Global Functional Protein Market Size, Share, Business Environment Analysis By Type (Whey protein concentrates, Whey protein isolates, Hydrolysates, Casein/Caseinates, Soy protein, Others), By Source (Animal, Plant), By Form (Dry, Liquid), By Functionality (Muscle Building and Recovery, Weight Management, Bone and Joint Health, Beauty and Skincare, Others), By Application (Functional Food, Functional Beverages, Dietary Supplements, Animal Nutrition, Sports Nutrition, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2024-2033

- Published date: Dec 2024

- Report ID: 136231

- Number of Pages: 211

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

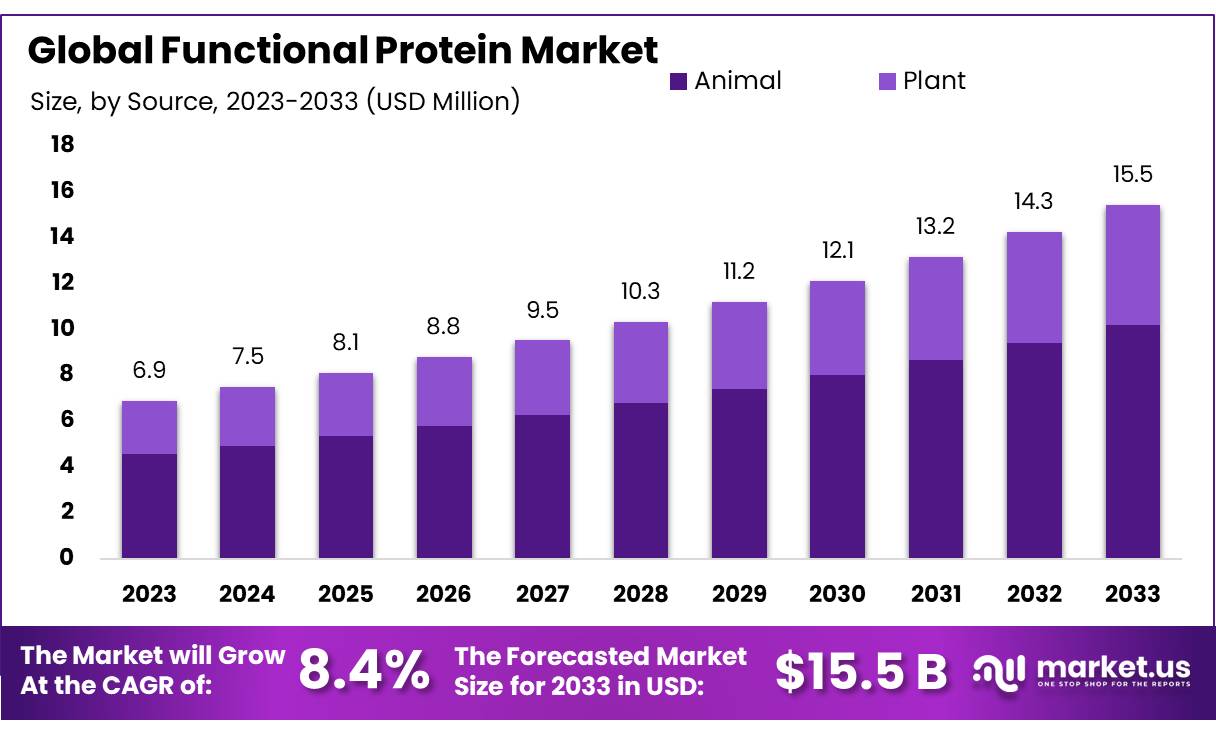

The Global Functional Protein Market size is expected to be worth around USD 15.5 Bn by 2033, from USD 6.9 Bn in 2023, growing at a CAGR of 8.4% during the forecast period from 2024 to 2033.

The functional protein market has been experiencing significant growth, driven by various end-use industries, government regulations, market dynamics, and investments from both public and private sectors.

The global demand for functional proteins has been increasing due to rising health awareness, fitness trends, and dietary preferences. According to the U.S. Department of Agriculture (USDA), the global protein market, particularly functional proteins, is expected to grow at a CAGR of 7.4% from 2023 to 2028.

In 2023, the nutraceuticals and dietary supplements industry accounted for the largest share of the functional protein market. The segment generated approximately $7.5 billion in revenue, with sports nutrition and weight management products being the primary drivers. Protein-enriched snacks and beverages have become increasingly popular, with the global protein beverages market estimated at $9.5 billion in 2023 and projected to grow at a CAGR of 8.1% by 2026.

The food and beverage sector is also experiencing a surge in demand for plant-based and dairy protein products, particularly soy, pea, and whey proteins. This has led to an increase in production and innovations such as plant-based protein shakes, which saw an 8.5% increase in sales in 2023 compared to the previous year.

Governments worldwide are implementing regulations and providing support to boost protein production. In the United States, the FDA (Food and Drug Administration) regulates protein labeling to ensure consumers receive accurate nutritional information. The European Food Safety Authority (EFSA) sets guidelines on protein content in food products, especially for those targeting vulnerable populations, like the elderly and children.

Governments are also fostering innovation in the protein sector through grants and initiatives. In 2023, the European Union (EU) allocated €120 million to support the development of plant-based protein alternatives, as part of its Green Deal initiative to promote sustainable farming. Additionally, the U.S. government announced an investment of $25 million in plant-based protein research and innovation through the National Institute of Food and Agriculture (NIFA).

The global trade of functional proteins is expanding rapidly, especially with countries like the U.S., China, and Germany being major exporters and importers of protein products. In 2023, the U.S. exported approximately $3.8 billion worth of protein products, including whey, soy, and casein, to global markets, with a significant portion going to China and Mexico.

On the import side, China remains the largest importer of functional proteins, especially whey protein, accounting for over 30% of global imports in 2023. The country’s demand for functional proteins is driven by increasing health-consciousness among the population and the growing prevalence of fitness and bodybuilding activities.

2023 saw several key investments and partnerships aimed at advancing the functional protein industry. For example, Nestlé Health Science invested $50 million in Mooala, a company that focuses on plant-based protein products, marking a strong shift towards plant-based protein options. Additionally, ADM (Archer Daniels Midland) partnered with Bunge Limited in a joint venture to create a new plant-based protein production facility in the Midwest. This partnership is expected to boost U.S. production capacity by 20% by 2024.

In terms of acquisitions, Danone acquired the U.S.-based company WhiteWave in 2023, which specializes in plant-based dairy and protein products, strengthening Danone’s position in the functional protein market. This acquisition is expected to increase Danone’s market share in North America by 3.5%.

Key Takeaways

- Functional Protein Market size is expected to be worth around USD 15.5 Bn by 2033, from USD 6.9 Bn in 2023, growing at a CAGR of 8.4%.

- Whey Protein Concentrates held a dominant market position, capturing more than a 34.5% share.

- Animal proteins held a dominant market position, capturing more than a 66.5% share of the global functional protein market.

- Dry forms held a dominant market position, capturing more than a 76.8% share of the global functional protein market.

- Muscle Building and Recovery held a dominant market position, capturing more than a 47.5% share.

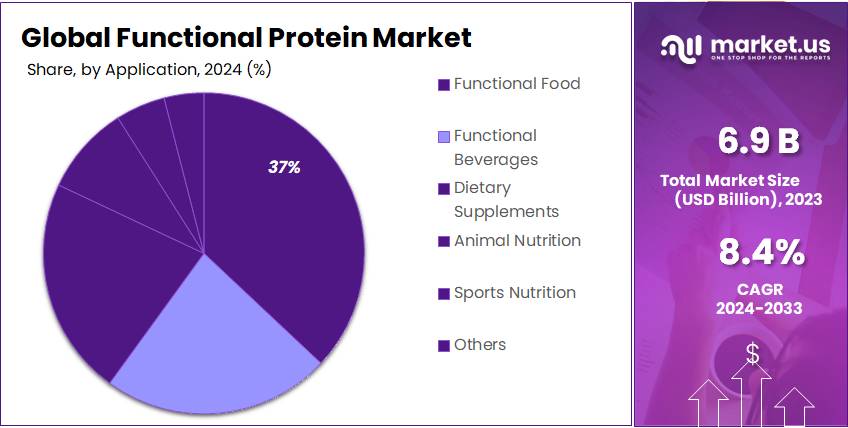

- Functional Food held a dominant market position, capturing more than a 37.1% share of the global functional protein market.

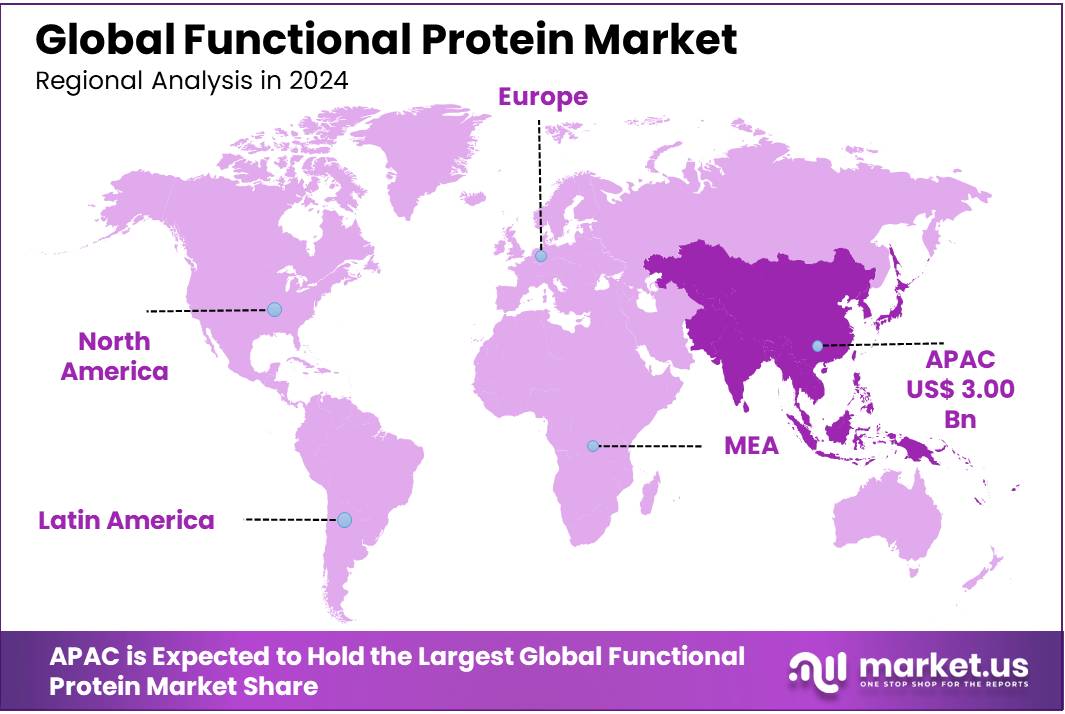

- Asia Pacific is the dominating region, accounting for 43.2% of the market share and valued at USD 3.00 billion.

By Type

In 2023, Whey Protein Concentrates held a dominant market position, capturing more than a 34.5% share of the global functional protein market. This segment’s growth has been driven by its versatility and nutritional benefits, making it a popular choice among athletes, fitness enthusiasts, and health-conscious consumers. Whey protein concentrates offer a rich source of essential amino acids, supporting muscle recovery and overall health, which explains its large share in the market.

Whey Protein Isolates, while slightly smaller in share compared to concentrates, has seen steady growth due to its higher protein content and lower fat levels, appealing to individuals looking for a more refined, low-carb alternative. In 2023, this segment continued to expand, driven by the rising demand for clean-label products and functional foods.

Hydrolysates, another important segment, accounted for a significant portion of the market in 2023. These proteins are pre-digested for faster absorption, making them highly sought after in both sports nutrition and medical nutrition products. The market for hydrolysates has been increasing steadily as more consumers seek proteins with enhanced bioavailability.

Casein/Caseinates have maintained a steady market presence, particularly among consumers looking for slow-digesting proteins. Known for its sustained-release benefits, casein continues to be popular in the meal-replacement and nighttime protein supplement markets. This segment showed moderate growth in 2023, catering to niche demands in both the nutrition and functional food industries.

Soy Protein has witnessed a slight but consistent increase in demand. As a plant-based protein, it appeals to the growing vegan and vegetarian population. It’s also a preferred choice for people with lactose intolerance, contributing to its steady market presence in 2023.

By Source

In 2023, Animal proteins held a dominant market position, capturing more than a 66.5% share of the global functional protein market. This strong market presence is primarily driven by the widespread use of animal-derived proteins such as whey, casein, and egg proteins, which are known for their high biological value and rich amino acid profiles. These proteins continue to dominate due to their proven effectiveness in promoting muscle growth, recovery, and overall health, making them the preferred choice for athletes, bodybuilders, and fitness enthusiasts.

The Plant protein segment, while smaller in comparison, has been gaining traction over recent years, driven by the increasing consumer shift towards plant-based diets. In 2023, the plant protein market continued its upward trajectory, fueled by growing demand for vegan and vegetarian protein options, as well as increasing awareness of the environmental and ethical benefits of plant-based sources. While plant proteins like soy, pea, and rice are still a smaller part of the overall market, their popularity is steadily increasing, especially among consumers seeking dairy-free or lactose-free alternatives.

By Form

In 2023, Dry forms held a dominant market position, capturing more than a 76.8% share of the global functional protein market. This segment’s strong performance is largely due to the convenience, longer shelf life, and cost-effectiveness of dry protein powders. These dry forms, which include protein isolates, concentrates, and hydrolysates, are widely used in a variety of applications such as sports nutrition, weight management, and meal replacement products. Their versatility in product formulations—ranging from shakes to protein bars—has made them the preferred choice for both manufacturers and consumers.

The Liquid form of functional proteins, while smaller in market share, has seen steady growth in recent years. The appeal of liquid protein products lies in their convenience and ease of consumption, especially for those who prefer ready-to-drink options. This segment includes protein beverages, liquid meal replacements, and fortified beverages, which are gaining popularity due to their quick absorption and portability. In 2023, the liquid protein segment continued to experience a rise in demand, driven by the growing on-the-go lifestyle and the increasing number of health-conscious consumers seeking quick, effective protein sources.

Although dry forms still dominate the market, liquid proteins are expected to expand in the coming years, particularly with innovations in packaging and formulations that improve taste, shelf life, and convenience. However, dry protein products will likely maintain a dominant position in the functional protein market, continuing to appeal to a broad range of consumers due to their efficiency, versatility, and established market presence.

By Functionality

In 2023, Muscle Building and Recovery held a dominant market position, capturing more than a 47.5% share of the global functional protein market. This segment’s strong performance is largely driven by the increasing demand for proteins that support athletic performance, muscle repair, and overall fitness goals.

As more consumers engage in fitness routines, particularly weight training and endurance sports, the need for high-quality protein to aid in muscle growth and recovery has surged. This trend is expected to continue as fitness awareness grows worldwide, with muscle-building proteins remaining the go-to choice for both casual gym-goers and professional athletes.

The Weight Management segment also experienced steady growth in 2023, accounting for a significant portion of the market. Functional proteins, especially those with lower calories and high satiety benefits, have become increasingly popular among individuals seeking to manage their weight.

These proteins help curb hunger, boost metabolism, and support lean muscle mass while assisting in fat loss. The increasing trend of health-conscious living, coupled with the demand for convenient, protein-rich meal replacements and snacks, has contributed to the steady rise of this segment.

Bone and Joint Health continued to show moderate growth in 2023, with consumers increasingly recognizing the importance of protein in supporting musculoskeletal health. Collagen-based proteins, in particular, have gained attention due to their potential benefits for joint flexibility and bone density, particularly in aging populations. This segment remains niche but is expanding as awareness around joint health and aging populations grows.

The Beauty and Skincare segment, while smaller compared to muscle building and weight management, has been gaining traction, particularly with the rise of “beauty from within” trends. Functional proteins, including collagen and peptides, are being marketed for their potential to improve skin elasticity, reduce wrinkles, and support healthy hair and nails. In 2023, this segment showed signs of growth, driven by an increasing consumer interest in holistic beauty and wellness products.

By Application

In 2023, Functional Food held a dominant market position, capturing more than a 37.1% share of the global functional protein market. This segment’s strong growth can be attributed to the increasing consumer preference for protein-enriched foods that offer additional health benefits beyond basic nutrition.

Functional foods, such as protein bars, fortified snacks, and ready-to-eat meals, are becoming essential parts of modern diets as people seek to improve their overall health, manage weight, and support specific health goals like muscle growth or bone health. The growing demand for convenience and clean-label products is further driving the popularity of functional food products in the market.

Functional Beverages also showed a steady rise in 2023, capturing a significant portion of the market. With the growing trend of on-the-go lifestyles, consumers are increasingly turning to protein-infused beverages like shakes, smoothies, and protein water for quick, convenient nutrition.

These beverages not only offer hydration but also provide added nutritional value, making them a preferred choice for fitness enthusiasts and health-conscious individuals looking for an easy way to boost their protein intake. As more companies innovate with flavor, texture, and packaging, the functional beverage segment is expected to continue growing.

Dietary Supplements accounted for a considerable share of the market as well, continuing to see strong demand, particularly in the form of protein powders and capsules. These products are popular among consumers who prioritize specific health benefits, such as muscle recovery, weight management, or joint health. In 2023, the market for dietary supplements remained robust, driven by increasing awareness about personal wellness and a greater focus on preventive healthcare.

Animal Nutrition, though a smaller segment, showed steady growth, particularly in markets where livestock production and pet health are major concerns. Animal protein supplements are being used to improve the growth, health, and productivity of livestock, while also gaining traction in the pet food industry for its potential to enhance the health and longevity of pets. As the demand for sustainable and high-quality animal nutrition products grows, this segment is expected to expand further.

Sports Nutrition continued to perform well in 2023, as athletes and fitness enthusiasts increasingly turn to functional protein products to support their performance and recovery. Protein shakes, bars, and other sports nutrition products are essential for muscle building and repair, and with the rise of sports participation and fitness culture, this segment remains a strong player in the market.

Key Market Segments

By Type

- Whey protein concentrates

- Whey protein isolates

- Hydrolysates

- Casein/Caseinates

- Soy protein

- Others

By Source

- Animal

- Plant

By Form

- Dry

- Liquid

By Functionality

- Muscle Building and Recovery

- Weight Management

- Bone and Joint Health

- Beauty and Skincare

- Others

By Application

- Functional Food

- Functional Beverages

- Dietary Supplements

- Animal Nutrition

- Sports Nutrition

- Others

Drivers

Growing Health Consciousness and Demand for Convenient Nutrition

As more people become aware of the link between diet and health, there has been an increasing demand for foods and beverages that offer more than just basic nutrition. Consumers are increasingly seeking functional protein products that provide additional health benefits, such as muscle recovery, weight management, and joint health, alongside their essential nutrient needs.

According to a report by the International Food Information Council (IFIC), 75% of Americans are actively trying to eat more protein in their diets, with 54% of them opting for plant-based protein sources. This shift is driven by a combination of factors, including the rise of lifestyle diseases such as obesity, diabetes, and heart disease, which have led consumers to make more informed dietary choices.

The increasing focus on convenience is another key factor fueling the demand for functional protein products. As people lead busier lives, they are turning to ready-to-consume protein-based products such as protein bars, shakes, and fortified snacks.

The functional food sector, including protein-enriched foods, is benefiting greatly from this shift. According to a report by the Food and Agriculture Organization (FAO), the global demand for functional foods is projected to reach $275 billion by 2025, growing at an annual rate of 6.5%.

Government initiatives and policies have also played a crucial role in promoting healthier eating habits, which indirectly support the growth of the functional protein market. For example, in the United States, the Healthy People 2030 initiative has set nutrition-related goals aimed at improving public health, including increasing the intake of high-quality proteins.

Similarly, the European Food Safety Authority (EFSA) has been promoting the benefits of protein consumption for different age groups and population segments, especially for aging adults who need more protein to maintain muscle mass and prevent sarcopenia (age-related muscle loss).

In 2023, the global sports nutrition market, which includes protein-based products like shakes, powders, and bars, was valued at over $30 billion, and it is expected to grow at a CAGR of 7.9% over the next five years, driven by increasing participation in fitness activities and the growing popularity of gym memberships. A survey by the International Sports Sciences Association (ISSA) found that 62% of gym-goers and athletes regularly consume protein supplements to enhance their performance and recovery.

These driving factors are compounded by a significant shift toward plant-based proteins. According to the Plant Based Foods Association (PBFA), sales of plant-based foods in the U.S. reached $7 billion in 2022, a 27% increase from the previous year. This growth reflects the increasing preference for plant-based, environmentally sustainable, and cruelty-free protein sources.

Restraints

High Cost of Functional Protein Products

One of the major restraining factors for the functional protein market is the high cost of protein-enriched products, which can limit their accessibility to a broader consumer base. While the demand for functional proteins continues to grow due to health trends and fitness awareness, the higher production costs associated with sourcing quality protein, especially from animal-based or specialized plant-based sources, have led to higher retail prices. This, in turn, can make these products less affordable for many consumers, particularly in price-sensitive markets.

In 2023, the cost of whey protein, one of the most popular sources of functional protein, was estimated to be around $5 to $8 per kilogram, depending on the purity level (whey concentrate vs. whey isolate). This is considerably higher than the cost of regular, non-functional food products. For example, the cost of basic protein-rich foods like eggs, chicken, or beans is much lower, often under $3 per kilogram in many regions. As a result, many consumers may choose more affordable protein sources over functional protein supplements.

The production costs of plant-based proteins, while somewhat lower than those of animal-based proteins, still present challenges. According to the Plant Based Foods Association (PBFA), the prices for plant-based protein products such as pea and soy protein have been increasing due to supply chain issues and growing demand.

For instance, pea protein prices rose by 20% to 25% in 2023, partly due to fluctuations in agricultural supply chains and a shortage of key ingredients like peas. This price increase affects the final retail cost of plant-based protein powders, bars, and other functional food products, potentially limiting their accessibility to lower-income groups.

Government subsidies and agricultural policies could play a significant role in mitigating these high costs. For example, in the United States, the Farm Bill has provided subsidies to certain crops like corn and soy, which indirectly benefit the production of plant-based proteins.

However, these subsidies typically favor large-scale, industrial agriculture, and do not directly address the production costs of high-quality protein sources used in functional foods. Similarly, the European Union’s Common Agricultural Policy (CAP) offers subsidies to farmers but has yet to significantly target the production of sustainable, high-quality plant-based protein for functional foods.

A report by the European Food Safety Authority (EFSA) highlighted that while plant-based proteins are increasingly being promoted as sustainable alternatives, the cost of production and processing is a significant barrier to mass adoption. In 2023, the price difference between plant-based and animal-based proteins was estimated to be up to 30% higher, further inhibiting widespread consumption, particularly in emerging markets.

Opportunity

Growing Demand for Plant-Based Proteins

A significant growth opportunity for the functional protein market lies in the increasing consumer demand for plant-based proteins. As more people adopt vegan, vegetarian, and flexitarian diets, there has been a shift away from animal-based protein sources toward plant-based alternatives.

This growing trend is driven by several factors, including health concerns, environmental sustainability, and animal welfare considerations. The rise of plant-based foods presents a significant opportunity for manufacturers of functional proteins to innovate and cater to this changing consumer preference.

According to a report from the Plant Based Foods Association (PBFA), plant-based food sales in the United States alone reached $7 billion in 2022, marking a 27% increase from the previous year. This data clearly reflects the strong consumer demand for plant-based alternatives, including plant-based proteins.

The health benefits associated with plant-based diets are a major driver of this shift. According to the Academy of Nutrition and Dietetics, plant-based diets are linked to lower risks of heart disease, high blood pressure, diabetes, and certain types of cancer. As more consumers seek ways to improve their overall health, plant-based proteins offer a way to increase protein intake without the risks associated with high levels of saturated fat and cholesterol found in animal products. Additionally, plant-based proteins are rich in fiber, vitamins, and minerals, making them an attractive option for health-conscious individuals.

Government initiatives also support the growth of plant-based proteins. In the United States, the U.S. Department of Agriculture (USDA) has launched several initiatives aimed at promoting plant-based foods, recognizing their potential for improving public health and sustainability.

Similarly, the European Union has supported plant-based agriculture through various policies designed to reduce the environmental impact of food production. The EU’s Farm to Fork Strategy encourages more sustainable food systems and includes initiatives to increase plant-based protein production, which further boosts the availability of plant-based protein sources.

Moreover, the growing awareness of the environmental impact of animal agriculture has fueled the demand for plant-based alternatives. According to the United Nations Food and Agriculture Organization (FAO), livestock farming accounts for approximately 14.5% of global greenhouse gas emissions, contributing significantly to climate change.

As consumers become more environmentally conscious, they are increasingly turning to plant-based foods as a more sustainable option. The rise of plant-based protein products, such as those made from peas, lentils, soy, and quinoa, is helping to address these environmental concerns while providing a nutritious alternative to traditional animal proteins.

Trends

Rise of Protein Fortification in Everyday Foods

One of the latest trends in the functional protein market is the growing fortification of everyday foods with functional proteins. Manufacturers are increasingly incorporating proteins into a wide variety of food products beyond traditional protein supplements.

This trend aligns with the increasing demand for nutritious, convenient, and on-the-go food options that can help consumers meet their daily protein needs without relying on specialized protein supplements. From snacks and beverages to dairy and baked goods, functional proteins are now being added to a broader range of products, appealing to health-conscious consumers and those with busy lifestyles.

According to the International Food Information Council (IFIC), 68% of U.S. adults are actively trying to incorporate more protein into their diets. This growing interest in protein-rich foods is driving manufacturers to innovate and create new products that offer both taste and nutritional benefits. For example, in the snack industry, companies are now fortifying chips, crackers, and cookies with protein, making it easier for consumers to meet their protein requirements while enjoying their favorite snacks. Similarly, the beverage market is also seeing a surge in protein-enriched drinks, such as protein-infused waters, coffee, and smoothies.

This growth is being fueled by the increasing consumer demand for high-protein foods that support overall health and wellness, including muscle building, weight management, and energy levels. As consumers become more aware of the benefits of adequate protein intake, they are seeking ways to incorporate it into their daily routines seamlessly.

A major contributor to this trend is the rise of plant-based proteins. Plant-based protein fortification has gained significant momentum in recent years, driven by the increasing adoption of vegetarian, vegan, and flexitarian diets.

According to the Plant Based Foods Association (PBFA), sales of plant-based foods in the U.S. reached $7 billion in 2022, a 27% increase from the previous year. Plant-based proteins, such as pea, soy, and rice protein, are now being used to fortify a variety of foods like pasta, breakfast cereals, and even desserts, catering to both health-conscious individuals and those with dietary restrictions.

Governments and international organizations are also supporting this trend. For example, the U.S. Department of Agriculture (USDA) has made several initiatives to encourage protein consumption as part of balanced nutrition, including guidelines in their MyPlate nutrition guide, which emphasizes the importance of incorporating protein-rich foods into meals. The European Union has been promoting protein fortification as part of its Farm to Fork Strategy, aiming to increase the availability of sustainable protein sources and reduce the environmental impact of food production. This is further supporting the shift toward fortified products.

Regional Analysis

Asia Pacific is the dominating region, accounting for 43.2% of the market share and valued at USD 3.00 billion. Rapid urbanization, growing health awareness, and increasing disposable incomes are pivotal factors driving demand. Countries such as China and India are experiencing a surge in demand due to growing middle-class populations and increasing availability of functional products.

North America is a prominent market for functional proteins, driven by a robust wellness culture and high consumer spending on health products. The region benefits from advanced biotechnological research facilities and a strong presence of leading market players, which foster innovation in protein formulations. The U.S. leads the regional market due to its significant demand in sports nutrition and functional foods.

Europe follows closely, with a market highly regulated to ensure product quality and safety. Consumer preference for sustainable and clean-label products is shaping the market landscape. The increasing popularity of plant-based diets in countries like Germany and the UK is prompting manufacturers to expand their plant-based functional protein offerings.

Middle East & Africa show promising growth, albeit from a smaller base, influenced by increasing economic diversification efforts beyond oil. The expanding fitness industry and rising health consciousness among the population are key growth drivers.

Latin America is witnessing growth fueled by improving economic conditions and a cultural shift towards preventive healthcare. Brazil and Mexico, in particular, are notable markets within the region, where local and international companies are investing to tap into the growing demand for dietary supplements and functional beverages.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Leading the market are major corporations such as Abbott Nutrition, Amway Corporation, and Glanbia plc, known for their extensive product lines that cater to diverse consumer needs, from sports nutrition to health supplements.

Glanbia, in particular, has established a strong foothold through continuous product innovation and strategic acquisitions, thereby enhancing its global presence. Similarly, Archer Daniels Midland Company and Cargill, Incorporated are pivotal in the supply of plant-based functional proteins, aligning with the rising consumer demand for sustainable and vegan-friendly options. These companies leverage their vast agricultural sourcing networks to innovate and deliver high-quality functional proteins.

On the innovation front, companies like Amai Proteins focus on developing novel protein technologies to create cost-effective and sustainable protein products with superior nutritional profiles. Merit Functional Foods and Plantible Foods represent newer entrants that are making significant strides in plant-based protein research, targeting the burgeoning vegan and vegetarian markets.

Meanwhile, traditional dairy giants such as Fonterra Co-operative Group and FrieslandCampina have expanded their portfolios to include specialized functional proteins catering to specific health and nutritional applications, thereby maintaining their competitive edge in a rapidly evolving market.

Top Key Players

- Abbott Nutrition

- Amai Proteins

- Amway Corporation

- Archer Daniels Midland Company

- Arla Foods

- Arla Foods Ingredients Group P/S

- BASF

- BENEO

- Cargill, Incorporated

- DSM

- DuPont

- DuPont de Nemours, Inc.

- Essentia Protein Solutions

- Fonterra

- Fonterra Co-operative Group

- FrieslandCampina

- Glanbia

- Glanbia plc

- Ingredion

- Kerry Group

- Merit Functional Foods

- Mycorena

- Omega Protein

- Plantible Foods

- ProtiFarm

- Roquette

Recent Developments

In early 2024, Abbott launched the PROTALITY™ brand, a new high-protein nutrition shake designed specifically to cater to adults interested in weight loss while maintaining muscle mass. This product line, which includes shakes containing 30 grams of protein each, is now available in major retailers like Walmart and CVS.

In 2023, Amway’s strategic focus on brand diversification and geographic expansion significantly bolstered its presence in this market. The company is recognized for its comprehensive approach to wellness and health products, leveraging direct selling to reach a broad consumer base globally.

Report Scope

Report Features Description Market Value (2023) USD 6.9 Bn Forecast Revenue (2033) USD 15.5 Bn CAGR (2024-2033) 8.4% Base Year for Estimation 2023 Historic Period 2020-2022 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Whey protein concentrates, Whey protein isolates, Hydrolysates, Casein/Caseinates, Soy protein, Others), By Source (Animal, Plant), By Form (Dry, Liquid), By Functionality (Muscle Building and Recovery, Weight Management, Bone and Joint Health, Beauty and Skincare, Others), By Application (Functional Food, Functional Beverages, Dietary Supplements, Animal Nutrition, Sports Nutrition, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Abbott Nutrition, Amai Proteins, Amway Corporation, Archer Daniels Midland Company, Arla Foods, Arla Foods Ingredients Group P/S, BASF, BENEO, Cargill, Incorporated, DSM, DuPont, DuPont de Nemours, Inc., Essentia Protein Solutions, Fonterra, Fonterra Co-operative Group, FrieslandCampina, Glanbia, Glanbia plc, Ingredion, Kerry Group, Merit Functional Foods, Mycorena, Omega Protein, Plantible Foods, ProtiFarm, Roquette Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Abbott Nutrition

- Amai Proteins

- Amway Corporation

- Archer Daniels Midland Company

- Arla Foods

- Arla Foods Ingredients Group P/S

- BASF

- BENEO

- Cargill, Incorporated

- DSM

- DuPont

- DuPont de Nemours, Inc.

- Essentia Protein Solutions

- Fonterra

- Fonterra Co-operative Group

- FrieslandCampina

- Glanbia

- Glanbia plc

- Ingredion

- Kerry Group

- Merit Functional Foods

- Mycorena

- Omega Protein

- Plantible Foods

- ProtiFarm

- Roquette

Our Clients

- 136231

- Dec 2024