ESIM Orchestration For IoT Market By Component (Platform, Services), By Application (Automotive, Consumer Electronics, Healthcare, Industrial, Energy & Utilities, Transportation & Logistics, Others), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By End-User (Telecommunications, Manufacturing, Healthcare, Automotive, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2026-2035

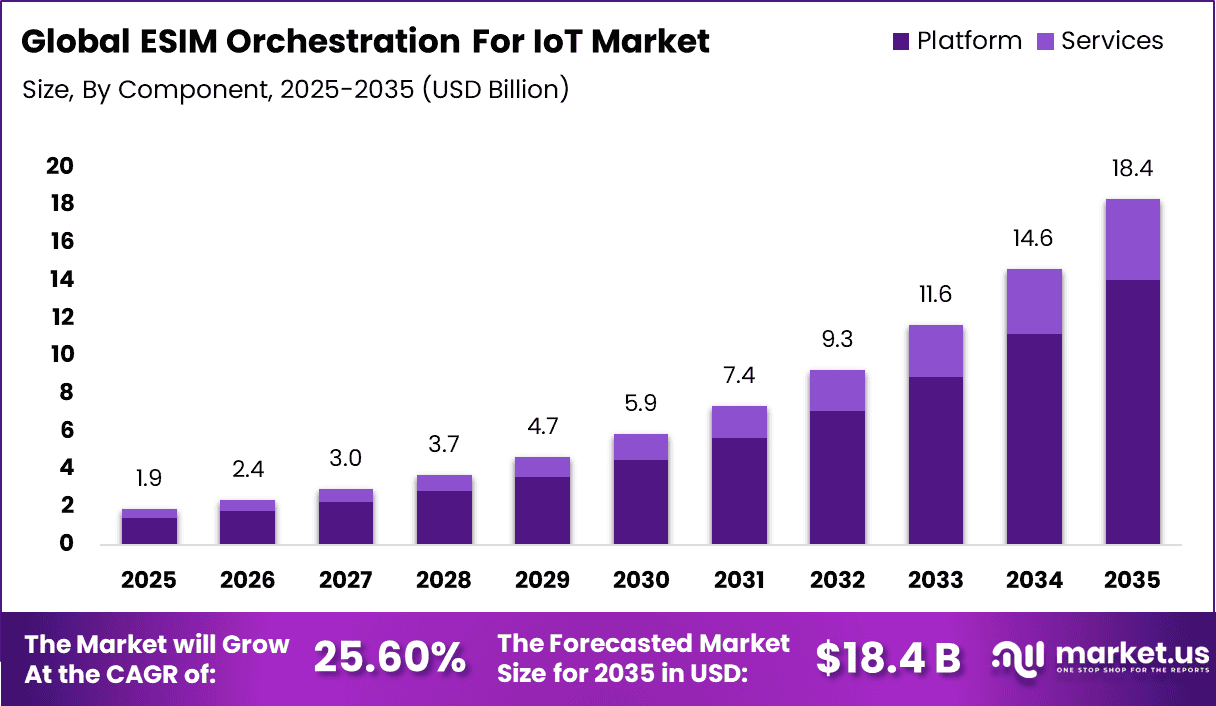

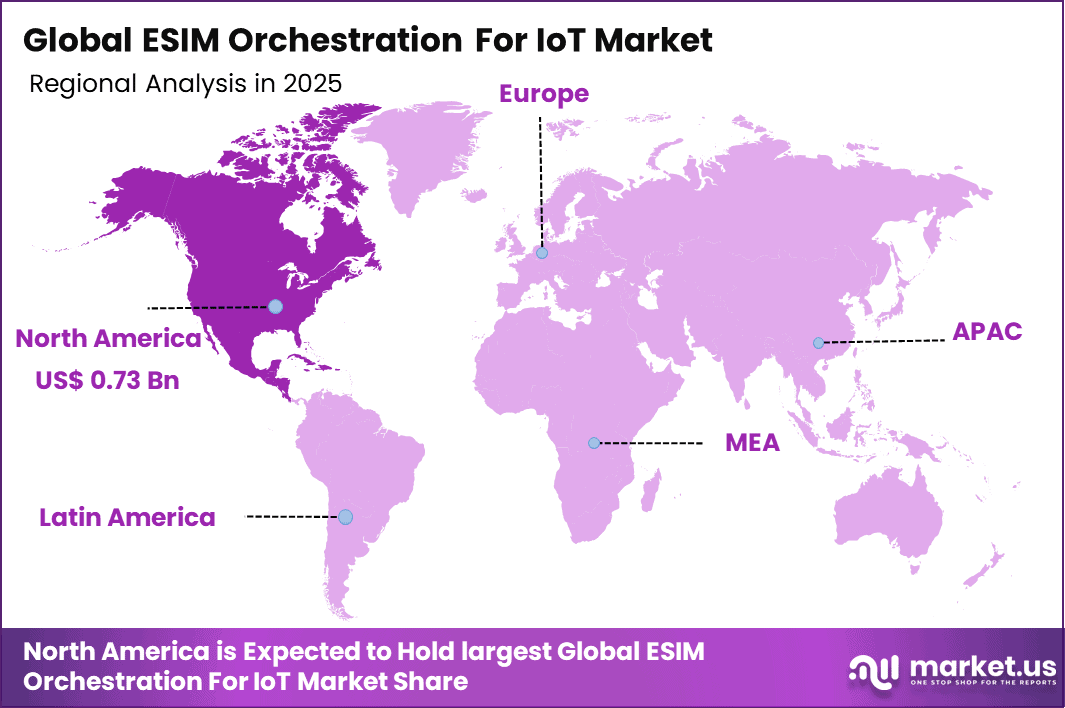

The Global ESIM Orchestration For IoT Market generated USD 1.9 billion in 2025 and is predicted to register growth from USD 2.4 billion in 2026 to about USD 18.4 billion by 2035, recording a CAGR of 25.60% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 39.2% share, holding USD 0.73 Billion revenue.

Top Market Takeaways

Platforms command 76.5% market share, delivering remote SIM provisioning, profile lifecycle automation, and multi-network switching for massive IoT fleets.

Automotive applications capture 38.6%, enabling over-the-air carrier switching, regional roaming optimization, and seamless V2X connectivity across vehicle lifecycles.

On-premises deployment dominates at 74.6%, ensuring data sovereignty, low-latency orchestration, and integration with automotive homologation systems.

Large enterprises hold 73.6%, leveraging scalable platforms for fleet-wide eSIM management, compliance reporting, and predictive connectivity analytics.

Telecommunications end-users represent 37.6%, powering IoT-as-a-Service models, global connectivity marketplaces, and embedded SIM monetization strategies.

North America drives 39.2% global value, with U.S. market at USD 0.62 billion and 23.5% CAGR, fueled by GM/Ford eSIM mandates and 5G automotive ecosystems.

ESIM orchestration for IoT refers to the software and control layer that manages embedded SIM connectivity across connected devices throughout their working life. It allows enterprises to activate, assign, update, and switch network profiles remotely without needing physical access to the device. This has become increasingly important as IoT deployments expand across vehicles, industrial equipment, utilities, healthcare devices, and smart infrastructure.

In many of these settings, devices remain in the field for years, so businesses need a reliable way to manage connectivity from a central platform. As a result, the market is developing as an important part of the wider connected device ecosystem because it improves flexibility, reduces manual effort, and supports long term device management.

The top driving factors are closely linked to scale, efficiency, and operational control. Enterprises are adopting ESIM orchestration because it helps simplify global device deployment and reduces the difficulty of handling multiple mobile network relationships across regions. It also supports faster onboarding of devices, easier profile changes, and better continuity when network conditions, service terms, or regional requirements change.

Another major factor is the growing need for secure and compliant connectivity management, especially in sectors where uptime and remote monitoring are critical. As IoT fleets become larger and more complex, organizations are placing greater value on platforms that can automate connectivity tasks and reduce the need for physical intervention.

Demand for ESIM orchestration for IoT is rising strongest in industries that depend on distributed assets and always connected operations. Automotive, logistics, industrial automation, energy, and asset tracking are creating steady demand because devices in these sectors are often mobile, geographically dispersed, and difficult to service manually.

Buyers are not only looking for connectivity activation, but also for lifecycle visibility, network flexibility, and stronger control over device behavior after deployment. This is why demand is moving beyond basic SIM management and toward more advanced orchestration capabilities that support large scale rollout, lower operating burden, and smoother connectivity performance across different markets.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Implementation Significance

Rapid growth in IoT device deployments across industries

+4.5%

Global

Short to Mid Term

Increases demand for scalable SIM lifecycle management

Rising adoption of remote SIM provisioning (RSP)

+3.9%

North America, Europe

Short Term

Enables seamless connectivity without physical SIM handling

Expansion of connected vehicles and smart mobility

+3.6%

North America, Asia Pacific

Mid Term

Drives need for dynamic network switching

Growing demand for global connectivity solutions

+3.2%

Global

Mid to Long Term

Supports cross-border IoT deployments

Increasing enterprise focus on device lifecycle automation

+2.8%

Europe, Asia Pacific

Mid Term

Improves operational efficiency and reduces manual effort

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

High initial integration and infrastructure complexity

-3.6%

Global

Short Term

Interoperability challenges across telecom ecosystems

-3.2%

Europe, Asia Pacific

Mid Term

Regulatory and compliance variations across regions

-2.9%

Global

Mid to Long Term

Data security and privacy concerns in IoT networks

-2.7%

North America, Europe

Short to Mid Term

Limited awareness among small and mid enterprises

-2.4%

Emerging Markets

Short Term

By Component Analysis

Platform accounted for 76.5% of the ESIM Orchestration for IoT Market. This segment leads because orchestration platforms manage the lifecycle of embedded SIM profiles, including provisioning, activation, and connectivity management. These systems enable centralized control over large volumes of IoT devices across different networks.

The segment is also supported by the need for scalable device management. Organizations prefer platform based solutions that can automate connectivity processes and support seamless switching between network operators, which strengthens adoption across IoT ecosystems.

By Application Analysis

Automotive represented 38.6% of the market. This segment dominates because connected vehicles rely on continuous and reliable connectivity for navigation, telematics, and real time data exchange. ESIM orchestration enables efficient management of connectivity across different regions.

The segment is driven by the growth of connected car technologies. Automotive companies adopt these solutions to ensure uninterrupted communication and improve service delivery across global vehicle deployments.

By Deployment Mode Analysis

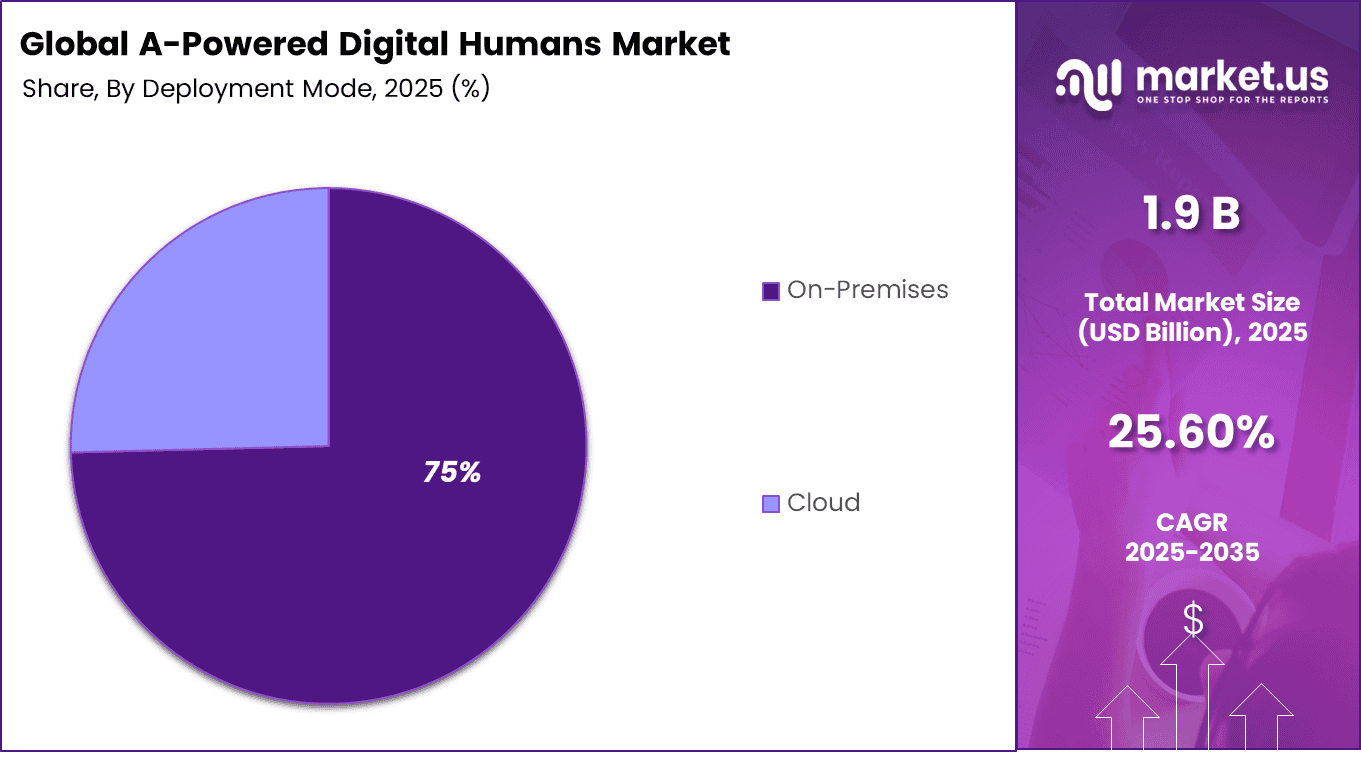

On premises deployment held 75% of the market. This segment leads because organizations prefer to manage ESIM orchestration systems within their own infrastructure to maintain control over connectivity data and device management processes. It allows secure handling of sensitive operational information.

The segment is also supported by the need for reliability and compliance. On premises solutions ensure consistent performance and reduce dependency on external systems, which is important for managing large scale IoT deployments.

By Enterprise Size Analysis

Large enterprises accounted for 73.6% of the market. This segment dominates because large organizations deploy extensive IoT networks and require advanced orchestration systems to manage connectivity efficiently. They need scalable solutions to handle large numbers of devices.

The segment is supported by higher investment capacity and complex operational requirements. Large enterprises adopt ESIM orchestration platforms to improve efficiency, maintain connectivity control, and support global IoT operations.

By End User Analysis

Telecommunications represented 37.6% of the market. This segment leads because telecom operators provide connectivity services and manage network access for IoT devices. ESIM orchestration helps them control subscriptions, manage profiles, and optimize network usage.

The segment is driven by increasing demand for IoT connectivity services. Telecom companies invest in orchestration platforms to enhance service delivery, improve network efficiency, and support growing IoT deployments.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture Capital Firms

High

High

North America, Europe

Strong interest in early-stage orchestration platforms

Private Equity Firms

Medium to High

Medium

Global

Focus on scaling mature IoT connectivity providers

Strategic Telecom Players

High

Medium

Global

Investing in ecosystem control and platform integration

Corporate Investors

Medium

Low to Medium

Asia Pacific, Europe

Targeting operational efficiency and automation gains

Government & Public Funds

Medium

Low

Asia Pacific, Europe

Supporting digital infrastructure and IoT expansion

Technology Enablement Analysis

Technology Factor

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

5G-enabled IoT ecosystem

+6.5%

Global, strong in NA & Asia

Short to Medium Term

Cloud-native orchestration platforms

+5.4%

Global

Medium Term

AI-driven connectivity management

+4.1%

North America, Europe

Medium to Long Term

Edge computing integration

+3.8%

Europe, Asia

Medium Term

GSMA-compliant eSIM standards evolution

+3.6%

Global

Long Term

Key Challenges

Managing large numbers of eSIM profiles across different IoT devices, regions, and network operators is a major challenge because deployments often span many countries and use cases.

Integration with different device types, connectivity platforms, and telecom systems can be difficult because IoT environments often include mixed hardware and software setups.

Remote provisioning and profile switching can be complex because devices must stay connected, secure, and properly configured during network changes.

Security remains a serious concern because eSIM orchestration platforms handle sensitive subscriber, device, and connectivity data that must be protected from unauthorized access.

Regulatory and operator related requirements create another challenge because eSIM usage rules, network agreements, and compliance needs can differ from one country to another.

Emerging Trends

A key trend in the eSIM Orchestration for IoT market is the increasing use of centralized platforms that manage connectivity across large fleets of devices from a single interface. These systems allow organizations to remotely provision, update, and switch network profiles without physical intervention.

As deployments scale across regions, orchestration tools help maintain consistent connectivity and simplify operations. This trend reflects a shift toward more flexible and software driven connectivity management where device control becomes more dynamic and location independent.

Growth Factors

The rapid expansion of IoT deployments is supporting the growth of eSIM orchestration solutions. Organizations operate connected devices across different geographies and network environments, which creates challenges in managing connectivity efficiently.

Orchestration platforms help streamline device management by enabling remote control over network configurations and reducing operational complexity. At the same time, the need for reliable and scalable connectivity encourages adoption of solutions that can support seamless communication across diverse and distributed IoT ecosystems.

Key Market Segments

By Component

Platform

Services

By Application

Automotive

Consumer Electronics

Healthcare

Industrial

Energy & Utilities

Transportation & Logistics

Others

By Deployment Mode

On-Premises

Cloud

By Enterprise Size

Small and Medium Enterprises

Large Enterprises

By End-User

Telecommunications

Manufacturing

Healthcare

Automotive

Others

Regional Analysis

North America accounted for 39.2% of the ESIM Orchestration for IoT Market, reflecting strong adoption of remote connectivity management solutions across enterprises and telecom operators. Organizations across the region increasingly deploy eSIM orchestration platforms to manage device connectivity, automate provisioning, and enable seamless switching between network providers.

The rapid growth of IoT deployments across sectors such as automotive, logistics, and smart infrastructure continues to drive demand for centralized and scalable connectivity management solutions across North America.

The U.S. generated about USD 0.62 Billion within the regional market and is projected to expand at a CAGR of 23.5%. Enterprises and service providers across the country continue to invest in platforms that simplify IoT device lifecycle management and ensure consistent network performance.

eSIM orchestration solutions help reduce operational complexity, support remote device activation, and enhance flexibility in managing large scale IoT networks. As connected ecosystems expand and require efficient connectivity control, demand for eSIM orchestration solutions continues to grow rapidly across the US market.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the eSIM Orchestration for IoT market includes digital connectivity providers, telecom technology firms, and SIM management specialists. Thales, Giesecke+Devrient (G+D), Truphone, ARM (Kigen), Idemia, Tata Communications, BICS, Vodafone, Ericsson, Aeris Communications, Sierra Wireless, Telit, and Amdocs hold strong positions because they offer eSIM provisioning, remote SIM lifecycle management, and secure connectivity tools for large scale IoT deployments. These companies compete by helping enterprises manage connected devices across multiple networks and regions more efficiently.

Other players such as 1oT, Workz Group, Mobileum, Eseye, Simfony, Cubic Telecom, and Soracom add competition through flexible orchestration platforms, IoT connectivity management, and multi operator support. The market is shaped by platform security, ease of integration, global coverage, and the ability to simplify device onboarding and network switching. Overall, companies compete by improving scalability, automation, and reliability for enterprise IoT connectivity management.

The future outlook for the ESIM Orchestration for IoT Market looks strong as more businesses deploy connected devices and need simple remote control of network profiles across large fleets. GSMA’s IoT eSIM standards are built for constrained devices and large scale remote provisioning, while current industry platforms already focus on orchestration, fleet management, and API based profile control for global deployments. As IoT networks expand across industries, demand for eSIM orchestration solutions is expected to grow steadily in the coming years.

Recent Developments

February, 2026 – Thales CipherTrust adds SGP.32 eSIM factory for 5G auto fleets and scales 10M profiles daily. Partners BMW for V2X trust and FIPS 140-3 HSM secures profiles. Adds quantum-safe profiles for defense IoT.

January, 2026 – Truphone Global IoT Platform adds eIM orchestration dashboard and 190 countries covered. Auto-switches best network and fleet management pioneer. Real-time cost optimization included.

Report Scope

Report Features

Description

Market Value (2025)

USD 1.9 Billion

Forecast Revenue (2035)

USD 18.4 Billion

CAGR(2025-2035)

25.60%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2026-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Platform, Services), By Application (Automotive, Consumer Electronics, Healthcare, Industrial, Energy & Utilities, Transportation & Logistics, Others), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By End-User (Telecommunications, Manufacturing, Healthcare, Automotive, Others)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA