Global Farm Implements Market Size, Share, And Industry Analysis Report By Product Type (Tractors, Harvesters, Soil Preparation and Cultivation Equipment, Planting, Seeding, and Fertilizing Equipment, Irrigation and Crop Protection Implements, Precision and Autonomous Implements, Haying and Forage Equipment), By Mode of Operation (Powered Implements, Unpowered Implements), By Power Output (Below 30 HP, 31 to 70 HP, 71 to 130 HP, Above 130 HP), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181130

- Number of Pages: 233

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

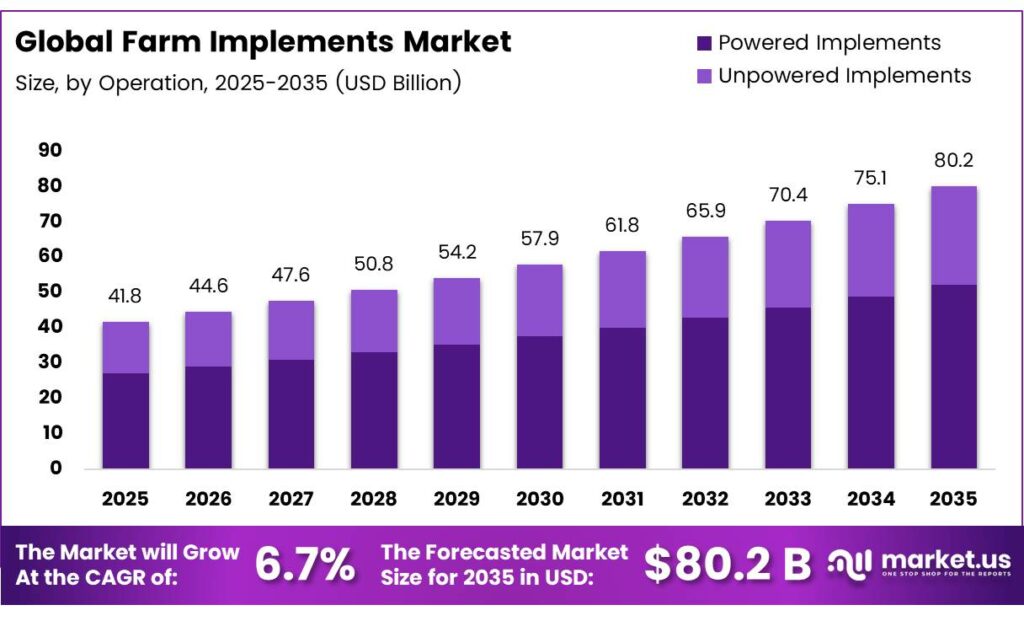

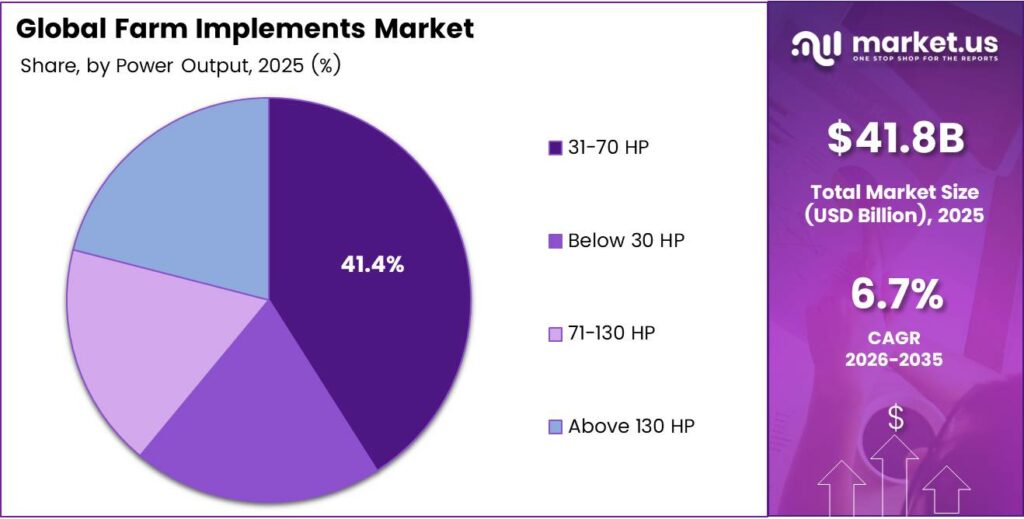

The Global Farm Implements Market size is expected to be worth around USD 80.2 billion by 2035 from USD 41.8 billion in 2025, growing at a CAGR of 6.7% during the forecast period 2026 to 2035.

Farm implements refer to the broad category of machinery and equipment used in agricultural operations. These tools include tractors, harvesters, soil preparation equipment, and advanced precision systems. Farmers and agribusinesses rely on these implements to improve productivity, reduce manual effort, and optimize resource use across diverse crop production cycles.

Modern farm implements cover everything from basic soil tillage tools to GPS-guided autonomous machinery. Consequently, the market spans multiple product segments serving smallholder farms in developing nations as well as large commercial operations in North America and Europe. This diversity in end-user profiles drives consistent demand across multiple price points and technology tiers.

- India tractor production totaled 1,151,273 units in calendar 2025, with total sales including exports reaching 1,195,287 units. This volume confirms India’s position as one of the world’s largest tractor markets, reflecting both domestic demand growth and strong export momentum toward emerging agricultural economies.

- The United States total farm tractor retail sales were 195,857 units in 2025, a decline of 9.9% from 217,279 units in 2024. This contraction highlights cyclical softening in mature markets, though analysts expect demand recovery as farm income stabilizes and replacement cycles resume in the near to medium term.

Precision agriculture technologies are reshaping how farm implements perform in the field. Manufacturers now integrate sensors, telematics, and machine learning systems into tractors and harvesters. Moreover, automated guidance systems reduce operator fatigue and input waste, making precision equipment increasingly attractive to farm operators seeking to lower their cost per hectare while raising yield consistency.

Key Takeaways

- The Global Farm Implements Market is projected to reach USD 80.2 billion by 2035, from USD 41.8 billion in 2025 at a CAGR of 6.7% during the forecast period 2026–2035.

- Tractors dominate with a 34.8% market share in 2025.

- Powered Implements holds the leading share at 67.2%.

- The 31–70 HP segment commands a 41.4% share in 2025.

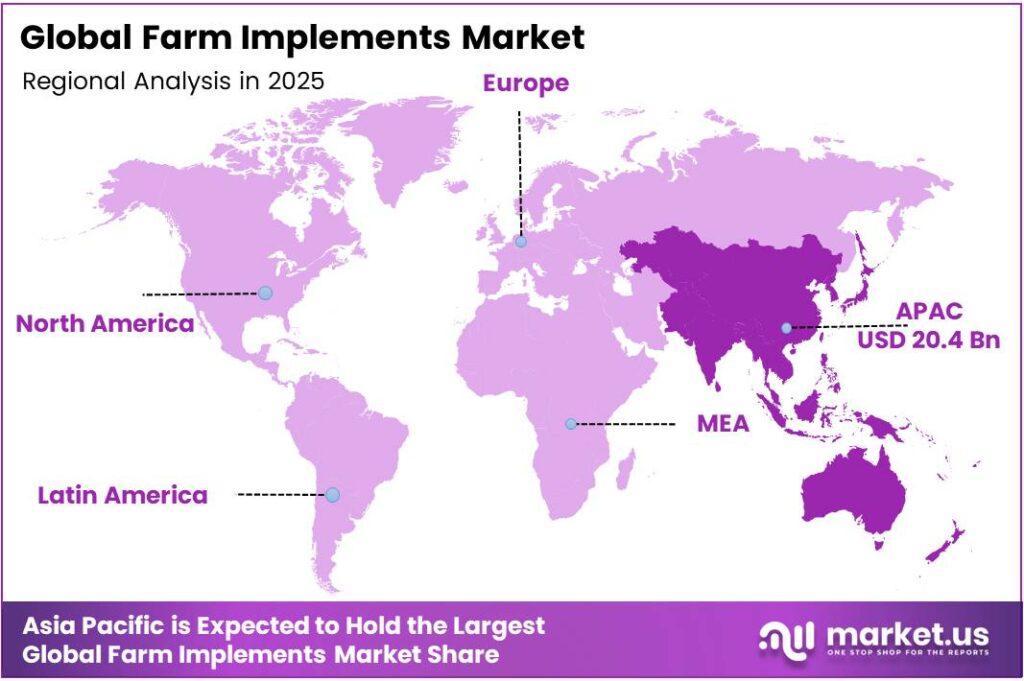

- Asia Pacific Dominates the Farm Implements Market with a Market Share of 48.8%, Valued at USD 20.4 Billion.

Product Type Analysis

Tractors dominate with 34.8% due to widespread use across all farm sizes and operations.

In 2025, Tractors held a dominant market position in the by-product type segment of the Farm Implements Market, with a 34.8% share. Tractors serve as the foundational power unit for most agricultural activities. Moreover, their compatibility with multiple attachments makes them indispensable across crop types, farm sizes, and geographic conditions worldwide.

Harvesters represent the second significant product category, widely used in grain, sugarcane, and vegetable cultivation. These machines drastically cut labor requirements during peak harvest seasons. Consequently, commercial farms in high-wage economies prioritize harvester adoption to reduce time-sensitive crop losses and maintain operational efficiency during narrow harvest windows.

Soil Preparation and Cultivation Equipment covers plows, tillers, and disc harrows used to ready land before planting. Farmers select this equipment based on soil type, crop rotation plans, and available tractor power. Additionally, growing interest in minimal tillage practices is shifting demand toward lighter, more fuel-efficient soil cultivation tools suitable for conservation agriculture systems.

Mode of Operation Analysis

Powered Implements dominate with 67.2% due to efficiency demands across commercial farming operations.

In 2025, Powered Implements held a dominant market position in the By Mode of Operation segment of the Farm Implements Market, with a 67.2% share. Engine-driven and PTO-connected equipment delivers the mechanical output required for large-scale operations. Moreover, labor shortages in rural regions accelerate the transition from manual to powered machinery across both developing and mature agricultural economies.

Unpowered Implements retain relevance among smallholder farmers in cost-sensitive markets. Animal-drawn plows and hand-operated tools remain in active use across parts of Sub-Saharan Africa and South Asia. However, government mechanization programs and affordable credit access are progressively reducing reliance on unpowered implements as farmers migrate toward entry-level motorized equipment.

Power Output Analysis

31–70 HP tractors dominate with 41.4% due to versatility across mid-size farm operations globally.

In 2025, the 31–70 HP segment held a dominant market position in the By Power Output segment of the Farm Implements Market, with a 41.4% share. This power range serves the broadest range of farm sizes and crop types. Additionally, tractors in this category balance fuel economy with fieldwork capability, making them the top choice for small to mid-scale producers across Asia, Eastern Europe, and Latin America.

The Below 30 HP category targets smallholder operations, orchards, and nurseries requiring compact, maneuverable machines. These low-horsepower units are popular in densely cultivated regions like Southeast Asia and South India. Moreover, their lower purchase price and operating cost make them accessible to first-time buyers entering the mechanized farming segment for the first time.

The 71–130 HP segment addresses mid-to-large farms engaged in row crop and grain production. Farmers in North America and Europe frequently select this power range for planting and harvesting operations. Consequently, manufacturers focus significant R&D investment on this bracket to integrate telematics, variable rate application, and automated guidance as standard features.

The Above 130 HP category encompasses high-capacity tractors used in large-scale commercial farming and land development. These premium machines support wide-span equipment like air seeders and deep tillage units. Therefore, North American and Australian broadacre farms represent the primary buyers, where field scale justifies the capital investment in maximum-power machinery.

Key Market Segments

By Product Type

- Tractors

- Harvesters

- Soil Preparation and Cultivation Equipment

- Planting, Seeding, and Fertilizing Equipment

- Irrigation and Crop Protection Implements

- Precision and Autonomous Implements

- Haying and Forage Equipment

- Others

By Mode of Operation

- Powered Implements

- Unpowered Implements

By Power Output

- Below 30 HP

- 31–70 HP

- 71–130 HP

- Above 130 HP

Emerging Trends

Multi-Fuel and Connected Technologies Transform Farm Equipment Capabilities

Equipment manufacturers are actively developing multi-fuel engine platforms capable of operating on diesel, ethanol, or electric power. France’s agricultural equipment market fell from €9 billion in 2023 to €8 billion in 2024, a decline of 14%, prompting manufacturers to invest in fuel-flexible designs to sustain buyer interest during market downturns.

- Farm equipment networks increasingly leverage 5G connectivity for real-time coordination between machines, sensors, and farm management systems. Manufacturers and telecom partners are jointly developing 5G-connected farm ecosystems that enable live data exchange across entire fields. CNH Industrial invested 5.9% of FY2024 sales in R&D, reflecting the industry’s commitment to next-generation powertrain development.

Dealer network consolidation is forming large-scale regional retail groups, changing how equipment reaches end buyers. Rising farmer preference for retrofitting autonomy kits on existing machinery also creates a parallel aftermarket growth channel. Moreover, these retrofit solutions allow budget-constrained operators to access precision guidance features without replacing entire fleets, extending equipment lifecycles, and reducing the total cost of ownership.

Drivers

Rising Food Demand and Mechanization Programs Accelerate Market Growth

Global food demand continues to rise as population growth and dietary shifts increase calorie requirements per capita. Farmers face pressure to produce more output per hectare using the same or less land area. Therefore, modern farm implements that boost yield efficiency through precision planting, optimized irrigation, and automated harvesting are becoming essential tools in both commercial and smallholder farming systems.

Precision agriculture technologies are transforming how farmers manage inputs and monitor field performance. Variable rate applicators, yield mapping systems, and automated sprayers allow operators to target resources exactly where needed. Additionally, these technologies reduce fertilizer and pesticide use, lowering production costs while improving environmental compliance, which further drives adoption among sustainability-focused commercial farm operators.

Europe registered 204,500 tractors in 2024, of which 144,400 were agricultural tractors, marking the lowest registration year in a decade. Despite this short-term cyclical decline, government subsidies and farm mechanization programs across developing nations continue to expand the global installed base of powered implements. Consequently, Asia Pacific and Latin America represent the strongest structural growth regions for new farm equipment demand through the forecast period.

Restraints

High Capital Costs and Supply Chain Vulnerabilities Limit Broader Market Penetration

High initial capital investment remains a primary barrier preventing smallholder farmers from upgrading to modern mechanized implements. Many subsistence and semi-commercial farmers in developing markets lack access to formal credit or face prohibitive interest rates on agricultural loans. Consequently, equipment adoption in lower-income rural areas progresses slowly despite clear productivity benefits, limiting addressable market growth for premium product segments.

- Brazil’s agricultural machinery wholesale sales were 48.9 thousand units in 2024, down 19.8% from 61.0 thousand units in 2023. This sharp contraction illustrates how economic volatility, unfavorable exchange rates, and tight credit conditions can rapidly suppress demand even in high-potential emerging markets. CNH Industrial, net sales for its Agriculture segment declined to $14.007 billion in FY2024, down 22.8% from FY2023, reflecting the broad impact of demand normalization across major markets.

Global supply chain fragility for critical electronic components and semiconductors creates ongoing production uncertainty. Modern precision equipment depends heavily on microcontrollers, sensors, and connectivity modules sourced from specialized suppliers. Therefore, any disruption in semiconductor availability, as seen during recent global chip shortages, can delay equipment deliveries, inflate prices, and erode dealer confidence in inventory planning and forward order commitments.

Growth Factors

Technology Innovation and Market Expansion Drive Long-Term Sector Opportunities

Specialized drone fleets for targeted crop monitoring and precision spraying represent one of the most commercially promising growth avenues. Agricultural drones reduce the volume of agrochemicals applied per field by delivering treatments only where sensor data identifies crop stress or pest activity. Escorts Kubota reported revenue from continuing operations of ₹10,187.0 crore in FY2025, up 4.7% from FY2024, demonstrating that companies combining traditional equipment with digital services generate resilient revenue even in softening markets.

- The Farm Equipment Sector recorded 407,094 domestic tractor sales in FY2025, the company’s highest-ever yearly domestic sales figure. This milestone reflects robust rural income growth and improving financing access across India’s agricultural sector. Expanding into emerging markets with tailored compact and utility tractor designs allows manufacturers to capture price-sensitive buyers who need reliable, low-maintenance equipment matched to local field conditions and crop systems.

Blockchain technology integration for transparent agricultural supply chain tracking offers manufacturers and farm operators new tools for quality verification and compliance documentation. Simultaneously, the emergence of Tractor-as-a-Service subscription models is removing upfront capital barriers for smallholder buyers. Consequently, these access-based business models expand the addressable market beyond traditional owner-operator buyers and create predictable recurring revenue streams for equipment providers.

Regional Analysis

Asia Pacific Dominates the Farm Implements Market with a Market Share of 48.8%, Valued at USD 20.4 Billion

Asia Pacific holds the leading position in the farm implements market due to the region’s large agricultural base, increasing mechanization, and supportive government initiatives aimed at improving farm productivity. Countries such as China and India are major contributors to the demand for modern equipment. The region accounts for 48.8% of the global market and is valued at USD 20.4 billion, reflecting strong adoption of efficient farming technologies.

North America represents a mature market characterized by high levels of farm mechanization and advanced agricultural technologies. The demand for precision farming equipment, autonomous machinery, and high-capacity implements continues to grow among large-scale farms. Government support programs and strong investments in agricultural innovation further support the steady expansion of the farm implements market across the region.

Europe’s farm implements market is driven by the region’s emphasis on sustainable agriculture, modern farming equipment, and technological innovation. Farmers increasingly adopt advanced implements to enhance productivity and comply with environmental regulations. Strong agricultural policies, modernization initiatives, and rising demand for efficient farming solutions continue to stimulate market growth across several European countries.

Latin America is experiencing increasing adoption of farm implements due to expanding commercial agriculture and rising demand for higher crop yields. Countries with large agricultural sectors are investing in modern machinery to improve efficiency and reduce labor dependency. Growing exports of agricultural commodities and supportive government initiatives are further contributing to the market’s development.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

- In 2025, Deere & Company finalized its acquisition of Tenna, a construction technology company. Tenna will operate as an independent business, focusing on mixed-fleet solutions for construction customers. Despite a forecasted market decline, John Deere is rehiring 140 employees at its Waterloo, Iowa, operations due to increased demand for its large 8R and 9R tractors.

- In 2025, AGCO announced the addition of Ritchie Implement as a new authorized full-line dealership in southwest Wisconsin, effective. The dealership will support AGCO’s Fendt, Massey Ferguson, and PTx brands and aligns with AGCO’s FarmerCore service strategy.

Top Key Players in the Market

- Deere and Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra and Mahindra Ltd.

- CLAAS KGaA mbH

- SAME Deutz-Fahr

- Yanmar Co., Ltd.

- J.C. Bamford Excavators Ltd.

- Tractors and Farm Equipment Ltd.

- Argo Tractors S.p.A.

- Sonalika International Tractors Ltd.

- Escorts Kubota Ltd.

- Kuhn Group

- Horsch Maschinen GmbH

Recent Developments

- In 2025, Deere & Company finalized its acquisition of Tenna, a construction technology company. Tenna will operate as an independent business, focusing on mixed-fleet solutions for construction customers. Despite a forecasted market decline, John Deere is rehiring 140 employees at its Waterloo, Iowa, operations due to increased demand for its large 8R and 9R tractors.

- In 2025, AGCO announced the addition of Ritchie Implement as a new authorized full-line dealership in southwest Wisconsin, effective. The dealership will support AGCO’s Fendt, Massey Ferguson, and PTx brands and aligns with AGCO’s FarmerCore service strategy.

Report Scope

Report Features Description Market Value (2025) USD 41.8 Billion Forecast Revenue (2035) USD 80.2 Billion CAGR (2026-2035) 6.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Tractors, Harvesters, Soil Preparation and Cultivation Equipment, Planting, Seeding, and Fertilizing Equipment, Irrigation and Crop Protection Implements, Precision and Autonomous Implements, Haying and Forage Equipment, Others), By Mode of Operation (Powered Implements, Unpowered Implements), By Power Output (Below 30 HP, 31–70 HP, 71–130 HP, Above 130 HP) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Deere and Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Mahindra and Mahindra Ltd., CLAAS KGaA mbH, SAME Deutz-Fahr, Yanmar Co. Ltd., J.C. Bamford Excavators Ltd., Tractors and Farm Equipment Ltd., Argo Tractors S.p.A., Sonalika International Tractors Ltd., Escorts Kubota Ltd., Kuhn Group, Horsch Maschinen GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Deere and Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra and Mahindra Ltd.

- CLAAS KGaA mbH

- SAME Deutz-Fahr

- Yanmar Co., Ltd.

- J.C. Bamford Excavators Ltd.

- Tractors and Farm Equipment Ltd.

- Argo Tractors S.p.A.

- Sonalika International Tractors Ltd.

- Escorts Kubota Ltd.

- Kuhn Group

- Horsch Maschinen GmbH

Our Clients

- 181130

- March 2026