Quick Navigation

Report Overview

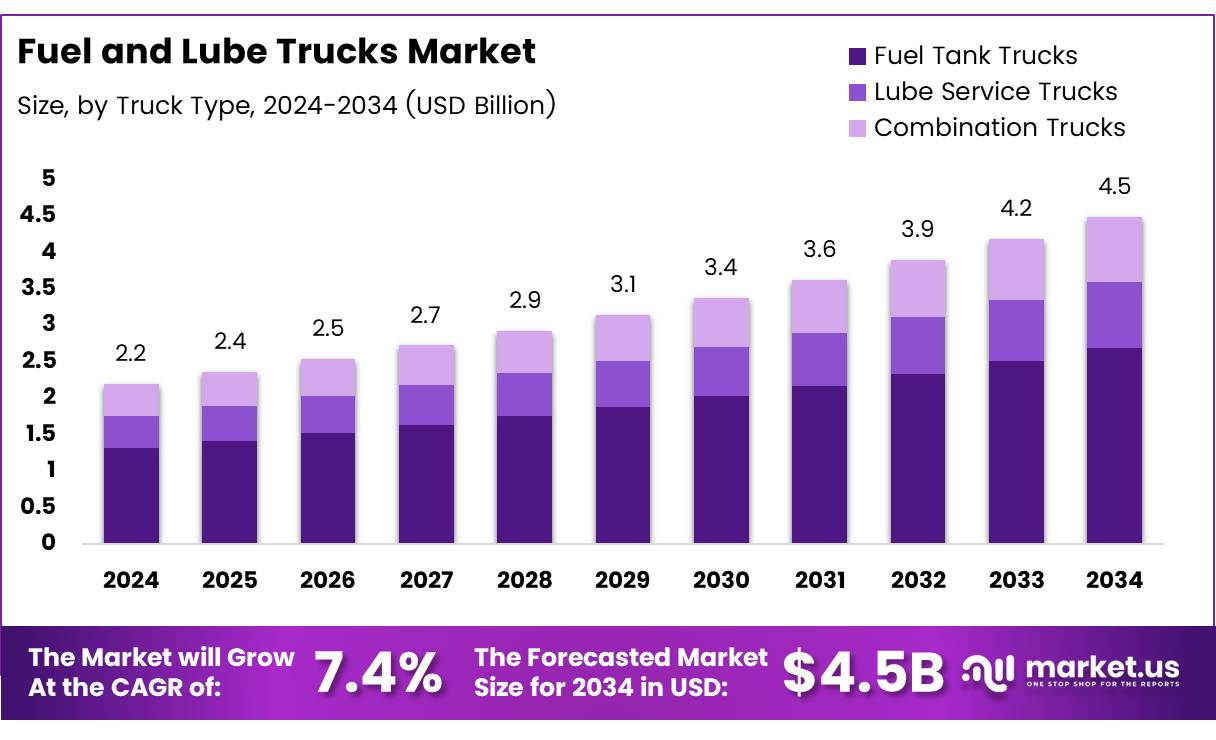

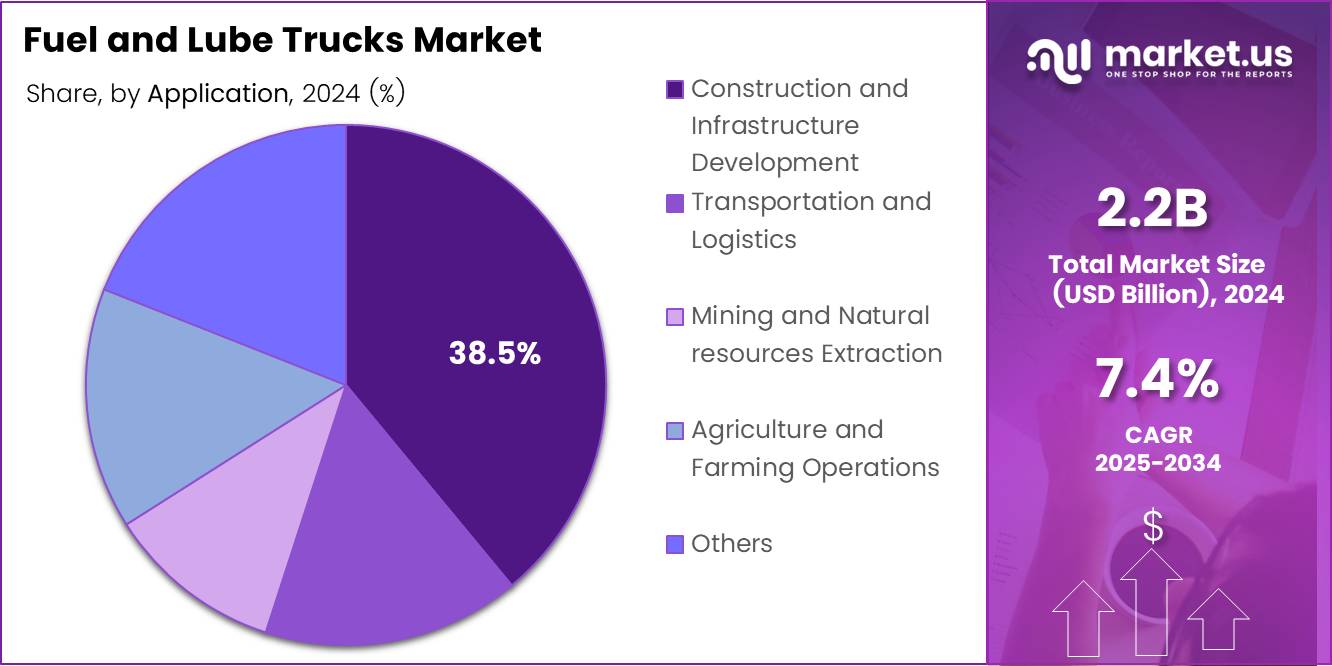

The Global Fuel and Lube Trucks Market size is expected to be worth around USD 4.5 Billion by 2034, from USD 2.2 Billion in 2024, growing at a CAGR of 7.4% during the forecast period from 2025 to 2034.

Fuel and lube trucks are specialized vehicles equipped to supply fuel and lubrication to various machinery and vehicles in field locations, particularly within industries such as mining, construction, and agriculture. These trucks are integral to operations where machinery must run efficiently and continuously without the downtime associated with returning to a central depot for maintenance.

Typically, fuel tanks on these trucks can vary significantly in size, ranging from 1,000 to 4,500 gallons (3,700 to 17,000 liters), enabling them to service a wide range of needs on a single trip, thus optimizing operational efficiency as per Truckpaper.

The market for fuel and lube trucks is primarily driven by the necessity for operational efficiency and the reduction of machinery downtime. As businesses strive to maximize productivity, the demand for on-site fueling and lubrication services grows, making these trucks indispensable in large-scale industrial operations.

This need is reflected in the predominance of diesel engines in heavy commercial vehicles in the United States, where approximately 11.4 million heavy trucks are diesel-powered, indicating a robust market for fuel and lube trucks catering to these vehicles as per Study.

The fuel and lube trucks market is poised for growth, driven by expanding industrial activities in sectors such as mining, construction, and large-scale agriculture. These industries require heavy machinery that operates continuously, and fuel and lube trucks play a critical role in ensuring these machines are serviced without significant interruptions.

Opportunities for market expansion also lie in the innovation of truck features, such as improved fuel efficiency and the integration of advanced technology for better fluid management and monitoring.

Government investments in infrastructure and regulatory frameworks significantly influence market dynamics. Regulations concerning emissions and the operation of diesel-powered vehicles affect the design and operation of fuel and lube trucks.

With over three-quarters of the heavy commercial vehicle fleet in the United States running on diesel, regulatory changes can spur advancements in fuel efficiency and environmental compliance in these trucks a per Study.

Moreover, the gradual shift towards renewable energy and the introduction of electric vehicles present both challenges and opportunities. While electric trucks currently represent a small fraction of the market with an estimated 15,000 units, their growing adoption might prompt the development of new types of fuel and lube trucks adapted to electric vehicle needs. This shift indicates a potential pivot point for the industry to innovate and capture new market segments as environmental regulations tighten and consumer preferences evolve.

Key Takeaways

- The global Fuel and Lube Trucks market is projected to grow from USD 2.2 Billion in 2024 to USD 4.5 Billion by 2034, with a CAGR of 7.4%.

- Fuel Tank Trucks led the Truck Type segment with a 60.2% share in 2024, crucial for transporting fuel across diverse terrains.

- The 15,000 to 25,000 kg capacity segment dominated the market with a 40.6% share in 2024, favored for its balance of capacity and maneuverability.

- Construction and Infrastructure Development was the leading application in 2024, holding a 38.5% market share.

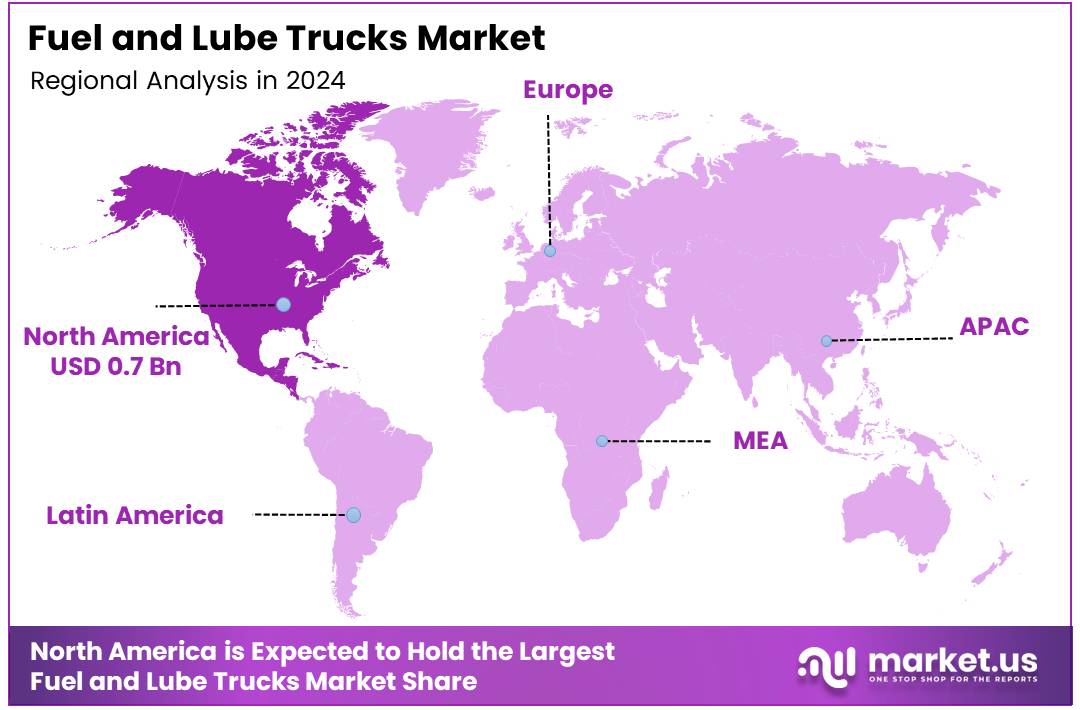

- North America dominated the market with a 35.8% share in 2024, driven by strong infrastructure investments and a focus on technological and environmental advancements.

Truck Type Analysis

Fuel Tank Trucks Lead with 60.2% Market Share Owing to High Demand and Versatility

In 2024, the By Truck Type Analysis segment of the Fuel and Lube Trucks market was predominantly led by Fuel Tank Trucks, which captured a significant 60.2% share. This dominance can be attributed to the trucks’ critical role in transporting large volumes of fuel efficiently across varied geographic terrains.

Fuel Tank Trucks are essential for industries reliant on consistent fuel supply, including agriculture, construction, and transportation, making them indispensable in operational logistics.

Lube Service Trucks also held a notable position in the market, supporting essential maintenance operations by providing on-site lubrication services that help reduce machinery downtime and enhance productivity in field operations. These trucks are equipped with tanks and tools necessary for the immediate servicing of heavy equipment, which is crucial for industries such as mining and heavy construction.

Combination Trucks, though smaller in market share compared to their counterparts, offer a versatile solution by combining the capabilities of both fuel and lube trucks. This dual-functionality makes them particularly valuable in remote or isolated project sites where they contribute to streamlined operations by fulfilling multiple service needs with one vehicle.

Collectively, these truck types form a vital component of the Fuel and Lube Trucks market, each serving unique industry needs that drive their demand and market positioning.

Capacity Analysis

15,000 to 25,000 kg Category Leads in Fuel and Lube Trucks Market with a 40.6% Share

In 2024, the By Capacity Analysis segment of the Fuel and Lube Trucks market saw the 15,000 to 25,000 kg category maintaining a dominant market position, capturing a substantial 40.6% share. This segment’s prominence is attributed to its optimal balance between capacity and maneuverability, making it highly suitable for a wide range of operational environments from urban to rugged terrain.

In contrast, the Below 10,000 kg category, known for its agility and suitability for tight spaces, held a smaller share. These lighter trucks are preferred in regions with restrictive weight regulations or in applications requiring frequent and nimble refueling capabilities.

The 10,000 to 15,000 kg category offers an intermediate option, combining reasonable fuel and lube capacity with enhanced ease of movement, which appeals to businesses looking for versatility without the bulk of larger trucks.

Lastly, the Above 25,000 kg trucks, while encompassing the smallest market share, are indispensable in settings that demand heavy-duty fuel and lubrication services, such as large-scale mining operations or extensive agricultural fields, where their high capacity maximizes operational efficiency and reduces downtime.

Application Analysis

Construction and Infrastructure Lead the Charge in Fuel and Lube Trucks Market with a 38.5% Share

In 2024, the By Application Analysis segment of the Fuel and Lube Trucks Market saw Construction and Infrastructure Development taking the lead with a substantial 38.5% market share.

This dominance is attributed to the surge in global infrastructure projects and the increasing complexity of construction activities requiring more specialized and efficient fuel and lubrication solutions on-site. These trucks are integral to maintaining the machinery essential for timely and efficient project completions, thereby reducing downtime and boosting productivity.

Following closely, the Transportation and Logistics sector also showed significant utilization of fuel and lube trucks, essential for maintaining vehicles that manage the supply chains across vast geographies. Meanwhile, Mining and Natural Resources Extraction industries relied heavily on these trucks to support their round-the-clock operations in remote and harsh environments, ensuring that heavy mining equipment operates smoothly with minimal interruptions.

Agriculture and Farming Operations, while having a lower share compared to other sectors, still recognized the value of these trucks in maintaining large fleets of farming machinery during critical planting and harvesting seasons. The Others category, which includes various smaller scale industries, also showed a diverse application of fuel and lube trucks, underlining their versatility across different sectors.

Key Market Segments

By Truck Type

- Fuel Tank Trucks

- Lube Service Trucks

- Combination Trucks

By Capacity

- 15,000 to 25,000 kg

- Below 10,000 kg

- 10,000 to 15,000 kg

- Above 25,000 kg

By Application

- Construction and Infrastructure Development

- Transportation and Logistics

- Mining and Natural resources Extraction

- Agriculture and Farming Operations

- Others

Drivers

Growth in Mining and Construction Boosts Fuel and Lube Trucks Market

The fuel and lube trucks market is witnessing significant growth driven by the expansion in mining and construction activities. As these sectors continue to grow, the demand for fuel and lube trucks intensifies, providing essential on-site maintenance services for heavy machinery.

Additionally, the surge in oil and gas exploration activities necessitates robust on-site fueling and lubrication services to support continuous drilling and exploration operations. Another key driver is the increasing focus on fleet management within the logistics sector, where companies are investing in mobile refueling and servicing solutions to enhance operational efficiency.

The agriculture industry also contributes to market expansion, as the rising adoption of heavy machinery for farming operations demands more mobile lubrication and refueling services. These factors combined are propelling the market forward, reflecting a growing reliance on fuel and lube trucks across various heavy industries for efficient and uninterrupted operations.

Restraints

Environmental Regulations Curb Growth in the Fuel and Lube Trucks Market

Environmental regulations are tightening up, and it’s really putting the brakes on the growth of the fuel and lube trucks market. Governments are cracking down on fuel emissions and making sure trucks don’t leak, which means companies have to spend more on the tech and materials to keep everything clean and compliant. This isn’t cheap, and it adds a lot to the cost of building these trucks.

On top of that, oil prices keep bouncing up and down like a yo-yo, which makes it tough for companies to figure out their costs and scares off some from investing in new fuel handling gear. These two big issues—tough rules on emissions and leaks, plus the wild swings in fuel prices—make it hard for the market to grow without some serious innovation.

Growth Factors

Smart Monitoring Enhances Fuel and Lube Trucks Efficiency

The fuel and lube trucks market is poised for significant growth, primarily driven by the integration of Internet of Things (IoT) and telematics technologies. These advancements enable smarter monitoring and tracking systems that not only improve fuel management but also boost operational efficiency across various industries.

In emerging economies, the surge in construction and mining activities offers lucrative opportunities for market expansion. Moreover, there’s a growing inclination towards sustainable and bio-based lubricants, which opens new segments and attracts environmentally conscious consumers.

Additionally, the market is experiencing a shift towards rental and leasing business models, as companies opt to rent fuel and lube trucks to reduce upfront investments and adapt to changing technological advancements more flexibly. These factors collectively contribute to a dynamic environment for market players, facilitating both growth and innovation in the sector.

Emerging Trends

Eco-Friendly Alternatives Boost Fuel and Lube Trucks Market

The fuel and lube trucks market is witnessing significant shifts, primarily driven by the adoption of electric and hybrid models as companies pivot towards more sustainable practices. This green transition is not only a response to increasing environmental regulations but also a reflection of growing consumer and corporate demand for eco-friendly alternatives.

Adding to the market’s dynamism is the integration of automation in fuel dispensing systems, which enhances operational efficiency and accuracy, reducing human error and time spent on refueling tasks. Furthermore, as industries face unique operational demands, the availability of customizable and modular fueling units allows businesses to tailor solutions to their specific needs, thereby optimizing their logistics and operations.

The market is also seeing a notable pivot towards alternative fuels like hydrogen and compressed natural gas (CNG), driven by the global push for cleaner energy sources. These trends collectively signal a robust pathway for growth and innovation in the fuel and lube trucks industry, with sustainability and technology at the forefront.

Regional Analysis

North America Leads with 35.8% Market Share Worth USD 0.7 Billion Due to Strong Infrastructure and Mining Investments

The global market for Fuel and Lube Trucks exhibits varied dynamics and growth patterns across different regions, reflecting a complex interplay of regional industrial activities, regulatory environments, and economic conditions.

North America is the dominant region in the Fuel and Lube Trucks market, holding a substantial market share of 35.8% valued at USD 0.7 billion. This prominence is driven by robust investments in infrastructure projects and the strong presence of mining and construction industries. The region benefits from advanced technological integration and stringent environmental regulations that promote the adoption of efficient and environmentally friendly fuel and lube trucks.

Regional Mentions:

Europe follows with significant market engagement, characterized by stringent emission standards and a focus on renewable energy projects. The region’s emphasis on sustainability encourages innovations in fuel and lube truck technologies, catering to a growing demand for greener and more efficient vehicles.

In the Asia Pacific, rapid industrialization and urbanization are propelling the market forward. Countries like China and India are witnessing substantial growth in construction and mining sectors, thereby boosting the demand for fuel and lube trucks. The region’s market is expected to expand at a brisk pace, driven by increasing infrastructure investments and the expansion of industrial activities.

The Middle East & Africa region presents a growing market, fueled by the expansion of the oil & gas industry and large-scale infrastructure projects. The demand in this region is characterized by the need for high-capacity and durable vehicles capable of operating in harsh environmental conditions.

Latin America, though smaller in comparison, shows potential for growth due to the development of the mining sector, particularly in countries like Brazil and Chile. The market here is benefitting from regional efforts to enhance infrastructure and industrial capacities.

Overall, while North America currently leads the market, the Asia Pacific region is poised for rapid growth, potentially reshaping the global market dynamics in the coming years due to its fast-paced industrial development and expanding infrastructure needs.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global fuel and lube trucks market remains highly competitive with key players like McLellan Industries, Inc., Niece Equipment, LP, and others striving to solidify their market positions through strategic innovations and expanded service offerings.

McLellan Industries, known for its robust and efficient fuel and lube trucks, continues to lead by integrating advanced technology that enhances the operational efficiency and reliability of its vehicles. This is critical as industries increasingly demand higher performance and environmentally friendly solutions.

Niece Equipment, LP stands out with its adaptable product range, catering to both small-scale operations and large mining projects, thereby broadening its market reach. The company’s commitment to customer service and the ability to customize products to meet specific client needs gives it a competitive edge, particularly in North America.

Panda Mechanical Equipment Co., Ltd., with its strong foothold in the Asian markets, drives innovation in cost-effective solutions, making it a formidable player against Western manufacturers. The company’s focus on expanding its international presence could see it capturing more market share in emerging markets, where cost considerations are paramount.

Companies like Thunder Creek Equipment (LDJ Manufacturing Inc.) and Ground Force Worldwide continue to excel in niche markets by offering specialized vehicles that cater to specific industry needs, such as agriculture and construction, which require unique fuel and lubrication solutions.

Overall, the market landscape in 2024 is shaped by technological advancements, customer-centric approaches, and strategic global expansions. As environmental regulations tighten and operational efficiency becomes more critical, companies that can innovate while maintaining high standards of quality and sustainability will likely lead the pack.

Top Key Players in the Market

- McLellan Industries, Inc.

- Niece Equipment, LP

- Panda Mechanical Equipment Co., Ltd.

- Engineered Transportation International

- Ground Force Worldwide

- Thunder Creek Equipment (LDJ Manufacturing Inc.)

- Tankmart International Inc.

- Platinum Tank Group

- Tremcar

- Stellar

- Others

Recent Developments

- In November 2024, Daimler secured a funding of US$239 million to enhance the production of fuel cell trucks, aiming to boost the adoption of cleaner energy sources in the trucking industry.

- In February 2025, Milence received a substantial funding of €111 million from the European Union to develop infrastructure for alternative fuels, supporting the transition to sustainable transportation.

- In October 2023, the HyHAUL project was awarded over £30 million in funding, initiating the roll-out of hydrogen fuel cell trucks to promote sustainable freight solutions.

- In July 2024, Volvo was granted $208 million to accelerate the production of heavy-duty electric trucks, furthering advancements in electric vehicle technology for the transport sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.2 Billion |

| Forecast Revenue (2034) | USD 4.5 Billion |

| CAGR (2025-2034) | 7.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Truck Type (Fuel Tank Trucks, Lube Service Trucks, Combination Trucks), By Capacity (15,000 to 25,000 kg, Below 10,000 kg, 10,000 to 15,000 kg, Above 25,000 kg), By Application (Construction and Infrastructure Development, Transportation and Logistics, Mining and Natural resources Extraction, Agriculture and Farming Operations, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | McLellan Industries, Inc., Niece Equipment, LP, Panda Mechanical Equipment Co., Ltd., Engineered Transportation International, Ground Force Worldwide, Thunder Creek Equipment (LDJ Manufacturing Inc.), Tankmart International Inc., Platinum Tank Group, Tremcar, Stellar, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |