Quick Navigation

Report Overview

The Global Encryption Software Market is estimated to be worth USD 16.7 billion in 2024 and projected to be valued at USD 60.7 billion in 2033. Between 2024 and 2033, the market is expected to register a growth rate of 15.4%.

Encryption software refers to programs that encode data and messages in a way that only authorized parties can access it. This is done by using algorithms and cryptographic protocols to scramble plain text into ciphertext that is very difficult to decipher without the encryption key. Encryption software provides data security and privacy for sensitive information transmitted and stored digitally. Common applications include encryption of files and disks, emails, network communications, databases, and cloud data. Leading encryption techniques include AES, RSA, SSL/TLS, PGP, etc.

The encryption software market covers products, services, and companies involved in providing encryption capabilities. This market has seen strong growth as demand rises for securing sensitive data and communications. Driving factors include cybersecurity threats, regulatory mandates, cloud adoption, and remote workforce expansion.

Note: Actual Numbers Might Vary In The Final Report

Key Takeaways

- Market Growth and Size: The Encryption Software Market is estimated to be worth USD 16.7 billion in 2024. It is projected to reach USD 60.7 billion by 2033.

- Market Drivers: Cybersecurity threats, regulatory requirements, and the adoption of cloud services are driving the demand for encryption software.

- Component Analysis: In 2023, the software segment held over a 68% share of the market, driven by data security needs in core application software.

- Deployment Model Analysis: In 2023, the cloud segment dominated the market, with more than a 61% share, due to widespread cloud service adoption.

- Function Insights: Communication encryption held over a 35% market share in 2023, emphasizing the importance of secure communication channels.

- Industry Vertical Analysis: BFSI sector held over a 21% market share in 2023, driven by the need to protect financial data and maintain customer trust.

- Driving Factors: Increasing cybersecurity threats, stringent data protection regulations, growing cloud adoption, and data privacy concerns are key drivers.

- Restraining Factors: Challenges include complexity in implementation, potential performance impact, cost of implementation, and key management complexity.

- Growth Opportunities: Opportunities include securing IoT devices, addressing quantum computing challenges, and integrating with big data analytics.

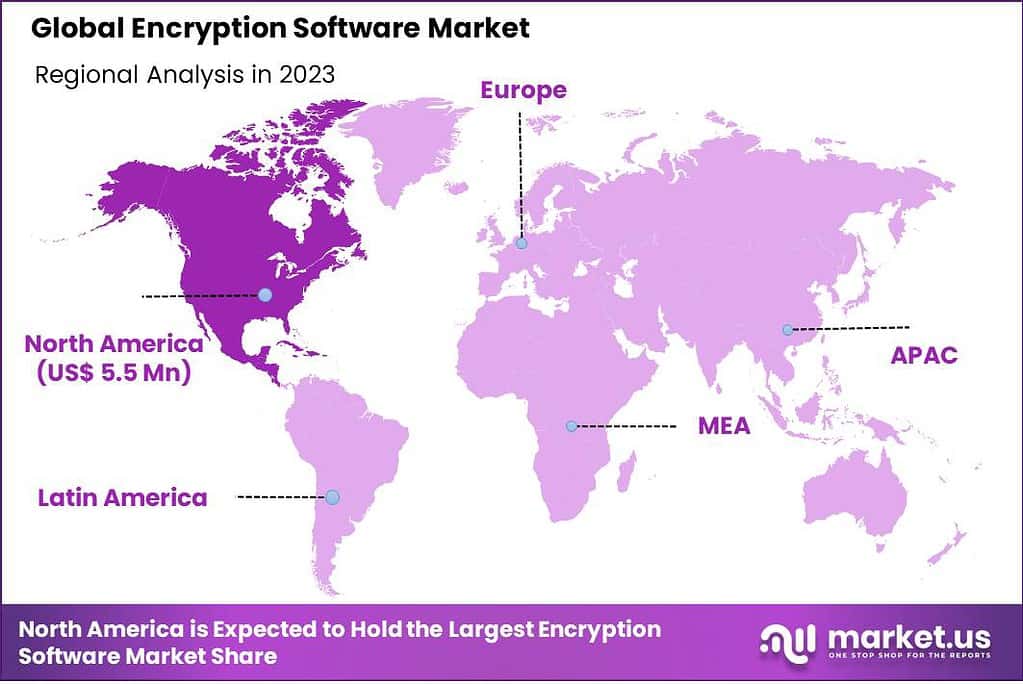

- Regional Analysis: North America dominated the market in 2023, accounting for over 38% of the share, driven by a highly developed IT infrastructure.

- Key Players: Top key players include Bloombase, Check Point Software Technologies, IBM, Symantec, and others.

Component Analysis

In 2023, the software segment held a dominant market position, capturing more than a 68% share of the global encryption software market. This large share is attributed to the rising need for data security and privacy capabilities built into core application software. Encryption features in email, messaging, file storage, and workplace collaboration tools are driving adoption. Increased cloud migration is also boosting demand for encryption software-as-a-service.

Meanwhile, the services segment accounted for the remaining market share. This includes professional and managed services around implementing, managing, and optimizing encryption software solutions. The complex key management involved in encryption drives demand for specialized consulting and support services.

Going forward, the software segment is expected to retain the larger share of the encryption software market. But services will likely see high growth as software adoption expands globally. Consulting and managed services help organizations effectively leverage encryption while optimizing cost and complexity. The market for complementary services around encryption software implementation and management will continue rising steadily.

Deployment Model Analysis

In 2023, the Cloud segment held a dominant market position in the Encryption Software Market, capturing more than a 61% share. This significant lead is primarily due to the widespread adoption of cloud services across industries, driving the need for advanced encryption to protect data in transit and at rest. Organizations are increasingly relying on cloud platforms for scalability, flexibility, and cost-efficiency, thus amplifying the demand for cloud-based encryption solutions to secure sensitive data against unauthorized access and breaches.

On-premise encryption software, while having a smaller market share, remains critical for certain sectors that require direct control over security measures due to regulatory, compliance, or specific risk management needs. Industries such as banking, government, and healthcare often prefer on-premise solutions for their ability to provide enhanced control over sensitive data. Despite the dominance of the cloud, the on-premise segment continues to evolve, focusing on catering to niche requirements and integrating with existing infrastructure.

Function Insights

In 2023, the Communication Encryption segment held a dominant market position in the Encryption Software Market, capturing more than a 35% share. This prominence is due to the growing need for secure communication channels across various industries and personal use, especially with the increasing prevalence of remote work and digital communication platforms.

Communication encryption software ensures that information transmitted over networks is secure from unauthorized access or interception, fostering trust and compliance with data protection regulations. As cyber threats become more sophisticated, the demand for robust communication encryption solutions continues to rise, driving significant growth in this segment.

Disk Encryption is another critical area, providing security by encrypting the data stored on a computer’s hard drive or other storage devices. This method is particularly effective in preventing data breaches in case of device theft or loss, making it a fundamental security measure for both individual users and organizations. With the escalating number of data theft incidents and stringent regulatory requirements, the disk encryption segment is witnessing steady growth as users seek to safeguard sensitive information at rest.

File/Folder Encryption allows users to protect specific documents and directories, offering a targeted approach to data security. This function is essential for protecting sensitive data in shared environments or when transmitting files across less secure networks. As businesses and individuals become more aware of the risks associated with unprotected data, the demand for file and folder encryption solutions is increasing, contributing to the growth of this market segment.

Cloud Encryption is rapidly gaining traction as more organizations migrate to cloud-based services. This function addresses the unique security challenges of the cloud environment, encrypting data before it moves out of the organization’s network and ensuring that only authorized users can access the information. With the ongoing shift towards cloud computing and the rising concerns over cloud security, the cloud encryption segment is poised for substantial growth.

Each of these segments addresses specific security needs and challenges, reflecting the diverse requirements of users in a digital and interconnected world. As technology evolves and cyber threats become more complex, the importance of encryption software across all these functions is expected to grow, driving innovation and market expansion.

Industry Vertical Analysis

In 2023, the BFSI (Banking, Financial Services, and Insurance) segment held a dominant market position in the Encryption Software Market, capturing more than a 21% share. This sector’s significant reliance on encryption software is driven by the need to protect sensitive financial data, comply with stringent regulatory standards, and maintain customer trust in an era of increasing cyber threats. Financial institutions are adopting advanced encryption solutions to secure transactions, safeguard online banking portals, and protect confidential communication, fueling substantial growth in this market segment.

The IT/Telecom industry is another major user of encryption software, as these businesses manage vast amounts of sensitive data and are often targets of cyber-attacks. Encryption is crucial for protecting intellectual property, customer information, and internal communications. As IT and telecom companies continue to expand their digital services, the demand for robust encryption solutions to secure data in transit and at rest is expected to rise.

Government and Public sector entities are increasingly focusing on encryption to protect state secrets, sensitive citizen data, and critical infrastructure from both external and internal threats. The growing awareness of national security and privacy concerns, coupled with regulatory compliance requirements, is driving the adoption of encryption technologies in this sector.

In the Retail industry, encryption software is vital for protecting customer transaction data, particularly payment information. As e-commerce grows and data breaches become more costly, retailers are investing in encryption to ensure a secure shopping experience and maintain consumer confidence.

Healthcare organizations are turning to encryption to secure patient records and other sensitive health data. With regulations like HIPAA in the United States mandating the protection of patient information, encryption is becoming an essential tool for compliance and data security in the healthcare sector.

The Aerospace and Defense industry requires encryption to secure highly sensitive data, including military communications and proprietary technology. The need for advanced security measures to protect against espionage and cyber-attacks is driving significant investment in encryption software within this sector.

Media and Entertainment companies are using encryption to protect intellectual property, such as films, music, and digital content, from unauthorized access and distribution. As the industry continues to digitize, the need for encryption to safeguard content and ensure copyright compliance is growing.

Other Industry Verticals, including manufacturing, education, and energy, are also recognizing the importance of encryption as they digitize their operations and handle more sensitive data. Across these sectors, the drive to protect intellectual property, ensure privacy, and comply with regulatory standards is contributing to the broader adoption of encryption software.

Driving Factors:

- Increasing Cybersecurity Threats: The rising frequency and sophistication of cyberattacks have fueled the demand for encryption software. Organizations across various sectors are adopting encryption solutions to protect sensitive data from unauthorized access, ensuring data security and compliance with data protection regulations.

- Stringent Data Protection Regulations: The implementation of stringent data protection regulations, such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), has mandated the use of encryption for safeguarding personal and sensitive data. This regulatory landscape is driving the adoption of encryption software among businesses to avoid potential data breaches and associated penalties.

- Growing Adoption of Cloud Services: With the increasing adoption of cloud computing and storage services, the need to secure data in transit and at rest has become paramount. Encryption software provides a critical layer of protection for data stored and transmitted through cloud platforms, addressing security concerns and fostering the growth of the encryption software market.

- Emphasis on Data Privacy and Confidentiality: The growing awareness and concerns regarding data privacy and confidentiality have propelled the demand for encryption software. Both individuals and organizations are recognizing the importance of encrypting their data to maintain privacy, prevent data leakage, and preserve the integrity of sensitive information.

Restraining Factors:

- Complexity and Integration Challenges: Implementing encryption software can be complex, requiring expertise in encryption algorithms, key management, and integration with existing IT infrastructure. Organizations may face challenges in integrating encryption solutions with their existing systems, leading to deployment delays and potential compatibility issues.

- Performance Impact: Encryption processes can introduce computational overhead, potentially impacting system performance, especially in resource-constrained environments. Balancing the need for strong encryption with optimal system performance can be a challenge, particularly in scenarios where real-time data processing is crucial.

- Cost of Implementation: The cost associated with encryption software implementation, including licensing fees, hardware requirements, and ongoing maintenance, can be a restraining factor for some organizations, particularly small and medium-sized enterprises (SMEs) with limited budgets. The perceived cost barriers may hinder the adoption of encryption solutions, especially among price-sensitive market segments.

- Key Management Complexity: Effective encryption relies on robust key management practices. The complexity of managing encryption keys, including key generation, distribution, storage, and rotation, can pose challenges for organizations. Inadequate key management practices can weaken the overall security posture, making it essential for businesses to invest in proper key management solutions and processes.

Growth Opportunities

- Increasing Adoption of IoT Devices: The proliferation of Internet of Things (IoT) devices generates vast amounts of data that require secure transmission and storage. Encryption software presents significant growth opportunities in securing IoT devices and the data they generate, ensuring the integrity and confidentiality of IoT ecosystems.

- Rise of Quantum Computing: As quantum computing continues to advance, there is a growing need for encryption algorithms resistant to quantum attacks. The development of quantum-safe encryption algorithms and solutions presents a promising growth opportunity for encryption software vendors to address future security challenges.

- Expansion of E-commerce and Digital Payments: The rapid growth of e-commerce and digital payment platforms necessitates robust security measures, including encryption, to protect financial transactions and customer data. The increasing adoption of encryption software in the e-commerce sector offers substantial growth prospects for encryption software providers.

- Integration with Big Data Analytics: The integration of encryption software with big data analytics platforms enables secure processing and analysis of large volumes of sensitive data. Encryption software vendors can capitalize on this opportunity by offering solutions that combine encryption with data analytics capabilities, providing enhanced security and data-driven insights.

Challenges

- Compliance with Global Encryption Regulations: Encryption software providers face the challenge of navigating complex and varying encryption regulations across different countries and jurisdictions. Ensuring compliance with these regulations, which often involve restrictions on encryption strength and key management practices, can pose significant challenges for vendors operating in global markets.

- Balancing Security and User Experience: Encryption software must strike a balance between robust security measures and a seamless user experience. Ensuring that encryption does not hinder user workflows or impede the usability of applications requires careful design and consideration of user needs, which can be a challenge for software developers.

- Evolving Threat Landscape: The encryption software market faces the ongoing challenge of keeping up with the constantly evolving threat landscape. As cyber threats continue to evolve and become more sophisticated, encryption software must adapt to address new vulnerabilities and encryption-breaking techniques, requiring continuous innovation and updates.

- Lack of Awareness and Understanding: Despite the importance of encryption for data security, there is still a lack of awareness and understanding among individuals and organizations. Educating users about the benefits and best practices of encryption software adoption presents a challenge for market players to drive widespread adoption and market growth.

Key Market Trend

An emerging trend in the encryption software market is the adoption of homomorphic encryption. Homomorphic encryption allows computations to be performed on encrypted data without the need for decryption, maintaining data privacy while enabling secure data processing and analysis. This trend is particularly relevant in sectors such as healthcare and finance, where data privacy is critical, and the ability to perform computations on encrypted data opens up possibilities for secure data sharing and collaborative analysis. The integration of homomorphic encryption into encryption software solutions represents a key market trend, catering to the growing demand for secure data processing and privacy-preserving analytics.

Key Market Segments

Component

- Software

- Services

Deployment Model

- On-premise

- Cloud

Function

- Disk Encryption

- Communication Encryption

- File/Folder Encryption

- Cloud Encryption

Industry Vertical

- BFSI

- IT/Telecom

- Government & Public

- Retail

- Healthcare

- Aerospace & Defense

- Media & Entertainment

- Other Industry Verticals

Regional Analysis

In 2023, North America held a dominant market position in the encryption software market, capturing more than a 38% share. The region’s strong market presence can be attributed to several factors. Firstly, North America has a highly developed IT infrastructure and a high level of digitalization across various industries, which has led to an increased focus on data security and privacy. Additionally, stringent data protection regulations, such as the GDPR and the California Consumer Privacy Act, have propelled the adoption of encryption software among businesses operating in the region. The presence of major encryption software vendors and cybersecurity companies in North America further contributes to the region’s market dominance.

Europe is another significant region in the encryption software market, accounting for a substantial market share. The region’s emphasis on data protection and privacy, backed by the GDPR and other regional regulations, has driven the adoption of encryption solutions across industries. European organizations are increasingly investing in advanced encryption technologies to safeguard sensitive data and comply with data protection laws. Additionally, the growing prevalence of cyber threats and high-profile data breaches has heightened the demand for encryption software in Europe.

The Asia Pacific (APAC) region is experiencing rapid growth in the encryption software market. Increasing digitalization, expanding e-commerce sectors, and the adoption of cloud services are driving the demand for encryption solutions in APAC. Countries such as China, Japan, and India are witnessing significant growth in the adoption of encryption software, primarily driven by the need to protect sensitive data and comply with data protection regulations. Moreover, the rising awareness regarding cybersecurity and the increasing investments in IT infrastructure contribute to the growth of the encryption software market in the region.

Latin America is also emerging as a promising market for encryption software. The region is witnessing an increasing number of cyber threats and data breaches, which has prompted organizations to invest in encryption solutions. Governments in Latin American countries are enacting data protection laws and regulations, encouraging the adoption of encryption software to ensure compliance and data security. Additionally, the growing e-commerce sector and the digitization of business processes fuel the demand for encryption software in Latin America.

The Middle East and Africa (MEA) region is gradually adopting encryption software to address cybersecurity concerns and protect sensitive data. The region’s growing reliance on digital technologies, coupled with the rising incidence of cyberattacks, has created a need for robust encryption solutions. Governments in the MEA region are implementing data protection regulations, which further drive the adoption of encryption software among businesses. While the market in MEA is still relatively nascent compared to other regions, it presents significant growth opportunities for encryption software vendors.

Overall, the encryption software market exhibits a strong presence in North America and Europe, driven by data protection regulations and a high level of digitalization. APAC, Latin America, and MEA are witnessing substantial growth due to increasing awareness of cybersecurity threats and the need for data privacy. The market dynamics vary across regions, influenced by regional regulations, level of digitalization, and industry-specific cybersecurity requirements.

Note: Actual Numbers Might Vary In The Final Report

Key Regions and Countries Covered in this Report:

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Thailand

- Singapore

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Encryption Software Market features a dynamic and competitive landscape with several key players that dominate the industry. These companies are at the forefront of innovation, offering advanced encryption solutions to meet the growing demand for data security across various sectors

Top Key Players

- Bloombase

- Check Point Software Technologie

- East-Tec

- Entrust

- Hewlett Packard

- IBM

- InterCrypto

- Trend Micro

- Symantec

- Cisco

- Other Key Players

Recent Developments

- In June 2023, IBM introduced a new tool aimed at aiding businesses in monitoring greenhouse gas emissions across their cloud services, enhancing sustainability efforts during the transition to hybrid and multi-cloud environments.

- In March 2023, SAS Customer Intelligence 360 became available for purchase through the AWS Marketplace, a digital catalog featuring thousands of software listings from independent vendors. This platform simplifies the process of browsing, testing, purchasing, and deploying software that operates on Amazon Web Services (AWS).

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 14.5 Bn |

| Forecast Revenue (2033) | USD 60.7 Bn |

| CAGR (2024-2033) | 15.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software, Services), By Deployment Model(On-premise, Cloud), By Function (Disk Encryption, Communication Encryption, File/Folder Encryption, Cloud Encryption), By Industry Vertical (BFSI, IT/Telecom, Government & Public, Retail, Healthcare, Aerospace & Defense, Media & Entertainment, Other Industry Verticals) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, and Rest of Europe; APAC- China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, and Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- South Africa, Saudi Arabia, UAE & Rest of MEA |

| Competitive Landscape | Bloombase, Check Point Software Technologie, East-Tec, Entrust, Hewlett Packard, IBM, InterCrypto, Trend Micro, Symantec, Cisco, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Encryption Software Market encompasses the industry involved in the development, distribution, and implementation of software solutions designed to encrypt data for the purpose of securing it from unauthorized access and ensuring confidentiality.

The Global Encryption Software Market is estimated to be worth USD 16.7 billion in 2024 and projected to be valued at USD 60.7 billion in 2033. Between 2024 and 2033, the market is expected to register a growth rate of 15.4%.

Growth in the Encryption Software Market is primarily driven by factors such as increasing cybersecurity threats, stringent data protection regulations, the growing adoption of cloud services, and a heightened emphasis on data privacy and confidentiality.

Challenges in implementing encryption software include complexity and integration issues, potential performance impacts on systems, the associated costs of implementation, and the complexity of key management practices.

An emerging trend in the Encryption Software Market is the adoption of homomorphic encryption. This technology allows computations on encrypted data without decryption, catering to sectors where data privacy is critical, such as healthcare and finance.