Quick Navigation

Report Overview

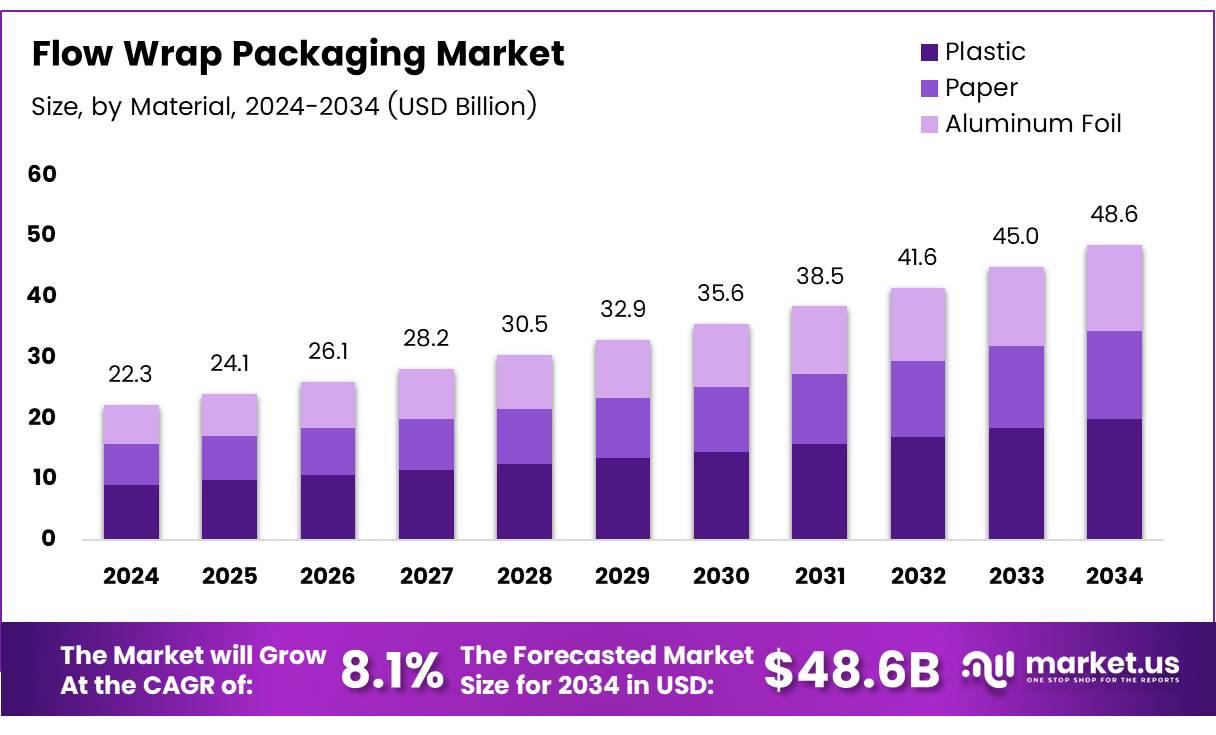

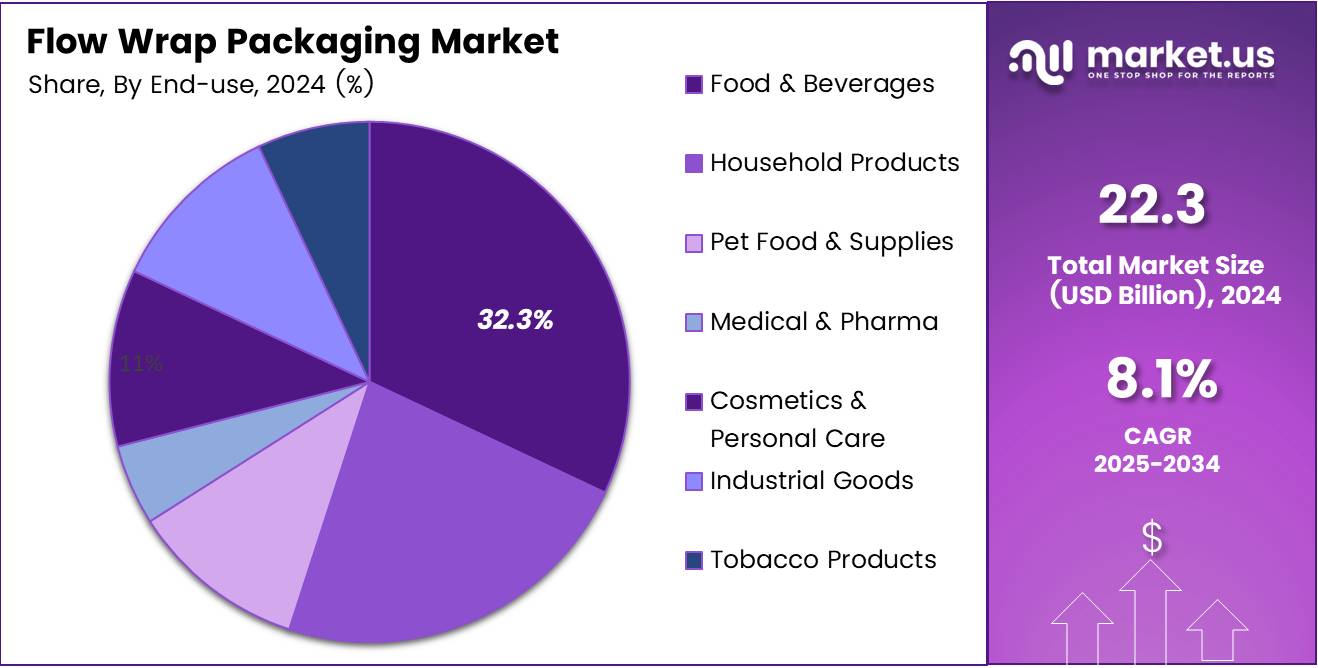

The Global Flow Wrap Packaging Market size is expected to be worth around USD 48.6 Billion by 2034, from USD 22.3 Billion in 2024, growing at a CAGR of 8.1% during the forecast period from 2025 to 2034.

Flow wrap packaging, a prevalent method within the packaging industry, involves wrapping products with plastic or other flexible materials using automated equipment. This method is distinguished by its speed and efficiency, typically utilized for consumer goods like food, electronics, and pharmaceuticals. The market for flow wrap packaging is expanding, driven by the growing demand for convenient, durable, and sustainable packaging solutions.

The capability of flow wrap machines, as highlighted by Jakpak, to efficiently produce up to 70 packs per minute underscores their critical role in high-volume manufacturing environments. This efficiency not only boosts production rates but also reduces labor costs and enhances overall operational effectiveness.

The flow wrap packaging market is experiencing significant growth, fueled by several key factors. Firstly, the increase in consumer demand for products with extended shelf life and easy accessibility is a major driver. Additionally, advancements in packaging technology that offer improved durability and product protection further propel this market’s expansion.

Government investment and regulatory frameworks also play pivotal roles. Regulations focusing on sustainability and waste reduction are prompting companies to adopt more eco-friendly packaging solutions.

For example, as reported by TalkingRetail, the flow wrapping process has enabled a 35% reduction in plastic packaging for certain products, translating to an annual saving of 100 tonnes of packaging material. This not only aligns with environmental objectives but also resonates with the growing consumer preference for sustainable practices.

The opportunities within the flow wrap packaging market are vast, particularly in terms of sustainability and technological innovation. The trend towards using recycled content in packaging materials is gaining momentum.

As noted by PepsiCo, some brands have successfully incorporated up to 50% recycled content in their packaging, showcasing a significant shift towards more sustainable packaging practices. This not only helps companies meet regulatory requirements but also enhances brand reputation and consumer loyalty.

In Germany, the consumption of plastic packaging hit 3.22 million tons in 2022, according to Study. This statistic highlights the substantial market size and the potential for introducing more sustainable materials and processes. Companies that can innovate to reduce plastic use or enhance recyclability will likely gain competitive advantages.

Key Takeaways

- Global Flow Wrap Packaging Market projected to grow from USD 22.3 Billion in 2024 to USD 48.6 Billion by 2034, at a CAGR of 8.1%.

- Plastic leads the Material Analysis segment with a 61.3% share in 2024 due to its cost-effectiveness and durability.

- Packaged Snacks dominate the Application Analysis segment, holding a 34.1% market share in 2024.

- Food & Beverages sector is the largest in the End-use Analysis segment, with a 32.3% share in 2024.

- Asia Pacific is the leading region in the market, accounting for 40.2% share, driven by rapid industrialization and investment in packaging technologies.

Material Analysis

Plastic Continues to Lead in Flow Wrap Packaging with 61.3% Market Share

In 2024, the By Material Analysis segment of the Flow Wrap Packaging Market was predominantly led by plastic, commanding a substantial 61.3% share. This dominance is attributed to plastic’s remarkable flexibility, durability, and cost-effectiveness, which make it highly preferred for preserving the quality and extending the shelf life of packaged goods. Furthermore, advancements in recycling processes and increased consumer awareness have mitigated some environmental concerns associated with plastic, bolstering its widespread adoption.

Paper material, recognized for its eco-friendliness and sustainability, also plays a critical role in the market. As businesses and consumers increasingly prioritize green packaging solutions, paper-based flow wrap packaging is gaining traction. This shift is driven by improving recycling practices and innovations in barrier technologies that enhance paper’s protective qualities without compromising biodegradability.

Aluminum foil, though a smaller segment, is valued for its superior barrier properties against moisture, light, and odors, making it an excellent choice for food products requiring extended shelf life. Despite its higher cost, aluminum foil remains a key material in specific applications where preservation and product integrity are paramount.

Each material brings distinct advantages to the table, shaping the dynamics of the Flow Wrap Packaging Market as manufacturers tailor solutions to meet evolving consumer preferences and regulatory standards.

Application Analysis

Packaged Snacks Lead the Way in Flow Wrap Packaging with a 34.1% Market Share

In 2024, the Flow Wrap Packaging Market witnessed significant growth in the By Application Analysis segment, with Packaged Snacks securing a leading position. Capturing a substantial 34.1% market share, this segment outperformed other categories due to its high demand across various consumer bases.

Packaged snacks, which typically include items like chips, nuts, and pretzels, benefit immensely from flow wrap packaging, as it extends shelf life and preserves freshness while offering convenience to consumers.

Following closely, the Chocolate & Confectionery segment also leveraged flow wrap technology to maintain product integrity and appeal with attractive, protective wrapping. Personal Hygiene Products, another major category, utilized flow wrapping to ensure sanitary packaging and ease of use, which is crucial for items such as wipes and diapers.

The Bakery Products segment capitalized on flow wrap packaging to address concerns over food safety and shelf life extension, making products like bread and pastries safer and longer-lasting on shelves. Medical Devices, though a smaller segment in this analysis, recognized flow wrap packaging as essential for maintaining sterility and providing user-friendly packaging solutions in healthcare environments.

Overall, the dominance of Packaged Snacks in the flow wrap packaging market underscores the segment’s adaptability and consumer appeal, driving forward market trends and packaging innovations.

End-use Analysis

Dominance of Food & Beverages in Flow Wrap Packaging with a 32.3% Market Share

In 2024, the Food & Beverages sector maintained a commanding presence in the By End-use Analysis segment of the Flow Wrap Packaging Market, capturing a significant 32.3% share. This sector’s dominance is largely attributable to the increasing demand for convenient, sustainable packaging solutions that align with the fast-paced lifestyle of modern consumers.

Flow wrap packaging, known for its efficiency and cost-effectiveness, is particularly favored in the food and beverage industry because it extends the shelf life of products while maintaining freshness.

Following closely, sectors such as Household Products and Pet Food & Supplies also leveraged flow wrap technology to enhance product appeal and ensure protection against contaminants.

The Medical & Pharma sector, driven by stringent regulations requiring robust and sterile packaging, increasingly adopted flow wrap solutions to meet safety standards. Similarly, the Cosmetics & Personal Care industry utilized this packaging to offer attractive yet durable packaging options that protect sensitive products during transit.

Furthermore, Industrial Goods and Tobacco Products sectors are not far behind, integrating flow wrap packaging to optimize durability and streamline manufacturing processes. This broad adoption across various industries highlights the versatility and efficiency of flow wrap packaging, making it a cornerstone in modern packaging strategies.

Key Market Segments

By Material

- Plastic

- Paper

- Aluminum Foil

By Application

- Packaged Snacks

- Chocolate & Confectionary

- Personal Hygiene Products

- Bakery Products

- Medical Devices

By End-use

- Food & Beverages

- Household Products

- Pet Food & Supplies

- Medical & Pharma

- Cosmetics & Personal Care

- Industrial Goods

- Tobacco Products

Drivers

E-commerce Expansion Spurs Growth in Flow Wrap Packaging Market

The flow wrap packaging market is experiencing robust growth, primarily fueled by the e-commerce boom, as online shopping surges globally, necessitating more efficient and durable packaging solutions. This trend is closely intertwined with escalating consumer demand for sustainability, prompting a shift towards biodegradable packaging materials in the flow wrap sector.

Technological advancements further propel the market, with innovations in printing technologies, barrier materials, and the integration of smart packaging solutions that enhance product functionality, safety, and consumer engagement.

Additionally, significant growth in the pharmaceuticals and healthcare industries demands higher standards for protective and tamper-evident packaging to ensure the safety and integrity of medicines and medical devices. These drivers collectively push the boundaries of the flow wrap packaging market, making it a critical component in modern packaging strategies and sustainability efforts.

Restraints

Environmental Scrutiny Challenges Flow Wrap Packaging Adoption

The flow wrap packaging market faces significant challenges, particularly from environmental concerns associated with the use of non-biodegradable plastics. As global awareness and regulatory pressures mount, the industry is grappling with increasing consumer backlash and stricter environmental regulations, which necessitate shifts toward more sustainable packaging options.

Additionally, the high initial investment required for advanced flow wrap machinery and automation technologies poses a substantial barrier for new entrants and can deter smaller players from adopting these innovations. These restraints complicate market expansion, as companies must balance cost considerations with the need for environmentally friendly and technologically advanced packaging solutions to remain competitive and compliant in a rapidly evolving market landscape.

Growth Factors

Innovations in Sustainable Materials Open New Avenues in Flow Wrap Packaging

The flow wrap packaging market is ripe with growth opportunities, particularly through the development of biodegradable and compostable packaging solutions. These innovations are driven by increasing consumer and regulatory demand for sustainable packaging materials.

Additionally, the adoption of smart packaging technologies, such as QR codes, NFC tags, and sensors, offers manufacturers the chance to enhance consumer engagement through interactive packaging. There is also a growing trend towards customization and personalization in packaging, with consumers increasingly seeking unique, printed, and customized packaging options that stand out on retail shelves.

Furthermore, the market is set to expand significantly in emerging regions such as Asia-Pacific and Latin America, where rising disposable incomes and rapid urbanization are driving demand for sophisticated packaging solutions. These factors collectively present lucrative opportunities for players in the flow wrap packaging industry to innovate and capture new markets.

Emerging Trends

Surging Interest in Recyclable Materials Shapes Flow Wrap Packaging Trends

The flow wrap packaging market is witnessing significant trends centered around sustainability and technological integration. There’s a noticeable rise in the use of recyclable materials, reflecting a broader industry shift towards more sustainable packaging solutions. Innovations in edible packaging are also gaining traction, with ongoing research into edible and biodegradable films that offer an environmentally friendly alternative to traditional packaging.

Additionally, the adoption of eco-friendly inks, such as water-based and soy-based options, is on the rise, aligning with global efforts to reduce the environmental impact of packaging production. The growth of paper-based flow wrap packaging further indicates a shift away from plastic-based wraps, as companies and consumers alike seek out greener alternatives.

Moreover, digital and AI-enabled technologies are increasingly employed in packaging production, enhancing automation and quality control systems to improve efficiency and product safety. These trends collectively signal a transformative period in the flow wrap packaging market, driven by a convergence of sustainability goals and technological advancements.

Regional Analysis

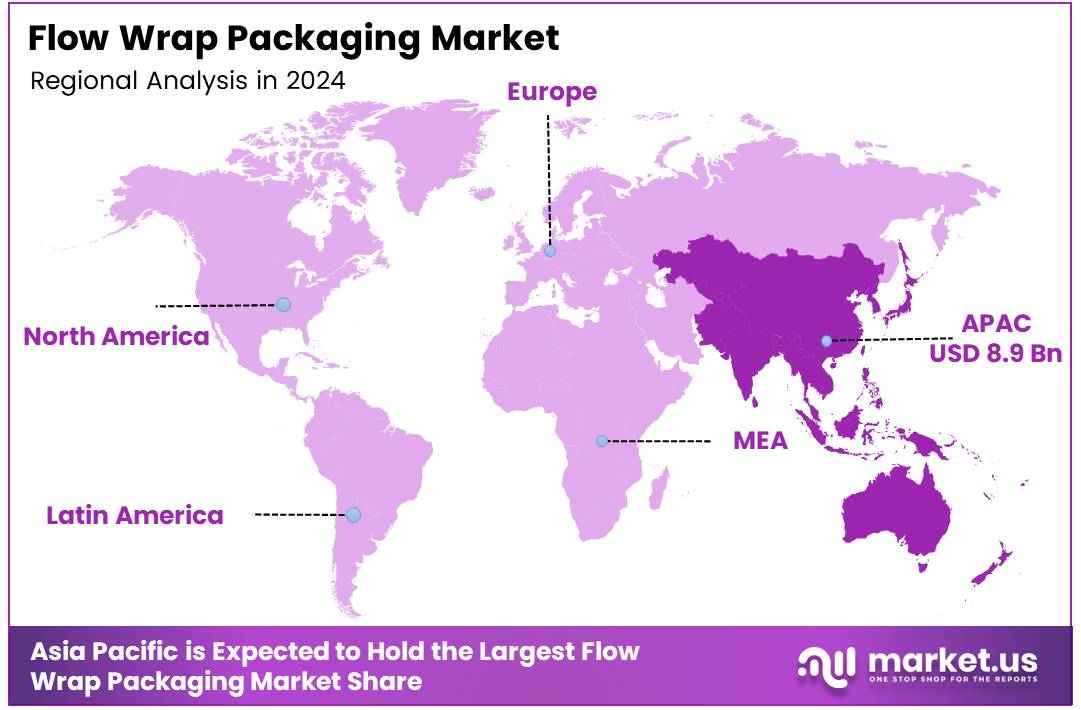

Asia Pacific Dominates Flow Wrap Packaging Market with a 40.2% Share Worth USD 8.92 Billion, Driven by Rapid Industrial Growth and Expanding Consumer Base

The global Flow Wrap Packaging market is distinctly segmented across various regions, each presenting unique growth dynamics and opportunities. Asia Pacific leads the market with a dominant share of 40.2%, valued at USD 8.92 billion, driven by rapid industrialization, expanding consumer markets, and substantial investments in packaging technologies.

This region benefits from the presence of large manufacturing bases in countries like China and India, which are increasingly adopting flexible packaging solutions to meet the demands of a growing middle class.

Regional Mentions:

In North America, the market is characterized by high demand for sustainable and innovative packaging solutions, catering to the evolving preferences of environmentally conscious consumers. The region’s strong regulatory framework promoting eco-friendly packaging materials has further propelled the adoption of flow wrap packaging in sectors such as food & beverages and pharmaceuticals.

Europe’s market is bolstered by stringent food safety regulations which require reliable and hygienic packaging solutions. European countries are pioneering in the adoption of automation in packaging processes, enhancing efficiency and consistency in packaging standards. The focus on recyclability and minimal plastic use aligns well with the region’s aggressive environmental targets.

The Middle East & Africa region is witnessing gradual growth in the Flow Wrap Packaging market. This growth is fueled by the expanding retail sector and increasing urbanization, with Gulf countries like Saudi Arabia and the UAE leading the way in luxury goods packaging, which demands high-quality and aesthetically pleasing packaging options.

Latin America shows potential for growth in flow wrap packaging, supported by the development of the food processing and pharmaceutical industries. The increase in modern retail formats is driving the demand for cost-effective yet durable packaging solutions that extend the shelf life of products.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global flow wrap packaging market continues to expand, driven by innovations in sustainability and technological advancements. Among the key players, Amcor plc stands out for its proactive approach in integrating eco-friendly materials and practices. This strategic focus is in response to increasing regulatory pressures and consumer demand for sustainable packaging solutions.

Constantia Flexibles Group and Huhtamäki OYJ are also significant contributors to the market’s growth, particularly in developing highly flexible and customized packaging solutions that cater to the evolving needs of the food and pharmaceutical sectors. These companies have successfully leveraged advanced printing technology to enhance brand visibility and consumer engagement.

Billerud AB and Sealed Air Corporation have made notable strides in improving the mechanical properties of packaging, which enhances product protection while reducing material use. Their efforts in creating high-barrier and durable packaging solutions have set industry benchmarks, particularly in perishable goods sectors.

Emerging players like ePac Holdings, LLC and Polysack Flexible Packaging Ltd. have carved out niche positions with their quick-turnaround and cost-effective solutions, particularly appealing to small and medium enterprises (SMEs). This agility has allowed them to capture significant market shares in a relatively short time frame.

MONDI PLC and Sonoco Products Company continue to excel in integrating digital and smart technologies, such as QR codes and NFC tags, which add value beyond traditional packaging by enhancing user interaction and traceability.

Overall, the key players in the 2024 flow wrap packaging market are characterized by their vigorous pursuit of innovation, sustainability, and customer-centric solutions, aligning closely with global trends and regulatory landscapes. These efforts not only drive their growth but also shape the competitive dynamics of the industry.

Top Key Players in the Market

- Amcor plc

- Constantia Flexibles Group

- Huhtamäki OYJ

- Billerud AB

- Sealed Air Corporation

- Polysack Flexible Packaging Ltd.

- MONDI PLC

- Sonoco Products Company

- Glenroy, Inc

- Coveris Holdings S.A

- ePac Holdings, LLC.

- Asteria Group (Packaging PrintCo NV)

- Winpak LTD.

- KM Packaging Services Ltd.

Recent Developments

- In December 2024, Movopack successfully secured $2.5 million in funding to enhance their development of sustainable packaging solutions aimed at reducing ecommerce waste.

- In December 2024, Bpacks obtained a €1 million pre-seed investment to launch the world’s first completely compostable packaging made from bark, marking a significant innovation in eco-friendly materials.

- In November 2024, Ukhi raised $1.2 million to expand their production of sustainable biomaterials, focusing on creating environmentally friendly packaging options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 22.3 Billion |

| Forecast Revenue (2034) | USD 48.6 Billion |

| CAGR (2025-2034) | 8.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Plastic, Paper, Aluminum Foil), By Application (Packaged Snacks, Chocolate and Confectionary, Personal Hygiene Products, Bakery Products, Medical Devices), By End-use (Food and Beverages, Household Products, Pet Food and Supplies, Medical and Pharma, Cosmetics and Personal Care, Industrial Goods, Tobacco Products) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amcor plc, Constantia Flexibles Group, Huhtamäki OYJ, Billerud AB, Sealed Air Corporation, Polysack Flexible Packaging Ltd., MONDI PLC, Sonoco Products Company, Glenroy, Inc, Coveris Holdings S.A, ePac Holdings, LLC., Asteria Group (Packaging PrintCo NV), Winpak LTD., KM Packaging Services Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |