Quick Navigation

Report Overview

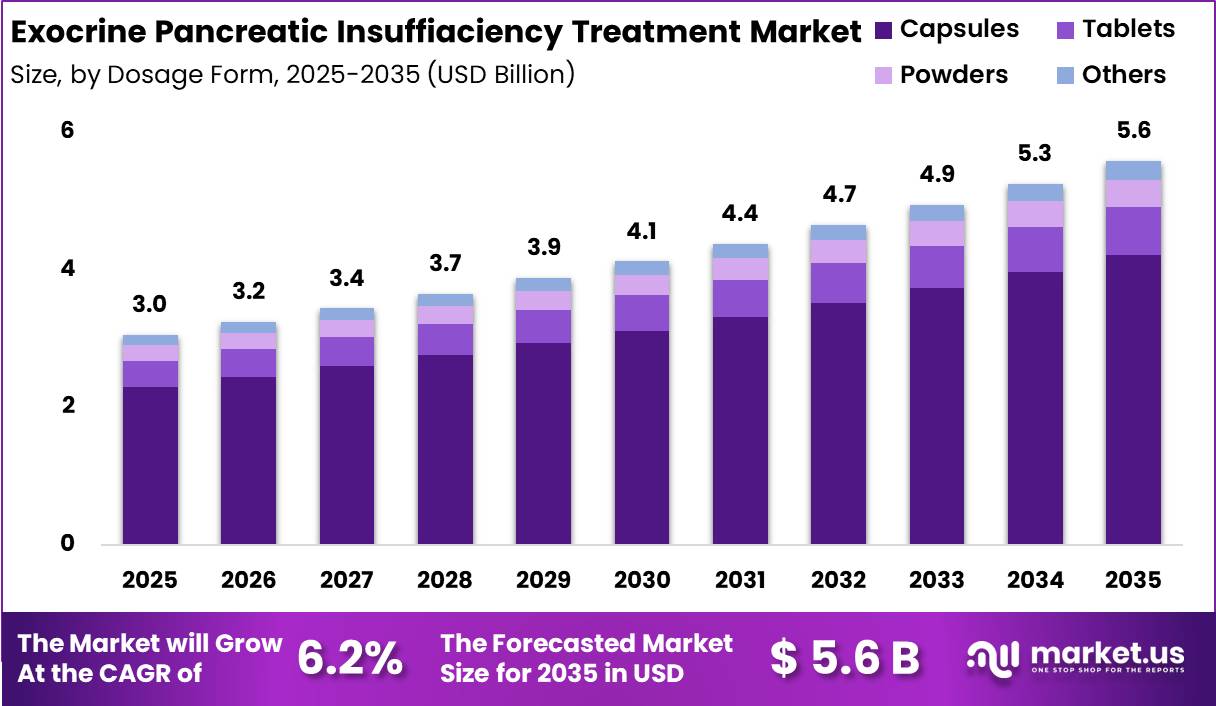

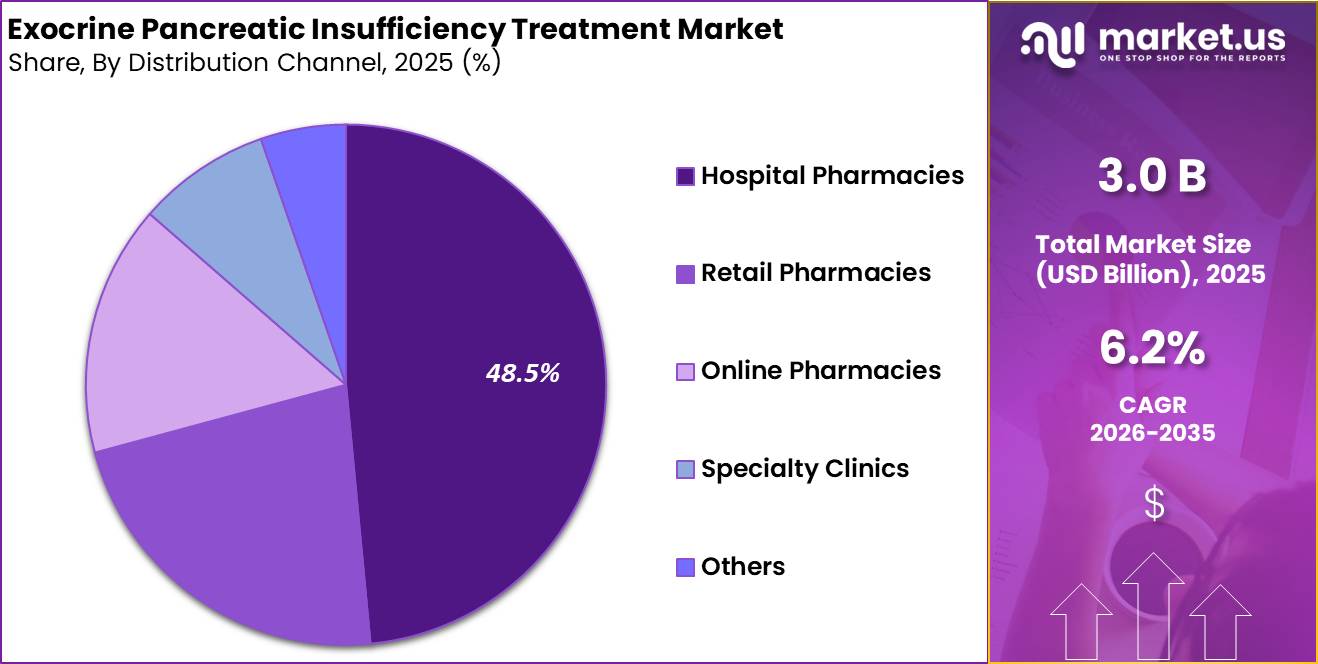

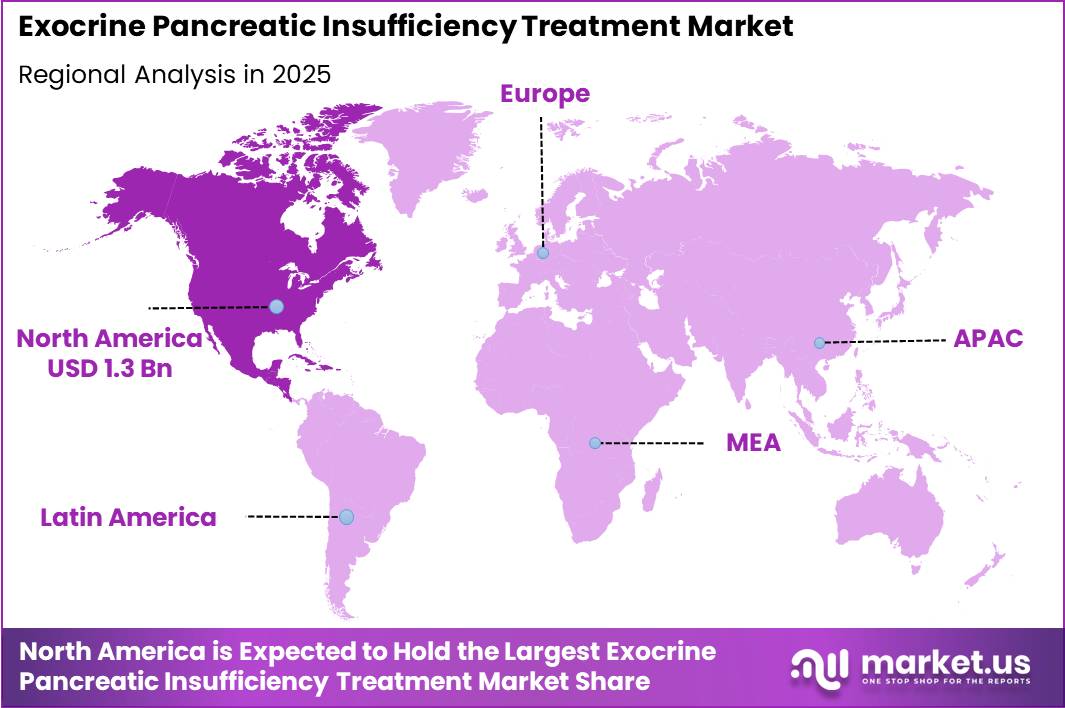

Global Exocrine Pancreatic Insufficiency (EPI) Treatment Market size is expected to be worth around US$ 5.6 Billion by 2035 from US$ 3.0 Billion in 2025, growing at a CAGR of 6.2% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.50% share with a revenue of US$ 1.3 Billion.

The Exocrine Pancreatic Insufficiency (EPI) Treatment Market is witnessing steady growth due to the increasing prevalence of pancreatic disorders, cystic fibrosis, pancreatic cancer, and age-related digestive diseases. EPI is a condition characterized by insufficient production or secretion of pancreatic digestive enzymes, resulting in malabsorption of fats, proteins, and carbohydrates. The condition can lead to weight loss, malnutrition, vitamin deficiencies, and reduced quality of life, thereby creating a significant demand for effective therapeutic interventions.

According to the U.S. National Institutes of Health (NIH), chronic pancreatitis, one of the leading causes of EPI, affects approximately 13.5 to 163 individuals per 100,000 population, with an incidence ranging from 5 to 31.7 new cases per 100,000 person-years. Furthermore, NIH-supported research indicates that nearly 85% of patients with cystic fibrosis develop pancreatic exocrine insufficiency and require pancreatic enzyme replacement therapy (PERT) during their lifetime. These statistics underscore the substantial patient population requiring long-term management and treatment.

Pancreatic Enzyme Replacement Therapy remains the standard of care for EPI and is recommended by major healthcare organizations for improving nutrient absorption and reducing gastrointestinal symptoms. The market is also benefiting from advancements in enzyme formulations, including enteric-coated pancreatic enzyme products that improve enzyme delivery and therapeutic efficacy.

Diagnostic innovations are further supporting market expansion. Fecal elastase-1 testing has become one of the most widely utilized non-invasive diagnostic tools for EPI. Recent clinical studies have demonstrated that fecal elastase-1 testing offers sensitivity rates of approximately 94% and specificity of around 69% at standard diagnostic thresholds, making it a valuable screening method for identifying pancreatic insufficiency in clinical practice.

Additionally, the growing global geriatric population, increasing awareness of digestive health, improved access to diagnostic services, and ongoing research into novel enzyme replacement therapies are expected to drive market growth. Continued development of precision dosing strategies and biomarker-based diagnostics is anticipated to enhance treatment outcomes and create new opportunities within the EPI treatment market over the forecast period.

Key Takeaways

- Market Size: Global Exocrine Pancreatic Insufficiency (EPI) Treatment Market size is expected to be worth around US$ 5.6 Billion by 2035 from US$ 3.0 Billion in 2025.

- Market Share: The market growing at a CAGR of 6.2% during the forecast period from 2026 to 2035.

- Drug Type Analysis: Porcine-derived Pancreatic Enzyme Replacement Therapy (PERT) dominates the market and is projected to account for 68.50% of the total market share in 2025.

- Application Analysis: Chronic Pancreatitis represents the largest application segment, accounting for 38.50% of the market share in 2025.

- Dosage Form Analysis: Capsules dominate the market and are expected to hold 72.50% of the global market share in 2025.

- Distribution Channel Analysis: Hospital Pharmacies account for the largest share, representing 48.50% of the market in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 42.50% share with a revenue of US$ 1.3 Billion.

Drug Type Analysis

The drug type segment of the Exocrine Pancreatic Insufficiency (EPI) Treatment Market is primarily driven by the widespread adoption of pancreatic enzyme replacement therapies (PERTs), which remain the standard of care for managing digestive enzyme deficiencies. Porcine-derived Pancreatic Enzyme Replacement Therapy (PERT) dominates the market and is projected to account for 68.50% of the total market share in 2025.

The segment’s leadership is attributed to its proven clinical efficacy, comprehensive enzyme composition, and strong physician preference for treating EPI associated with chronic pancreatitis, cystic fibrosis, and pancreatic cancer. Regulatory approvals and established reimbursement frameworks further support its market position.

Pancrelipase Capsules represent a significant segment owing to their optimized formulation containing lipase, amylase, and protease enzymes. These products are widely prescribed due to their superior absorption characteristics and convenient dosing. Pancreatin Tablets continue to maintain a stable market presence, particularly in cost-sensitive regions where affordability influences treatment decisions.

The Others category, including plant-based enzymes and fungal-derived enzymes, is witnessing gradual growth due to increasing demand for non-animal-derived therapeutic alternatives among specific patient populations. Ongoing research focused on improving enzyme stability, bioavailability, and patient compliance is expected to support innovation across all drug categories, contributing to sustained market expansion during the forecast period.

Application Analysis

The application segment of the Exocrine Pancreatic Insufficiency (EPI) Treatment Market is categorized into chronic pancreatitis, cystic fibrosis, pancreatic cancer, post-surgical conditions, diabetes mellitus, and other rare disorders. Chronic Pancreatitis represents the largest application segment, accounting for 38.50% of the market share in 2025.

The dominance of this segment is driven by the progressive destruction of pancreatic tissue, resulting in long-term enzyme deficiency and a growing requirement for continuous pancreatic enzyme replacement therapy. Increasing incidence of alcohol-related and idiopathic pancreatitis globally further supports segment growth.

Cystic Fibrosis remains a major application area due to the high prevalence of pancreatic insufficiency among affected patients, making lifelong enzyme supplementation essential. Pancreatic Cancer is another important segment, supported by rising cancer incidence and increased recognition of malabsorption complications during treatment. The Post-Surgical segment, including patients undergoing pancreatectomy and gastrectomy, is expanding steadily as surgical interventions frequently impair digestive enzyme production.

Diabetes Mellitus is gaining clinical attention due to the growing association between pancreatic dysfunction and diabetes-related exocrine insufficiency. The Others category, comprising conditions such as Shwachman-Diamond Syndrome and other rare pancreatic disorders, contributes a smaller but steadily growing share. Improved diagnostic rates and greater awareness of EPI symptoms across disease groups are expected to drive broader treatment adoption.

Dosage Form Analysis

Based on dosage form, the Exocrine Pancreatic Insufficiency (EPI) Treatment Market is segmented into capsules, tablets, powders, and others. Capsules dominate the market and are expected to hold 72.50% of the global market share in 2025. Their leading position is attributed to the widespread availability of enteric-coated formulations that protect enzymes from gastric acid degradation and ensure effective delivery to the small intestine. Capsules also offer convenient administration, accurate dosing, and improved patient adherence, making them the preferred choice among healthcare providers and patients.

Tablets constitute the second-largest segment and continue to be utilized in several regional markets due to their cost-effectiveness and ease of manufacturing. Although tablet formulations may have limitations regarding enzyme protection compared to enteric-coated capsules, ongoing formulation advancements are improving their therapeutic performance. Powders are particularly beneficial for pediatric patients, elderly populations, and individuals experiencing swallowing difficulties. Their flexible dosing capability supports personalized treatment approaches in specialized patient groups.

The Others segment includes sachets, granules, and emerging novel delivery systems designed to enhance enzyme stability and digestive efficacy. Increasing emphasis on patient-centric therapies, combined with technological advancements in enzyme encapsulation and controlled-release formulations, is expected to support growth across all dosage form categories while maintaining capsules as the dominant segment throughout the forecast period.

Distribution Channel Analysis

The distribution channel segment of the Exocrine Pancreatic Insufficiency (EPI) Treatment Market comprises hospital pharmacies, retail pharmacies, online pharmacies, specialty clinics, and other channels. Hospital Pharmacies account for the largest share, representing 48.50% of the market in 2025.

Their dominance is supported by the high proportion of EPI diagnoses occurring within hospital settings, particularly among patients with chronic pancreatitis, pancreatic cancer, cystic fibrosis, and post-surgical complications. Hospital pharmacies also facilitate specialist supervision, prescription management, and access to advanced pancreatic enzyme replacement therapies.

Retail Pharmacies represent a substantial segment due to their extensive geographic reach and accessibility, enabling patients requiring long-term enzyme supplementation to obtain medications conveniently. Online Pharmacies are experiencing rapid growth as digital healthcare adoption increases and patients seek home delivery services, competitive pricing, and improved medication access. Specialty Clinics play an important role in distributing EPI therapies through gastroenterology and pancreatic care centers, where specialized treatment protocols and patient monitoring are provided.

The Others segment includes community health centers, institutional healthcare providers, and alternative distribution networks that support treatment access in underserved regions. Increasing healthcare infrastructure development, expanding reimbursement coverage, and growing awareness of EPI management are expected to strengthen all distribution channels, while hospital pharmacies continue to maintain their leadership position during the forecast period.

Key Market Segments

By Drug Type

- Porcine-derived Pancreatic Enzyme Replacement Therapy (PERT)

- Pancrelipase Capsules

- Pancreatin Tablets

- Others (Plant-based Enzymes, Fungal Enzymes)

By Application

- Chronic Pancreatitis

- Cystic Fibrosis

- Pancreatic Cancer

- Post-Surgical (Pancreatectomy, Gastrectomy)

- Diabetes Mellitus

- Others (Shwachman-Diamond Syndrome, etc.)

By Dosage Form

- Capsules

- Tablets

- Powders

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Clinics

- Others

Driving Factors

Rising Burden of Pancreatic and Gastrointestinal Disorders Driving Demand for EPI Treatment

The increasing prevalence of diseases associated with exocrine pancreatic insufficiency (EPI) is a major driver of the EPI treatment market. EPI develops when the pancreas fails to produce sufficient digestive enzymes, resulting in malabsorption of fats, proteins, and carbohydrates.

According to the U.S. National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), pancreatic enzyme dysfunction occurs in approximately 30%–90% of patients with chronic pancreatitis and 80%–90% of patients with cystic fibrosis, making these conditions the primary contributors to EPI incidence.

The growing prevalence of chronic pancreatitis, pancreatic cancer, diabetes, inflammatory bowel disease, and gastrointestinal surgeries has expanded the population requiring long-term pancreatic enzyme replacement therapy (PERT). NIDDK identifies PERT as the standard treatment for EPI and recommends its use during meals and snacks to improve nutrient absorption and reduce symptoms.

In addition, increasing awareness among healthcare professionals regarding malnutrition-related complications has improved diagnosis rates. Untreated EPI can lead to deficiencies in vitamins A, D, E, and K, osteoporosis, and immune dysfunction, prompting earlier therapeutic intervention. The combination of a growing patient pool, higher diagnosis rates, and the necessity for lifelong enzyme supplementation is supporting sustained demand for EPI treatment products globally.

Trending Factors

Growing Adoption of Personalized Pancreatic Enzyme Replacement Therapy (PERT)

A significant trend in the Exocrine Pancreatic Insufficiency treatment market is the increasing adoption of personalized pancreatic enzyme replacement therapy (PERT) regimens. Healthcare providers are moving away from uniform dosing approaches and increasingly tailoring treatment based on disease severity, dietary fat intake, body weight, nutritional status, and patient response. The NIDDK identifies PERT as the cornerstone of EPI management and emphasizes proper timing with meals and snacks to maximize digestive efficiency.

Clinical practice is also placing greater emphasis on monitoring nutritional deficiencies and treatment outcomes. According to the National Center for Biotechnology Information (NCBI), patients diagnosed with EPI should undergo regular assessments for body weight, body mass index, and fat-soluble vitamin levels to evaluate treatment effectiveness. Annual monitoring is recommended to optimize therapy and reduce malnutrition-related complications.

Another emerging trend is the integration of nutritional counseling alongside enzyme therapy. NIDDK recommends individualized dietary management, including small frequent meals and specialized nutrition plans, to improve patient outcomes.

Advancements in enteric-coated enzyme formulations and growing physician awareness regarding appropriate dose adjustments are further improving treatment adherence and clinical outcomes. These developments are contributing to a more patient-centric treatment landscape and supporting the long-term growth of the EPI treatment market.

Restraining Factors

Underdiagnosis and Delayed Identification of Exocrine Pancreatic Insufficiency

One of the key restraints affecting the Exocrine Pancreatic Insufficiency treatment market is the persistent underdiagnosis and delayed diagnosis of the disease. EPI symptoms, including bloating, abdominal discomfort, diarrhea, weight loss, and nutritional deficiencies, often overlap with those of other gastrointestinal disorders such as irritable bowel syndrome, celiac disease, and inflammatory bowel disease. This clinical similarity frequently leads to delayed recognition and treatment initiation.

According to NIDDK, EPI is considered a relatively rare condition in the general population, although pancreatic enzyme dysfunction is common among patients with chronic pancreatitis and cystic fibrosis. Because symptoms often develop gradually over several years, many patients remain undiagnosed until significant malabsorption and nutritional deficiencies occur.

Diagnosis generally requires specialized testing such as fecal elastase measurement, pancreatic function tests, blood assessments, and imaging studies. These diagnostic procedures may not be routinely performed in primary care settings, particularly in developing healthcare systems, limiting early detection rates.

Furthermore, insufficient awareness among patients regarding EPI symptoms contributes to delayed medical consultation. The resulting diagnostic gap reduces the number of patients receiving timely pancreatic enzyme replacement therapy. Consequently, underdiagnosis remains a major challenge that restricts treatment uptake and limits the full growth potential of the EPI treatment market despite the availability of effective therapies.

Opportunity

Expanding Clinical Research and Improved Screening Among High-Risk Populations

A major opportunity within the Exocrine Pancreatic Insufficiency treatment market lies in expanding screening initiatives and clinical research focused on high-risk patient populations. Government-supported institutions such as NIDDK are actively supporting studies aimed at improving the diagnosis and treatment of EPI and the underlying diseases responsible for pancreatic dysfunction.

Large patient groups remain insufficiently screened despite having elevated EPI risk. NIDDK reports that pancreatic enzyme dysfunction affects 30%–90% of chronic pancreatitis patients and 80%–90% of cystic fibrosis patients, while EPI can also occur in individuals with diabetes, pancreatic cancer, celiac disease, and inflammatory bowel disease. Expanding routine screening among these populations could significantly increase diagnosis rates and treatment adoption.

Research published through NCBI indicates that 60%–90% of chronic pancreatitis patients develop EPI within 10–12 years of diagnosis, highlighting a substantial population that could benefit from earlier intervention and continuous monitoring.

Additional opportunities exist in the development of advanced enzyme formulations, improved diagnostic biomarkers, and digital patient-monitoring programs. Increasing healthcare investments in rare digestive diseases and growing recognition of malnutrition-related complications are expected to support wider treatment access. As awareness improves and screening expands among high-risk populations, a larger proportion of undiagnosed patients may enter the treatment pathway, creating significant growth opportunities for EPI therapeutics.

Regional Analysis

North America dominated the Exocrine Pancreatic Insufficiency (EPI) Treatment Market in 2025, accounting for over 42.50% of the global market share and generating revenue of approximately US$ 1.3 billion. The region’s leadership can be attributed to the high prevalence of pancreatic disorders, cystic fibrosis, chronic pancreatitis, and pancreatic cancer, all of which are major causes of EPI. The presence of advanced healthcare infrastructure, widespread access to diagnostic services, and strong awareness among healthcare professionals has further supported market growth.

The United States represents the largest contributor within the region, driven by favorable reimbursement policies, increased adoption of pancreatic enzyme replacement therapy (PERT), and continuous advancements in treatment options. Additionally, ongoing clinical research activities and the presence of leading pharmaceutical manufacturers have strengthened the availability of innovative therapies across the region.

Canada also contributes significantly to market expansion, supported by rising healthcare expenditure and growing awareness regarding gastrointestinal and pancreatic health. Early diagnosis initiatives and improved patient access to specialty care have enhanced treatment uptake throughout the country.

Furthermore, the increasing aging population in North America, which is more susceptible to pancreatic insufficiency and related digestive disorders, continues to drive demand for effective treatment solutions. The region is expected to maintain its dominant position during the forecast period, supported by continuous healthcare advancements, robust regulatory frameworks, and ongoing investments in pancreatic disease management and therapeutic development.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Exocrine Pancreatic Insufficiency (EPI) Treatment Market is characterized by the presence of several established pharmaceutical companies focusing on pancreatic enzyme replacement therapies (PERTs), product innovation, and geographic expansion.

Key market participants are actively investing in research and development to improve treatment efficacy, patient compliance, and therapeutic outcomes. Strategic initiatives such as product approvals, partnerships, acquisitions, and distribution agreements are commonly adopted to strengthen market positions.

Leading companies maintain a competitive advantage through strong product portfolios, extensive distribution networks, and established relationships with healthcare providers. The market is primarily driven by the growing adoption of enzyme replacement therapies for managing EPI associated with chronic pancreatitis, cystic fibrosis, pancreatic cancer, and other gastrointestinal disorders.

Additionally, companies are emphasizing awareness programs and educational initiatives to improve diagnosis rates and treatment accessibility. Expansion into emerging markets, where healthcare infrastructure is rapidly improving, presents significant growth opportunities. As demand for effective digestive health treatments continues to rise, key players are expected to focus on innovation, regulatory approvals, and market penetration strategies to sustain long-term growth and competitiveness.

Market Key Players

- Abbott Laboratories

- AbbVie

- Digestive Care

- Essential Pharma

- Eisai

- Nestlé

- Nordmark Pharma

- Sun Pharmaceutical Industries

- Viatris

- VIVUS

- Zentiva Pharma

- Others

Recent Developments

- July, 2025 – AbbVie reported second-quarter 2025 earnings with worldwide net revenue of about 15.4 billion USD, and signalled continued investment in manufacturing modernization and patient services that help sustain Creon’s uptake in EPI, even as the wider pancreatic enzymes market becomes more competitive.

- September, 2025 – Viatris remained listed among the “major competitors” in the global EPI therapeutics market, primarily via its legacy Mylan portfolio in pancreatic enzyme products; during 2025, the company was more active in broad R&D collaborations (for example, an earlier Idorsia R&D deal) than in any visible, EPI-specific acquisition or product launch.

- September, 2025 – Digestive Care continued to position Pertzye as a differentiated PERT option, leveraging its bicarbonate-buffered enteric-coated microsphere technology to compete against larger brands like Creon and Zenpep; the company’s 2025 promotional focus centred on educational outreach to gastroenterologists and cystic fibrosis centres rather than headline M&A.

- September, 2025 – Nestlé Health Science was cited as a leading PERT player with Zenpep, which it had previously acquired from Allergan; during 2025, Zenpep continued to underpin Nestlé’s specialized medical nutrition and gastrointestinal franchise, and the company focused on portfolio integration and medical-nutrition synergies rather than announcing new Zenpep-specific deals.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 3.0 Billion |

| Forecast Revenue (2035) | US$ 5.6 Billion |

| CAGR (2026-2035) | 6.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (Porcine-derived Pancreatic Enzyme Replacement Therapy (PERT), Pancrelipase Capsules, Pancreatin Tablets, Others (Plant-based Enzymes, Fungal Enzymes)) By Application (Chronic Pancreatitis, Cystic Fibrosis, Pancreatic Cancer, Post-Surgical (Pancreatectomy, Gastrectomy), Diabetes Mellitus, Others (Shwachman-Diamond Syndrome, etc.), By Dosage Form ( Capsules, Tablets, Powders, Others) By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Clinics, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Abbott Laboratories, AbbVie, Digestive Care, Essential Pharma, Eisai, Nestlé, Nordmark Pharma, Sun Pharmaceutical Industries, Viatris, VIVUS, Zentiva Pharma, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |