Quick Navigation

Report Overview

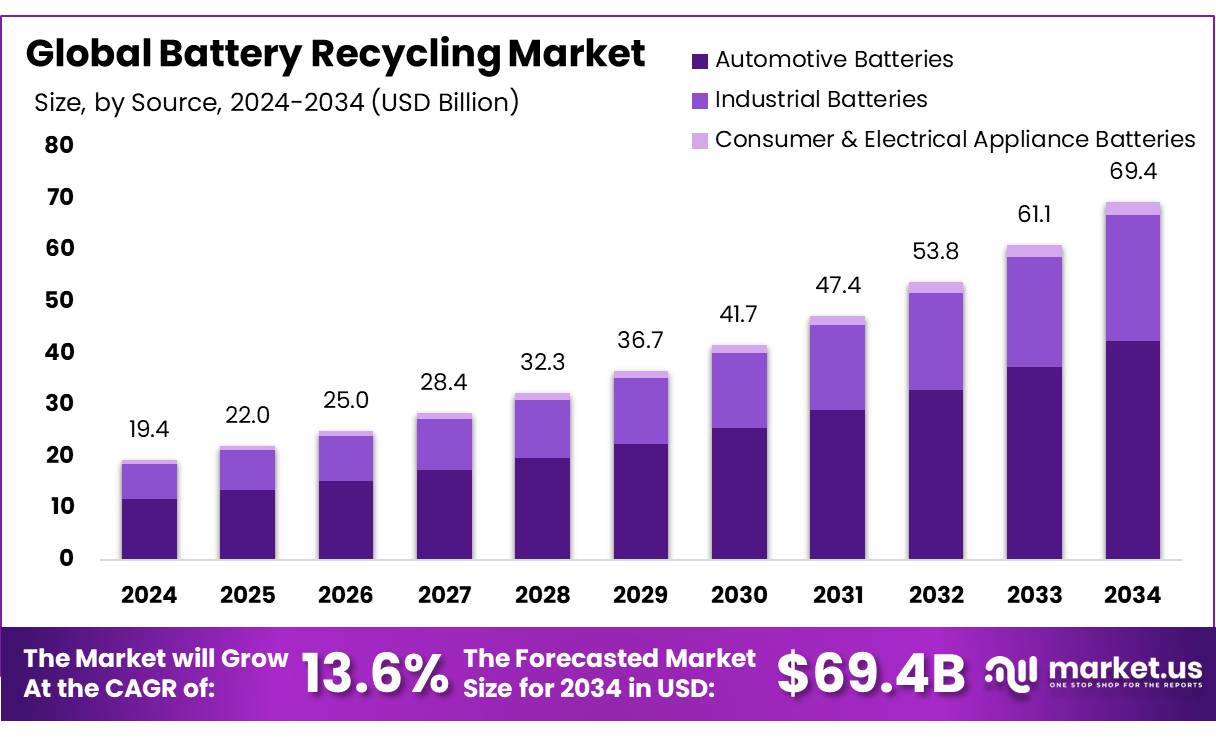

The Global Battery Recycling Market size is expected to be worth around USD 69.4 Billion by 2034, from USD 19.4 Billion in 2024, growing at a CAGR of 13.6% during the forecast period from 2025 to 2034.

Battery recycling involves the recovery of valuable materials, such as nickel, lithium, cobalt, and graphite, from spent batteries to be reused in the production of new batteries or other products. As the demand for batteries increases, especially with the rise of electric vehicles (EVs) and portable electronics like smartphones and laptops, recycling helps reduce the reliance on mining for raw materials, preventing harmful environmental impacts from improper disposal.

The growing use of battery-powered devices, coupled with the rising global population, has made the disposal of these systems even more challenging, as they contain hazardous chemicals and heavy metals that can pollute the environment. Recycling emerges as a powerful solution to reduced carbon emissions, and promoting a sustainable, circular economy. As global battery demand continues to soar, the market for battery recycling is expanding, driven by the need for environmentally friendly solutions and the rising value of recovered materials. This growing market is not only vital for reducing waste but also presents economic opportunities, ensuring a more sustainable future.

- Consumer electronics (CE) accounts for 50% of the global lithium-ion battery market and use 39% of all cobalt in LIBs, driving the need for sustainable recycling to recover valuable materials and reduce environmental impact.

Key Takeaways

- The global battery recycling market was valued at USD 19.4 billion in 2024.

- The global battery recycling market is projected to grow at a CAGR of 13.6 % and is estimated to reach USD 69.4 billion by 2034.

- Among sources, automotive batteries accounted for the largest market share of 61.2%.

- Among battery chemistry, lead-acid accounted for the majority of the market share at 72.1%.

- By technology, pyrometallurgy accounted for the largest market share of 56.2%.

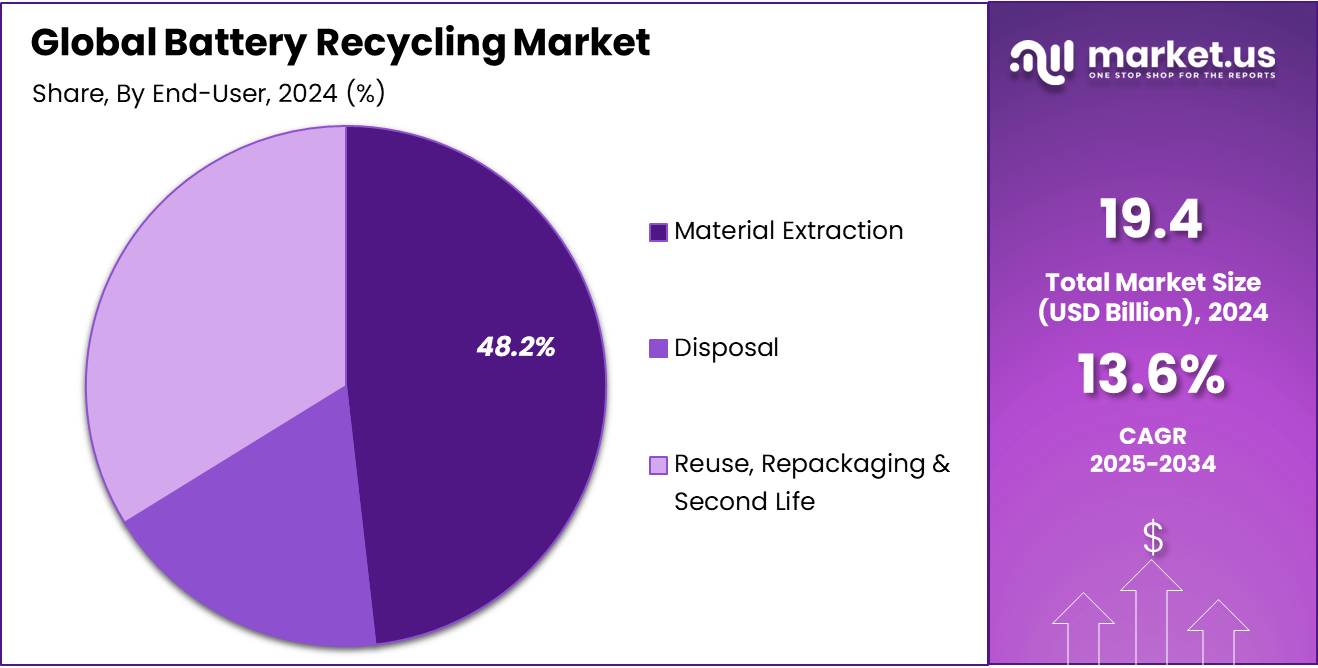

- By end-use, material extraction accounted for the majority of the market share at 48.2%.

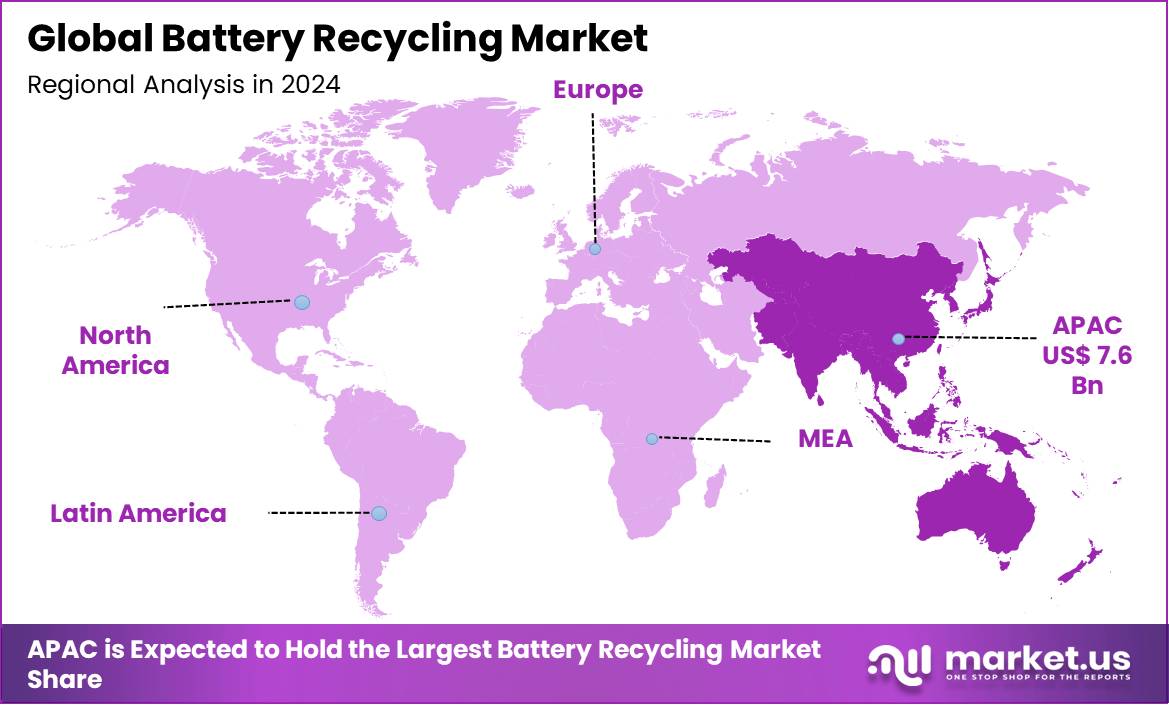

- Asia-Pacific is estimated as the largest market for battery recycling with a share of 39.4% of the market share.

Source Analysis

The Automotive Batteries Segment In the Battery Recycling Market is driven By The Rise In Electric Vehicle Adoption And Stricter Recycling Regulations.

The battery recycling market is segmented based on source into automotive batteries, industrial batteries, and consumer & electrical appliance batteries. In 2024, the Automotive Batteries segment held a significant revenue share of 61.2%. Driven by the growing adoption of electric vehicles (EVs) and the rising volume of end-of-life EV batteries requiring recycling.

Additionally, stringent government regulations promoting sustainable practices and the need for critical material recovery such as lithium, cobalt, and nickel have further accelerated recycling efforts in the automotive sector. This trend is expected to continue as the global EV fleet expands and battery recycling technologies improve.

Battery Chemistry Analysis

Lead-acid Batteries Dominate Due To Their Widespread Use In Automotive Applications, Cost-Effectiveness, And Established Recycling Infrastructure.

Based on battery chemistry, the market is further divided into lithium-ion, lead-acid, nickel-based, flow batteries, and others. The predominance of the lead-acid, commanding a substantial 72.1% market share in 2024. Due to their widespread use in automotive applications, particularly in conventional internal combustion engine (ICE) vehicles. Their established recycling infrastructure, cost-effectiveness, and long-standing presence in industries like automotive and backup power systems further contribute to their market dominance. Despite the rise of newer battery technologies, lead-acid remains a key player in the recycling sector.

Technology Analysis

Pyrometallurgy dominates the market due to its efficiency in recovering valuable metals from various battery chemistries and its scalability in large-scale operations.

Based on technology, the market is further divided into pyrometallurgy, hydrometallurgy, and mechanical separation. The predominance of the pyrometallurgy, commanding a substantial 56.2% market share in 2024. Due to its effectiveness in extracting valuable metals such as nickel, cobalt, and copper from different battery chemistries. Its established industrial processes, high throughput, and scalability make it the preferred choice for large-scale battery recycling operations. Additionally, the ability to handle diverse battery types and chemistries further strengthens its dominance in the market.

End-Use Analysis

Material Extraction leads the market due to the high demand for critical raw materials like lithium, cobalt, and nickel essential for new battery production.

Based on end-use, the market is further divided into material extraction, disposal, and reuse, repackaging & second life. The predominance of material extraction commanded a substantial 48.2% market share in 2024. Due to the rising demand for critical raw materials such as lithium, cobalt, and nickel, which are vital for the production of new batteries.

Efficient recycling processes enable the recovery of these valuable materials, driving the demand for material extraction. Additionally, the increasing focus on reducing reliance on mined resources and promoting a circular economy further strengthens the market for material extraction.

Key Market Segments

By Source

- Automotive Batteries

- Passenger Cars

- Light & Heavy Commercial

- Others (2 & 3 Wheelers)

- Industrial Batteries

- Consumer & Electrical Appliance Batteries

By Battery Chemistry

- Lithium-ion

- Lithium Cobalt Oxide (LCO)

- Lithium Manganese Oxide (LMO)

- Lithium Nickel Manganese Cobalt Oxide (NMC)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

- Lithium Iron Phosphate (LFP)

- Others

- Lead-acid

- Nickel based

- Flow Batteries

- Others

By Technology

- Pyrometallurgy

- Hydrometallurgy

- Mechanical Separation

By End-Use

- Material Extraction

- Disposal

- Reuse, Repackaging & Second Life

Drivers

Rising Adoption Of Electric Vehicles

The rising adoption of electric vehicles (EVs) is significantly driving the growth of the global battery recycling market. The demand for EVs rising rapidly, driven by net-zero emission goals, supportive government policies, and rapid advancements in EV technology. With this surge in EV sales, the volume of end-of-life lithium-ion batteries is also rising, creating an urgent need for scalable and efficient recycling solutions.

- According to European Electric vehicles (EVs) are rapidly growing in popularity, with over 30 million expected on European roads by 2020. As this number rises, so will the volume of end-of-life batteries.

Furthermore, EV batteries contain toxic materials like lithium, cobalt, and nickel. If not recycled, they can pollute soil and groundwater. Recycling recovers these materials, reducing the need for new mining and supporting a circular economy.

- According to the International Energy Agency (IEA), the demand for sustainable lithium-ion batteries (SLIBs) is projected to grow significantly, from 400 GWh in 2035 to 1300 GWh by 2040. This surge in demand is expected to boost the global battery recycling market.

- Recycling lithium-ion batteries (LIBs) reduces energy consumption and environmental impact by 5-30%, consuming nine times less energy than producing new batteries. It also lowers fine particulate matter by 17% and reduces mineral resource scarcity by 25%, supporting sustainable development.

- Battery recycling led to a 17 % decrease in EVs’ fine particulate matter formation, improving air quality by reducing waste incineration and landfills.

The growing emphasis on battery recycling is further supported by evolving regulatory frameworks, as governments worldwide implement strict regulations on battery waste management. These initiatives are forcing electric vehicle producers to take responsibility for the handling and treatment (collection, storage, transport, recycling, and disposal) of used batteries. Additionally, governments are offering financial incentives to encourage investments in lithium-ion battery recycling.

- For instance, In Europe, the Battery Regulation mandates ambitious recovery targets by 2030, while several U.S. states are introducing Extended Producer Responsibility (EPR) laws to hold manufacturers accountable for battery recycling. These regulations are driving substantial investments in advanced recycling technologies.

- For instance, the Inflation Reduction Act of 2022 provides tax credits for recycled battery materials, while the EU’s End-of-Life Vehicles Directive mandates automotive Original Equipment Manufacturers (OEMs) to reclaim end-of-life batteries, These policies drive battery recycling demand by making it financially viable and ensuring a consistent supply of used batteries.

- In 2023, the EU introduced new Battery Regulations covering the entire lifecycle of batteries, requiring manufacturers to recover 50% of lithium from old batteries by 2027 and 80% by 2031. Companies must also track carbon footprints, meet recycling content targets by 2025, and implement a digital battery passport for improved transparency by 2027.

Restraints

High recycling cost

High recycling costs are a significant restraint on the growth of the battery recycling market, as they make it less economically viable for companies to recycle certain battery types, especially those with complex chemistries. The costs involved in collection, transportation, and processing, coupled with the need for advanced technology, can limit profitability for recycling companies.

Additionally, fluctuating market prices for recovered materials and the need for regulatory compliance further increase operational costs. These factors can slow down the expansion of the market, especially in regions where recycling infrastructure is still developing.

Opportunity

Technological advancements

The advancements in battery recycling technologies present significant opportunities for the global market. These innovations boost scalability and operational efficiency, enabling industries to manage the growing volume of batteries in various industries, keeping pace with rapid adoption across sectors. Furthermore, the development of sustainable methods, such as green solvents and energy-efficient technologies, supports global sustainability goals, driving further demand in the market.

Moreover, Emerging technologies like direct recycling, biotechnology-based recycling, and blockchain for material traceability are paving the way for significant growth in the battery recycling sector. These innovations not only reduce environmental impact but also improve the economic feasibility of recycling processes.

- According to the International Energy Agency (IEA), recycling and reuse efforts could substantially reduce the primary supply requirements for selected minerals in the Sustainable Development Scenario between 2030 and 2040.

- With electric vehicles (EVs) accounting for 41% of the market share, this growth will drive greater investment in recycling technologies and processes to meet the rising demand for battery materials and reduce environmental impacts.

Moreover, utilizing recycled materials in second-life applications, such as stationary energy storage systems, opens up new market opportunities and extends the lifespan of battery components. As the EV market continues to expand, these technological advancements are creating a strong foundation for a circular economy, driving sustained growth and long-term prospects in the battery recycling industry.

- According to a report published by the European Commission state that, By 2025, approximately 3.4 million end-of-life EV batteries, totaling 953 GWh, are expected to be discarded. Despite losing 20% of their nominal capacity, these batteries still hold usable energy, making them suitable for second-life applications, such as stationary storage. This repurposing helps reduce the demand for new Lithium-ion materials and promotes a circular economy by minimizing environmental impact.

Trends

Growth of Second Life Battery Application

The growth of second-life battery applications is a significant trend in the global battery recycling market, driven by the potential to repurpose electric vehicle (EV) batteries that still retain usable capacity after no longer meeting vehicle performance requirements. These repurposed batteries can be utilized for energy storage in residential, industrial, and grid-scale applications, such as storing renewable energy, providing backup power, or stabilizing the electricity grid.

Additionally, they are being employed in less demanding EV applications such as electric bicycles, scooters, and low-speed vehicles. This trend not only extends the lifespan of battery materials but also contributes to sustainability by reducing waste and maximizing the utility of used batteries, all while supporting the transition to cleaner energy systems and lowering the cost of energy storage solutions.

Geopolitical Impact Analysis

Geopolitical Impact of U.S. Tariffs on the Global Battery Recycling Market.

The recent geopolitical tensions and trade restrictions between the United States and China, along with escalating U.S. tariffs on several countries globally, are significantly impacting the global battery recycling market. U.S. tariffs on Chinese-made batteries are impacting the global battery recycling market. As tariffs raise the cost of new batteries, demand for battery replacements may decrease, leading to fewer used batteries for recycling. Additionally, higher costs for raw materials make recycling less cost-effective, and supply chain disruptions could slow down the recycling process, hindering the industry’s growth and efficiency.

- For instance, the latest round of U.S. tariffs on Chinese-made batteries, set to reach 82% by January 2026, will significantly increase the cost of imported batteries from China, potentially doubling their prices. China faces an additional 34% tariff on top of prior measures, including a 20% tariff and two 10% increases. Combined with existing duties like the 3.4% global tariff on lithium-ion batteries and a Section 301 tariff (7.5%, set to rise to 25% in 2026), these tariffs will severely disrupt global supply chains, affecting both battery production and recycling processes.

Regional Analysis

In 2024, Asia Pacific dominated the global Battery Recycling market, accounting for 39.4% of the total market share, Driven by stringent environmental regulations and the increasing adoption of electric vehicles (EVs) in China, Japan, and South Korea. As EVs become more widespread, the need for efficient battery recycling grows, driven by the challenge of managing battery end-of-life disposal. This rising demand for EVs emphasizes the need for advanced recycling processes to recover valuable materials such as lithium, cobalt, and nickel, accelerating market growth.

Furthermore, governments prioritized battery recycling implementing stringent environmental regulations playing a crucial role in shaping the market. Governments are actively promoting policies that incentivize manufacturers to develop and adopt advanced recycling technologies, and that provide clear regulations for battery collection, processing, and disposal. This regulatory support is vital for ensuring the safe and efficient recycling of used batteries, particularly lithium-ion batteries, which are commonly used in electric vehicles and energy storage systems.

- For instance, China introduced key recycling laws starting in 2016, with the Ministry of Industry and Information Technology (MIIT) setting strict rules on battery handling and recycling standards in 2018. The 2020 Solid Waste Pollution Law halted waste imports and promoted recycling, while the Circular Economy Development Plan (2021-2025) emphasizes battery reuse.

Additionally, favorable public and private investments in technological advancements are enhancing the efficiency of battery recycling processes. These innovations not only reduce costs but also minimize the environmental impact of battery disposal. Together, these factors are creating a conducive environment for the growth of the battery recycling market in the Asia Pacific region, supporting the transition to a more sustainable, circular economy.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Key players in the battery recycling market focus on expanding their recycling capabilities through technological innovation, such as implementing advanced hydrometallurgical and pyrometallurgical processes for higher recovery rates. They are also investing in scaling up operations, increasing production capacity, and forming strategic partnerships with automotive manufacturers and energy companies.

Additionally, these players emphasize sustainability by improving the environmental impact of their processes and meeting regulatory requirements. Their strategies aim to enhance operational efficiency and address the growing demand for critical raw materials in battery production.

Major Players in the Industry

- BASF SE

- Accurec Recycling GmbH

- Fortum

- Glencore

- Umicore

- Exide Industries Ltd

- Gravita India Ltd

- Li-Cycle

- RecycLiCo Battery Materials

- Tata Chemicals Ltd.

- American Battery Technology Company

- Cirba Solutions

- Gopher Resource LLC

- East Penn Manufacturing

- Aqua Metals

- Eco-Bat Technologies

- Ganfeng Lithium Group Co., Ltd.

- Lithion Recycling Inc.

- EnerSys

- Redwood Materials, Inc.

- Element Resources LLC

- Contemporary Amperex Technology Co. Limited

- Stena Recycling

- REDUX Recycling GmbH

- Other Key Players

Recent Development

- In April 2025 – Henan’s State Grid Electric Power Company, through its subsidiary, developed the world’s first international standard for decommissioned battery recycling, IEC 63648, which outlines safe discharge and pre-treatment methods. The company has also pioneered a fully automated dry-process battery recycling production line and contributed to national standards for lithium-ion battery disposal.

- In April 2025 – American Battery Technology Company (ABTC) successfully doubled its quarterly production at its lithium-ion battery recycling facility by implementing 24/7 continuous operations and optimizing manufacturing throughput. This milestone showcases the effectiveness of the company’s first-of-its-kind recycling technologies, which recover critical battery materials that meet stringent quality standards.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 19.4 Bn |

| Forecast Revenue (2034) | USD 69.4 Bn |

| CAGR (2025-2034) | 13.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Automotive Batteries, (Passenger Cars, Light & Heavy Commercial, Others (2 & 3 Wheelers), Industrial Batteries, Consumer & Electrical Appliance Batteries), By Battery Chemistry (Lithium-ion, (Lithium Cobalt Oxide (LCO), Lithium Manganese Oxide (LMO), Lithium Nickel Manganese Cobalt Oxide (NMC), Lithium Nickel Cobalt Aluminum Oxide (NCA), Lithium Iron Phosphate (LFP), Others), Lead-acid, Nickel-based, Flow Batteries, Others), By Technology (Pyrometallurgy, Hydrometallurgy, Mechanical Separation), By End-use (Material Extraction, Disposal, Reuse, Repackaging & Second Life) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF SE, Accurec Recycling GmbH, Fortum, Glencore, Umicore, Exide Industries Ltd, Gravita India Ltd., Li-Cycle, RecycLiCo Battery Materials, Tata Chemicals Ltd., American Battery Technology Company, Cirba Solutions, Gopher Resource LLC, East Penn Manufacturing, Aqua Metals, Eco-Bat Technologies, Ganfeng Lithium Group Co., Ltd., Lithion Recycling Inc., EnerSys, Redwood Materials, Inc., Element Resources LLC, Contemporary Amperex Technology Co. Limited, Stena Recycling, REDUX Recycling GmbH, Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |