Quick Navigation

Report Overview

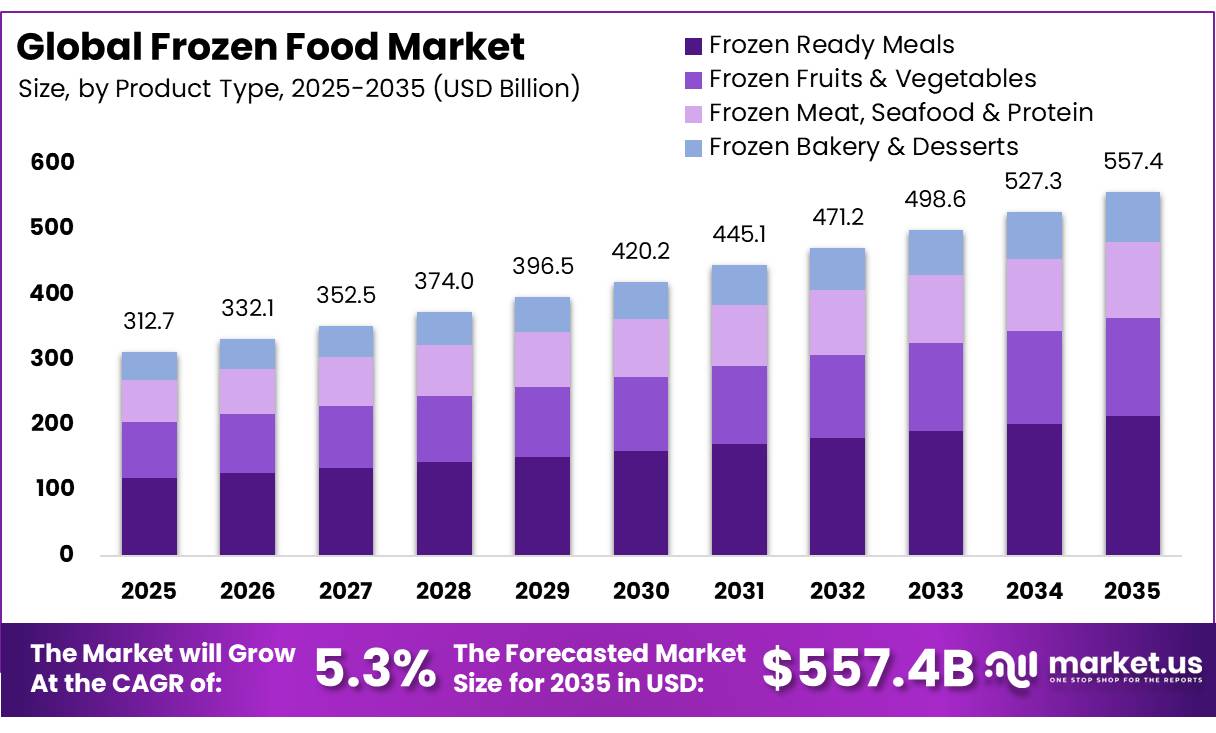

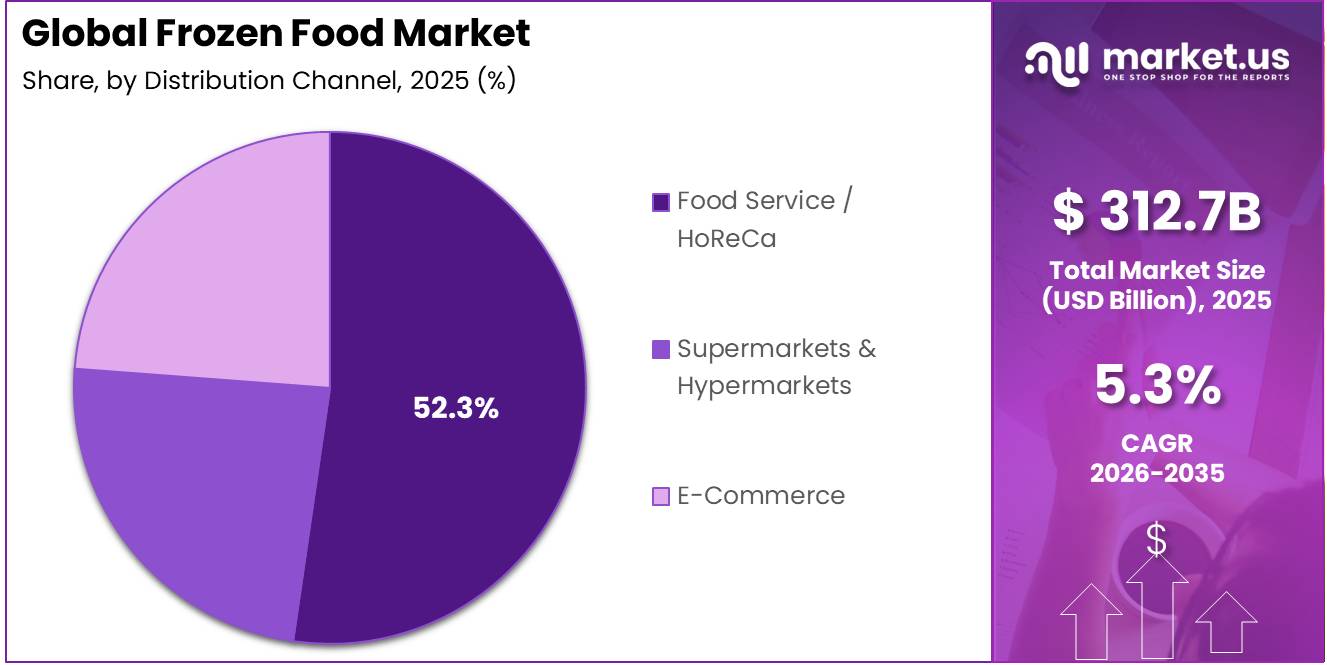

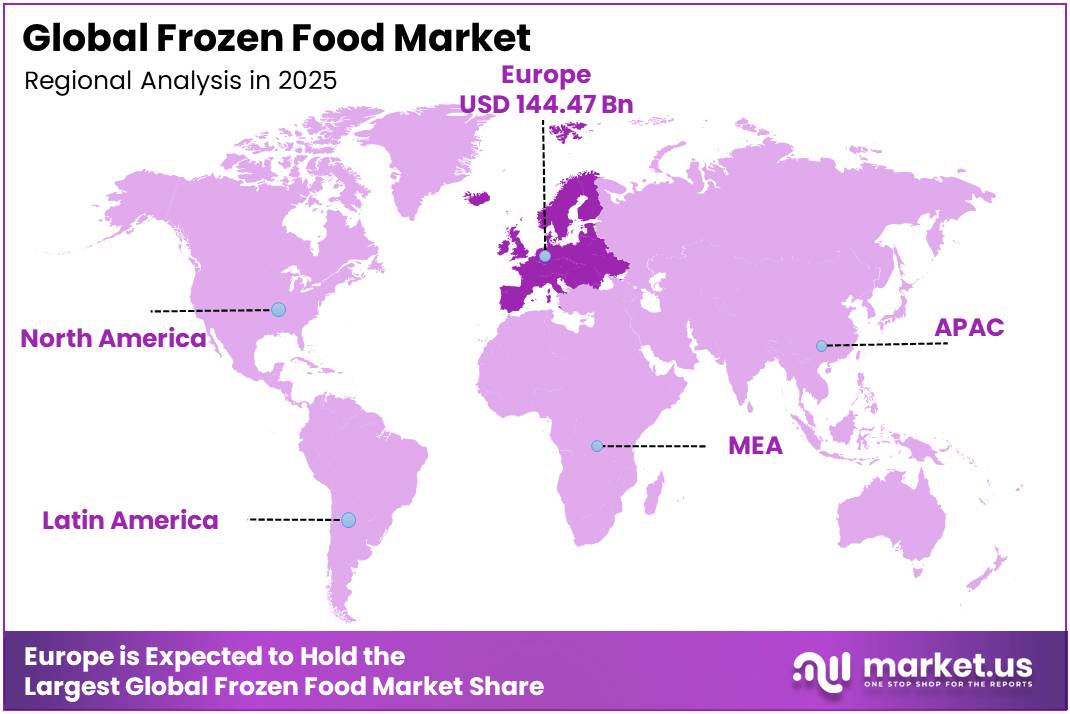

In 2025, the Global Frozen Food Market was valued at US$312.7 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.3%, reaching about US$557.4 billion by 2035. In 2025, Europe led the market, achieving over 46.2% share with a revenue of US$144.47 Billion.

The frozen food industry represents a vital segment of the global food and beverage sector, providing consumers with convenient, safe, and long-lasting food products while preserving nutritional quality through advanced freezing technologies. Frozen foods include vegetables, fruits, meat, seafood, bakery products, ready meals, and dairy-based products that are processed and stored at low temperatures to extend shelf life.

- According to the UNEP Food Waste Index Report 2024 and the latest FAO SDG 12.3 monitoring updates, around 19% of food is wasted at the retail, food service, and household levels, while food loss occurring from post-harvest to retail remains significant at approximately 13%, highlighting persistent inefficiencies across the global food supply chain.

Key Takeaways

- The Global Frozen Food Market was valued at USD 312.7 billion in 2025.

- The market is projected to grow at a CAGR of 5.3% and is estimated to reach USD 557.4 billion by 2035.

- Frozen Ready Meals dominated the Product Type segment, holding a 38.3% share in 2025.

- Raw Material led the Type segment, accounting for 46.3% of the market in 2025, while Ready-to-Eat emerged as the fastest-growing sub-segment.

- Blast Freezing remained the leading Freezing Technique, capturing 52.7% share in 2025.

- Food Service/HoReCa was the dominant Distribution Channel, representing 52.3% of sales in 2025.

- Europe led the regional landscape, contributing a 46.2% share in 2025.

Frozen food industry is expected to emerge from investments in sustainable cold chain infrastructure, energy-efficient refrigeration systems, and advanced food preservation technologies. Government and international organizations are supporting food preservation and supply chain modernization initiatives to strengthen food security and reduce post-harvest losses.

In addition, rising demand for plant-based frozen foods, premium ready-to-eat meals, clean-label products, and environmentally sustainable packaging is expected to create new opportunities for manufacturers. Continued technological innovation and expanding global food distribution networks are likely to support the long-term development of the frozen food industry.

Frozen Food Market Segmentation

Product Type Analysis

Frozen Ready Meals dominate the market as consumers continue to seek convenient meal solutions.

In 2025, Frozen Ready Meals held a dominant market position, capturing more than a 38.3% share. The segment maintained its leadership due to the growing preference for convenient and time-saving food options among consumers with busy lifestyles. Frozen ready meals offer ease of preparation, consistent taste, and longer shelf life, making them a practical choice for households and working professionals. Retailers and food manufacturers continued to expand their product portfolios with a wider range of meal options, including healthier recipes and premium offerings, which further supported demand.

- An AFFI survey conducted in October 2025 among frozen-food consumers found that 40% use frozen foods daily or every few days, with ease of preparation, price, and taste identified as the leading purchase drivers.

Frozen Fruits & Vegetables is the fastest growing segment. The segment has been gaining momentum as consumers increasingly focus on nutritious and minimally processed food products. The availability of frozen fruits and vegetables throughout the year, regardless of seasonal limitations, has contributed to their growing popularity. Growing awareness about healthy eating habits and the increasing use of frozen produce in home cooking and meal preparation are expected to support the segment’s continued expansion in the coming years.

Type Analysis

Raw Material-based frozen foods lead the market supported by broad product usage across food categories.

In 2025, Raw Material held a dominant market position, capturing more than a 46.3% share. The segment maintained its leading position due to its extensive use across multiple frozen food categories, including vegetables, fruits, meat, seafood, and other primary food ingredients. Demand remained strong as consumers increasingly preferred frozen products that offer longer shelf life while preserving freshness and nutritional value.

Ready-to-Eat is the fastest growing segment. The segment continued to gain strong traction as consumers increasingly looked for quick and hassle-free meal options that fit busy daily schedules. The growing demand for convenient food products, combined with changing eating habits and higher preference for time-saving meal solutions, supported segment expansion. Frozen ready-to-eat products also benefited from continuous product innovation, including healthier recipes, premium offerings, and diverse cuisine options.

Freezing Technique Analysis

Blast Freezing leads the market share due to its efficiency and wide industrial adoption.

In 2025, Blast Freezing held a dominant market position, capturing more than a 52.7% share. The segment remained the preferred freezing technique across the frozen food industry because of its ability to rapidly lower product temperatures while maintaining food quality and safety. Food processors continued to adopt blast freezing for a wide range of products, including meat, seafood, bakery items, fruits, vegetables, and ready meals. The technique helped preserve texture, flavor, and nutritional content while supporting large-scale production requirements.

- A 2025 study published in the International Journal of Thermal Sciences found that increasing the fan speed in a batch air-blast freezer from 560 rpm to 840 rpm improved the average surface heat-transfer coefficient by 34%–39%.

Individual Quick Freezing (IQF) is the fastest growing segment. The segment continued to expand as food manufacturers and consumers increasingly recognized the benefits of freezing products individually rather than in bulk. IQF technology helps maintain the original shape, texture, and quality of food items while preventing them from clumping together during storage. This advantage has made the technique particularly popular for frozen fruits, vegetables, seafood, and specialty food products. Growing demand for premium frozen foods, combined with increasing focus on product quality and convenience, supported the wider adoption of IQF technology.

Distribution Channel Analysis

Food Service / HoReCa dominates the market share driven by large-scale demand for frozen food products.

In 2025, Food Service / HoReCa held a dominant market position, capturing more than a 52.3% share. The segment maintained its leadership due to the extensive use of frozen food products across hotels, restaurants, cafés, catering services, and institutional kitchens. Frozen ingredients and ready-to-cook products helped foodservice operators improve inventory management, reduce food waste, and maintain consistent quality throughout the year. The growing preference for quick meal preparation and efficient kitchen operations further supported the adoption of frozen foods within the HoReCa sector.

Supermarkets & Hypermarkets is the fastest growing segment. The segment continued to witness strong growth as consumers increasingly relied on organized retail outlets for their frozen food purchases. These stores offer a wide variety of frozen products, ranging from fruits and vegetables to ready meals, seafood, and bakery items, allowing shoppers to compare brands and product options in one location. The expansion of modern retail infrastructure, along with improved freezer storage facilities and attractive promotional activities, has encouraged higher consumer spending on frozen foods.

Key Market Segments

By Product Type

- Frozen Ready Meals

- Frozen Fruits & Vegetables

- Frozen Meat, Seafood & Protein

- Frozen Bakery & Desserts

By Type

- Raw Material

- Half-cooked

- Ready-to-Eat

By Freezing Technique

- Blast Freezing

- Individual Quick Freezing (IQF)

- Belt Freezing

By Distribution Channel

- Supermarkets & Hypermarkets

- Food Service/HoReCa

- E-Commerce

Driver Analysis

Convenience-led at-home meal substitution

Frozen food is gaining from a durable shift in meal economics rather than a temporary pantry-loading effect: USDA reported May 2026 food-at-home inflation at 2.7% year over year versus 3.5% for food-away-from-home, while all food was up 3.1%, reinforcing the relative affordability of grocery-based meal occasions over restaurant spend.

That spread matters because frozen products convert consumer value perception into repeat volume through lower waste, portion control, and shorter preparation time; when the gap between restaurant inflation and grocery inflation stays near 0.8 percentage points, the category captures budget-conscious weekday meals, especially in North America and major EU cities.

The impact is strongest in short-cycle categories such as frozen ready meals, vegetables, potato products, and snack formats because they fit the operating model of dual-income households: lower absolute basket risk, fewer spoilage losses, and more predictable consumption cadence, which together support an estimated +1.2 percentage-point uplift to baseline CAGR rather than a one-off sales spike.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-led at-home meal substitution | +1.2% | North America core, EU urban centers, APAC metros | Short term (≤ 2 years) |

| Cold-chain and processing capacity build-out | +1.0% | India, Southeast Asia, South America spill-over, North America logistics nodes | Medium term (2-4 years) |

| Inflation-driven value migration from foodservice | +0.9% | North America core, UK, EU, selected APAC cities | Short term (≤ 2 years) |

| Health-label reformulation and nutrient-density positioning | +0.7% | U.S. core, Canada spill-over, EU premium retail | Medium term (2-4 years) |

| Retail freezer efficiency and inventory normalization | +0.6% | U.S., Western Europe, Japan, Korea | Medium term (2-4 years) |

| Export channel scaling in processed and frozen agri-food | +0.5% | India export corridors, Gulf markets, EU import channels, North America niche ethnic retail | Long term (≥ 4 years) |

Restraint Analysis

Sodium reformulation pressure

The FDA issued updated draft voluntary sodium reduction goals in August 2024 covering 163 food categories with a three-year compliance-oriented horizon and an intended reduction of average sodium intake toward about 2,750 mg per day, while the agency also continues to define “high sodium” consumer-facing thresholds through Nutrition Facts labeling conventions that directly affect frozen meals, snacks, pizzas, and prepared entrées.

For the frozen food market, the restraint is not an immediate sales collapse but a reformulation burden: sodium reduction in frozen systems often requires texture stabilizers, flavor masking, ingredient rebalancing, and shelf-life validation, which can extend product redevelopment cycles by 6 to 12 months, raise R&D and plant trial costs by an estimated 1 to 2 percent of category sales for affected portfolios, and increase the risk of taste-led delistings if execution is poor; this creates a modeled 0.8 percentage-point medium-term CAGR drag because compliance-oriented renovation redirects spend away from line expansion and depresses commercialization speed in high-sodium subsegments

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain capacity tightness | -1.1% | North America core | Short term (≤ 2 years) |

| Energy-cost volatility | -1.4% | EU, North America core, APAC import corridors | Short term (≤ 2 years) |

| Ingredient cost inflation | -1.2% | Global, EU, North America core | Medium term (2-4 years) |

| Sodium reformulation pressure | -0.8% | North America core | Medium term (2-4 years) |

| Packaging compliance inflation | -0.9% | EU, UK-aligned markets | Medium term (2-4 years) |

| Trade and import friction | -0.7% | APAC-North America lanes, EU import corridors | Long term (≥ 4 years) |

Opportunity Analysis

Integrated cold-chain build-out for frozen retail

A realistic upside scenario assumes coordinated investments in integrated end‑to‑end TCL networks similar in scale to pilots where IFC and private players commit about USD 6–10 million per node for warehouses, rolling stock, and IT systems scaled to 50–100 city clusters across South Asia, Sub‑Saharan Africa, and Latin America, yielding incremental frozen food TAM of USD 25–40 billion by 2035 through improved on‑shelf availability, lower spoilage, and reduced stock‑outs.

At an operating level, shifting from unorganised single‑item cold stores to integrated networks can lower logistics cost per tonne‑km by 10–20%, reduce product loss rates from double‑digit percentages to below 5%, and improve average inventory turns from 6–8x to 10–12x annually, allowing manufacturers and retailers to expand frozen assortments with 3–5 percentage‑point margin expansion on premium SKUs while justifying higher capex intensity.

Because most baseline forecasts assume gradual, not transformational, cold‑chain upgrading, a deliberate push to build integrated TCL tied to frozen retail could add around 2 percentage points to global frozen food CAGR through 2035, particularly in markets where total TCL demand in major hinterlands already exceeds 5–7 million tonnes and policy frameworks for concessional financing, viability gap funding, and land allocation are being set up but not yet fully directed toward frozen retail penetration.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Integrated cold-chain build-out for frozen retail | +2.0% | South Asia, Sub-Saharan Africa, LATAM emerging | Long term (≥ 4 years) |

| Export-oriented frozen protein & prepared meals platforms | +1.5% | Latin America, ASEAN, Eastern Europe | Medium term (2-4 years) |

| Health- and sustainability-certified frozen product lines | +1.2% | North America core, EU, developed APAC | Short term (≤ 2 years) |

| Digital direct-to-freezer distribution and micro-fulfilment | +1.0% | North America, EU, urban APAC | Medium term (2-4 years) |

| Institutional and social safety net frozen food programs | +1.3% | Low- and middle-income regions globally | Long term (≥ 4 years) |

| Green cold-chain financing and PPP structures | +0.8% | Global, with focus on Asia and Africa | Medium term (2-4 years) |

Challenges Analysis

Energy-intensive freezing costs

The frozen food sector is structurally exposed to energy-price volatility because blast freezing, sub-zero storage, and refrigerated transport collectively account for a significant share of operating costs, and official data show that even as industrial energy prices in the EU stabilized in 2024, they remained elevated relative to pre-2022 levels and continued to exhibit month-to-month volatility of around 1–2 percent.

Energy-intensive cold-chain equipment, from -18 °C storage rooms to continuous freezers, operates near-baseload utilization, so a sustained 10–15 percent elevation in industrial electricity and gas prices versus pre-crisis norms can add 3–5 percentage points to total operating costs for frozen processors and cold stores; given typical net margins in the mid-single digits, this translates into a 1.3 percentage point drag on otherwise attainable CAGR as firms delay capex, push through staggered price increases, or reconfigure product portfolios away from energy-intensive SKUs.

Strategically, leading producers and logistics operators must respond through multi-year energy management programs, including transitioning 20–30 percent of cold storage capacity to contracts backed by renewables or on-site generation within 3–4 years, retrofitting high-consumption sites with variable-speed drives and advanced insulation to reduce energy intensity by 10–20 percent, and piloting innovative freezing technologies that can shave 5–15 kWh per tonne of product; collectively, these measures reduce the amplitude of energy-cost shocks on unit economics and enable more aggressive pricing and distribution strategies without permanently sacrificing growth.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Cold-chain capacity gaps | -1.8% | Emerging markets, rural APAC, Africa | Long term (≥ 4 years) |

| Energy-intensive freezing costs | -1.3% | EU, North America, energy-importing Asia | Medium term (2-4 years) |

| Skilled cold-chain labor deficits | -0.9% | North America, EU logistics hubs | Medium term (2-4 years) |

| Food loss in frozen supply | -1.0% | Global agri-export corridors | Medium term (2-4 years) |

| Regulatory and sustainability pressure | -0.8% | EU regulatory hubs, OECD markets | Long term (≥ 4 years) |

| Demand volatility & price sensitivity | -0.7% | Global urban middle-income segments | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Global Supply Chain Disruptions and Trade Uncertainty Affect Frozen Food Industry

The geopolitical conflicts between Europe and the Middle East have created challenges for the global frozen food industry by disrupting supply chains, increasing transportation costs, and affecting the availability of key food commodities. Frozen food manufacturers depend heavily on reliable cold-chain logistics, stable energy supplies, and uninterrupted international trade routes. When conflicts impact shipping corridors, ports, or transportation networks, companies often face delays in sourcing raw materials and delivering finished products to retailers and foodservice customers.

The frozen food sector has also been affected by fluctuations in energy prices. Cold storage facilities, refrigerated warehouses, and temperature-controlled transportation require significant energy to maintain product quality. During periods of geopolitical uncertainty, higher fuel and electricity costs can increase operating expenses across the supply chain. These additional costs may place pressure on manufacturers and distributors, particularly those operating across multiple international markets.

Trade restrictions, sanctions, and changing import-export policies have further influenced the movement of agricultural products used in frozen foods, including vegetables, fruits, seafood, and processed ingredients. In response, many companies have diversified their supplier networks and increased regional sourcing to reduce dependence on any single market.

Despite these challenges, demand for frozen food has remained relatively stable because consumers continue to value convenience, affordability, and longer shelf life. As companies strengthen supply chain resilience and invest in local production capabilities, the industry is adapting to geopolitical risks while maintaining a steady flow of products to global consumers.

Regional Analysis

Europe Leads the Frozen Food Market with Strong Consumption and Advanced Cold-Chain Infrastructure.

Europe dominated the frozen food market in 2025, accounting for 46.2% of the global market and reaching a value of USD 144.47 Bn. The region maintained its leading position due to high consumer acceptance of frozen food products, a well-established retail network, and advanced cold-chain infrastructure. Frozen vegetables, ready meals, seafood, bakery products, and frozen snacks continue to be widely consumed across European households. The region also benefits from one of the world’s largest food manufacturing industries.

- According to Food DrinkEurope Data & Trends 2024 (published in 2025), the European food and drink industry generated approximately EUR 1.2 trillion in turnover, employed around 4.7 million people, and contributed nearly EUR 250 billion in value added, making it the largest manufacturing industry in the European Union.

North America continues to represent a significant market supported by strong frozen food consumption and a highly developed retail sector. Asia-Pacific is emerging as an important growth region due to expanding urban populations, rising disposable incomes, and increasing adoption of modern retail formats. The growing popularity of ready-to-eat and ready-to-cook food products is supporting regional demand.

Meanwhile, Latin America and the Middle East & Africa are witnessing gradual market expansion driven by improving cold storage infrastructure, increasing supermarket penetration, and greater awareness of food preservation benefits. Across these regions, investments in refrigerated transportation, food processing facilities, and organized retail channels are expected to support future market development and strengthen the global footprint of frozen food products.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global frozen food market demonstrates a moderately fragmented competitive structure, with several multinational food companies competing alongside regional and specialized frozen food manufacturers. While a few well-established brands hold strong positions across major product categories, the market remains open to numerous local and private-label producers that cater to specific consumer preferences and regional demand patterns.

The presence of a wide variety of frozen products, including ready meals, vegetables, fruits, seafood, snacks, and desserts, has prevented the market from becoming highly consolidated. Large companies continue to benefit from strong distribution networks, recognized brands, extensive product portfolios, and long-standing relationships with retailers and foodservice operators.

Nestlé S.A., Unilever PLC, and Nomad Foods Ltd. maintain significant influence through their broad frozen food offerings and strong international presence. Companies such as Wawona Frozen Foods, Bellisio Parent, LLC, OOB Organic contribute to market competition by focusing on specific product categories and niche consumer segments.

Competitive activity is largely driven by product innovation, healthier frozen food options, sustainable packaging initiatives, and expansion into new retail and foodservice channels. As consumer demand continues to diversify, market participants are expected to strengthen their positions through innovation, strategic partnerships, and investments in manufacturing and cold-chain capabilities.

The Major Players in The Industry

- Unilever PLC

- Nestlé S.A.

- General Mills, Inc.

- Nomad Foods Ltd.

- Tyson Foods Inc.

- Conagra Brands Inc.

- Wawona Frozen Foods

- Bellisio Parent, LLC

- Kellanova

- The Kraft Heinz Company

- OOB Organic

- Omar International Pvt Ltd

Key Development

- In March 2025, Unilever PLC continued strengthening its frozen dessert business through the separation of its ice cream division into a standalone operating structure under The Magnum Ice Cream Company. The company remained focused on premium frozen categories through brands including Magnum, Wall’s, and Ben & Jerry’s. Unilever reported EUR 60.8 billion in group turnover for 2024 and continued investing in supply chain efficiency and cold distribution capabilities.

- In December 2025, Kellanova continued expanding its frozen breakfast portfolio through Eggo innovation, including additional protein-focused waffle and breakfast product launches. The company also entered a transformational phase following the completion of Mars’ USD 35.9 billion acquisition on 11 December 2025, one of the largest food and snacking transactions in recent years.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 312.7 Bn |

| Forecast Revenue (2035) | USD 557.4 Bn |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Frozen Ready Meals, Frozen Fruits & Vegetables, Frozen Meat, Seafood & Protein, and Frozen Bakery & Desserts), By Type (Raw Material, Half-cooked, and Ready-to-Eat), By Freezing Technique (Blast Freezing, Individual Quick Freezing (IQF), and Belt Freezing), By Distribution Channel (Supermarkets & Hypermarkets, Food Service/HoReCa, and E-Commerce) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Unilever PLC, Nestlé S.A., General Mills, Inc., Nomad Foods Ltd., Tyson Foods Inc., Conagra Brands Inc., Wawona Frozen Foods, Bellisio Parent, LLC, Kellanova, The Kraft Heinz Company, OOB Organic, Omar International Pvt Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |