Global Beverage Cans Market Size, Share, And Industry Analysis Report By Material (Aluminum, Steel), By Product Type (1-piece cans, 2-piece cans, 3-piece cans), By Capacity (Small, Medium, Large), By Application (Carbonated Soft Drinks, Alcoholic Beverages, Fruits & Vegetable Juices, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182195

- Number of Pages: 397

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

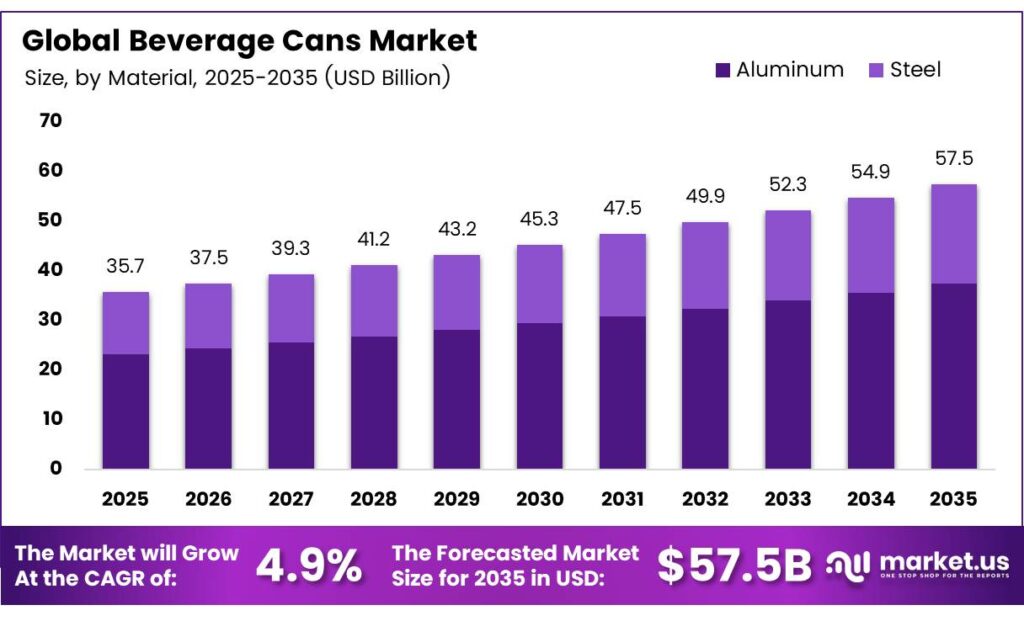

The Global Beverage Cans Market is expected to reach approximately USD 57.5 billion by 2035, up from USD 35.7 billion in 2025, growing at a CAGR of 4.9% over the forecast period 2026 to 2035.

The beverage cans market covers metal containers used to package carbonated soft drinks, alcoholic beverages, juices, energy drinks, and ready-to-drink products. Manufacturers primarily use aluminum and steel to produce these containers at high speed. The market serves both consumer and commercial packaging needs across global retail and food service channels.

Beverage cans offer a strong combination of portability, shelf life, and product protection. Aluminum cans retain carbonation effectively and block light, thereby preserving flavor quality. Consequently, beverage brands across multiple categories continue to choose cans as their preferred primary packaging format for mainstream and premium products alike.

According to the International Aluminium Institute, the global aluminum beverage can recycling rate reached 75% in 2023, demonstrating strong circularity compared to other packaging materials. This high recovery rate lowers production costs for manufacturers and supports the sustainability commitments of major global beverage brands.

Global consumption of aluminum beverage cans reached approximately 180 billion units annually, reflecting robust demand from the beer and soda industries worldwide. Ball Corporation’s South American shipments represented 45% of regional volume within a total market of 43 billion containers in 2024, highlighting the scale of regional demand concentration.

Growth in the global market connects directly to rising urbanization, expanding middle-class populations, and increasing on-the-go consumption habits. Craft beer, RTD cocktails, and functional energy drinks are driving premiumization trends within the beverage can segment. Moreover, brand owners increasingly invest in innovative can designs to differentiate products on competitive retail shelves.

Key Takeaways

- The Global Beverage Cans Market is valued at USD 35.7 billion in 2025 and is projected to reach USD 57.5 billion by 2035 at a CAGR of 4.9% during the forecast period 2026 to 2035.

- Aluminum holds the dominant share at 78.4% of the total beverage cans market.

- The 2-piece cans lead the segment with a 76.5% market share.

- Medium (330ml – 500ml) cans dominate with a 65.1% share.

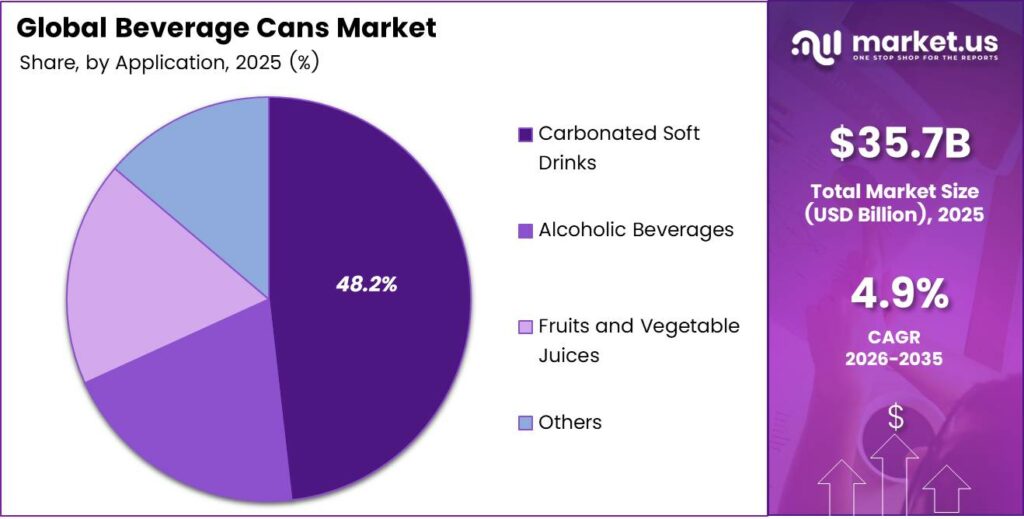

- Carbonated Soft Drinks hold the largest share at 48.2% of total applications.

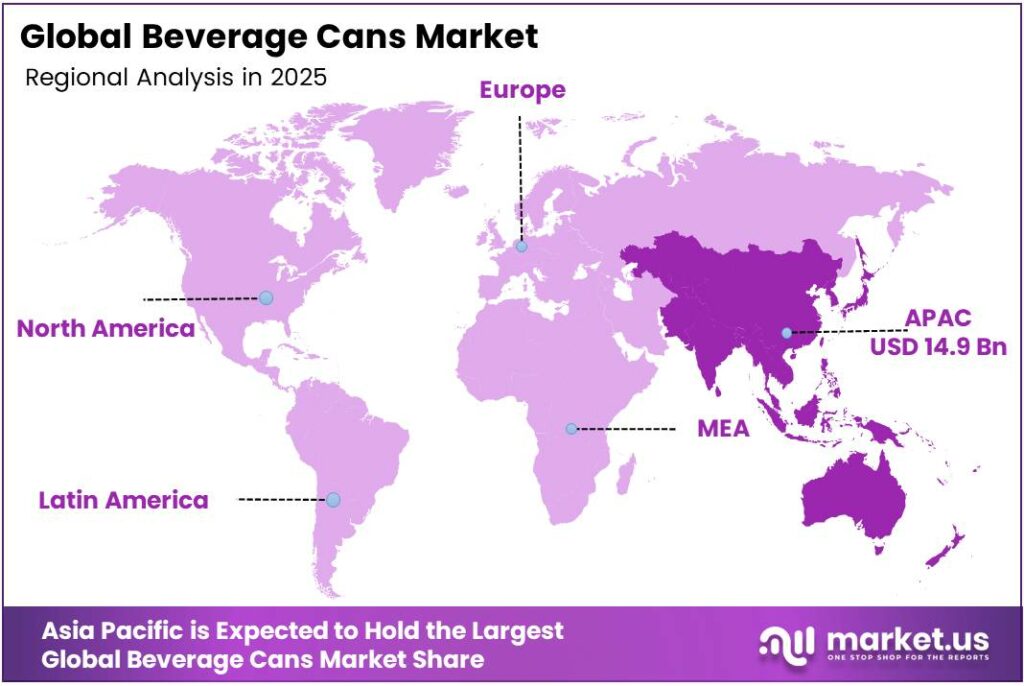

- Asia Pacific leads all regions with a 41.6% market share, valued at USD 14.9 billion.

Material Analysis

Aluminum dominates with 78.4% due to its lightweight properties, infinite recyclability, and widespread brand preference.

In 2025, Aluminum held a dominant market position in the By Material segment of the Beverage Cans Market, with a 78.4% share. Aluminum cans offer superior corrosion resistance, lightweight portability, and full recyclability without quality loss. Additionally, aluminum’s ability to maintain carbonation and block UV light makes it the preferred choice for beverage manufacturers targeting both mainstream and premium product categories.

Steel cans serve specific applications where higher structural strength and pressure resistance are required. Steel performs well in certain industrial beverage formats and maintains relevance in markets where aluminum availability or cost is a constraint. However, steel’s heavier weight and lower recycling rate compared to aluminum limit its broader adoption across modern high-volume beverage packaging supply chains globally.

Product Type Analysis

2-piece cans dominate with 76.5% due to seamless construction, lighter weight, and lower production cost at high volumes.

In 2025, 2-piece cans held a dominant market position in the By Product Type segment of the Beverage Cans Market, with a 76.5% share. These cans are manufactured from a single aluminum sheet drawn and wall-ironed into a seamless body, eliminating side seams. Consequently, 2-piece construction improves structural integrity, reduces material usage, and supports high-speed filling lines favored by large-scale beverage manufacturers worldwide.

1-piece cans represent a smaller but specialized segment used in specific packaging applications. Moreover, 3-piece cans consist of a body and two separate end pieces joined by seams. These remain relevant in markets requiring customized sizes and specialty applications. However, their higher material usage and more complex manufacturing process place them at a cost disadvantage compared to the more efficient 2-piece production method.

Capacity Analysis

Medium (330ml–500ml) cans dominate with 65.1% due to ideal single-serve portioning and universal consumer acceptance.

In 2025, Medium (330ml – 500ml) capacity cans held a dominant market position in the By Capacity segment of the Beverage Cans Market, with a 65.1% share. This size range aligns perfectly with single-serve consumption occasions across carbonated drinks, beer, and energy drink categories. Additionally, medium cans fit standard refrigeration shelving formats, making them the default choice for retail, convenience, and food service channels.

Small (below 330ml) cans serve niche segments including children’s beverages, premium spirits mixers, and portion-controlled health drinks. Furthermore, Large (above 500ml) cans target value-conscious consumers in markets where larger pack sizes offer cost efficiency. However, large cans face regulatory restrictions in some regions regarding single-serve alcohol limits, which moderates their growth potential compared to the dominant medium capacity format.

Application Analysis

Carbonated Soft Drinks dominate with 48.2% due to high consumption frequency and global brand distribution scale.

In 2025, Carbonated Soft Drinks held a dominant market position in the By Application segment of the Beverage Cans Market, with a 48.2% share. Globally recognized beverage brands rely on aluminum cans to maintain carbonation quality and support high-volume retail distribution. Moreover, the convenience and recyclability of cans support consumer preference for soft drinks packaged in metal containers across supermarkets and convenience stores worldwide.

Alcoholic Beverages represent the fastest-growing application, driven by craft beer and RTD cocktail premiumization trends. Fruits and Vegetable Juices increasingly shift toward cans due to superior light and oxygen barrier properties. Additionally, the Others category covers energy drinks, sparkling water, and functional beverages, which are expanding rapidly as health-conscious consumers seek convenient, sustainable packaging formats beyond traditional plastic bottles.

Key Market Segments

By Material

- Aluminum

- Steel

By Product Type

- 1-piece cans

- 2-piece cans

- 3-piece cans

By Capacity

- Small (below 330 ml)

- Medium (330ml – 500ml)

- Large (above 500 ml)

By Application

- Carbonated Soft Drinks

- Alcoholic Beverages

- Fruits and Vegetable Juices

- Others

Emerging Trends

Digital Printing and Hyper-Customization Transform Beverage Can Branding

Beverage brands rapidly adopt digital printing technologies to produce hyper-customized, high-resolution graphics directly on aluminum cans. This capability allows limited-edition seasonal releases and personalized packaging campaigns at a commercial scale. Moreover, digital printing reduces setup costs and lead times significantly. Consequently, brand owners and can manufacturers can collaborate closely to deliver shelf-differentiated products that attract premium consumer segments globally.

Ultra-Thin Can Designs and Smart Coatings Drive Sustainability and Performance

Manufacturers across the industry transition toward ultra-thin, high-strength can designs that reduce material weight and lower logistics carbon footprints. Additionally, advanced internal coating technologies extend flavor preservation and shelf life for sensitive beverages. Collaborative brand-manufacturer initiatives are driving shaped and textured can innovations. Therefore, these developments position the beverage can as a high-performance, environmentally responsible packaging solution for the next decade.

Drivers

Rising RTD Beverage Demand and Recyclability Strengths Fuel Can Market Growth

Global consumer demand for ready-to-drink beverages and on-the-go consumption patterns are accelerating beverage can adoption across all categories. Urban lifestyles and convenience preferences drive higher purchase frequency for canned products. India’s aluminum beverage cans market reached USD 412.1 million in 2023 with a projected annual growth rate of 10.8%, reflecting the scale of emerging market demand expansion.

Aluminum’s Circular Economy Advantage and Premiumization Trends Support Volume Growth

Aluminum cans support strict circular economy mandates through their infinite recyclability, giving brands a strong sustainability narrative. Crown Holdings reported quarterly revenue of USD 2.78 billion in Q1 2024, illustrating the substantial commercial scale of leading can manufacturers responding to growing market demand. Furthermore, premiumization in craft beer, RTD cocktails, and energy drinks expands higher-margin can applications for global packaging suppliers.

Restraints

Aluminum Price Volatility and Raw Material Instability Pressure Manufacturer Margins

Persistent volatility in aluminum coil and raw material pricing creates significant margin pressure for beverage can manufacturers globally. Input cost fluctuations make long-term pricing agreements with customers difficult to maintain. The United States faces a structural aluminum supply gap of approximately 4 million metric tons annually in 2025, impacting raw material availability for the broader beverage can manufacturing sector.

PET Bottle Competition Challenges Beverage Can Adoption in Price-Sensitive Segments

Lightweight PET bottles intensify competition against aluminum cans in price-sensitive beverage segments, particularly in emerging markets. PET packaging offers lower upfront filling costs and consumer familiarity with resealable formats. Therefore, beverage brands operating under tight cost structures often default to PET for mainstream soft drink and juice lines, limiting incremental can volume growth in developing economies where price sensitivity remains a dominant purchase driver.

Growth Factors

Asia-Pacific Emerging Markets and Resealable Smart Can Technologies Open New Revenue Streams

Asia-Pacific emerging markets present untapped expansion potential driven by rising urban populations and growing beverage consumption. Ball Corporation’s total quarterly revenue reached USD 3.34 billion in Q2 2025, representing a 7.8% year-over-year increase, confirming strong demand momentum. Moreover, Ball Corporation’s beverage can shipments increased by 1% in 2024, indicating stable global volume growth despite regional fluctuations.

Recycled Aluminum Supply Chains and Health-Focused Beverage Categories Accelerate Expansion

Brands scale high-recycled content aluminum supply chains to meet aggressive sustainability targets mandated by global retailers and regulators. Resealable and interactive smart can technologies enable premium consumer engagement and differentiation in competitive shelf environments. Additionally, niche formats for sparkling water, health drinks, and functional beverages can diversify revenue streams beyond traditional carbonated soft drink and alcohol categories for manufacturers worldwide.

Regional Analysis

Asia Pacific Dominates the Beverage Cans Market with a Market Share of 41.6%, Valued at USD 14.9 Billion

Asia Pacific leads the global beverage cans market with a 41.6% share, valued at USD 14.9 billion. The region benefits from large and rapidly urbanizing populations in China, India, Japan, and Southeast Asia. Rising disposable incomes and expanding modern retail infrastructure accelerate beverage can consumption. Moreover, regional manufacturing investments and government support for sustainable packaging further strengthen the Asia Pacific’s dominant market position.

North America represents a mature and high-volume beverage can market driven by strong craft beer, energy drink, and carbonated soft drink consumption. The United States leads regional demand, supported by well-established can recycling infrastructure and sustainability mandates. Additionally, premiumization trends in functional beverages and RTD cocktails continue to expand the addressable can market across retail and foodservice channels in the region.

Europe’s beverage can market grows steadily, supported by stringent EU circular economy regulations requiring higher recycled content in aluminum packaging. Deposit-return schemes across Germany, Scandinavia, and the UK achieve high can collection rates and support material recovery. Furthermore, premiumization in craft beer and sparkling water categories drives incremental can volume growth beyond traditional carbonated soft drink applications across European markets.

The Middle East and Africa region shows emerging growth potential for beverage cans, driven by rising energy drink and non-alcoholic beverage consumption. Gulf Cooperation Council countries lead regional adoption due to young demographics and premium beverage preferences. However, limited local manufacturing capacity and infrastructure constraints moderate near-term growth. Consequently, import reliance remains high for most markets across the broader Middle East and African region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ball Corporation stands as one of the largest global beverage can manufacturers, operating across North America, South America, Europe, and the Asia Pacific. The company leads in aluminum can technology, lightweighting innovation, and sustainability-linked supply chain programs. Ball consistently invests in production capacity expansion to serve growing demand across beer, soft drink, energy drink, and RTD beverage categories for major global brand customers.

Ardagh Group S.A. is a leading international packaging manufacturer with significant beverage can operations serving major drink brands across Europe and North America. The company focuses on sustainable aluminum and steel packaging solutions aligned with circular economy targets. Ardagh invests in advanced manufacturing technologies to deliver lightweight, high-quality cans that meet stringent brand specifications and performance requirements for carbonated and non-carbonated beverage applications globally.

Toyo Seikan Co., Ltd. is a Japan-based packaging conglomerate and one of Asia’s largest can manufacturers serving the beverage, food, and industrial packaging sectors. The company develops advanced can technologies, including internal coatings and specialized end designs for the Japanese and broader Asian market. Toyo Seikan maintains a strong position in the premium segment by combining material science expertise with high-precision manufacturing across its integrated production network.

Orora Packaging Australia Pty. Ltd. is a leading packaging manufacturer in the Australasia region, offering aluminum beverage cans and related packaging solutions. The company serves major beverage brands across Australia and New Zealand with domestically manufactured cans. Orora focuses on supply chain reliability, sustainability performance, and product innovation to retain long-term customer relationships in a competitive regional packaging market that demands consistent quality and environmental responsibility.

Top Key Players in the Market

- Ball Corporation

- Ardagh Group S.A.

- Toyo Seikan Co., Ltd.

- Orora Packaging Australia Pty. Ltd.

- CANPACK

- Crown Holdings, Inc.

- Mahmood Saeed Can and End Industry Company Limited (MSCANCO)

- Kian Joo Can Factory Berhad

- SWAN Industries (Thailand) Company Limited

- GZI Industries Limited

Recent Developments

- In December 2025, Ball acquired a majority stake in Benepack’s aluminum beverage can manufacturing businesses in Europe, including two production facilities in Belgium and Hungary. The move strengthens its European footprint and supports growing demand for sustainable aluminum beverage cans.

- In November 2024, Toyo Seikan and UACJ announced the next-generation EcoEnd aluminum beverage can as part of ongoing horizontal recycling efforts (building on their February 2023 alliance to boost recycled content in cans).

Report Scope

Report Features Description Market Value (2025) USD 35.7 Billion Forecast Revenue (2035) USD 57.5 Billion CAGR (2026-2035) 4.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Aluminum, Steel), By Product Type (1-piece cans, 2-piece cans, 3-piece cans), By Capacity (Small (below 330 ml), Medium (330ml – 500ml), Large (above 500 ml)), By Application (Carbonated Soft Drinks, Alcoholic Beverages, Fruits & Vegetable Juices, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Ball Corporation, Ardagh Group S.A., Toyo Seikan Co., Ltd., Orora Packaging Australia Pty. Ltd., CANPACK, Crown Holdings, Inc., Mahmood Saeed Can and End Industry Company Limited (MSCANCO), Kian Joo Can Factory Berhad, SWAN Industries (Thailand) Company Limited, GZI Industries Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Ball Corporation

- Ardagh Group S.A.

- Toyo Seikan Co., Ltd.

- Orora Packaging Australia Pty. Ltd.

- CANPACK

- Crown Holdings, Inc.

- Mahmood Saeed Can and End Industry Company Limited (MSCANCO)

- Kian Joo Can Factory Berhad

- SWAN Industries (Thailand) Company Limited

- GZI Industries Limited

Our Clients

- 182195

- March 2026