Quick Navigation

Report Overview

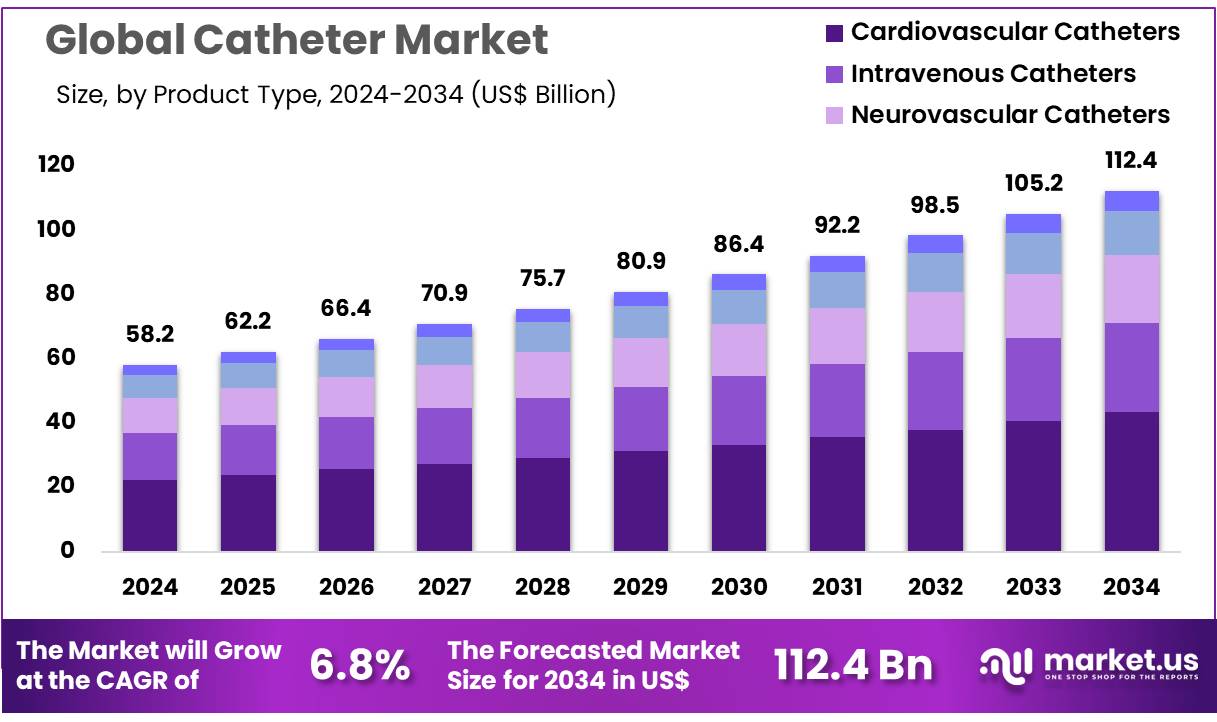

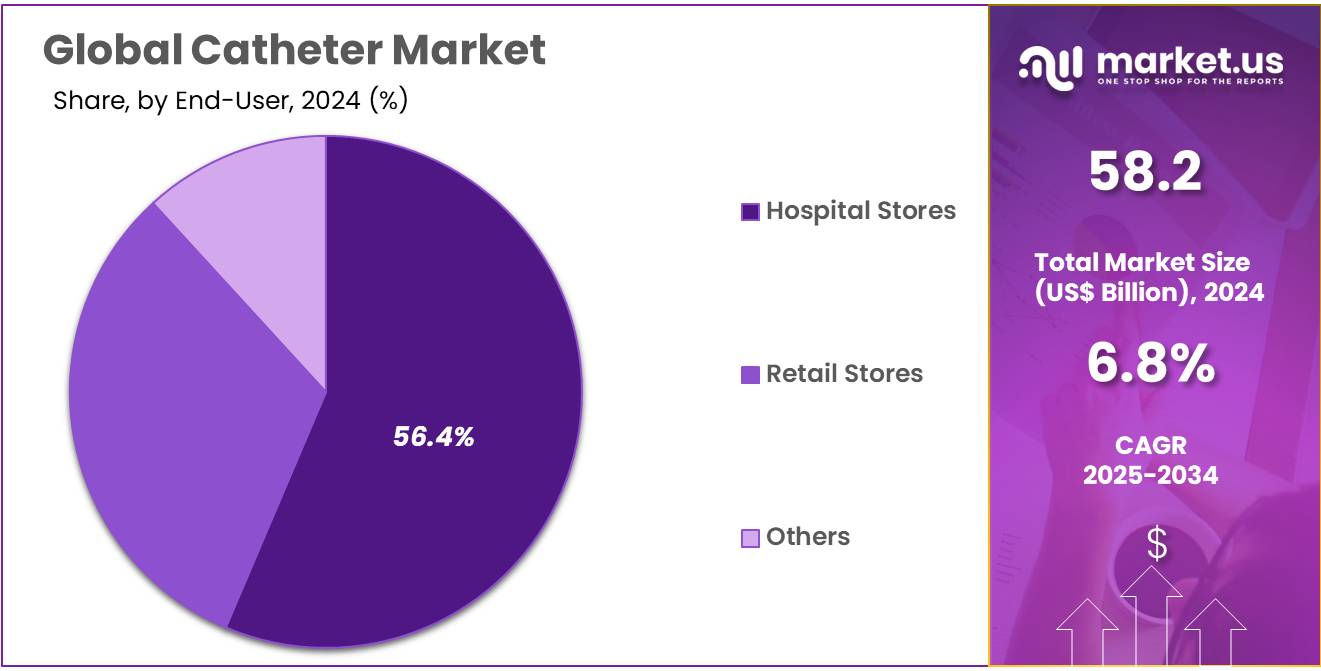

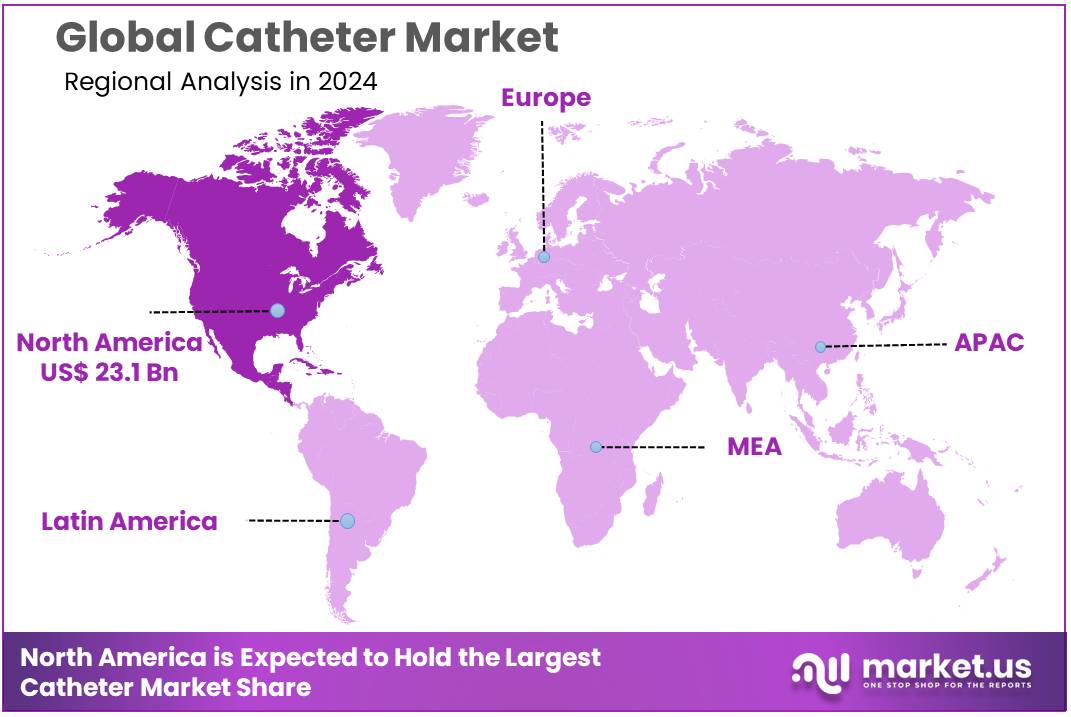

Global Catheter Market size is expected to be worth around US$ 112.4 billion by 2034 from US$ 58.2 billion in 2024, growing at a CAGR of 6.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.7% share with a revenue of US$ 23.1 Billion.

Increasing demand for advanced medical devices to support long-term patient care is driving growth in the catheter market. The rising prevalence of chronic diseases, including cardiovascular disorders, kidney diseases, and urinary incontinence, is fueling the need for specialized catheter solutions across various medical applications. The growing number of surgical procedures, coupled with an aging population requiring continuous medical intervention, is further accelerating market expansion.

In October 2023, the U.S. FDA granted approval for the Orchid SRV safety release valve, a device developed by Linear Health Sciences to enhance IV catheter durability. Designed for universal IV access applications, the valve helps prevent catheter rupture and reduces the frequency of device replacements in clinical settings. The increasing adoption of antimicrobial-coated and drug-eluting catheters is reducing infection risks and improving patient safety.

Technological advancements, including sensor-integrated smart catheters, are transforming disease monitoring and treatment precision. The growing shift toward minimally invasive procedures is boosting demand for interventional catheters in cardiac and neurovascular applications. Rising healthcare expenditures and the expansion of ambulatory care services are creating significant opportunities for catheter manufacturers to introduce cost-effective and patient-friendly solutions.

The increasing use of Foley catheters in long-term urinary management is strengthening the market’s growth trajectory. Enhanced material innovations, such as silicone and hydrogel-coated catheters, are improving biocompatibility and patient comfort. The adoption of disposable and single-use catheters is minimizing the risk of hospital-acquired infections and improving procedural efficiency.

The integration of robotic-assisted catheter placement systems is enhancing precision in complex medical interventions. The expanding role of catheters in dialysis procedures is addressing the growing burden of kidney-related disorders. As medical technology advances and healthcare providers prioritize infection control and efficiency, the catheter market is expected to witness sustained growth in the coming years.

Key Takeaways

- In 2024, the market for catheter generated a revenue of US$ 58.2 billion, with a CAGR of 6.8%, and is expected to reach US$ 112.4 billion by the year 2033.

- The product type segment is divided into cardiovascular catheters, intravenous catheters, neurovascular catheters, urology catheters, specialty catheters, with cardiovascular catheters taking the lead in 2023 with a market share of 38.6%.

- Considering end-user, the market is divided into hospital stores, retail stores, others. Among these, hospital stores held a significant share of 54.4%.

- North America led the market by securing a market share of 39.7% in 2023.

Product Type Analysis

The cardiovascular catheters segment led in 2023, claiming a market share of 38.6% owing to the rising prevalence of cardiovascular diseases (CVDs) worldwide. Cardiovascular catheters are used in a variety of procedures, such as coronary angiography, angioplasty, and stent placement, which are essential for diagnosing and treating heart conditions. The increasing global incidence of heart disease, along with the growing adoption of minimally invasive surgeries, is anticipated to drive demand for cardiovascular catheters.

Furthermore, technological advancements in catheter design, including innovations aimed at improving precision, flexibility, and patient comfort, are projected to contribute to the growth of this segment. The expanding aging population, particularly those at higher risk of CVDs, is also likely to support the increasing use of cardiovascular catheters in medical treatments.

End-user Analysis

The hospital stores held a significant share of 56.4% due to the increasing reliance on healthcare facilities for purchasing medical supplies. Hospital stores play a critical role in the procurement, distribution, and management of medical devices, including catheters. With rising patient volumes, particularly in hospitals treating chronic conditions and conducting surgeries, the demand for catheters is expected to rise.

Additionally, the growing trend of hospitals favoring in-house procurement to maintain inventory control and reduce costs is anticipated to drive market growth. As hospitals continue to adopt more specialized catheter products to meet diverse patient needs, the hospital stores segment is likely to see steady growth. Moreover, hospital-centric purchasing channels provide a streamlined approach to maintaining medical supplies, which further boosts the segment’s demand.

Key Market Segments

Product Type

- Cardiovascular Catheters

- Electrophysiology Catheters

- PTCA Balloon Catheters

- PTA Balloon Catheters

- IVUS Catheters

- Intravenous Catheters

- Peripheral Catheters

- Midline Peripheral Catheters

- Central Venous Catheters

- Neurovascular Catheters

- Urology Catheters

- Hemodialysis Catheters

- Peritoneal Catheters

- Intermittent Catheters

- Foley Catheters

- External Catheters

- Specialty Catheters

- Wound/Surgical Catheters

- Thermodilution Catheters

- Oximetry Catheters

- IUI Catheters

End-user

- Hospital Stores

- Retail Stores

- Others

Drivers

Rising Prevalence of Neurological Conditions Driving the Catheter Market

Increasing neurological disorders are anticipated to drive the demand for catheters, particularly in patients experiencing mobility impairments and neurogenic bladder dysfunction. In 2023, a study published by the National Library of Medicine revealed that nearly one in seven people globally experience neurological conditions, significantly affecting mobility, cognition, and overall quality of life. The rising prevalence of these disorders highlights the urgent need for innovative treatment approaches and improved access to neurological care.

Many individuals suffering from conditions such as multiple sclerosis, Parkinson’s disease, and spinal cord injuries require urinary catheters for bladder management. Healthcare providers are increasingly adopting intermittent catheterization to minimize infection risks and improve patient comfort. The introduction of antimicrobial and hydrophilic-coated catheters is reducing catheter-associated complications.

Growing investments in neurorehabilitation programs are expanding catheter accessibility for patients with chronic neurological impairments. Medical device manufacturers are prioritizing the development of user-friendly catheter systems designed for at-home use. Increased awareness about catheter-related infections is encouraging hospitals to adopt advanced drainage systems.

Research in neuromodulation therapies is supporting the integration of catheters into minimally invasive procedures. As the aging population grows, neurological disorders are expected to rise, further increasing the need for catheterization solutions. The expansion of rehabilitation centers specializing in neurological care is also fostering market growth.

Restraints

Risk of Catheter-Associated Infections

Growing concerns over catheter-associated infections are expected to restrain market growth, particularly in hospital settings. Catheter-associated urinary tract infections (CAUTIs) account for nearly 75% of all hospital-acquired UTIs, increasing patient morbidity and healthcare costs. Prolonged catheter use often leads to bacterial colonization, resulting in complications such as sepsis and bladder inflammation. Biofilm formation on indwelling catheters further exacerbates infection risks, making treatment more challenging.

Antibiotic-resistant pathogens contribute to rising concerns over catheter-related bloodstream infections (CRBSIs). Healthcare facilities must implement stringent infection control protocols, increasing operational complexity and costs.

The need for frequent catheter replacements due to contamination and blockage raises expenses for both patients and hospitals. While advancements in antimicrobial coatings and closed catheter systems aim to address these concerns, infection risks remain a critical challenge in widespread catheter adoption.

Opportunities

Rising Urological Disorders Creating Opportunities in the Catheter Market

Increasing cases of urological conditions are expected to create significant growth opportunities in the catheter industry. According to the World Health Organization, urological disorders now affect over 200 million individuals worldwide, with nearly 25 million cases recorded in the U.S. alone. Women account for the majority of these cases, making up approximately 80% of the affected population, emphasizing the growing need for specialized urological treatments and early intervention strategies.

Conditions such as urinary incontinence, benign prostatic hyperplasia (BPH), and kidney diseases are driving demand for advanced catheterization techniques. The adoption of self-catheterization is increasing, particularly among individuals with chronic bladder dysfunction. Growing awareness about minimally invasive treatments is promoting the use of single-use and hydrophilic-coated catheters. Innovations in catheter design, including silicone-based and antimicrobial-coated variants, are enhancing patient safety and reducing infection risks.

The expansion of home healthcare services is further boosting the accessibility of catheterization solutions. Healthcare providers are prioritizing early diagnosis and treatment of urological conditions, encouraging faster catheter adoption. Increased investments in urology research are supporting the development of next-generation catheters with improved comfort and efficiency. As the prevalence of urological diseases continues to rise, the catheter market is projected to experience steady growth in the coming years.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the catheter market. On the positive side, the growing demand for minimally invasive procedures, driven by the increasing prevalence of chronic diseases such as cardiovascular conditions and diabetes, fosters market growth. Governments’ emphasis on improving healthcare access, particularly in emerging economies, boosts demand for affordable, high-quality medical devices, including catheters.

Furthermore, healthcare investments in advanced technologies and infrastructure development present new opportunities for catheter manufacturers. However, economic downturns and budgetary constraints in healthcare systems could limit investment in medical devices. Geopolitical tensions and trade restrictions may disrupt supply chains, leading to delays and increased production costs.

Additionally, regulatory hurdles across various regions can slow down market entry for new catheter technologies. Despite these challenges, the ongoing demand for innovative catheter solutions and the rising focus on patient-centric care continue to drive the market forward, ensuring long-term growth.

Latest Trends

Surge in Government Approvals Driving the Catheter Market

The surge in government approvals is a recent trend significantly driving the catheter market. High demand for advanced medical devices has led to an increase in regulatory approvals for innovative catheter products that enhance treatment outcomes. Rising healthcare regulations and industry standards have prompted manufacturers to seek timely approvals for their devices, fueling the market’s growth.

The growing focus on improving healthcare systems and procedural efficiency is expected to lead to more government-backed initiatives and regulatory clearances for advanced catheter technologies. This trend is likely to accelerate the adoption of catheters across various healthcare settings, including hospitals, surgical centers, and specialized clinics.

In February 2023, Teleflex Incorporated announced that its Triumph Catheter had received 510(k) clearance from the U.S. FDA. Engineered for precise wire control and superior visualization, the catheter aims to improve procedural efficiency. Additionally, the company confirmed the first successful clinical use of its GuideLiner Coast Catheter at the UW Medicine Heart Institute in Seattle, marking a milestone in interventional cardiology. The continuous rise in regulatory approvals for such devices will likely foster growth in the catheter market.

Regional Analysis

North America is leading the Catheter Market

North America dominated the market with the highest revenue share of 39.7% owing to the rising prevalence of cardiovascular diseases and advancements in minimally invasive procedures. The American College of Cardiology reported in July 2023 that over 12 million individuals in the United States are living with peripheral artery disease (PAD), highlighting the increasing need for catheter-based interventions.

The growing incidence of heart arrhythmias, coronary blockages, and congenital heart defects further fueled demand for advanced vascular access solutions. Technological advancements, such as drug-coated and bioresorbable catheters, improved patient outcomes and reduced procedure-related complications. The expanding geriatric population, which is more susceptible to cardiovascular disorders, contributed to higher adoption rates of interventional cardiology devices.

Strong investments in research and development by medical device companies led to the introduction of next-generation products with enhanced flexibility and precision. Additionally, government initiatives promoting early diagnosis and improved reimbursement policies for catheter-based treatments supported market expansion across the U.S. and Canada.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to increasing healthcare investments and rising cardiovascular disease prevalence. Expanding healthcare infrastructure in countries like China, India, and Japan is expected to improve access to advanced medical procedures. Government initiatives aimed at enhancing early disease detection and preventive care are likely to encourage the adoption of minimally invasive treatments.

Collaborations between international manufacturers and regional healthcare providers are projected to improve affordability and availability of innovative vascular solutions. The rising burden of lifestyle-related conditions, including diabetes and hypertension, is anticipated to further drive demand for precision-engineered cardiovascular tools.

Increasing adoption of robotic-assisted and AI-powered interventional procedures is expected to enhance surgical accuracy and patient outcomes. Additionally, medical tourism in Asia Pacific, particularly in countries offering cost-effective yet high-quality cardiac care, is likely to support market growth in the coming years.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the catheter market focus on developing advanced materials, antimicrobial coatings, and minimally invasive designs to enhance patient safety and comfort. Companies invest in research and development to introduce smart catheters with real-time monitoring capabilities for improved disease management.

Strategic partnerships with hospitals and healthcare providers help expand product adoption and improve accessibility. Geographic expansion into regions with increasing demand for urinary, cardiovascular, and intravenous catheters supports further market growth. Many players also emphasize cost-effective and eco-friendly solutions to align with sustainability and healthcare affordability.

Boston Scientific is a leading company in this market, offering innovative catheter solutions such as the Polaris and Watchman systems for cardiovascular procedures. The company focuses on continuous technological advancements and strong collaborations with healthcare institutions to improve patient outcomes. Boston Scientific’s commitment to quality, innovation, and expanding global healthcare access establishes it as a key player in the industry.

Top Key Players

- Teleflex Incorporated

- Medtronic

- Hollister Incorporated

- Cure Medical LLC

- Cook Medical

- ConvaTec Group Plc

- BD

- Braun

Recent Developments

- In January 2024, Cook Medical unveiled its latest hydrophilic catheter, the Slip-Cath Beacon Tip, now available in both the U.S. and Canada. Specially designed for a wide range of vascular and non-vascular procedures, this catheter incorporates advanced coating technology to improve maneuverability and precision in complex medical interventions.

- In October 2023, B. Braun unveiled the Introcan Safety 2 IV Catheter, incorporating multi-access blood control technology. This next-generation catheter is designed to minimize exposure risks for healthcare professionals while improving patient safety during intravenous procedures.

- In May 2023, BD introduced an advanced prefilled flush syringe, the BD PosiFlush SafeScrub, aimed at enhancing efficiency in IV catheter care. Designed to streamline the catheter flushing and disinfection process, the syringe reduces contamination risks while improving overall patient safety in hospital and clinical settings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 58.2 billion |

| Forecast Revenue (2034) | US$ 112.4 billion |

| CAGR (2025-2034) | 6.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Cardiovascular Catheters (Electrophysiology Catheters, PTCA Balloon Catheters, PTA Balloon Catheters, IVUS Catheters), Intravenous Catheters (Peripheral Catheters, Midline Peripheral Catheters, Central Venous Catheters), Neurovascular Catheters, Urology Catheters (Hemodialysis Catheters, Peritoneal Catheters, Intermittent Catheters, Foley Catheters, External Catheters), Specialty Catheters (Wound/Surgical Catheters, Thermodilution Catheters, Oximetry Catheters, IUI Catheters)), By End-user (Hospital Stores, Retail Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Teleflex Incorporated, Medtronic, Hollister Incorporated, Cure Medical LLC, Cook Medical, ConvaTec Group Plc, BD, and B. Braun. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |