (US primary); US FTA partners | Medium term (2–4 years) |

| Optical-Coating & Advanced Ceramics Grade Monetisation | +0.5% | North America (defence optics), EU, Japan, South Korea | Long term (≥ 4 years) |

Challenges

Real-Time Bath Chemistry Control Latency

The root structural vulnerability in the cryolite consumption economics of aluminium smelting is the persistent latency gap between bath chemistry events and actionable measurement data: in the conventional potline control paradigm still the dominant practice at more than 80% of global smelting facilities in 2026 operators collect a physical bath sample, perform laboratory XRF or titration analysis, and receive a cryolite ratio (CR) result 3–6 hours after the bath event that triggered the anomaly, during which time the cell may be operating at a CR outside the target range of 2.0–2.4, causing excess fluoride vaporisation losses, reduced alumina solubility, or anode effect events that drive unplanned AlF₃ and soda ash additions to re-establish bath stability.

STAS Inc., a global potroom instrumentation company, published technical analysis confirming that this latency results in smelters routinely adding 5–10% more cryolite bath material per campaign than the stoichiometric minimum requirement conservatively equivalent to a USD 3–6 per tonne of aluminium produced in avoidable fluoride input cost, and across a global primary production base of approximately 75 million tonnes in 2026, a systemic overconsumption drag of approximately 75,000–150,000 tonnes of synthetic cryolite annually above technically optimal consumption levels.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Real-Time Bath Chemistry Control Latency | -1.3% | Global; most acute in APAC new builds, GCC, Africa | Medium term (2–4 years) |

| China Export Control Ambiguity on Fluorides | -1.1% | North America, EU, Japan, South Korea import dependency | Short–Medium (≤ 3 years) |

| EU Energy Cost Competitiveness Erosion | -1.0% | EU-27 primary; UK secondary | Long term (≥ 4 years) |

| Fluoride Chemistry Talent Pipeline Attrition | -0.8% | North America, EU, Japan primary; APAC secondary | Long term (≥ 4 years) |

| Hazardous Cargo Compliance & Logistics Cost Inflation | -0.6% | Global; most acute in EU, North America regulatory hubs | Medium term (2–4 years) |

| PFAS Restriction Spillover to Fluoride Processing | -0.5% | EU primary; UK, Australia secondary | Medium term (2–4 years) |

Geopolitical Impact analysis

Fluorspar Concentration and Trade Dependence Reshaping Cryolite Supply Chains

Current geopolitical conditions are reshaping the cryolite market through concentrated fluorspar production, import dependence, mining restrictions, and regional raw-material security policies. Synthetic cryolite production depends on fluorine-bearing feedstocks, making changes in fluorspar availability directly relevant to manufacturing costs, procurement schedules, and plant operating decisions.

Global fluorspar mine production declined by 1% to approximately 10 million metric tons in 2025. China produced nearly 6 million metric tons, representing a major concentration within the global supply base. Domestic mining inspections and production suspensions tightened availability, leading China’s fluorspar imports to increase by 48% to 856,000 metric tons during the first half of 2025. Mongolia supplied 86% of these imports, creating an increasingly important cross-border supply corridor.

Import exposure is also significant in North America. The United States remained 100% net import reliant for fluorspar in 2025 and imported approximately 21,000 metric tons of cryolite. The absence of a government fluorspar stockpile increases sensitivity to trade interruptions, shipping delays, border restrictions, and supplier concentration.

Governments are responding through diversification and domestic-capacity initiatives. The European Union classifies fluorspar as a critical raw material and aims to meet 10% of annual strategic-material consumption through domestic extraction, 40% through regional processing, and 25% through recycling by 2030. Meanwhile, a Canadian fluorspar operation restarted shipments with planned annual output of 200,000 metric tons.

Regional Analysis

In 2025, Asia Pacific dominated the Cryolite Market with a 44.7% share, valued at USD 112.02 million. The region’s leadership is supported by its aluminium-smelting base, expanding non-ferrous metal output, and established fluoride-chemical supply networks. China’s National Bureau of Statistics reported that primary aluminium production reached 45.02 million tonnes in 2025, increasing 2.4% from the previous year, which sustained strong consumption of cryolite as an electrolyte and flux.

Regional alumina availability also reinforces smelter activity. The International Aluminium Institute recorded March 2026 alumina production of 7.53 million tonnes in China and 1.358 million tonnes in Oceania. Producers across the region benefit from integrated mineral processing, industrial clusters, and proximity to aluminium manufacturers. Demand is further supported by abrasive, welding, glass, and enamel production. Regional investment in efficient smelting technologies and cleaner process materials is expected to strengthen Asia Pacific’s position while creating opportunities for higher-purity synthetic and granular cryolite grades.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global cryolite market is a fragmented competitive landscape in which no single player has dominant control over the entire market. A diverse mix of multinational chemical corporations, specialist fluoride companies, and regional manufacturers are actively competing to meet the aluminum industry’s growing demand. Product purity, production capacity, supply reliability, pricing strategies, and the strength of collaborative relationships with aluminum smelters all have an impact on competition among these companies.

Within this fragmented market, synthetic cryolite has emerged as the largest and most strategically important segment, prompting key players to invest heavily in advanced chemical process technologies and develop robust raw material sourcing strategies. To remain cost competitive, major market participants have shifted their primary focus to increasing production capacity while also developing energy-efficient manufacturing processes.

Market Key Players

- Solvay

- Fluorsid

- B.Chemicals

- Sanyo Corporation of America

- Eclipse Metals Ltd.

- Henan Jinhe Industry Co., Ltd

- American Elements

- Harshil Industries

- Skyline Chemical Corporation

- DO-FLUORIDE NEW ENERGY TECHNOLOGY CO.LTD

- Other Key Players

Key Development

- In June 2026, Eclipse Metals Ltd. confirmed fluorite and other critical minerals at the Ivigtut Mine in Greenland. The update advanced the assessment of its critical-mineral project, which includes the historic Ivigtut cryolite-polymetallic deposit.

- In October 2025, Fluorsid reported further progress on its EU-supported LIFE SYNFLUOR project developed with Pirelli. The project uses hexafluorosilicic acid from fertilizer production to create synthetic calcium fluoride and precipitated silica, supporting circular fluorochemical production.

- In September 2025, Solvay announced a restructuring of its Bad Wimpfen chemical facility in Germany. The company planned to discontinue selected trifluoroacetic-acid products by early 2026 and gradually cease hydrogen fluoride production at the site by the end of 2026.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 250.6 Mn |

| Forecast Revenue (2035) | USD 402.9 Mn |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Natural Cryolite and Synthetic Cryolite), By Form (Powder, Granular, and Sandy), By Application (Aluminium Smelting, Abrasive Production, Metal Surface Treatment, Enamel and Glass Frits, Welding Flux, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Solvay, Fluorsid, S.B. Chemicals, Sanyo Corporation of America, Eclipse Metals Ltd., Henan Jinhe Industry Co., Ltd., American Elements, Harshil Industries, Skyline Chemical Corporation, Do-Fluoride New Energy Technology Co., Ltd., and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |