Quick Navigation

Report Overview

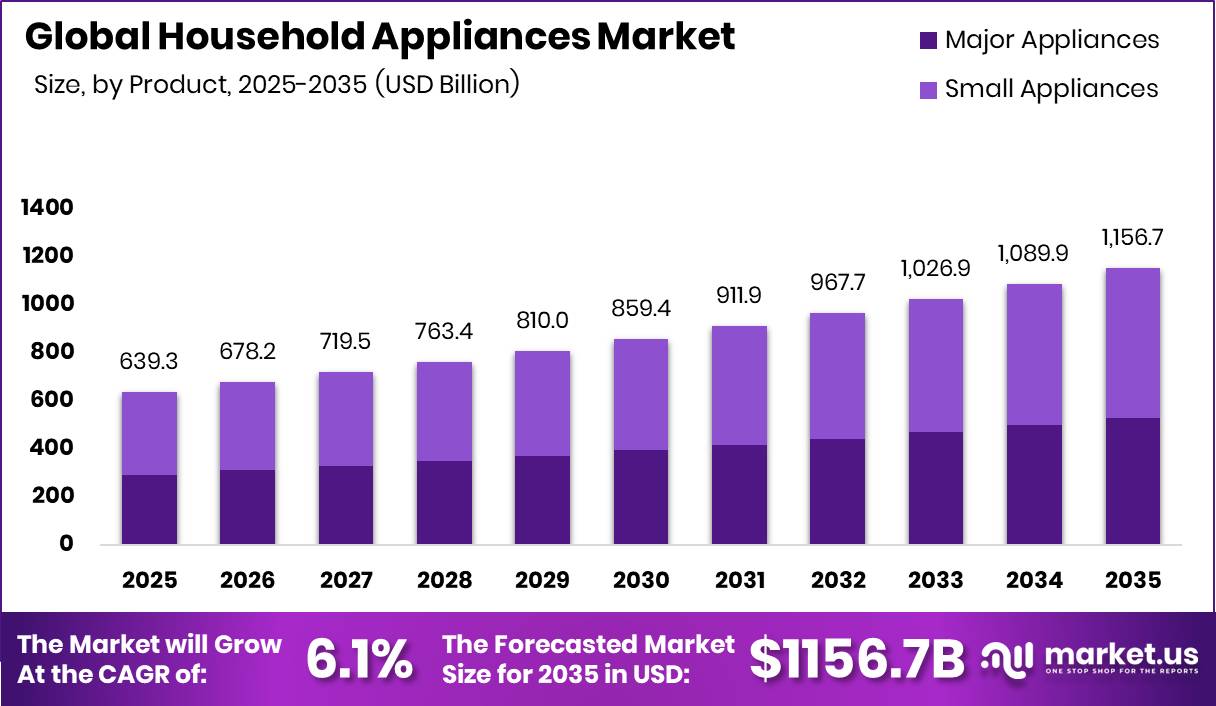

Global Household Appliances Market size is expected to be worth around USD 1,156.7 Billion by 2035 from USD 639.3 Billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035. This trajectory places the market among the largest consumer durables sectors globally, with absolute value addition exceeding USD 517 Billion over the decade.

The household appliances market covers electrical and mechanical devices used in residential settings for food preparation, fabric care, climate control, and personal grooming. This market splits into two core product tiers: major appliances such as refrigerators, washing machines, and air conditioners, and small appliances including coffee makers, air fryers, and electric trimmers. Distribution spans electronic stores, supermarkets, exclusive brand outlets, and online channels.

Key Takeaways

- Global Household Appliances Market was valued at USD 639.3 Billion in 2025.

- The market is forecast to reach USD 1,156.7 Billion by 2035, at a CAGR of 6.1%.

- Small Appliances dominates the By Product segment with a 54.2% share.

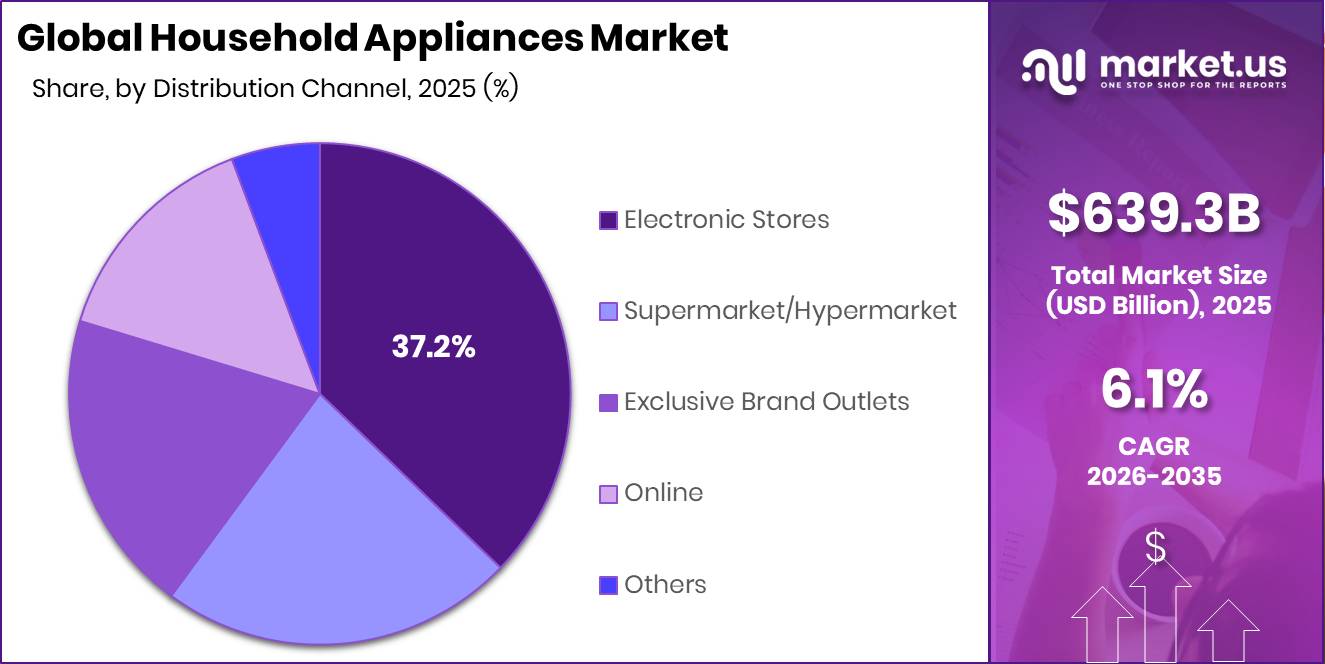

- Electronic Stores leads By Distribution Channel with a 37.2% share.

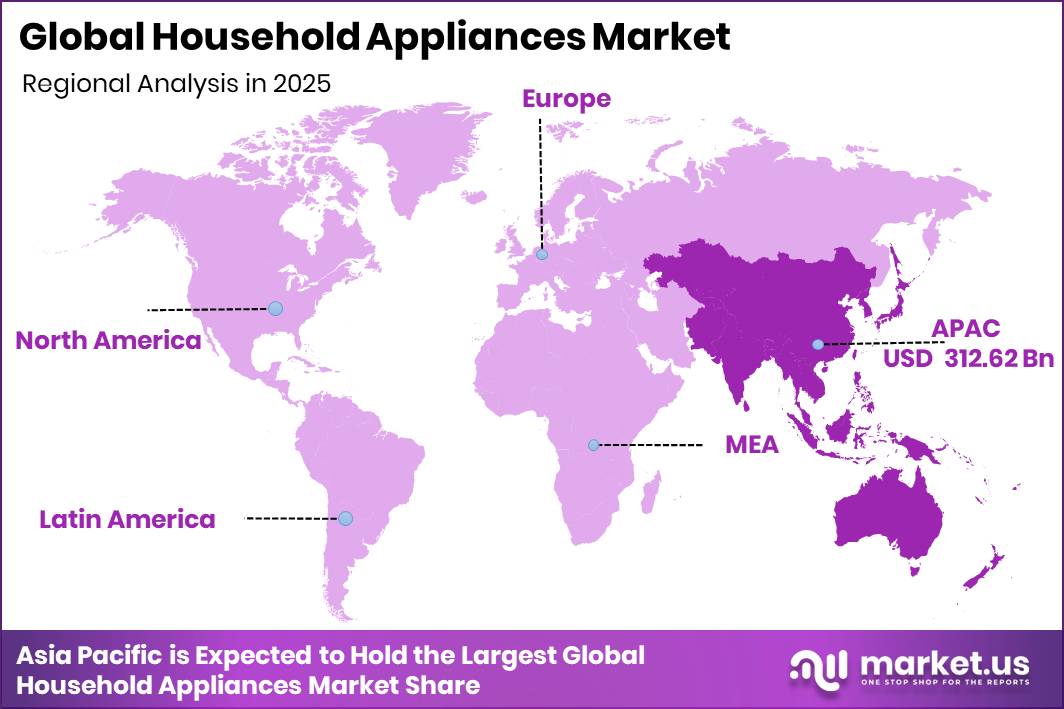

- Asia Pacific dominates regional market share at 48.9%, valued at USD 312.6 Billion.

According to the U.S. Energy Information Administration, water heating, lighting, and refrigeration together represented 25% of total annual household energy consumption in U.S. residences in 2020. This concentration of energy use within core appliance categories means energy efficiency upgrades in refrigerators and water heaters directly reduce household operating costs, strengthening consumer willingness to replace aging units.

Data from a 2025 field study shows that model-predictive control systems for heat pump water heaters reduced energy consumption by 37% compared with constant high-temperature operation. This performance gap between legacy and advanced systems creates a measurable economic case for replacement. As reported by the same study, electricity-cost reductions reached 23% under time-of-use pricing and 28% under hourly pricing, further reinforcing consumer demand for technology-upgraded appliances. In December 2025, LG Electronics unveiled its next-generation LG SIGNATURE refrigerator featuring integrated generative AI functionality, signaling that premium OEMs are embedding AI as a core product architecture rather than an optional feature.

Segments Overview

Product Analysis

Small Appliances dominates with 54.2% due to high purchase frequency and lower unit price.

In 2025, Small Appliances held a dominant market position in the By Product segment of the Household Appliances Market, with a 54.2% share. This majority position reflects the breadth of the sub-category, spanning coffee makers, air fryers, hair dryers, and air purifiers, which carry lower price points and shorter replacement cycles than major appliances. Vendors serving this segment benefit from higher annual transaction volumes per household.

Major Appliances account for 45.8% of the product segment, covering refrigerators, washing machines, air conditioners, and dishwashers. These products carry higher average selling prices and longer replacement cycles, making each sale higher in value but lower in frequency. In June 2025, Samsung launched the Bespoke AI Laundry Combo, integrating washing and drying into a single unit with AI fabric care, a direct response to urban households seeking space-saving multi-function solutions that compress replacement decisions into a single higher-value purchase.

Distribution Channel Analysis

Electronic Stores dominate with 37.2% due to hands-on product comparison demand.

In 2025, Electronic Stores held a dominant market position in the By Distribution Channel segment of the Household Appliances Market, with a 37.2% share. This leadership reflects consumer preference for in-store evaluation before committing to high-value appliance purchases. For manufacturers, strong electronic store placement directly influences brand visibility and allows premium product features to be demonstrated at point of sale.

Supermarkets and Hypermarkets hold a 23% channel share, driven by convenience purchasing for small appliances and impulse-driven accessories. This channel suits lower-complexity products where brand recognition substitutes for in-store demonstration. In March 2025, Samsung launched the Bespoke AI Jet Ultra cordless vacuum with up to 400W suction power and AI-powered cleaning optimization, a product whose feature complexity suits dedicated electronic store demonstration over impulse channels.

Online channels account for 15% of distribution, a share that understates strategic importance given its faster growth trajectory relative to physical formats. Online platforms lower the cost of market entry for challenger brands and compress geographic barriers. This creates direct pricing pressure on exclusive brand outlets, which hold a 20% share but face margin erosion as price comparison shifts online.

Key Market Segments

By Product

- Major Appliances

- Water Heater

- Dishwasher

- Refrigerator

- Cooktop, Cooking Range, Microwave, and Oven

- Vacuum Cleaner

- Washing Machine and Dryers

- Air Conditioner

- Small Appliances

- Coffee Makers

- Juicers, Blenders and Food Processors

- Hair Dryers

- Irons

- Deep Fryers

- Space Heater

- Electric Trimmers and Shavers

- Air Purifiers

- Humidifiers and Dehumidifiers

- Rice Cookers and Steamers

- Air Fryers

By Distribution Channel

- Supermarket/Hypermarket

- Electronic Stores

- Exclusive Brand Outlets

- Online

- Others

Drivers

Mandatory energy efficiency legislation across the EU, India, and Southeast Asia functions as a government-mandated demand accelerant, forcing retirement of legacy appliances before natural end of life. The EU’s Ecodesign for Sustainable Products Regulation entered into force on 18 July 2024, covering refrigerators, washing machines, air conditioners, and other major categories. India’s Bureau of Energy Efficiency Appliance Labelling and Compliance Regulations took effect on 1 January 2026, adding QR-coded star labels, BIS lab testing, and penalty provisions for non-compliance.

The IEA’s Energy Efficiency 2025 report confirmed that global energy intensity improved at only 1.8% in 2025, far below the 4% annual rate required by 2030 COP28 targets, with over 250 new or updated energy efficiency policies announced globally in 2025 alone. This regulatory gap signals further tightening well through 2030. According to the U.S. Energy Information Administration, space heating and air conditioning alone accounted for 52% of total U.S. household energy consumption in 2020, establishing these categories as the highest-priority targets for efficiency-driven replacement mandates. Figures from ENERGY STAR show certified clothes washers use approximately 20% less energy and about 30% less water than conventional washers, which directly quantifies the cost savings that justify consumer replacement spending.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI and IoT Integration — Smart ecosystems via AI, edge computing, Matter/Thread interoperability | +1.8% | North America core; APAC corridors (China, India, South Korea); EU spill-over | Short to Medium term (1–4 yrs) |

| Urbanization and Middle-Class Expansion — Rising incomes, first-time appliance ownership in emerging economies | +1.5% | APAC corridors (India, SE Asia); South America spill-over; Africa frontier | Medium to Long term (3–7 yrs) |

| Mandatory Energy Efficiency Regulations — EU ESPR, BEE Compliance Norms 2026, IEA MEPS mandates | +1.2% | EU core; India; Australia; SE Asia | Short to Medium term (1–4 yrs) |

| E-Commerce and D2C Channel Expansion — Digital-first journeys via BNPL, quick-commerce, social commerce | +0.9% | APAC corridors (India, China); North America; Western Europe | Short term (2 yrs or less) |

| Premiumization and Multi-Functionality — Feature-rich, design-forward upgrades in urban markets | +0.8% | North America; EU; Urban APAC (India, China); GCC | Medium term (2–4 yrs) |

| Inverter and BLDC Motor Technology — Efficiency-led hardware platform replacing legacy induction motors | +0.6% | India core; APAC corridors; EU and North America replacement market | Medium term (2–4 yrs) |

Restraints

Chinese household appliance brands expanded their global market share by 40.1% in Small Domestic Appliances and by 23.5% in Major Domestic Appliances in the first half of 2025, according to NIQ’s Home Appliances Outlook 2026. The MDA share gain traces to competitive pricing rather than product innovation, signaling that Chinese OEMs are using a structural cost advantage of approximately 20 to 30% relative to Western incumbents to systematically compress average selling prices across export markets.

As per our research indicates that a NIQ survey of 24,000 consumers in China found that 71% used government trade-in subsidies to upgrade appliances by end 2024, accelerating domestic inventory turnover and creating surplus export capacity now deployed in Europe, Southeast Asia, the GCC, and Latin America. The U.S. Energy Information Administration data shows televisions, cooking appliances, clothes washers, dryers, and computers accounted for 23% of total U.S. residential energy consumption in 2020. This breadth of electrified product categories amplifies ASP deflation risk, as Chinese OEMs compete across virtually every major energy-consuming appliance category simultaneously.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity and Freight Cost Inflation (Copper, Aluminium, Steel) | -1.0% | Global; concentrated in import-dependent markets — North America, EU, South and Southeast Asia | Medium term (2–4 years) |

| US–China Tariff Regime and Trade Fragmentation | -0.9% | North America core; secondary effects across EU, APAC sourcing corridors | Short to Medium term (1–3 years) |

| Housing Market Stagnation and Deferred Replacement Demand | -0.8% | North America, India metros, China tier-1 cities | Short to Medium term (1–3 years) |

| Escalating Energy-Efficiency Regulatory Compliance Burden | -0.7% | EU (Ecodesign Regulation 2023/826), US (DOE MEPS), India (BEE star-rating mandates) | Medium to Long term (2–5 years) |

| China Rare Earth and Permanent Magnet Export Controls | -0.6% | Global; most acute for US-bound supply chains and motor-intensive appliance categories | Medium to Long term (2–5 years) |

| Intensified Price Competition from Chinese OEM Expansion | -0.5% | Global; most acute in APAC, EU budget segment, GCC, and Latin America | Medium term (2–4 years) |

Challenges

The U.S. imposed a 145% tariff on Chinese imports at peak in 2025, partially reduced to approximately 20% in additional levies plus approximately 25% on many Chinese industrial products under the October 2025 trade truce framework. U.S. aggregate tariffs on Chinese goods now sit at nearly 48% compared to a pre-Trump baseline of 3.1%. This structural tariff elevation directly inflates appliance input costs for manufacturers sourcing from China.

By mid 2026, ovens averaged approximately 9% price increases and washers and dryers rose close to 6% compared to mid 2025 levels. The Trump administration additionally proposed new 12.5% forced labor-related tariffs in June 2026 targeting China and 44 other nations, while a potential 15% copper tariff is under consultation for 2027 implementation. These cost layers reduce consumer affordability and compress OEM margins simultaneously, creating a dual revenue and cost squeeze across the supply chain.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Geopolitical Tariff and Trade Protectionism | ~-0.8% | North America, EU–China corridors, APAC export hubs | Medium term (2–4 years) |

| Memory and Semiconductor Supply Tightness | ~-0.7% | East Asia OEM hubs, North America, Western Europe | Long term (4 years or more) |

| Raw Material and Industrial Commodity Inflation | ~-0.6% | Global; acute in North America, EU manufacturing zones | Medium term (2–4 years) |

| Multi-Jurisdictional Energy Efficiency Compliance | ~-0.5% | India BEE-regulated markets, EU ecodesign zones, North America | Long term (4 years or more) |

| Technical Talent and Skilled Workforce Deficit | ~-0.5% | North America, EU manufacturing belts, emerging APAC factories | Long term (4 years or more) |

| Smart Appliance Interoperability and Ecosystem Fragmentation | ~-0.4% | North America smart-home markets, Western Europe, urban APAC | Medium term (2–4 years) |

Opportunities

Fewer than 8% of major white goods shipped globally in 2025 incorporated validated health sensing hardware as a core product tier. This gap between consumer wellness expectations and current product architecture represents a structurally untapped adjacent market for appliance OEMs. A premium health-feature tier incorporating PM2.5 sensing, VOC detection, and nutritional analytics in cooking appliances could command a 25 to 40% price premium over base SKUs.

Deloitte’s Digital Consumer Trends 2026 documents that 63% of UK consumers had used a generative AI application by May 2026, confirming broad consumer readiness for AI-powered health and energy monitoring interfaces embedded in appliance apps. EU Ecodesign and EPBD frameworks provide regulatory momentum for stricter indoor environment standards through 2030. This creates a two to four year execution window that aligns directly with major OEM product development and homologation cycles.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Appliance-as-a-Service (AaaS) OEM Subscription Monetization | +1.8% | APAC (Singapore, India, SE Asia), EU (Sweden, UK) | Short term (2 years or less) |

| Health and Wellness Feature Integration in White Goods | +1.5% | North America, EU, China, Urban APAC | Medium term (2–4 years) |

| Sub-Saharan Africa and Frontier South Asia TAM Expansion | +2.2% | Sub-Saharan Africa, India Tier-2/3, Bangladesh, Pakistan | Medium term (2–4 years) |

| AI-Enabled Predictive Maintenance as Recurring Revenue | +1.3% | North America, EU, Japan, South Korea | Medium term (2–4 years) |

| Circular Economy and OEM-Led Refurbishment Recommerce | +1.0% | EU, India, ASEAN, Latin America | Short-to-Medium term (1–3 years) |

| B2B Institutional Channel Build-Out (Hospitality, Co-Living, Multifamily) | +1.6% | North America, Middle East, APAC | Long term (4 years or more) |

Regional Analysis

Asia Pacific Dominates the Household Appliances Market with a Market Share of 48.9%, Valued at USD 312.6 Billion

Asia Pacific holds a near-majority share of the global household appliances market, driven by urbanization velocity, a rapidly expanding middle class in China, India, and Southeast Asia, and first-time appliance ownership at scale. The region’s manufacturing depth, anchored in China and increasingly Vietnam and India, gives domestic producers a structural cost advantage that foreign incumbents cannot replicate. This dual demand and supply concentration locks in Asia Pacific’s regional leadership through the forecast period.

North America represents a high-value replacement market where energy efficiency mandates and smart home adoption drive premiumization. In June 2025, GE Appliances announced a USD 490 million investment to relocate washing machine production from China to its Kentucky facilities, reflecting both tariff-driven supply chain restructuring and an opportunity to market domestically produced appliances to cost-sensitive American consumers. This investment signals a structural shift in North American appliance sourcing economics.

Europe operates under the EU Ecodesign for Sustainable Products Regulation, which entered into force on 18 July 2024 and mandates Digital Product Passports from 2027 to 2028 across regulated appliance categories. This compliance burden raises minimum product quality floors, suppressing low-cost import competition and rewarding incumbent OEMs with established energy-efficient product lines. As a result, average selling prices in European appliance categories are structurally elevated relative to other regions.

Latin America and the Middle East and Africa represent frontier expansion zones where rising household income, urban infrastructure investment, and expanding retail channels support first-time appliance ownership. However, both regions lack the regulatory frameworks and grid infrastructure that drive premium tier adoption seen in North America and Europe. This means market entry in these regions requires volume-led strategies rather than margin-led premiumization.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Whirlpool Corporation maintains its competitive position through a broad North American distribution network and a strong brand portfolio spanning multiple price tiers. Its domestic manufacturing footprint positions it to benefit directly from tariff-driven reshoring of appliance production. However, its slower integration of AI-powered features relative to Asian OEMs creates a product differentiation risk in the premium smart appliance segment.

Samsung Electronics Co. Ltd. has positioned itself as the innovation leader in connected and AI-enabled household appliances. In December 2025, Warburg Pincus and Bharti Enterprises agreed to acquire a combined 49% stake in Haier India, valued at approximately USD 1.67 billion, signaling intensified competition in the Indian market where Samsung holds a significant presence. Samsung’s aggressive product launch cadence across vacuum, laundry, and refrigeration categories reinforces its first-mover advantage in AI-integrated appliances.

Key Players

- Whirlpool Corporation

- Samsung Electronics Co. Ltd.

- Robert Bosch GmbH

- LG Electronics Inc.

- Electrolux AB

- Haier Smart Home Co., Ltd.

- Panasonic Corporation

- Sharp Corporation

- Miele

- Midea Group

Recent Developments

- January 2026 – Bosch launched its first Matter-enabled refrigerator, the 100 Series French Door Bottom Mount Refrigerator, supporting cross-platform interoperability across Matter-compatible smart home ecosystems.

- January 2026 – Hisense introduced the ConnectLife AI-powered X-Zone Master Washer-Dryer featuring a modular multi-drum architecture and AI-based fabric recognition technology.

- January 2026 – Samsung unveiled the Bespoke AI Jet Bot Steam Ultra robotic vacuum with liquid detection, obstacle recognition, and autonomous cleaning capabilities.

- January 2026 – Bosch expanded its smart appliance portfolio by introducing Matter connectivity support for major home appliance categories through its Home Connect ecosystem.

- January 2026 – Hisense showcased AI-powered kitchen appliances integrated with its ConnectLife platform, enabling cross-device automation between refrigerators, cooking appliances, and laundry systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 639.3 Billion |

| Forecast Revenue (2035) | USD 1,156.7 Billion |

| CAGR (2026-2035) | 6.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Major Appliances: Water Heater, Dishwasher, Refrigerator, Cooktop/Cooking Range/Microwave/Oven, Vacuum Cleaner, Washing Machine and Dryers, Air Conditioner; Small Appliances: Coffee Makers, Juicers/Blenders/Food Processors, Hair Dryers, Irons, Deep Fryers, Space Heater, Electric Trimmers and Shavers, Air Purifiers, Humidifiers and Dehumidifiers, Rice Cookers and Steamers, Air Fryers); By Distribution Channel (Supermarket/Hypermarket, Electronic Stores, Exclusive Brand Outlets, Online, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Whirlpool Corporation, Samsung Electronics Co. Ltd., Robert Bosch GmbH, LG Electronics Inc., Electrolux AB, Haier Smart Home Co., Ltd., Panasonic Corporation, Sharp Corporation, Miele, Midea Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |