Global Bath and Shower Products Market Size, Share, Growth Analysis By Product Type (Bath Soaps, Body Wash/Shower Gel, Bath Additives, Others), By Form (Solid, Gels & Jellies, Liquid, Others), By End-User (Women, Men), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Online Stores, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181793

- Number of Pages: 363

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

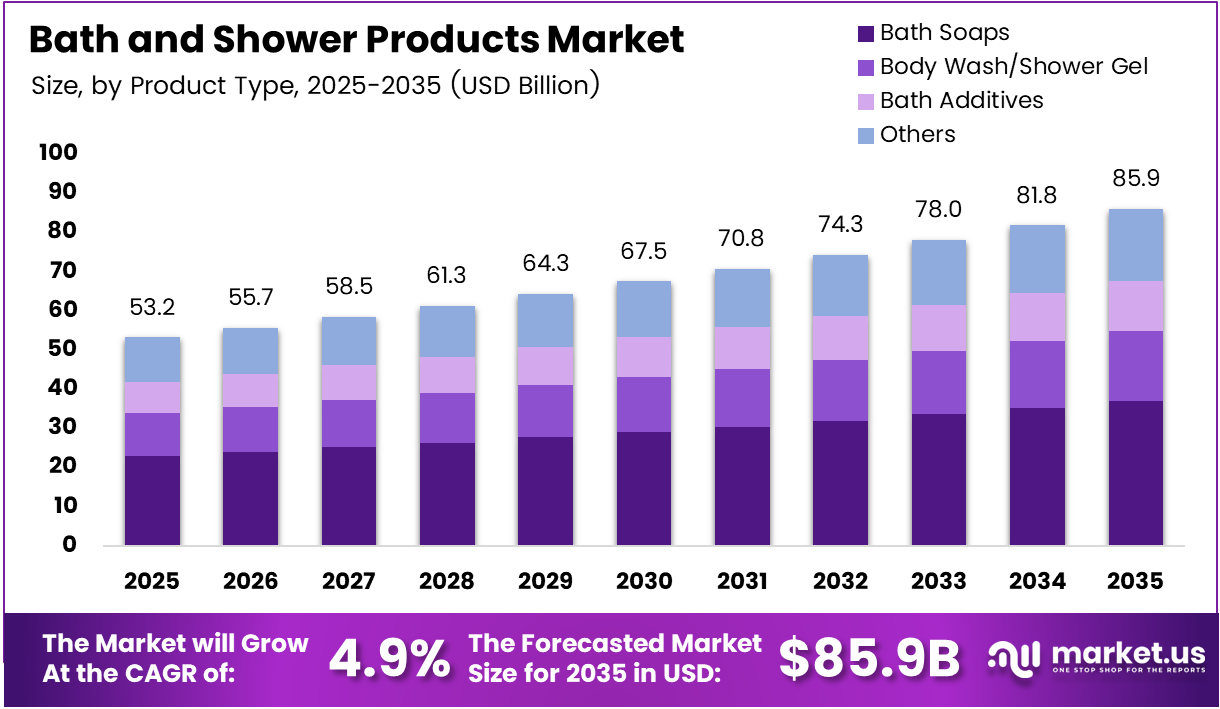

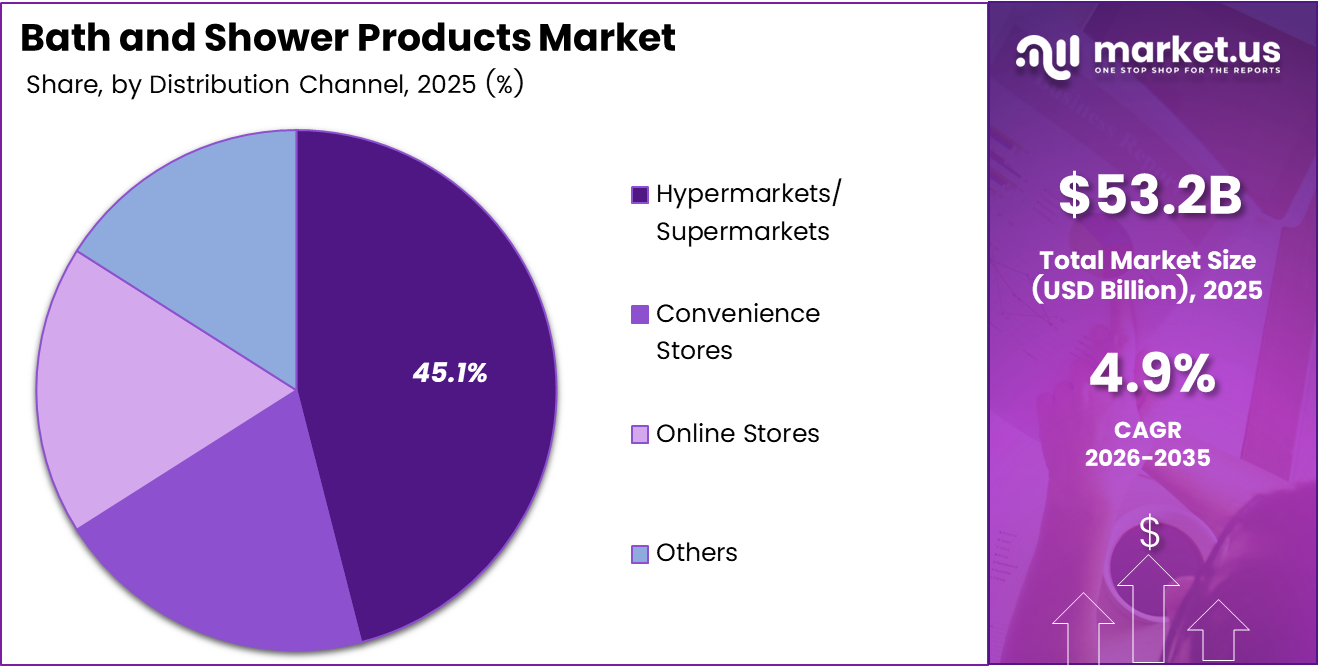

The Global Bath and Shower Products Market size is expected to be worth around USD 85.9 Billion by 2035 from USD 53.2 Billion in 2025, growing at a CAGR of 4.9% during the forecast period 2026 to 2035.

Bath and shower products cover a broad category of personal care formulations including bath soaps, body washes, shower gels, and bath additives used daily for hygiene and skin care. This market sits at the intersection of functional necessity and personal wellness — a combination that makes it structurally resilient across economic cycles.

Women represent the largest end-user base, holding 61.4% of demand, reflecting decades of product development targeted at female consumers. However, the men’s grooming segment is now emerging as an active growth front, with brands investing in natural soap and body wash lines designed specifically for male buyers.

Hypermarkets and supermarkets command 45.1% of distribution, anchoring the market in physical retail. However, online channels are gaining traction as brands build direct-to-consumer capabilities — a structural shift that compresses margins for traditional retailers while expanding reach for challenger brands.

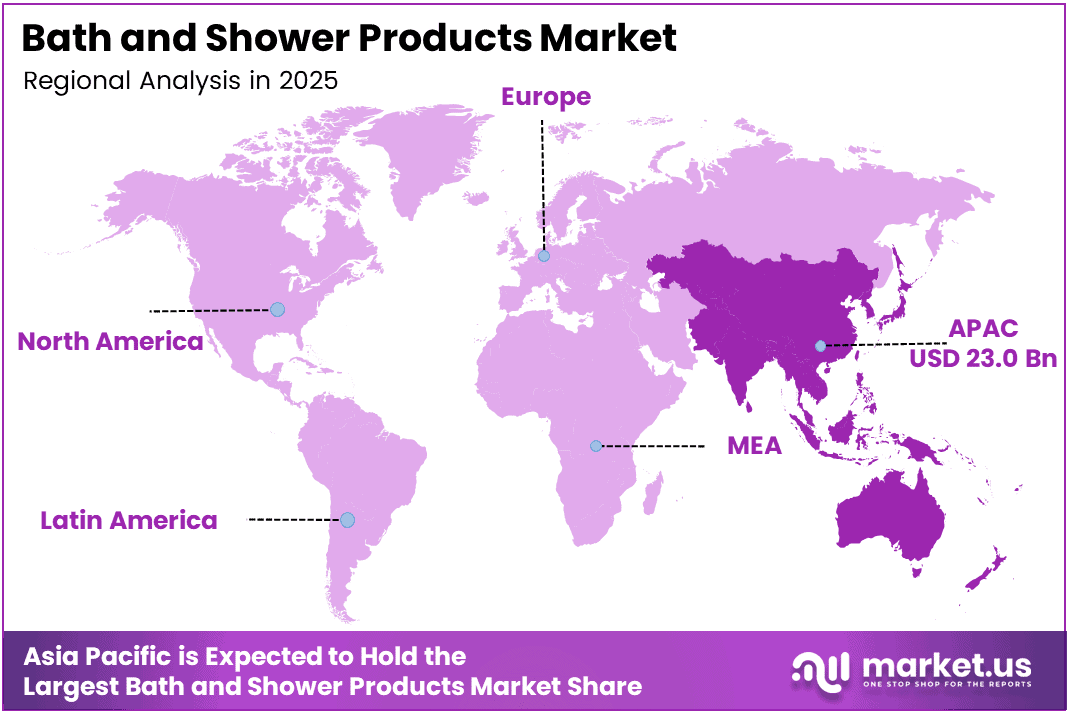

Asia Pacific leads regional demand with a 43.5% share, valued at USD 23 Billion. Urban population growth across China, India, and Southeast Asia is expanding the addressable consumer base at a pace that outstrips most other global regions, making APAC the primary battleground for volume growth through 2035.

Premium and fragrance-infused formulations are drawing higher spending per unit across developed markets. Brands that command shelf space in both organized retail and e-commerce are better positioned to capture these premiumization tailwinds without sacrificing volume-led growth in price-sensitive emerging markets.

According to the Alliance for Water Efficiency, using 2-in-1 shampoo and conditioner products reduces water use by 5.25 gallons per shower compared to separate product applications. This signals a structural shift in buyer preference toward multi-functional formulations — a behavior that product developers can leverage to align sustainability with convenience.

According to the Alliance for Water Efficiency, annual water savings reach 1,318 gallons per person when consumers switch to combined wash formats. This scale of impact is reshaping how brands position efficiency-focused products — not as niche eco-options but as mainstream alternatives with measurable household benefits. In November 2025, Kimberly-Clark announced its acquisition of Kenvue at approximately USD 48.7 Billion, combining portfolios that include body washes and shampoos under brands like Aveeno and Neutrogena — underscoring how consolidation is accelerating at the top of this market.

Key Takeaways

- The Global Bath and Shower Products Market was valued at USD 53.2 Billion in 2025 and is forecast to reach USD 85.9 Billion by 2035.

- The market grows at a CAGR of 4.9% during the forecast period 2026 to 2035.

- By Product Type, Bath Soaps dominate with a 42.6% market share in 2025.

- By Form, Solid formats lead with a 48.3% share, reflecting strong consumer preference for bar soaps and solid cleansers.

- By End-User, Women account for 61.4% of total market demand.

- By Distribution Channel, Hypermarkets and Supermarkets hold the largest share at 45.1%.

- Asia Pacific dominates regional demand with a 43.5% share, valued at USD 23 Billion.

Product Type Analysis

Bath Soaps dominate with 42.6% due to universal daily use and low price point.

In 2025, Bath Soaps held a dominant market position in the By Product Type segment of the Bath and Shower Products Market, with a 42.6% share. Bar soap remains the most purchased personal care format globally because it requires no packaging beyond a wrapper, carries a low unit cost, and delivers consistent hygiene performance across all income levels — making it the default choice for both premium and mass-market buyers.

Body Wash and Shower Gel carries the highest margin potential within the liquid personal care category. These products command premium pricing through fragrance layering, moisturizing additives, and lifestyle branding — factors that make them the preferred format for urban, higher-income consumers seeking more than basic cleansing. The segment benefits directly from the premiumization trend across personal care.

Bath Additives serve as the entry point for wellness-oriented consumers who treat bathing as a self-care ritual rather than a functional routine. Products in this category — including bath salts, oils, and effervescent tablets — attract buyers willing to spend more per occasion. This positions bath additives as a margin-accretive complement to core cleansing formats. In January 2025, Native launched its limited-edition Dunkin’ collaboration featuring donut-inspired scents in body wash and shampoo formats at USD 10 each, demonstrating how novelty-driven bath additive concepts can generate retail buzz and expand buyer demographics.

Others within the product type category include specialty formats such as cleansing oils, micellar body waters, and exfoliating scrubs. These products occupy a fast-moving but fragmented part of the market, driven by dermatologist-recommended skin care crossover — particularly among consumers managing sensitive or condition-prone skin.

Form Analysis

Solid formats dominate with 48.3% due to cost efficiency and plastic-free positioning.

In 2025, Solid formats held a dominant market position in the By Form segment of the Bath and Shower Products Market, with a 48.3% share. Solid bar formats benefit from zero liquid content, which lowers shipping weight, eliminates preservative requirements, and enables plastic-free packaging — a combination that satisfies both cost-conscious mass-market buyers and eco-aware premium shoppers simultaneously.

Gels and Jellies differentiate through sensory appeal — delivering texture, lather density, and fragrance retention that solid formats cannot match. This sensory premium is the primary reason gels and jellies command higher per-unit prices in organized retail and direct-to-consumer channels. The format appeals disproportionately to younger consumers seeking a differentiated shower experience.

Liquid formats serve the broadest distribution footprint across hypermarkets, convenience stores, and online platforms. Their pump-and-pour format suits high-frequency household use and positions them as the workhorse format for family-size SKUs. Brands competing in liquid body wash benefit from high repurchase frequency and strong potential for subscription-based direct-to-consumer models.

Others in the form category include powders, concentrates, and dissolvable formats. These represent emerging formulation innovation rather than volume segments. Brands investing in concentrate-to-dilute formats, for example, are responding directly to consumer demand for reduced packaging and lower carbon-per-use metrics — an area where innovation investment outpaces current commercial scale.

End-User Analysis

Women dominate with 61.4% due to higher product variety usage and premium format adoption.

In 2025, Women held a dominant market position in the By End-User segment of the Bath and Shower Products Market, with a 61.4% share. Female consumers drive this dominance through multi-product usage — combining body washes, bath additives, and specialized skin care cleansers in daily routines that male consumers do not yet replicate at scale. This translates into higher basket size and stronger repeat purchase frequency.

Men represent the fastest-evolving end-user segment in the bath and shower category. The shift is structural: brands like Dr. Squatch — acquired by Unilever in June 2025 — built their entire value proposition around natural soaps and body washes formulated specifically for male skin. This acquisition signals that large FMCG players now recognize men’s grooming as a priority growth segment requiring dedicated product architecture, not just repackaged unisex formulas.

Distribution Channel Analysis

Hypermarkets and Supermarkets dominate with 45.1% due to high footfall and broad SKU availability.

In 2025, Hypermarkets and Supermarkets held a dominant market position in the By Distribution Channel segment of the Bath and Shower Products Market, with a 45.1% share. Physical large-format retail gives brands the visibility, shelf presence, and trial-driving capability that digital channels cannot replicate — particularly for consumers making first-time purchases across new product formats or scent profiles.

Convenience Stores serve the impulse and top-up purchase occasions that hypermarkets miss. Smaller pack sizes and strategic placement near checkout points make convenience retail an important secondary channel — particularly in dense urban markets across Asia Pacific and Latin America where small-format retail dominates foot traffic.

Online Stores are restructuring the competitive dynamics of the bath and shower category. Direct-to-consumer brands bypass traditional retail markups, use subscription models to lock in repeat purchases, and access consumer data that informs faster product iteration. This channel shift is compressing shelf space for mid-tier brands in physical retail while creating room for digitally native challengers to scale.

Others in the distribution channel include specialty beauty retailers, pharmacies, and professional salon channels. These channels carry outsized influence relative to their volume share — particularly pharmacies, where dermatologist endorsement and clinical positioning can shift consumer perception of a product from cosmetic to therapeutic, justifying premium pricing.

Key Market Segments

By Product Type

- Bath Soaps

- Body Wash/Shower Gel

- Bath Additives

- Others

By Form

- Solid

- Gels & Jellies

- Liquid

- Others

By End-User

- Women

- Men

By Distribution Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Stores

- Others

Drivers

Hygiene Awareness, Premiumization, and E-Commerce Expansion Drive Bath and Shower Product Adoption

Consumer focus on personal hygiene has moved from periodic awareness to daily behavioral commitment — a shift that directly expands the addressable market for bath and shower products. Brands offering clinically formulated, dermatologically tested cleansers are capturing buyers who previously purchased on price alone. This transition lifts both category volume and average transaction value simultaneously.

Premiumization is the second structural force reshaping revenue potential. Consumers in urban markets actively seek fragrance-infused body washes, botanical soap formulations, and multi-benefit shower gels. In April 2025, Unilever acquired UK brand Wild — known for sustainable, refillable body care — to capture this premium-and-eco buyer segment. According to L’Oréal’s Responsible Water Use Policy, rinse-off products such as shower gels are now formulated to deliver at least 15% less water consumption while maintaining hygiene performance, reflecting how premium formulation and sustainability goals are converging.

Organized retail and e-commerce expansion are the distribution-side drivers that make volume growth possible at scale. Online channels, in particular, enable brands to reach consumers in markets where physical retail infrastructure remains underdeveloped. Higher disposable income across urbanizing Asia Pacific and Latin American markets further supports regular spending on branded personal care products — converting infrequent buyers into habitual category participants.

Restraints

Chemical Safety Concerns and Price Sensitivity Constrain Market Expansion in Emerging Segments

Consumer concern over parabens, sulfates, and synthetic fragrances in bath and shower products is forcing formulation redesigns across the category. Brands that cannot credibly verify ingredient safety face accelerating risk of market share erosion — particularly among female buyers aged 25–45 who actively research product labels before purchasing. This clean-beauty pressure raises R&D costs for established players.

Reformulating without parabens and sulfates requires substituting proven, low-cost preservatives with more expensive alternatives that may not perform identically across all product formats. This cost pressure is absorbed either by the brand through margin compression or passed to consumers through higher prices — neither outcome is commercially neutral. Smaller manufacturers face an existential challenge if reformulation capex outpaces their revenue base.

Price sensitivity in emerging economies further limits the pace at which premium and reformulated products penetrate high-volume markets. Consumers in price-sensitive segments prioritize cost per wash over ingredient transparency, which means the clean beauty shift drives revenue in premium tiers while leaving volume-led segments largely insulated from reformulation pressure. This bifurcation makes it harder for single-product-line brands to serve both market tiers efficiently.

Growth Factors

Organic Formulations, Sustainable Packaging, and DTC Channel Expansion Create New Revenue Frontiers

Demand for organic, natural, and plant-based bath and shower products is creating a commercially distinct sub-category that commands meaningful price premiums. Brands positioned in this space attract buyers who treat personal care as an extension of their broader wellness philosophy. This is not a fringe preference — it reflects a structural reorientation of consumer priorities toward ingredient transparency and environmental accountability.

Sustainable packaging is accelerating as both a regulatory response and a brand differentiator. According to ADA Cosmetics, its automated Refillution system for hotel bath and shower amenities reduces plastic waste by up to 95%, equivalent to approximately 4.5 kg per room per year. This scale of plastic reduction, applied across commercial and retail channels, signals that refillable formats can deliver measurable sustainability impact — making them viable beyond premium hospitality contexts.

Direct-to-consumer brands are unlocking growth by bypassing retail intermediaries and building subscription-based repurchase models. In June 2025, Unilever acquired Dr. Squatch — a natural soap and body wash brand targeting male consumers — to extend its DTC capabilities in men’s personal care. This move reflects a broader industry recognition that DTC channel economics and gender-specific product positioning together define the next phase of revenue expansion in this market.

Emerging Trends

Wellness Positioning, Multi-Functional Formulas, and Clean Beauty Drive the Next Generation of Bath Products

Aromatherapy and wellness-integrated bath products are reshaping buyer expectations — consumers now seek shower experiences that deliver stress relief, mood elevation, and sensory ritual alongside basic cleansing. In March 2025, Oceania Cruises launched its bespoke Aquamar bath and skincare collection across all guest accommodations, featuring Vetiver and Green Leaves-scented shampoos, conditioners, and body washes. Hospitality-grade wellness branding is increasingly setting the reference point for premium retail positioning.

Multi-functional formulations are gaining traction as a direct response to consumer demand for efficiency and reduced routine complexity. Body washes that simultaneously moisturize, protect the skin barrier, and deliver fragrance reduce the number of products a consumer needs — and reduce water use per shower. According to L’Oréal’s Responsible Water Use Policy, its Water Saver technology reduces water consumption by up to 69% during rinse-off processes — demonstrating that multi-function formulation and water efficiency now reinforce each other as product design targets.

Clean beauty and social media influence are reshaping purchase decisions at a structural level. Consumers increasingly require dermatological testing credentials before committing to a new body wash or soap brand. Beauty influencers on short-form video platforms compress the trial-to-purchase cycle — turning a new fragrance launch into a sellout event within days. Brands that align clean beauty certification with an active influencer strategy hold a measurable acquisition advantage over those relying solely on traditional retail merchandising.

Regional Analysis

Asia Pacific Dominates the Bath and Shower Products Market with a Market Share of 43.5%, Valued at USD 23 Billion

Asia Pacific leads the Bath and Shower Products Market with a 43.5% share, valued at USD 23 Billion. Urban population expansion across China, India, and Southeast Asia is structurally expanding the addressable consumer base. Rising middle-class income in these markets is shifting purchasing behavior from unbranded commodity soaps toward branded cleansers with specific functional and sensory benefits.

North America Bath and Shower Products Market Trends

North America maintains a mature but premiumizing market position. Consumers here allocate more spend per unit toward clean-label, dermatologically tested, and fragrance-led formulations. The region’s well-developed e-commerce infrastructure and subscription retail ecosystem give direct-to-consumer brands a structural advantage over traditional retail-dependent competitors, accelerating channel mix evolution.

Europe Bath and Shower Products Market Trends

Europe leads on regulatory stringency, with cosmetic ingredient regulations among the most demanding globally. This creates a compliance-driven reformulation cycle that raises category quality standards — and raises entry barriers for brands relying on ingredient profiles that do not meet EU safety thresholds. Sustainable packaging mandates are further accelerating the transition to refillable and low-plastic formats across retail.

Latin America Bath and Shower Products Market Trends

Latin America presents a high-volume, price-sensitive market where value-format bath soaps and affordable body washes dominate. Brazil and Mexico anchor regional demand. However, a growing urban middle class is creating incremental appetite for mid-tier branded products — particularly body washes with fragrance and moisturizing benefits previously accessible only at premium price points.

Middle East and Africa Bath and Shower Products Market Trends

The Middle East and Africa region shows structurally differentiated demand — the GCC states support a strong premium and luxury personal care market, while Sub-Saharan Africa remains predominantly volume-driven. Cultural emphasis on cleanliness and hygiene across both sub-regions sustains consistent baseline demand for bath soaps and body wash formats across income tiers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Unilever holds one of the broadest brand portfolios in global bath and shower, spanning mass-market cleansers through to premium sustainable formats. Its April and June 2025 acquisitions of Wild and Dr. Squatch signal a deliberate strategy to capture two high-growth sub-segments — eco-conscious refillables and men’s natural grooming — before these niches consolidate under category incumbents. This dual flanking move is strategically aggressive.

Colgate-Palmolive Co. leverages its oral and personal care distribution infrastructure to support bath and shower product penetration across both developed and emerging markets. Its competitive strength lies in retail relationship depth — particularly in Latin America and Asia Pacific — giving it shelf access that newer, digitally native brands cannot replicate without significant trade marketing investment over multiple years.

Beiersdorf AG anchors its bath and shower positioning on dermatological credibility. Its flagship brand strategy — built around skin science claims and clinical validation — creates a durable trust advantage with consumers who prioritize skin health over fragrance or lifestyle branding. This positioning is especially defensible in European markets where regulatory rigor rewards formulation transparency.

Henkel AG & Co. KGaA operates across both consumer and professional personal care channels, giving it exposure to retail volume and to the premium salon and hospitality segments where formulation standards are higher. This dual-channel presence allows Henkel to test innovation in professional settings and translate proven formulations to retail — a product pipeline discipline that reduces launch risk and accelerates commercialization speed.

Key Players

- Unilever

- Colgate Palmolive Co.

- Beiersdorf AG

- Henkel AG & Co. KGaA

- Natura & Co. Holding S.A.

- Procter & Gamble

- L’Occitane International S.A.

- Lion Corporation

- Johnson & Johnson Services, Inc.

- Reckitt Benckiser Group plc

Recent Developments

- November 2025 — Kimberly-Clark announced its acquisition of Kenvue in a deal valued at approximately USD 48.7 Billion enterprise value, combining portfolios that include bath and shower products such as body washes and shampoos under Aveeno and Neutrogena brands. This consolidation ranks among the largest personal care M&A transactions of the decade.

- January 2025 — Native launched a limited-edition collaboration with Dunkin’, releasing donut-inspired scents across Body Wash, Shampoo, Conditioner, and 2-in-1 formats priced at USD 10 each, available exclusively at Walmart and Native’s website. The collaboration demonstrates how novelty-driven scent concepts can drive rapid retail sell-through in mass-market bath categories.

- March 2025 — Oceania Cruises announced its bespoke Aquamar bath and skincare collection, including shampoo, conditioner, body wash, and soaps infused with Vetiver and Green Leaves scent, debuting across all guest accommodations from Spring 2025. The launch reinforces the convergence of premium hospitality and branded personal care positioning.

Report Scope

Report Features Description Market Value (2025) USD 53.2 Billion Forecast Revenue (2035) USD 85.9 Billion CAGR (2026-2035) 4.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Bath Soaps, Body Wash/Shower Gel, Bath Additives, Others), By Form (Solid, Gels & Jellies, Liquid, Others), By End-User (Women, Men), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Online Stores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Unilever, Colgate Palmolive Co., Beiersdorf AG, Henkel AG & Co. KGaA, Natura & Co. Holding S.A., Procter & Gamble, L’Occitane International S.A., Lion Corporation, Johnson & Johnson Services, Inc., Reckitt Benckiser Group plc Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Bath and Shower Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Bath and Shower Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Unilever

- Colgate Palmolive Co.

- Beiersdorf AG

- Henkel AG & Co. KGaA

- Natura & Co. Holding S.A.

- Procter & Gamble

- L'Occitane International S.A.

- Lion Corporation

- Johnson & Johnson Services, Inc.

- Reckitt Benckiser Group plc

Our Clients

- 181793

- Mar 2026