Quick Navigation

Report Overview

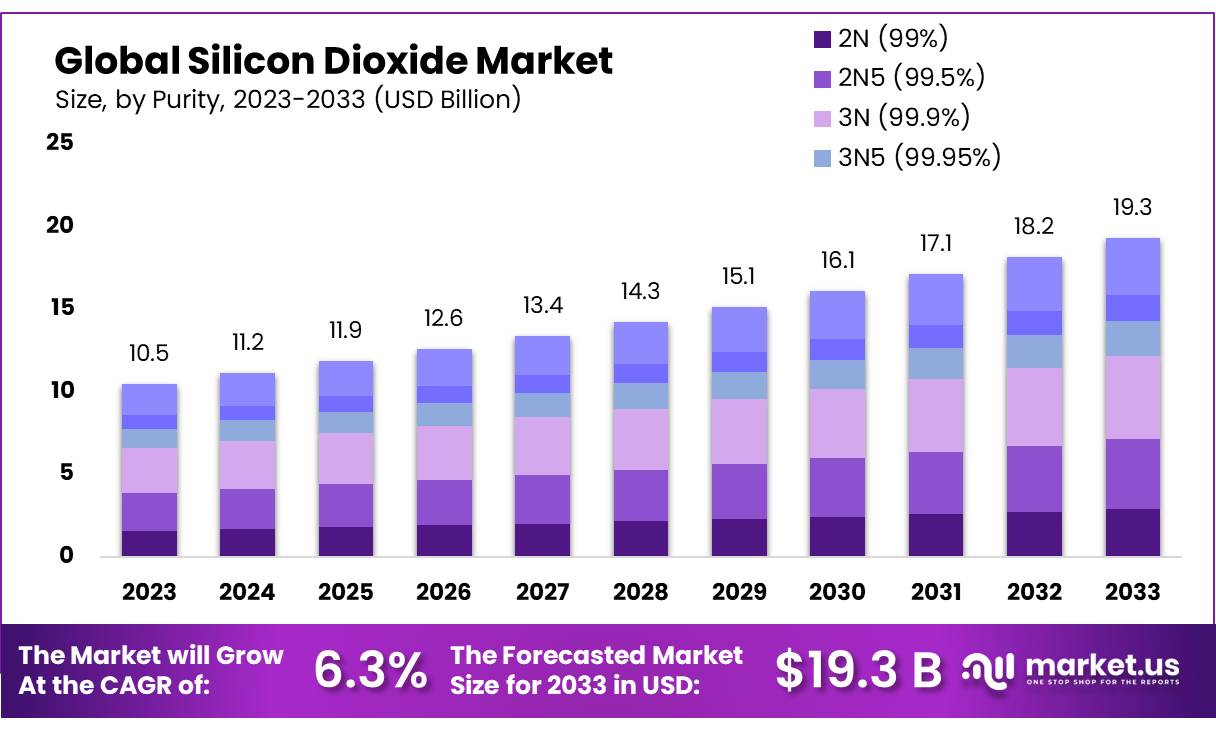

The Global Silicon Dioxide Market size is expected to be worth around USD 19.3 Bn by 2033, from USD 10.5 Bn in 2023, growing at a CAGR of 6.3% during the forecast period from 2024 to 2033.

Silicon dioxide, also known as silica, is a naturally occurring compound composed of silicon and oxygen, existing in various forms such as crystalline quartz and amorphous fused silica. Its versatility makes it an integral material across numerous industries, including construction, glass manufacturing, electronics, and pharmaceuticals. The wide-ranging applications of silica have solidified its role as a vital industrial resource.

The silicon dioxide market is expanding due to several driving factors. In the healthcare sector, silica nanoparticles are increasingly adopted for drug delivery and biosensors, highlighting their growing importance. In the food and beverage industry, silicon dioxide is used as an anti-caking agent in powdered products, driven by rising consumer demand for processed and convenience foods. Additionally, the push for renewable energy solutions has accelerated the use of silica in photovoltaic cells and battery technologies.

The construction industry remains a significant consumer of silicon dioxide, with the building and construction segment projected to account for more than 39.9% of the market share by 2037. Urbanization and the rise in residential and commercial construction activities have heightened the demand for silica, particularly as a key ingredient in cement and glass manufacturing. For instance, in November 2023, SRMPR Cements in India launched its Portland pozzolana cement (PPC) with an investment of USD 27 million in production facilities, further driving silica demand in the region.

Geographically, China has emerged as a dominant player in the Asia-Pacific silicon dioxide market, primarily due to its leadership in electronics and semiconductor production, which require a steady supply of high-purity silica. In October 2024, China’s silicon dioxide exports were estimated at USD 75.2 million, while imports stood at USD 19.3 million, reflecting a positive trade balance. This positions China as a global powerhouse in silica exports, presenting lucrative opportunities for market growth and reinforcing its influence in the global market landscape.

Key Takeaways

- Silicon Dioxide Market size is expected to be worth around USD 19.3 Bn by 2033, from USD 10.5 Bn in 2023, growing at a CAGR of 6.3%.

- 3N (99.9%) purity segment of silicon dioxide held a dominant market position, capturing more than a 25.6% share.

- Amorphous silicon dioxide held a dominant position in the market, capturing more than a 38.6% share.

- Building Materials segment of the silicon dioxide market held a dominant position, capturing more than a 29.3% share.

- Building & Construction segment of the silicon dioxide market held a dominant position, capturing more than a 34.4% share.

- Asia Pacific (APAC) region dominated the silicon dioxide market, accounting for a significant 41.5% market share and generating approximately USD 4.3 billion in revenue.

Business Environment Analysis

The silicon dioxide (SiO₂) market has witnessed consistent growth, driven by its versatile applications across various industries, including construction, electronics, food and beverages, pharmaceuticals, and personal care. Silicon dioxide, commonly found as quartz and sand, serves as a critical raw material due to its excellent thermal stability, hardness, and insulating properties. Global demand is influenced by industrial advancements, urbanization, and increasing emphasis on product innovation.

In the food and beverage industry, silicon dioxide is widely employed as an anti-caking agent and a stabilizer. With global processed food sales reaching USD 4 trillion in 2024, the demand for food-grade silicon dioxide is expected to grow. Regulatory approvals for its use in food and pharmaceuticals also enhance its market penetration. In personal care, silicon dioxide’s application as an abrasive in toothpaste and a thickening agent in cosmetics has expanded its reach, supported by the USD 500 billion global cosmetics market, which grows annually by 5-7%.

Geographically, Asia-Pacific dominates the silicon dioxide market, accounting for nearly 40% of global consumption due to its robust manufacturing base, rapid urbanization, and infrastructure projects in countries like China and India. Europe and North America follow, driven by high demand from advanced electronics and pharmaceutical sectors. For instance, the European pharmaceutical market, valued at over USD 260 billion in 2023, contributes significantly to the region’s silicon dioxide demand.

Despite its broad utility, the silicon dioxide market faces challenges, including environmental concerns associated with sand mining and stringent regulations on silica dust exposure. Research and development in alternative materials and sustainable extraction methods aim to mitigate these issues. Technological advancements, such as synthesizing amorphous silica from rice husk ash, present eco-friendly opportunities.

By Purity

In 2023, the 3N (99.9%) purity segment of silicon dioxide held a dominant market position, capturing more than a 25.6% share. This level of purity is highly sought after in sectors that require high performance and reliability, such as in semiconductors and pharmaceuticals, where even minor impurities can significantly affect product quality.

The 2N (99%) and 2N5 (99.5%) purity levels also play critical roles in various industrial applications. These include glass manufacturing and construction, where slightly lower purity levels are acceptable. These segments benefit from lower production costs while still meeting necessary standards for a wide range of applications.

Higher purities, such as 3N5 (99.95%), 4N (99.99%), and 5N (99.999%), are essential in more specialized fields. For example, the 4N and 5N segments are crucial in the electronics industry for making components where supreme purity ensures optimal electronic performance. These high-purity segments are smaller in market share but command premium prices due to their specialized use and stringent manufacturing requirements.

Lastly, the segment with less than 99% purity, although smaller, finds its use in applications where high purity is less critical. This includes various construction materials and non-specialty glass products, providing a cost-effective solution for manufacturers who do not require ultra-high purity levels.

By Form

In 2023, Amorphous silicon dioxide held a dominant position in the market, capturing more than a 38.6% share. This form of silicon dioxide is favored for its versatility and wide range of applications in industries such as electronics, pharmaceuticals, and food and beverage. Its non-crystalline nature makes it ideal for uses where low bioreactivity and high chemical stability are required.

Quartz silicon dioxide also represents a significant segment of the market. Known for its crystalline form, quartz is primarily used in the making of glass and ceramic products. Its unique optical and thermal properties make it essential in the manufacture of electronics and optical devices.

The Cristobalite form of silicon dioxide, though less common than amorphous or quartz, finds its niche in specialized applications where its high-temperature stability is crucial, such as in foundry molds and refractory materials.

Coesite and Tridymite, while smaller in market share, are utilized in very specific industrial applications. Coesite is used in high-pressure manufacturing processes, whereas Tridymite is often employed in filters and refractory materials due to its thermal stability.

Keatite, a synthetically produced form of silicon dioxide, is used in specific scientific and industrial applications where its unique properties, such as its piezoelectric characteristics, are required. Although it holds a smaller portion of the market, ongoing research and development could expand its applications and market share in the coming years.

By Application

In 2023, the Building Materials segment of the silicon dioxide market held a dominant position, capturing more than a 29.3% share. This segment leverages the durability and strength-enhancing properties of silicon dioxide, making it integral to concrete and cement mixtures used in construction projects.

The Glass & Ceramics sector also utilizes a significant amount of silicon dioxide, especially in the production of glass where its properties help improve hardness and chemical resistance. This application is essential for both household and industrial glass products, ranging from windows to glass used in high-tech applications.

Silicon dioxide is equally vital in the Paints & Coatings industry. It is used to enhance the durability and glossiness of paints and coatings, providing protection against weather and wear. This application benefits from its ability to distribute evenly within coatings, ensuring consistent application and finish.

In Adhesives & Sealants, silicon dioxide is used to improve the adhesion properties and the stability of these products. Its fine particles provide better binding capabilities in various adhesives used in both industrial and retail settings.

The Food & Pharmaceutical sector uses silicon dioxide primarily as an anti-caking agent to ensure product consistency and prevent clumping. Its inert nature makes it safe for consumption and effective in maintaining the desired texture and flow properties of powdered substances.

Silicon Wafers represent a specialized application of silicon dioxide, particularly in the production of semiconductor devices. The purity and properties of silicon dioxide are crucial in creating high-quality wafers that form the base for integrated circuits and microchips.

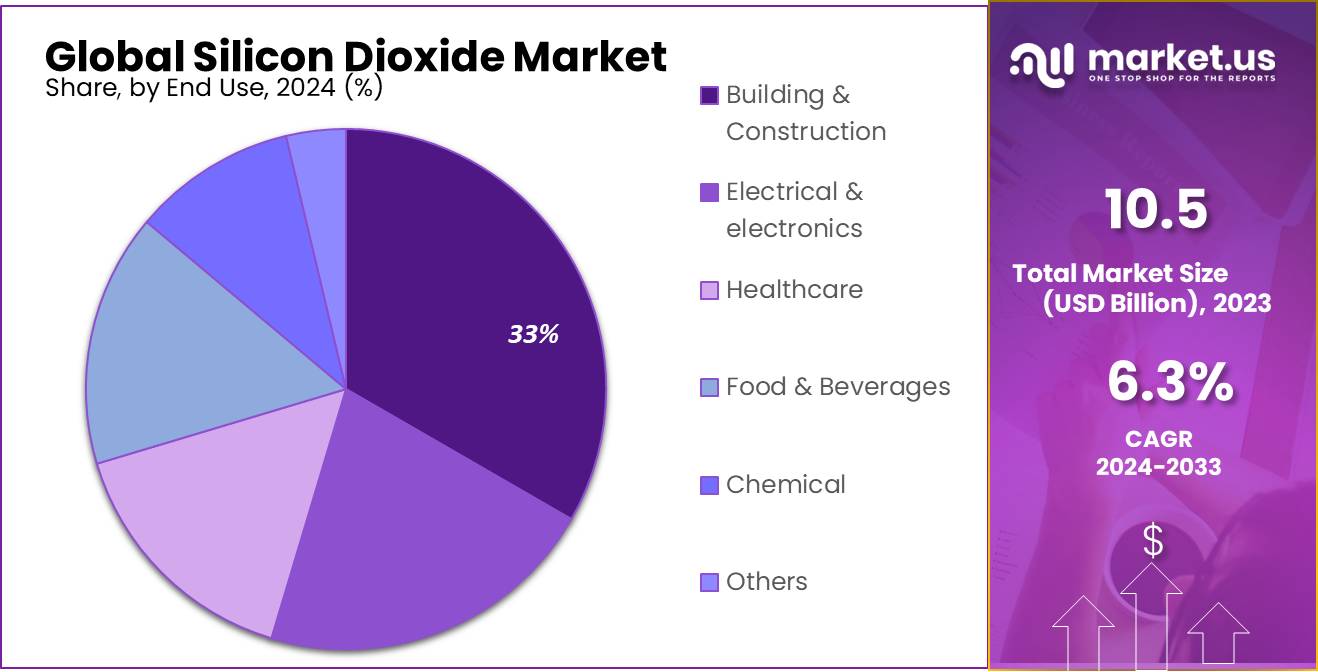

By End Use

In 2023, the Building & Construction segment of the silicon dioxide market held a dominant position, capturing more than a 34.4% share. This segment extensively utilizes silicon dioxide for its strength-enhancing and durability properties, crucial in the production of high-quality concrete and cement, which are foundational to modern construction.

The Electrical & Electronics segment also plays a significant role in the silicon dioxide market. Here, silicon dioxide is used primarily as an insulator and in the fabrication of microchips and semiconductors, due to its excellent dielectric properties. This application is critical for the ongoing advancement and miniaturization of electronic devices.

In the Healthcare sector, silicon dioxide is used for its properties as an excipient and filler in the production of pharmaceuticals. It helps in the controlled release of drugs and enhances the storage stability of medications, making it invaluable in medical formulations.

The Food & Beverages industry employs silicon dioxide as an anti-caking agent to prevent clumping in powders and to enhance the flow of ingredients during processing. This application ensures consistency and quality in food products, particularly in spices, powdered mixes, and supplements.

In the Chemical industry, silicon dioxide is used as a raw material and a catalyst support in various chemical reactions. It is essential for its porous structure, which provides a high surface area for reactions, crucial in the production of a wide range of chemical products.

Key Market Segments

By Purity

- 2N (99%)

- 2N5 (99.5%)

- 3N (99.9%)

- 3N5 (99.95%)

- 4N (99.99%) 5N (99.999%)

- Less than 99% Purity

By Form

- Amorphous

- Quartz

- Keating

- Cristobalite

- Coesite

- Tridymite

By Application

- Building materials

- Glass & Ceramics

- Paints & Coatings

- Adhesive & Sealants

- Food & Pharmaceutical Sealant

- Silicone Wafers

- Others

By End Use

- Building & Construction

- Electrical & electronics

- Healthcare

- Food & Beverages

- Chemical

- Others

Drivers

Increasing Demand in the Food & Beverage Industry

One of the major driving factors for the growth of the silicon dioxide market is its expanding use in the food and beverage industry. Silicon dioxide is widely utilized as an anti-caking agent in food products, which helps to prevent clumping and ensures the free flow of powdered substances. This property is particularly valuable in products such as spices, powdered milk, soup mixes, and coffee creamers.

According to the Food and Drug Administration (FDA), silicon dioxide is generally recognized as safe (GRAS) when used in accordance with good manufacturing or feeding practice. This endorsement allows food producers to use silicon dioxide without additional approvals, facilitating its widespread adoption in the industry. The FDA’s stance on silicon dioxide reflects its importance in maintaining the quality and consistency of a wide array of food products, thereby supporting the market growth.

Furthermore, the global trend towards processed and convenience foods, which require extensive use of additives to maintain quality and longevity, is another significant contributor to the demand for silicon dioxide. As urbanization increases and consumer lifestyles become more hectic, the demand for quick and easy meal options is rising, subsequently driving the use of food additives. A report by the United Nations Food and Agriculture Organization highlights the rise in global processed food consumption, correlating with urban growth and lifestyle changes. This trend directly impacts the demand for silicon dioxide in food applications.

Government initiatives around food safety and quality also play a crucial role in supporting the silicon dioxide market. For instance, the European Food Safety Authority (EFSA) regulates the use of silicon dioxide as a food additive under the designation E551, ensuring it meets strict safety standards before it can be used in foods within the European Union. These regulations help maintain consumer trust and confidence in food safety, further bolstering the market for silicon dioxide.

In addition to regulatory support, technological advancements in food processing and additive manufacturing also contribute to the growth of the silicon dioxide market. These advancements improve the efficiency and effectiveness of silicon dioxide as an anti-caking agent, making it more appealing for food manufacturers seeking to optimize their production processes and extend the shelf life of their products.

Restraints

Health Concerns and Regulatory Scrutiny

A significant restraining factor impacting the growth of the silicon dioxide market is the increasing health concerns associated with its use, particularly in food and pharmaceutical applications. Although silicon dioxide is approved by major regulatory bodies like the Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) for use as an anti-caking agent and is generally recognized as safe (GRAS) when used in accordance with good manufacturing practices, there is ongoing scrutiny regarding its impact on human health, especially when consumed in large quantities.

Concerns mainly revolve around the potential for silicon dioxide to contribute to gastrointestinal issues if ingested in large amounts. Some consumer advocacy groups and health researchers suggest that excessive consumption of additives like silicon dioxide could lead to inflammation or other digestive disorders. This has led to a cautious approach among health-conscious consumers, who are increasingly scrutinizing product labels and opting for products with fewer synthetic additives.

These health concerns are mirrored by stringent regulatory standards, which can act as a double-edged sword. On one hand, they assure consumers of the safety of food products; on the other, they can restrict the use of certain additives like silicon dioxide. For instance, the EFSA continuously reviews the safety of food additives, including silicon dioxide, to ensure that they pose no health risks to consumers. Changes in regulatory standards can lead to reformulations of food and pharmaceutical products, which may reduce the use of silicon dioxide.

The trend towards natural and organic food products also significantly restrains the market for silicon dioxide. As more consumers demand “clean label” products with ingredients they recognize and trust, the food industry is responding by reducing the use of synthetic additives. Market reports from leading food industry analysts have noted a significant rise in the demand for natural ingredients, which is compelling food manufacturers to explore alternatives to silicon dioxide.

Furthermore, technological advancements in the formulation of natural and synthetic substitutes that can mimic or exceed the properties of silicon dioxide are gaining momentum. These substitutes are being designed to provide similar or enhanced anti-caking characteristics without the associated health risks, making them more attractive to health-conscious consumers and manufacturers aiming to maintain clean labels.

Opportunity

Expansion in the Global Pharmaceutical Sector

One significant growth opportunity for the silicon dioxide market is its expanding use in the pharmaceutical sector. Silicon dioxide is extensively used as an excipient in the formulation of drugs, where it serves crucial roles such as improving the flow of powders and stabilizing drug formulations. As the global demand for medications and supplements rises, so does the need for reliable and effective excipients like silicon dioxide.

The pharmaceutical industry is experiencing rapid growth, driven by an aging population, increased prevalence of chronic diseases, and continuous advancements in drug development. According to data from the World Health Organization (WHO), global spending on health is expected to increase, reaching over $10 trillion by the mid-2020s. This growth in healthcare expenditure indicates a rising demand for pharmaceuticals, which in turn drives the demand for excipients.

Silicon dioxide’s role in enhancing the bioavailability of drugs is particularly valuable. It helps in the controlled release of active ingredients, ensuring that medications are effective while minimizing side effects. Its inert nature also makes it ideal for use in a variety of formulations, including tablets, capsules, and powders.

Moreover, government initiatives to improve healthcare infrastructure and increase access to medicines are boosting the pharmaceutical industry. For example, initiatives like the Affordable Care Act in the United States have increased the number of individuals with access to prescription medications, thereby increasing the demand for pharmaceuticals and their components.

Innovations in drug delivery systems also present new opportunities for the use of silicon dioxide. Advanced formulations such as nano-encapsulations and high-efficiency delivery systems often require high-quality excipients to ensure stability and effectiveness. Silicon dioxide’s physical and chemical properties make it an excellent candidate for these advanced applications.

Additionally, the shift towards generic medications, driven by cost-cutting measures in healthcare, further boosts the demand for excipients like silicon dioxide. Generics require excipients to match the efficacy and stability of branded drugs, and silicon dioxide’s versatility makes it an attractive option for generic drug manufacturers.

Trends

Surge in Demand for Natural and Organic Silicon Dioxide in the Food Industry

A significant trend in the silicon dioxide market is the growing demand for natural and organic forms of silicon dioxide in the food industry. As consumers become increasingly aware of the ingredients in their food products, there is a notable shift towards ingredients that are perceived as natural and healthier. This trend is reflected in the rising preference for natural and organic silicon dioxide used as an anti-caking agent and other functional roles in food processing.

The food industry is responding to this consumer-driven demand by reformulating products to include naturally sourced silicon dioxide. This version of silicon dioxide is derived from organic materials and undergoes minimal processing, aligning with the clean label movement that seeks to offer products with easily recognizable and fewer ingredients.

Market data from leading food organizations indicate a substantial increase in the market share of natural food additives. According to a report by the Food and Agriculture Organization (FAO), the global market for organic food additives is projected to grow significantly, driven by consumer preferences for organic and natural products. This trend is further supported by governmental initiatives promoting organic farming and the production of natural food additives, which ensure a sustainable supply chain for these ingredients.

In addition to consumer demand, regulatory bodies are also playing a crucial role in this trend. For example, the United States Department of Agriculture (USDA) has set stringent standards for organic certification, which includes criteria for natural additives used in food products. These regulations not only ensure the safety and quality of food additives but also build consumer trust and drive the market for natural ingredients.

The shift towards natural and organic silicon dioxide is also encouraging innovation in the food processing industry. Companies are developing new methods to extract and purify silicon dioxide from natural sources without compromising its effectiveness as an anti-caking agent. These innovations are crucial for meeting both the regulatory standards and consumer expectations for natural products.

Furthermore, the trend towards natural ingredients is not limited to the food industry alone. The pharmaceutical and cosmetics industries are also observing a similar shift, with an increased demand for natural excipients and fillers, including silicon dioxide. This broader industry adaptation further underscores the significance of this trend and its potential to influence multiple markets.

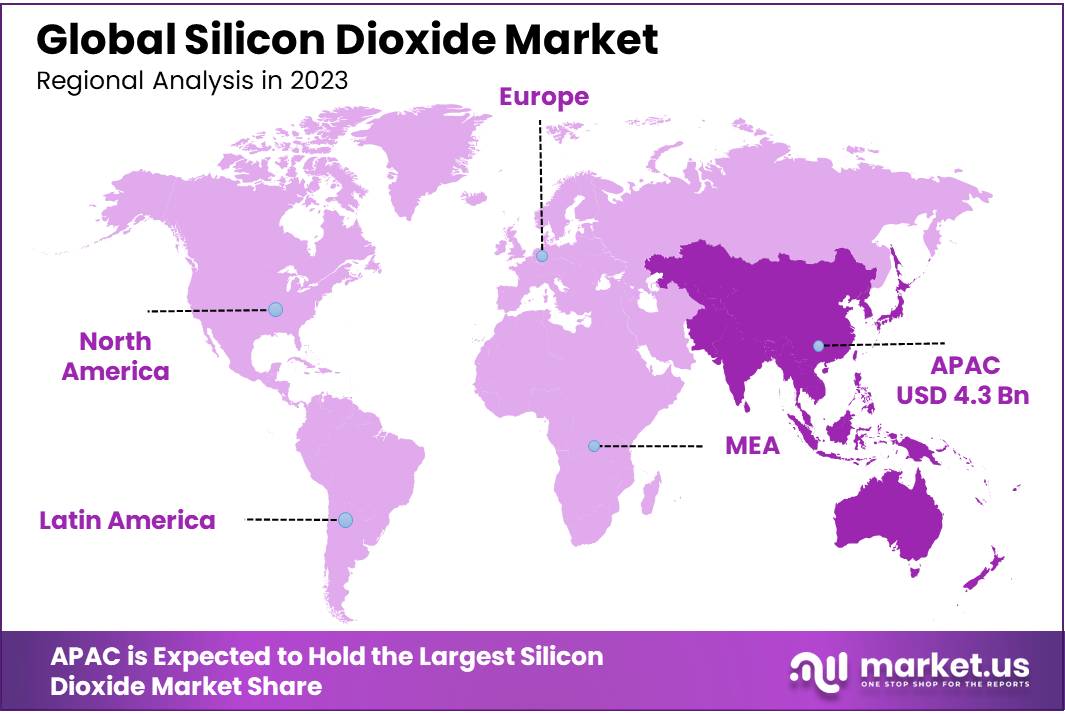

Regional Analysis

In 2023, the Asia Pacific (APAC) region dominated the silicon dioxide market, accounting for a significant 41.5% market share and generating approximately USD 4.3 billion in revenue. This dominance is driven by the region’s strong industrial base and the extensive use of silicon dioxide across key industries, including construction, electronics, and food and beverages.

Countries like China, India, and Japan lead the demand, with increasing investments in infrastructure development and advancements in semiconductor manufacturing further fueling market growth. APAC’s position as a major hub for electronics production has bolstered the demand for high-purity silicon dioxide, particularly in the fabrication of semiconductors and optical fibers.

In North America, the market is primarily driven by the expanding use of silicon dioxide in food and pharmaceuticals. The United States, with its stringent food safety regulations, has seen significant adoption of silicon dioxide as an anti-caking agent and stabilizer in processed foods and dietary supplements. Furthermore, the growth of the healthcare and construction sectors has spurred additional demand in the region.

Europe represents a mature market, with a focus on clean-label food ingredients and sustainable construction practices. The use of silicon dioxide in advanced coatings and specialty glass manufacturing is also notable, particularly in Germany, France, and the UK.

Meanwhile, the Middle East & Africa and Latin America are emerging markets, showing gradual growth due to increased industrialization and urbanization. These regions are leveraging silicon dioxide in building materials, adhesives, and coatings, while the food and beverage sectors are also beginning to adopt its applications more widely.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The silicon dioxide market is shaped by a mix of global leaders and regional players who bring innovation and scale to this highly competitive space. BASF SE and Evonik Industries AG are among the major players, leveraging their robust research and development capabilities to provide advanced silicon dioxide solutions for diverse industries, including construction, automotive, and food. Cabot Corporation and Wacker Chemie AG focus on high-performance applications such as specialty coatings and rubber reinforcements, contributing significantly to the market’s growth.

Companies like Merck KGaA and Shin-Etsu Chemical Co., Ltd. are pivotal in driving innovation in electronics and pharmaceuticals, where high-purity silicon dioxide is critical. Gelest Inc., a part of the Mitsubishi Chemical Group Corporation, is known for its tailored solutions, catering to niche markets like biomedicine and high-tech coatings. Similarly, PPG Industries, Inc. and Solvay SA lead in silicon dioxide applications for paints, adhesives, and advanced materials, aligning with global sustainability trends.

Emerging players such as JIOS Aerogel Pte Ltd. and Nanografi Nano Technology focus on cutting-edge nanomaterials and aerogels, expanding the scope of silicon dioxide applications in energy storage and insulation. Regional manufacturers, including Lorad Chemical Corporation and Tosoh Corporation, play an essential role in addressing localized demand while ensuring a steady supply of specialized products.

Top Key Players

- American Elements

- BASF SE

- Cabot Corporation

- Evonik Industries AG

- Gelest Inc. by Mitsubishi Chemical Group Corporation

- JIOS Aerogel Pte Ltd.

- Junsei Chemical Co.,Ltd.

- KANTO CHEMICAL CO.,INC.

- Lorad Chemical Corporation

- Merck KGaA

- Nacalai Tesque, Inc.

- Nanografi Nano Technology

- Otto Chemie Pvt. Ltd.

- OXFORD LAB FINE CHEM LLP

- PPG Industries, Inc.

- ProLuke

- Shin-Etsu Chemical Co., Ltd.

- Sinosi Group Corporation

- Solvay SA

- Spectrum Chemical Mfg. Corp.

- The Kurt J. Lesker Company

- Tokuyama Corporation

- Tosoh Corporation

- Vizag Chemicals

- Wacker Chemie A

Recent Developments

In 2024, BASF forecasts an EBITDA before special items ranging between €8.0 billion and €8.6 billion for the 2024 fiscal year, indicating anticipated growth and sustained demand across its product lines, including silicon dioxide.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 10.5 Bn |

| Forecast Revenue (2033) | USD 19.3 Bn |

| CAGR (2024-2033) | 6.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Purity (2N (99%), 2N5 (99.5%), 3N (99.9%), 3N5 (99.95%), 4N (99.99%) 5N (99.999%), Less than 99% Purity), By Form (Amorphous, Quartz, Keating, Cristobalite, Coesite, Tridymite), By Application (Building materials, Glass and Ceramics, Paints and Coatings, Adhesive and Sealants, Food and Pharmaceutical Sealant, Silicone Wafers, Others), By End Use (Building And Construction, Electrical And electronics, Healthcare, Food And Beverages, Chemical, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | American Elements, BASF SE, Cabot Corporation, Evonik Industries AG, Gelest Inc. by Mitsubishi Chemical Group Corporation, JIOS Aerogel Pte Ltd., Junsei Chemical Co.,Ltd., KANTO CHEMICAL CO.,INC., Lorad Chemical Corporation, Merck KGaA, Nacalai Tesque, Inc., Nanografi Nano Technology, Otto Chemie Pvt. Ltd., OXFORD LAB FINE CHEM LLP, PPG Industries, Inc., ProLuke, Shin-Etsu Chemical Co., Ltd., Sinosi Group Corporation, Solvay SA, Spectrum Chemical Mfg. Corp., The Kurt J. Lesker Company, Tokuyama Corporation, Tosoh Corporation, Vizag Chemicals, Wacker Chemie A |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |