Quick Navigation

Report Overview

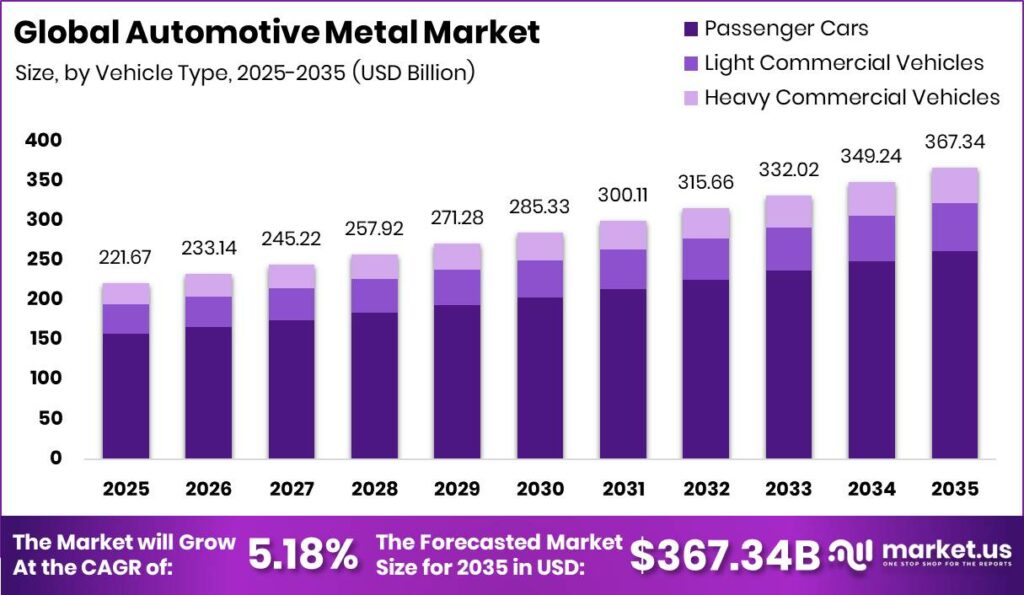

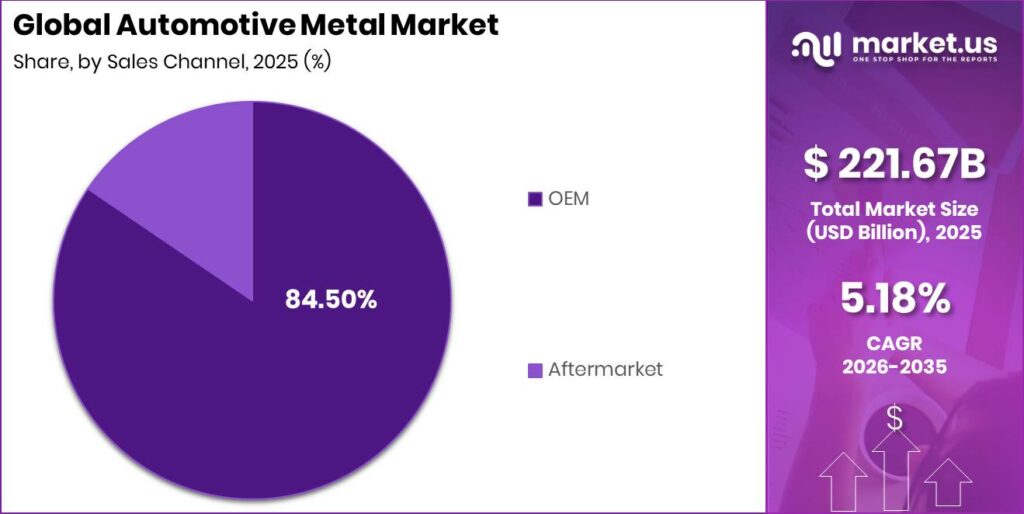

Global Automotive Metal Market size is expected to be worth around USD 367.34 Billion by 2035 from USD 221.67 Billion in 2025, growing at a CAGR of 5.18% during the forecast period 2026 to 2035. Automotive metals form the structural foundation of modern vehicles. Manufacturers utilize steel and aluminum to construct passenger cabins, chassis frameworks, and powertrain assemblies. This market encompasses the production and supply of these essential raw materials to automotive fabricators.

Therefore, material selection dictates vehicle safety ratings and fuel efficiency metrics globally. Automakers continually balance raw metal weight against stringent crash test performance requirements. The industry strictly prioritizes engineered alloys that reduce overall vehicle mass without compromising passenger structural integrity. This creates immediate procurement shifts toward automotive advanced high strength steel and lightweight aluminum compounds for modern assembly lines. Consequently, metal suppliers must upgrade their forming capabilities.

Key Takeaways

- The Global Automotive Metal Market size will reach USD 367.34 Billion by 2035, exhibiting a CAGR of 5.18%.

- Steel dominates the metal type segment with a 61.80% market share.

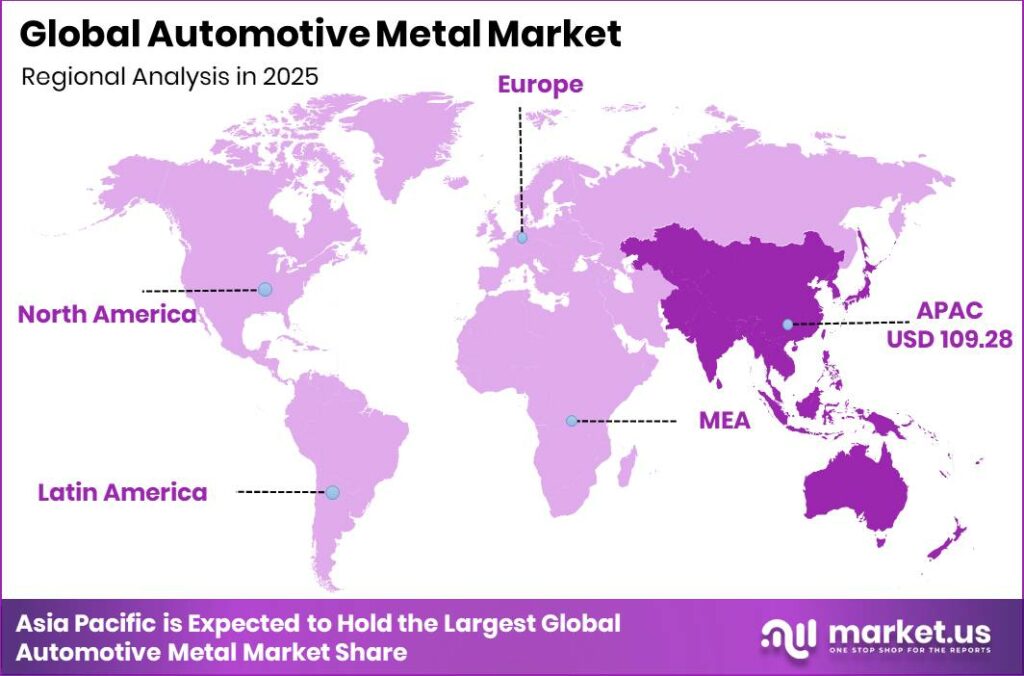

- Asia Pacific leads the global market with a 49.30% share, valued at USD 109.28 Billion.

Government emission regulations force strict lightweighting mandates across the broader automotive sector. Regulatory bodies impose heavy financial penalties on manufacturers failing to meet corporate average fuel economy standards. This mandates a rapid transition away from heavy conventional materials toward automotive lightweight materials. Suppliers heavily align their production pipelines with these rigid regulatory constraints. Consequently, automakers vastly accelerate the integration of high-grade automotive metals to absolutely achieve mandatory compliance.

Data from the World Steel Association indicates that automotive manufacturing accounts for 12% of total global steel use by end-use sector, exposing steelmakers heavily to vehicle production cycles. Any disruption in passenger car assembly immediately impacts mill order volumes. As reported by the OECD, global steel production will grow at an average annual rate of 0.9% between 2025 and 2030. This slow capacity expansion tightens the supply of premium automotive grades, forcing buyers to accept higher contract pricing.

Metal Type Analysis

Steel dominates with 61.80% due to superior tensile strength and basic affordability.

In 2025, Steel held a dominant market position in the Metal Type segment of the Automotive Metal Market, with a 61.80% share. Global steel production reached 1,888 million tonnes in 2024, and automakers consumed nearly 12% of this total volume. This massive consumption relies on established global supply chains and clear cost advantages over alternative metals. Manufacturers securing long-term steel procurement contracts effectively insulate their profit margins against short-term commodity pricing volatility.

Application Analysis

Body Structure & Chassis dominates with 42.60% due to massive vehicle frame material requirements.

In 2025, Body Structure & Chassis held a dominant market position in the Application segment of the Automotive Metal Market, with a 42.60% share. A standard light-duty Automotive Chassis requires roughly 400 kilograms of raw material, while US automakers utilize approximately 3.9 million tonnes of specialized metals annually for body assemblies. This heavy material concentration represents the largest single cost center in vehicle fabrication. Suppliers dominating this structural category consistently capture the highest revenue volume per vehicle produced.

Vehicle Type Analysis

Passenger Cars dominates with 71.40% due to extremely high global consumer fleet volumes.

In 2025, Passenger Cars held a dominant market position in the Vehicle Type segment of the Automotive Metal Market, with a 71.40% share. Global production facilities assembled over 67 million passenger units during 2024, with factory utilization rates in major manufacturing hubs exceeding 75% for personal transport lines. This massive volume requires uninterrupted daily metal deliveries to prevent extremely costly assembly stoppages. Therefore, material suppliers aggressively prioritize passenger vehicle contracts to secure stable long-term baseline revenue.

Sales Channel Analysis

OEM dominates with 84.50% due to standardized factory mass material procurement contracts.

In 2025, OEM held a dominant market position in the Sales Channel segment of the Automotive Metal Market, with an 84.50% share. Major automotive groups execute direct supply agreements covering up to 5 million tonnes of metal annually, representing nearly 90% of their total raw material spending. Direct factory purchasing eliminates intermediary markups and completely guarantees strict metallurgical quality control. Consequently, metal producers lock in guaranteed multi-year demand that easily justifies new billion-dollar processing facility investments.

Key Market Segments

By Metal Type

- Steel

- Aluminum

- Magnesium

- Copper

- Titanium

- Others

By Application

- Body Structure & Chassis

- Powertrain Components

- Suspension Components

- Wheels & Tires Components

- Interior Components

- Electrical & Electronic Components

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Sales Channel

- OEM

- Aftermarket

Regional Analysis

Asia Pacific Dominates the Automotive Metal Market with a Market Share of 49.30%, Valued at USD 109.28 Billion

Asia Pacific commands the global landscape due to overwhelming vehicle manufacturing density across China and India. Local mills output massive volumes of flat-rolled steel, directly feeding adjacent automotive assembly hubs with minimal logistics costs. Regional governments actively subsidize heavy industrial expansion to maintain export competitiveness and protect localized supply chains. As a result, domestic material suppliers capture nearly all regional sector growth while entirely blocking foreign metal producers.

North America represents the fastest-growing territory, driven heavily by aggressive legislative pushes toward domestic electric vehicle production. Federal infrastructure investments compel automakers to redesign architectures around Automotive Aluminum to properly offset heavy battery pack weights. Regional supply chain restructuring forces the rapid construction of new domestic processing lines to avoid trans-Pacific shipping delays. Consequently, investors aggressively fund advanced metal stamping facilities directly alongside existing American automotive corridors.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Localized electric vehicle supply chains and new commercial fleets present critical entry windows

Automakers in the United States aggressively pursue domestic metal sourcing to legally comply with lucrative federal electric vehicle incentive frameworks. Current supply networks remain heavily reliant on imported structural components, exposing assembly lines to severe tariff and shipping volatility. The push toward domestic assembly creates immediate demand for newly localized metal processing and forming lines. Therefore, early investors establishing advanced stamping operations within the North American corridor will quickly capture these displaced import volumes.

The lightweight commercial vehicle sector across Asia Pacific remains severely underexploited by advanced lightweight material suppliers. Regional manufacturers historically utilized heavy conventional steels for these utility fleets to ruthlessly maximize upfront production margin. However, aggressive new regional emission targets now force these aging commercial platforms to shed excess mass rapidly. Upgrading these extensive commercial structures with Automotive Composites unlocks an entirely new high-volume revenue channel for proactive mid-tier metal suppliers entering the Asian ecosystem.

Electric vehicle battery enclosures represent a massively underserved niche within the broader global passenger car segment. Automakers currently struggle to perfectly balance thermal management requirements with structural crash safety in lower-floor battery pack designs. Transitioning these specific enclosures from heavy steel plates toward specialized lightweight metals reduces overall vehicle weight dramatically. Consequently, specialized metal extruders focusing strictly on underbody battery protection hardware currently face virtually zero established market competition from legacy component suppliers.

Technology and Innovation Landscape - Advanced forming techniques and zero-carbon metallurgy reshape fundamental production economics

The integration of extreme hot-stamping processes completely revolutionizes the deployment of third-generation advanced high-strength steels. Traditional cold-forming methods cannot manipulate these ultra-rigid grades without inducing severe microscopic fractures in the underlying material structure. New specialized thermal presses solve this by simultaneously heating and instantly quenching the metal within a 20-second cycle. As a result, automakers can successfully form complex single-piece structural geometries that drastically reduce the total number of required welded frame components.

Continuous galvanizing lines engineered specifically for high-stress applications represent a truly critical manufacturing breakthrough for modern vehicle architecture. These advanced coating operations apply highly uniform protective zinc layers directly to specialized steel substrates rated up to 1180 MPa. This specific technology permanently eliminates the severe corrosion vulnerabilities previously associated with ultra-thin high-tensile vehicle frames. This means suppliers wielding these advanced coating lines secure exclusive premium vendor status by guaranteeing decades of operational integrity.

Decarbonized metallurgy utilizing hydrogen direct reduced iron effectively eliminates the massive carbon footprint historically tied to traditional blast furnaces. This green production pathway actively bypasses coal-intensive melting stages, successfully dropping embedded emissions below one tonne of carbon per metal tonne. Scaling this specific zero-carbon technology directly shields global automotive end-users from impending aggressive cross-border carbon taxation penalties. Therefore, early green metallurgy adopters command unprecedented market price premiums while allowing vehicle brands to market fully verified zero-emission supply chains.

Drivers

The sustained recovery of global vehicle production significantly boosts structural metal consumption across all major manufacturing corridors. Annual light vehicle output is stabilizing around 90 million units, directly driving heavy utilization of automotive-grade steel and aluminum processing mills. Each vehicle requires up to 1,100 kilograms of metal, immediately filling supplier order books and restoring crucial pricing power on long-term contracts. Consequently, these restored profit margins enable aggressive capital investments into advanced press-hardened steel capabilities.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Vehicle Production Recovery & Fleet Expansion Sustaining Structural Metal Demand | +1.55% | China, India, Southeast Asia, North America | Short term (≤ 2 years) |

| Lightweighting Mandates Driving Advanced High-Strength Steel & Aluminium Alloy Adoption | +1.20% | Global — led by Europe, North America, Japan | Medium term (2–4 years) |

| EV Platform Structural Architecture Shifting to Aluminium & High-Grade Steel Intensive Designs | +0.95% | China, Europe, North America, South Korea | Medium term (2–4 years) |

| Commercial Vehicle Fleet Renewal & Infrastructure-Linked Demand Expansion | +0.80% | India, China, Brazil, North America | Short term (≤ 2 years) |

| Crash Safety Regulatory Upgrades Increasing Structural Metal Content per Vehicle | +0.65% | India, ASEAN, Latin America, Middle East | Medium term (2–4 years) |

| Nearshoring & Regional Supply Chain Restructuring Expanding Domestic Metal Processing Capacity | +0.38% | Mexico, Eastern Europe, India, Vietnam | Medium term (2–4 years) |

Restraints

China’s structural steel overcapacity, exceeding 200 million metric tonnes, creates severe downward pricing pressure globally. High export volumes of competitively priced cold-rolled grades artificially suppress international hot-rolled coil benchmark prices across all major markets. This structural price floor compression actively damages the profitability of non-Chinese metal producers who bear significantly higher regional energy costs. Therefore, critical green steel and emission-reduction investment projects face repeated indefinite delays due to fundamentally damaged return projections.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chinese Steel Overcapacity & Dumping Suppressing Global Automotive Metal Pricing | -1.30% | Global — most acute in Southeast Asia, Middle East, Europe | Short term (≤ 2 years) |

| US Section 232 & EU Carbon Border Adjustment Tariffs Disrupting Metal Trade Flows | -0.80% | United States, European Union, Canada, Mexico | Short term (≤ 2 years) |

| Material Substitution by Composites & Plastics Eroding Metal Content per Vehicle | -0.55% | Europe, North America, Japan | Medium term (2–4 years) |

| High Energy Costs Compressing Steel & Aluminium Smelting Margins in Europe | -0.42% | European Union, United Kingdom | Short term (≤ 2 years) |

| Iron Ore & Bauxite Price Volatility Creating Input Cost Instability | -0.30% | Global — most acute in import-dependent emerging markets | Short term (≤ 2 years) |

Challenges

The rapid adoption of third-generation advanced high-strength steels severely outpaces the available technical workforce. Modern press-hardened steels require extreme hot-stamping processes and specialist engineers with extensive operational training. Developing manufacturing hubs in emerging markets face massive capability shortfalls, leading to first-article rejection rates peaking near 15%. This high scrap rate immediately inflates vehicle program launch budgets. This means Tier-1 suppliers must internally finance extensive multi-year vocational training programs before authorizing local production.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| AHSS & PHS Forming Skill Deficit | -0.70% | South Asia, Southeast Asia, Eastern Europe, Latin America | Long term (≥ 4 years) |

| Automotive Steel Decarbonisation Transition Cost | -0.60% | European Union, United Kingdom, Japan, South Korea | Long term (≥ 4 years) |

| Multi-Material Joining & Dissimilar Metal Compatibility | -0.50% | Global — concentrated in EV & premium OEM programs | Medium term (2–4 years) |

| Scrap Quality & Circular Economy Integration | -0.40% | Europe, North America, Japan | Long term (≥ 4 years) |

| OEM Supplier Consolidation Reducing Tier-2 Metal Processor Margins | -0.33% | North America, Europe, Japan | Medium term (2–4 years) |

Opportunities

Strict corporate sustainability mandates generate massive procurement demand for fully certified low-carbon automotive steel. The phased implementation of European carbon border tariffs penalizes conventional imported materials, which fundamentally alters core structural material economics. Low-carbon steel currently commands strong market premiums, unlocking substantial gross margin expansion for verified green metal producers. This creates a highly profitable, multi-year runway for early movers deploying zero-carbon metallurgical capacity while the severe global supply deficit persists.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Green & Low-Carbon Steel Premium Monetisation via OEM Sustainability Mandates | +1.45% | European Union, Japan, North America, South Korea | Medium term (2–4 years) |

| EV Battery Enclosure & Structural Pack Integration in High-Grade Aluminium | +1.00% | China, Europe, North America | Medium term (2–4 years) |

| Closed-Loop Automotive Scrap Recycling & Circular Metal Economy Buildout | +0.75% | European Union, Japan, United States | Long term (≥ 4 years) |

| India & ASEAN Domestic Automotive Steel Capacity Investment | +0.60% | India, Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

| Magnesium Alloy Adoption for Ultra-Lightweight Structural Components | +0.40% | China, Japan, Germany, South Korea | Long term (≥ 4 years) |

Key Company Insights

ArcelorMittal S.A. strengthens its structural positioning through targeted infrastructure expansions in the electrical steel segment. By constructing a new manufacturing facility in Alabama during 2025, the company directly targets the expanding electric vehicle motor supply chain. This localized American footprint shields the manufacturer from transatlantic import tariffs. This means they capture high-margin early contracts from domestic automakers launching next-generation platforms.

POSCO Holdings Inc. utilizes massive Asian production capacity to absolutely dominate regional material procurement channels. The supplier integrates advanced metallurgical processing directly alongside major Korean and Chinese vehicle assembly hubs. This geographic advantage drastically cuts shipping delays for high-volume automotive clients requiring continuous material feeds. Consequently, the firm blocks smaller challengers from displacing its foundational structural supply agreements across the continent.

Key Players

- ArcelorMittal S.A.

- POSCO Holdings Inc.

- Nippon Steel Corporation

- SSAB AB

- Novelis Inc.

- Constellium SE

- Norsk Hydro ASA

- Gerdau S.A.

- United States Steel Corporation

- Tata Steel Limited

- Baosteel Group Corporation

- Voestalpine AG

Recent Developments

- July 2025: AM/NS India commissioned India’s first Continuous Galvanising Line capable of producing Advanced High-Strength Steel up to 1180 MPa specifically for automotive manufacturing.

- September 2025: ArcelorMittal began serial deliveries of low-carbon Usibor 1500 XCarb steel to Renault Group for structural components used in its next-generation battery electric vehicles.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 221.67 Billion |

| Forecast Revenue (2035) | USD 367.34 Billion |

| CAGR (2026-2035) | 5.18% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | Metal Type (Steel, Aluminum, Magnesium, Copper, Titanium, Others), Application (Body Structure & Chassis, Powertrain Components, Suspension Components, Wheels & Tires Components, Interior Components, Electrical & Electronic Components), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ArcelorMittal S.A., POSCO Holdings Inc., Nippon Steel Corporation, SSAB AB, Novelis Inc., Constellium SE, Norsk Hydro ASA, Gerdau S.A., United States Steel Corporation, Tata Steel Limited, Baosteel Group Corporation, Voestalpine AG |

| Customization Scope | Customization for segments, region / country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License | Multi-User License (Up to 5 Users) | Corporate Use License (Unlimited User and Printable PDF) |