Quick Navigation

Report Overview

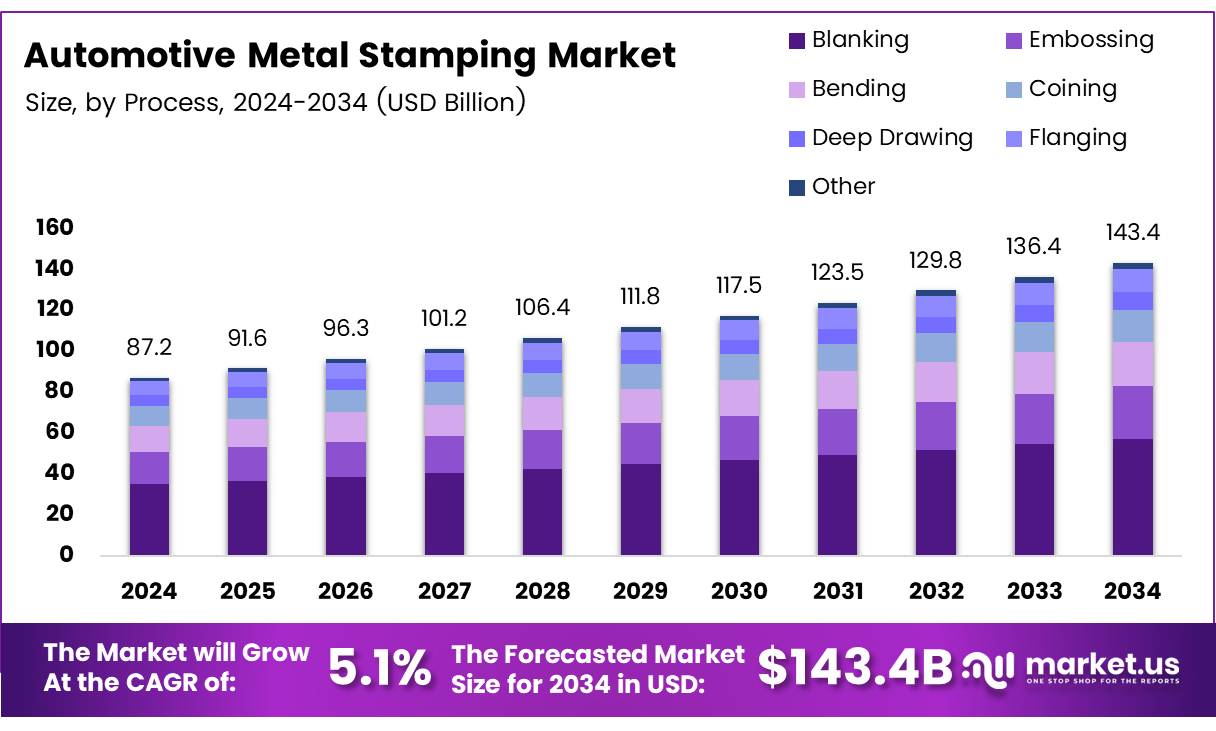

The Global Automotive Metal Stamping Market size is expected to be worth around USD 143.4 Billion by 2034, from USD 87.2 Billion in 2024, growing at a CAGR of 5.1% during the forecast period from 2025 to 2034.

Automotive metal stamping is a pivotal manufacturing process used in the automotive industry to cut and shape metal into various components. This technique involves several processes, including punching, embossing, bending, and coining. It is integral to forming parts that meet precise specifications required in vehicle assembly.

The automotive metal stamping market leverages this process extensively to produce durable and high-quality parts ranging from large panels to intricate connectors. This market serves as the backbone for manufacturing numerous critical vehicle components essential for structural integrity and aerodynamic performance.

The automotive metal stamping market is currently witnessing substantial growth, driven by increasing global vehicle production and advancements in metal stamping technology. This market is crucial for the automotive sector due to its role in enhancing production efficiency and reducing manufacturing costs.

Stamping processes are highly favored for their ability to produce lighter, stronger, and more complex parts, which are increasingly demanded in modern vehicles. Furthermore, the shift towards electric vehicles (EVs) has opened new avenues for metal stamping, as these vehicles require uniquely designed lightweight components to improve battery efficiency and vehicle dynamics.

Regarding growth, the automotive metal stamping market is poised for expansion, catalyzed by the automotive industry’s evolution. Governments worldwide are increasingly investing in automotive sectors to bolster economic growth, enhance technological advancements, and support domestic manufacturing bases.

For instance, according to USTR, the percentage of vehicles imported from Canada or Mexico for which duties were paid escalated significantly from 0.5% (valued at $517 million) in 2019 to 8.2% (valued at $8.9 billion) in 2023. This indicates a growing reliance on cross-border automotive trade, which directly impacts the metal stamping market through increased demand for stamped parts.

Additionally, regulatory frameworks are being strengthened to ensure more sustainable and safe automotive manufacturing practices. The introduction of stringent emissions regulations compels automakers to seek more efficient, lighter-weight metal components, frequently achieved through advanced stamping techniques.

Moreover, in response to the USMCA’s automotive Rules of Origin, U.S. vehicle producers ramped up production by 1,464 vehicles in 2024, as per USTR. This adaptation underscores the strategic alignment of automotive production processes with regional trade agreements, fostering growth in the metal stamping sector.

The automotive metal stamping industry is further highlighted by its significant role in the production of automotive parts. According to Pressmach, over 40% of the more than 2,000 automotive parts are stamping parts of sheet metal, showcasing the indispensable status of stamping process equipment in the industry.

Key Takeaways

- The global automotive metal stamping market is projected to reach USD 143.4 billion by 2034, growing at a CAGR of 5.1%.

- Blanking process dominated the market in 2024, holding a 40.5% share.

- Steel remains the leading material, owing to its strength, reliability, and cost-efficiency.

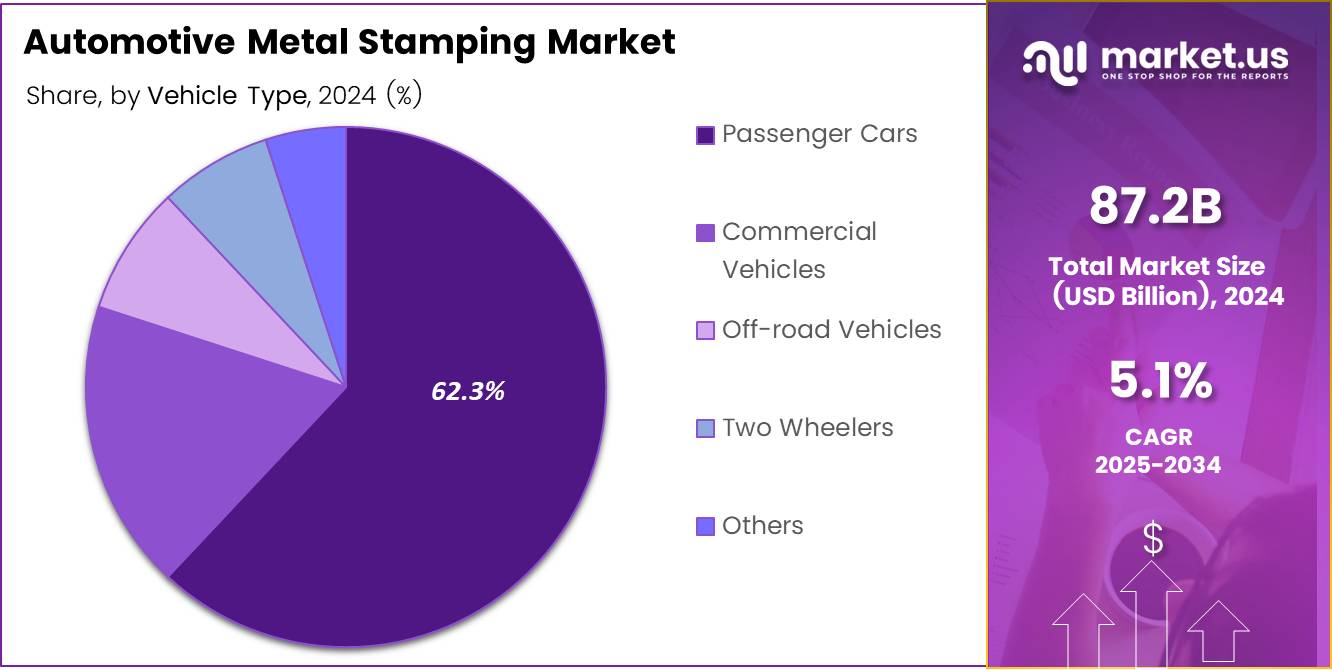

- Passenger cars held the largest market share (62.3%) within the vehicle type segment in 2024.

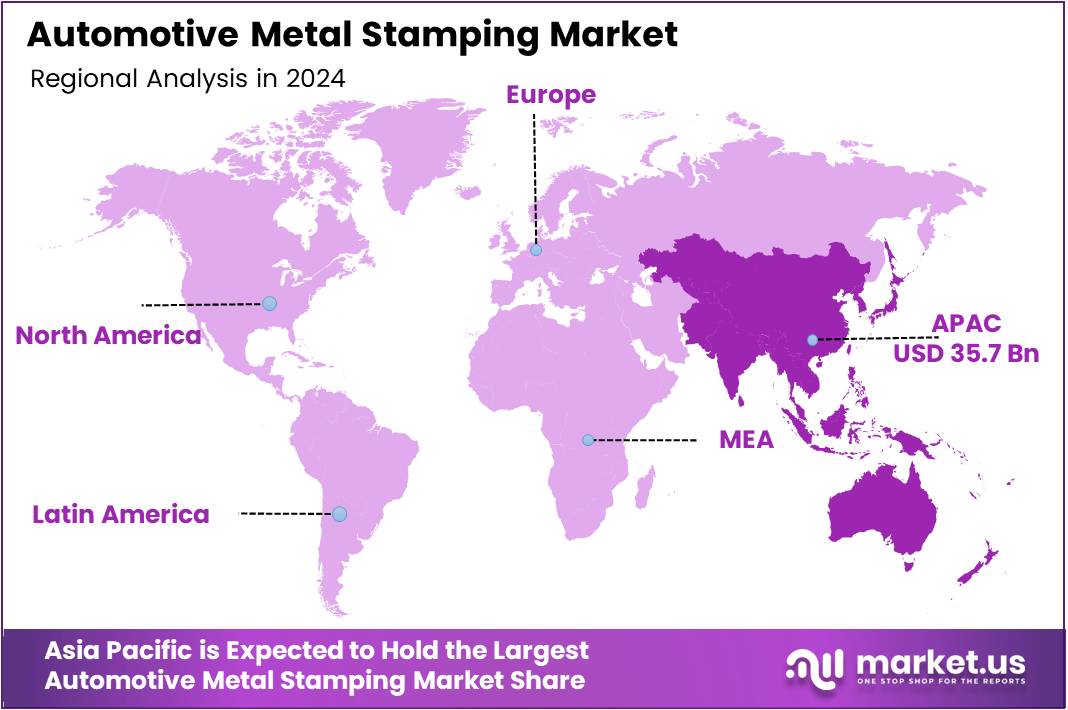

- Asia Pacific leads the market with a 41.2% share, driven by major automotive manufacturers in China, Japan, South Korea, and India.

Process Analysis

Blanking Leads with 40.5% in Automotive Metal Stamping’s By Process Analysis

In 2024, Blanking held a dominant market position in the By Process Analysis segment of the Automotive Metal Stamping Market, boasting a 40.5% share. This process, vital for its precision and efficiency, involves cutting flat metal sheets into appropriate shapes, a crucial step in forming components that meet stringent automotive industry standards.

Following Blanking, Embossing also showed notable market uptake due to its ability to add strength and rigidity to metal sheets through patterning, enhancing both aesthetic and functional qualities of automotive parts.

Bending and Coining processes were also key contributors. Bending, essential for shaping metal parts at specific angles, and Coining, known for its ability to create detailed part features, supported complex component fabrications required in modern vehicles.

Deep Drawing and Flanging processes catered effectively to the demand for deeper or extended objects, playing critical roles in fabricating parts like panels and tanks. The segment labeled as Other includes specialized techniques such as trimming and piercing, which address more specific needs in the automotive stamping process.

This detailed segmentation underlines the diverse technologies propelling the Automotive Metal Stamping Market forward, highlighting the importance of adapting to technological advancements and varying industrial demands.

Material Analysis

Steel Leads the By Material Analysis Segment in Automotive Metal Stamping Market

In 2024, steel held a dominant market position in the By Material Analysis segment of the Automotive Metal Stamping Market. This leadership is largely attributed to steel’s long-standing reputation for reliability and cost-efficiency within the automotive industry. Its inherent strength and durability make it an ideal choice for meeting the rigorous safety and quality standards required in vehicle manufacturing.

Aluminum followed, benefiting from the industry’s pivot towards lightweight materials aimed at improving fuel efficiency and reducing emissions. Its lightness combined with resistance to corrosion makes aluminum an increasingly popular choice, particularly in the production of electric vehicles.

Copper was also notable, primarily for its superior electrical conductivity which is essential in automotive electrical components and wiring systems.

Other materials, including magnesium and titanium, accounted for a smaller portion of the market, chosen for their specific properties such as high strength-to-weight ratios and high-temperature resistance, which are critical in specialized automotive applications.

As the automotive sector evolves with advancements in technology and environmental standards, the material landscape in metal stamping continues to adapt, with steel maintaining its foundational role due to its unmatched cost and performance benefits.

Vehicle Type Analysis

Passenger Cars Lead the Pack in Automotive Metal Stamping with a 62.3% Market Share

In 2024, the Automotive Metal Stamping Market saw Passenger Cars firmly in the lead within the By Vehicle Type Analysis segment, holding a commanding 62.3% market share. This dominant position underscores the sustained demand for passenger vehicles, which continue to be a staple in personal transportation, reflecting broader economic factors such as increased consumer spending power and urbanization.

Following Passenger Cars, Commercial Vehicles also made a significant impact, catering to the continuous expansion of logistic networks and e-commerce, necessitating robust fleets of commercial transport. Off-road Vehicles, while occupying a smaller slice of the market, remain crucial in sectors such as agriculture and construction, where their utility in rugged terrains drives their demand.

Two Wheelers and Other vehicle types represent niche markets within the metal stamping landscape. Two Wheelers are especially prevalent in densely populated urban areas in emerging economies, where cost-effectiveness and mobility are paramount. The category labeled ‘Others’ includes specialized vehicles which, although limited in number, are integral to specific industrial operations, further diversifying the market landscape.

Collectively, these segments illustrate a dynamic and evolving Automotive Metal Stamping Market, driven by diverse demands across various vehicle types.

Key Market Segments

By Process

- Blanking

- Embossing

- Bending

- Coining

- Deep Drawing

- Flanging

- Other

By Material

- Steel

- Aluminum

- Copper

- Other

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Off-road Vehicles

- Two Wheelers

- Others

By End User

- OEM (Original Equipment Manufacturer)

- Tier Automotive Manufacturer

Drivers

Rising Vehicle Production Fuels Automotive Metal Stamping Market Growth

The global surge in automotive production is significantly propelling the automotive metal stamping market. As consumer demand for vehicles climbs, manufacturers are ramping up production, which in turn boosts the need for essential metal components made through stamping processes.

Additionally, the automotive industry’s pivot towards electric vehicles (EVs) is expanding the market further, as these vehicles require specialized stamped metal parts that differ from traditional automotive components.

This shift is not only about quantity but also quality; as manufacturers integrate high-strength materials like advanced steels and aluminum to meet safety and efficiency standards, the metal stamping industry must evolve to offer more sophisticated solutions.

Moreover, metal stamping remains a cost-effective production method for high-volume manufacturing, making it an attractive option for automakers looking to optimize production costs while maintaining high-quality standards in their vehicles.

This convergence of factors—increased vehicle production, the rise of EVs, the integration of high-strength materials, and cost-efficiency—collectively drives the growth of the automotive metal stamping market.

Restraints

Economic Downturns Impact Demand for Automotive Metal Stamping

As an analyst observing the automotive metal stamping market, it’s crucial to recognize that market volatility, particularly economic downturns, significantly influences this sector.

During periods of economic recession, the demand for new vehicles typically diminishes as consumers and businesses alike tighten their budgets. This decline in vehicle production directly impacts the automotive metal stamping market, as fewer cars on the assembly line mean reduced need for stamped metal parts.

Additionally, the presence of substitute technologies such as forging and casting also poses a challenge. These alternatives offer different benefits in terms of durability and cost-effectiveness, which can divert potential growth from the metal stamping market, especially in segments where material properties and production efficiency are paramount.

This competitive environment demands that stakeholders in the metal stamping market stay agile and innovate continuously to maintain their market position and navigate through these restraints effectively.

Growth Factors

Innovations in Metal Stamping Techniques Propel Market Expansion

As an analyst observing the automotive metal stamping market, the emergence of innovative stamping techniques presents significant growth opportunities. These new methods are geared towards enhancing efficiency and reducing waste during production, potentially capturing a larger share of the market.

Additionally, there’s a rising trend towards the development of sustainable stamping solutions that minimize environmental impact, aligning with global sustainability goals. The market also benefits from improved recycling practices, where companies are increasingly recycling metal waste back into the production cycle, further reducing costs and environmental footprint.

Moreover, there is a growing demand from the luxury and sports car sectors, which require high precision and customized metal parts. These factors collectively contribute to the vibrant growth prospects in the automotive metal stamping market, making it an attractive area for investments and innovation.

Emerging Trends

3D Printing Revolutionizes Stamping Die Manufacturing

In the automotive metal stamping market, one of the key trending factors is the adoption of 3D printing for producing stamping dies. This innovation significantly reduces both the time and costs associated with die manufacturing, thereby enhancing production efficiencies.

Another prominent trend is the custom stamping for niche markets, including the production of specific components for electric vehicles (EVs) and bespoke designs that cater to unique customer demands.

Furthermore, an increasing number of Original Equipment Manufacturers (OEMs) are opting for vertical integration, bringing stamping operations in-house to better control costs and maintain quality. This shift is complemented by the expansion of servicing and repair networks, which boosts the demand for stamped parts necessary for maintenance and repair activities.

These trends collectively signal a dynamic phase of growth and adaptation in the automotive metal stamping market, driven by technological advancements and strategic industry shifts.

Regional Analysis

Asia Pacific Leads the Automotive Metal Stamping Market with 41.2% Share and USD 35.7 Billion

The global automotive metal stamping market is experiencing significant growth, with varying dynamics across different regions. Asia Pacific holds the largest share of the market, contributing approximately 41.2% of the global market revenue, valued at USD 35.7 billion. This dominance is driven by the presence of major automotive manufacturers in countries like China, Japan, South Korea, and India.

Additionally, Asia Pacific’s burgeoning automotive industry, combined with increasing vehicle production rates, bolsters demand for metal stamping components. Rising disposable income and expanding middle-class populations in the region further contribute to the demand for automotive parts, thus accelerating market growth.

Regional Mentions:

In North America, the automotive metal stamping market is projected to continue expanding, driven by robust automotive production in the United States and Mexico. The region’s focus on technological advancements and lightweight materials also propels the demand for precision metal stamping solutions.

Europe also holds a strong position in the automotive metal stamping market, supported by the presence of renowned automobile manufacturers, particularly in Germany, France, and the UK. The region’s emphasis on sustainability and the transition toward electric vehicles enhances demand for efficient manufacturing processes, including metal stamping.

The Middle East & Africa market is smaller in comparison, but it shows promising growth due to the increasing automotive manufacturing activities in countries like South Africa and the UAE, coupled with a rise in infrastructure projects.

Latin America is a growing market for automotive metal stamping, with Brazil being the key player in the region. The demand for automotive parts is expected to increase as the automotive industry continues to expand in the region, albeit at a slower rate compared to other regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global Automotive Metal Stamping Market continues to be driven by key players focused on innovation, efficiency, and meeting the increasing demand for lightweight, high-performance components. Among the leading companies, Ford Motor Company and General Motors (GM) are standout participants, with significant investments in electric vehicle (EV) production and sustainability.

These automakers’ commitment to cutting-edge manufacturing techniques is driving the demand for precision stamping of components, such as body panels, chassis, and structural parts, that are essential for both internal combustion engine (ICE) vehicles and EVs.

Tempco Manufacturing, CAPARO, and Goshen Stamping Company are strengthening their positions in the sector through technological advancements and an expanding portfolio of offerings. These companies focus on enhancing the accuracy, quality, and cost-effectiveness of metal stamping processes. They are also increasingly leveraging automation and robotics to boost operational efficiency, which is essential in responding to the rising production volumes and regulatory demands for emission reductions.

Nissan, FCA (now part of Stellantis), and AAPICO Hitech Public Company Limited are also crucial players, driving market growth through partnerships and the introduction of new vehicle models. AAPICO, in particular, is expanding its presence in Asia with a focus on providing high-quality stamped parts to a wide range of OEMs.

Gestamp and Kenmode, Inc., known for their advanced stamping technology, are leading the charge in lightweight materials and complex stamping processes. They are particularly well-positioned to capitalize on the increasing demand for electric vehicles and hybrid models, where lightweight, durable components are essential to improving vehicle efficiency.

Top Key Players in the Market

- Ford Motor Company

- Tempco Manufacturing Company, Inc.

- CAPARO

- Nissan Motor Co., Ltd

- FCA

- Goshen Stamping Company

- D&H Industries, Inc.

- Gestamp

- Kenmode, Inc.

- General Motors

- AAPICO Hitech Public Company Limited

- American Industrial Co.

Recent Developments

- In August 2024, Mexican company GIMSA will invest $40 million to establish a new metal stamping plant for the automotive industry, aimed at increasing production capacity and meeting growing demand. This facility will focus on manufacturing high-precision components for the automotive sector, enhancing GIMSA’s capabilities in the global market.

- In June 2024, Martinrea will invest nearly $35 million to expand its Ridgetown, Ontario facility, which includes the addition of a 3000T stamping press. The new equipment will allow the company to produce larger, more complex automotive parts, supporting the growing needs of its OEM customers.

- In June 2023, General Motors announced a $1 billion investment into its Flint, Michigan ICE truck plants. The investment will modernize the plants, enhance production efficiency, and support the production of upcoming models, reaffirming GM’s commitment to the future of internal combustion engine vehicles.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 87.2 Billion |

| Forecast Revenue (2034) | USD 143.4 Billion |

| CAGR (2025-2034) | 5.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Process (Blanking, Embossing, Bending, Coining, Deep Drawing, Flanging, Other), By Material (Steel, Aluminum, Copper, Other), By Vehicle Type (Passenger Cars, Commercial Vehicles, Off-road Vehicles, Two Wheelers, Others), By End User (OEM, Tier Automotive Manufacturer) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ford Motor Company, Tempco Manufacturing Company, Inc., CAPARO, Nissan Motor Co., Ltd, FCA, Goshen Stamping Company, D&H Industries, Inc., Gestamp, Kenmode, Inc., General Motors, AAPICO Hitech Public Company Limited, American Industrial Co. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |