Quick Navigation

- Report Overview

- Key Takeaways

- U.S. Market Size and Growth

- Component Analysis

- Deployment Mode Analysis

- Compliance Type Analysis

- End User Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Impact of AI on EdTech

- Key Regions and Countries

- Key Player Analysis

- Updates From Key Players

- Report Scope

Report Overview

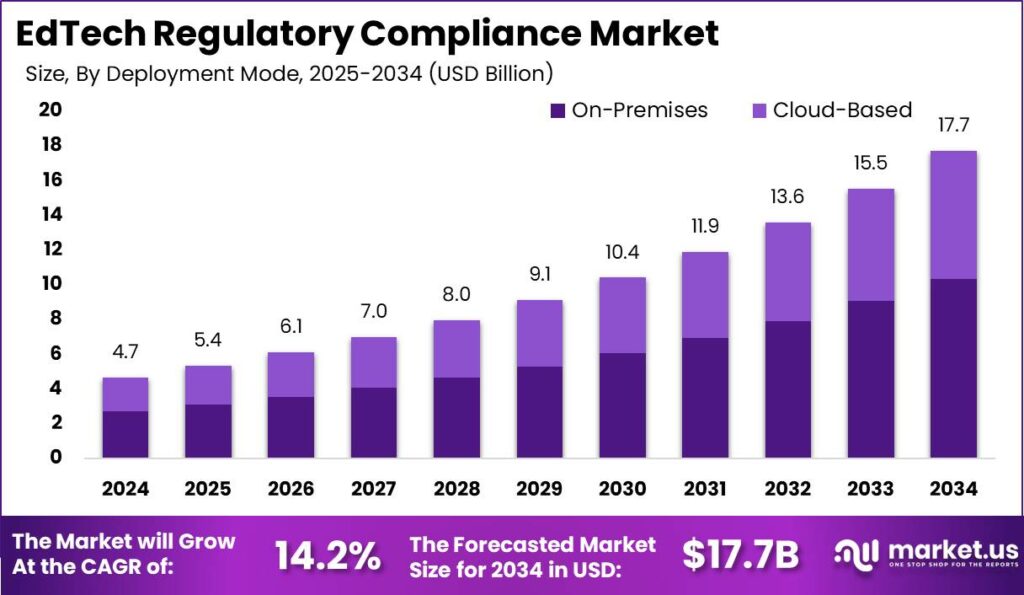

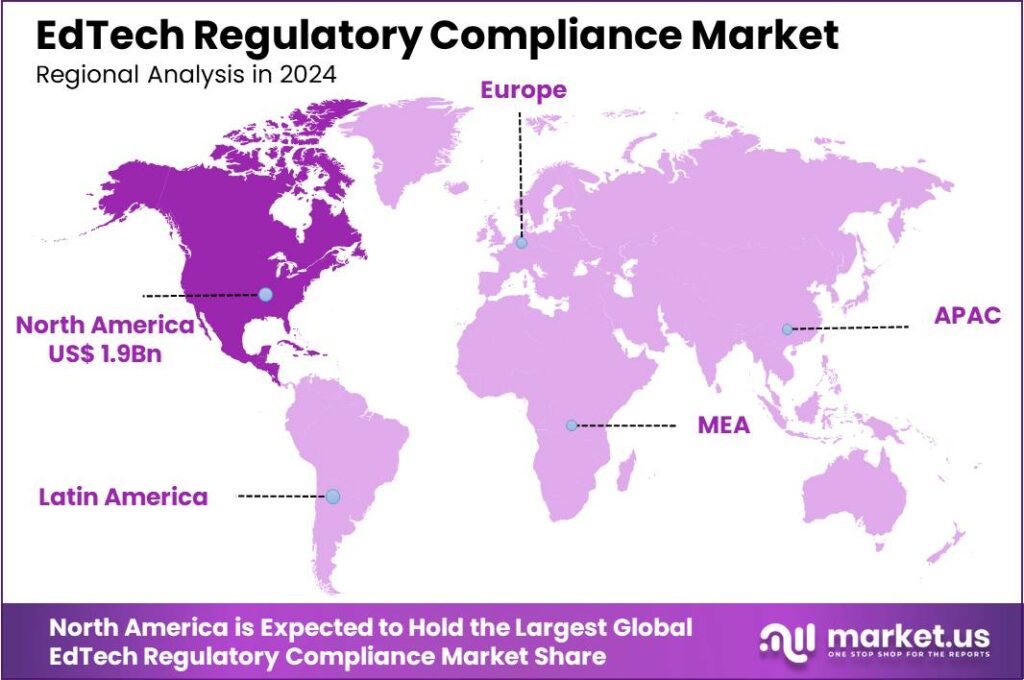

The Global EdTech Regulatory Compliance Market size is expected to be worth around USD 17.7 Billion By 2034, from USD 4.7 billion in 2024, growing at a CAGR of 14.2% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 42% share, holding USD 1.9 Billion revenue.

EdTech regulatory compliance encompasses the legal requirements and guidelines that education technology companies must adhere to in order to operate legally and ethically. This includes regulations related to data privacy, accessibility, content standards, and consumer protection. The aim of regulatory compliance in the EdTech sector is to ensure that technological advancements in education do not compromise student safety, privacy, and the quality of education.

The EdTech regulatory compliance market involves services and solutions that help educational institutions and technology providers meet the stringent legal requirements imposed on them. This market has seen substantial growth due to the increasing digitization of education and the complex legal landscapes of different regions. Companies in this market offer consulting, auditing, training, and compliance management software to ensure that educational technologies are developed and implemented in accordance with the law.

The growth of the EdTech regulatory compliance market can be attributed to several key factors. Firstly, the global surge in the adoption of digital learning tools has necessitated stringent data protection measures to safeguard student information. Additionally, the expansion of online learning platforms across borders has introduced complex regulatory challenges, requiring expertise in multiple legal frameworks.

Furthermore, increasing awareness and concern about digital equity and accessibility in education drive demand for compliance to ensure that all students can benefit from technological advancements. Demand in the EdTech Regulatory Compliance Market is high among institutions that are either adopting new technologies or scaling existing digital education solutions.

Market.us’s findings show that the global EdTech market is projected to grow significantly, reaching an estimated USD 810.3 billion by 2033, up from USD 220.5 billion in 2023. This represents an impressive compound annual growth rate (CAGR) of 13.9% between 2024 and 2033. In 2023, North America led the market, contributing more than 37.3% of the total revenue, equivalent to USD 82.24 billion.

Interestingly, a survey by Local Circle highlights growing consumer concerns in this sector. About 66% of respondents feel that edtech should be regulated, and an overwhelming 96% support the introduction of a code of conduct for subscription plans and service packages offered by these platforms.

India’s education system also underscores the vast opportunities and challenges in this field. According to the Economic Survey 2023-24, the country has 265.2 million school students, approximately 43 million enrolled in higher education, and over 110 million individuals in skilling programs. These numbers emphasize the critical need for innovation and investment in education technology.

Meanwhile, regulatory frameworks are becoming stricter worldwide. In the European Union, businesses face penalties of 2% to 4% of their revenue for violating GDPR, while in the United States, failing to comply with COPPA can lead to fines of up to $43,280 per child privacy violation. Such regulations push edtech companies to prioritize compliance and transparency as they expand globally.

Technological advancements play a crucial role in the EdTech Regulatory Compliance Market. Innovations such as AI and machine learning are being leveraged to automate compliance processes, predict potential compliance risks, and provide more robust data security measures. These technologies enable more efficient management of compliance tasks, reducing the burden on educational institutions and enhancing the overall reliability of compliance audits.

Key Takeaways

- The global market for EdTech regulatory compliance is projected to reach an estimated value of USD 17.7 billion by 2034, up from USD 4.7 billion in 2024. This represents a robust compound annual growth rate (CAGR) of 14.2% from 2025 to 2034.

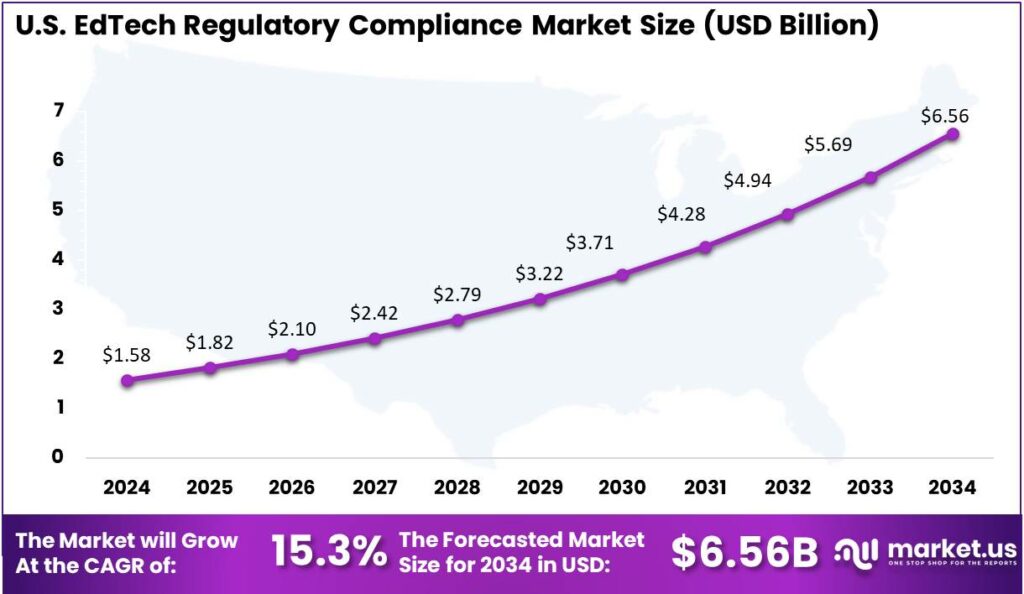

- In 2024, North America emerged as a leading player in this market, securing more than 42% of the global share, translating to revenues of USD 1.9 billion. Specifically, the United States demonstrated significant market size, valued at USD 1.58 billion with a projected CAGR of 15.3%.

- Focusing on the product offerings within this market, the Solution segment proved predominant, holding over 64.7% of the market share in 2024.

- Regarding deployment modes, the On-Premises option was preferred by a majority, with over 58.4% of the market opting for this traditional method of software implementation in 2024.

- The Data Privacy and Protection segment within the market also held significant sway, capturing more than 30.2% of the market share.

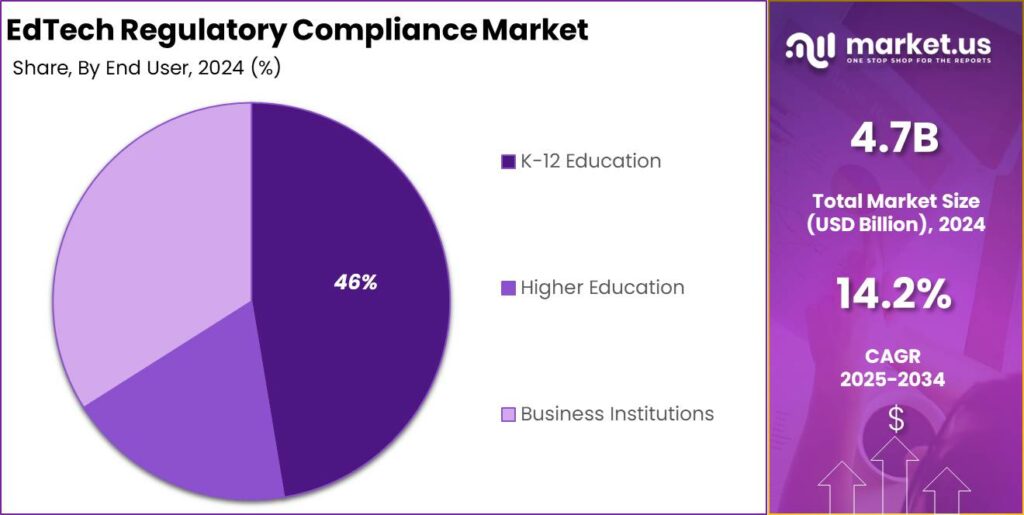

- Lastly, the K-12 Education segment maintained a solid footing, with over 46% share in 2024.

U.S. Market Size and Growth

The US EdTech Regulatory Compliance Market size was exhibited at USD 1.58 Bn in 2024 with CAGR of 15.3%. The North American region is currently leading the global EdTech Regulatory Compliance market with significant growth and market share, due in part to several key factors that drive this dominance.

Firstly, the region benefits from an advanced technological infrastructure which facilitates the rapid deployment and scaling of EdTech solutions. This is particularly evident in the United States, which is home to major technology hubs like Silicon Valley. The environment fosters innovation and early adoption of digital education tools, allowing for swift integration into educational settings and thereby promoting substantial market growth.

In addition to technological advantages, North America sees substantial investment from both the public and private sectors, which further propels the development and adoption of EdTech solutions. For example, significant venture capital investments and government funding for digital education have been instrumental in shaping the market dynamics and fueling the sector’s expansion.

Moreover, the demand in North America for personalized and accessible educational technologies drives ongoing innovation within the EdTech sector. Companies in this region are increasingly focusing on creating learning solutions tailored to individual needs using advanced technologies like AI and data analytics. This approach not only enhances learning outcomes but also aligns with the growing trend towards personalized education, making the market particularly responsive to these advancements.

In 2024, North America held a dominant market position in the EdTech Regulatory Compliance sector, capturing more than a 42% share and generating revenue of approximately USD 1.9 billion. This leadership can be attributed to several key factors that uniquely position the region at the forefront of the industry.

The advanced technological infrastructure in North America, particularly in the United States, supports the rapid development and deployment of EdTech solutions. Major technology hubs such as Silicon Valley serve as the epicenter for innovation and digital education advancements, fostering an environment conducive to the growth of the EdTech market.

Furthermore, North America benefits from significant investment in educational technology, both from the public sector and private investors. This financial backing not only accelerates the adoption of new technologies in education but also stimulates ongoing innovation within the sector.

Additionally, there is a strong emphasis on regulatory compliance in North America, driven by stringent data protection laws and a high awareness of cybersecurity needs within educational institutions. These regulations ensure that EdTech products not only enhance educational outcomes but also prioritize student data safety and institutional accountability.

Component Analysis

In 2024, the Solution segment of the EdTech regulatory compliance market held a dominant position, capturing more than 64.7% of the market share. This substantial share can be attributed to several critical factors that underline the pivotal role of compliance solutions within the educational technology sector.

Firstly, the increasing adoption of digital learning platforms necessitates robust compliance tools to ensure the protection of student data and adherence to various educational standards and regulations. Learning Management Systems (LMS), which form a core component of this segment, are essential for the structured delivery of online courses and content.

Their compliance with standards such as SCORM (Sharable Content Object Reference Model) and others specific to different regions is crucial for interoperability and functionality across different educational systems and borders. Additionally, data privacy and protection software are increasingly in demand as educational institutions and technology providers strive to comply with stringent regulations such as the General Data Protection Regulation (GDPR) in the European Union and the Family Educational Rights and Privacy Act (FERPA) in the United States.

The emphasis on securing student information and ensuring privacy is driving the adoption of advanced security solutions within the EdTech space, further solidifying the Solution segment’s market position. Moreover, the ongoing digital transformation in education – accelerated by the COVID-19 pandemic – has highlighted the importance of compliance and regulatory solutions that can adapt to rapidly changing educational environments and technological advancements.

As schools and universities expand their digital footprints, the need for comprehensive compliance frameworks that can integrate seamlessly with existing and new technologies becomes more critical. This adaptability not only supports compliance but also enhances the overall effectiveness and reach of digital education platforms.

These factors collectively contribute to the robust growth and dominant market share of the Solution segment in the EdTech regulatory compliance market. As this sector continues to evolve, the reliance on effective compliance solutions is expected to grow, driven by the increasing complexity of educational technologies and the global expansion of digital learning.

Deployment Mode Analysis

In 2024, the On-Premises deployment mode in the EdTech regulatory compliance market retained a dominant position, securing over 58.4% of the market share. This leading role can be largely attributed to several inherent benefits that on-premises solutions provide to educational institutions, particularly in terms of security, control, and customization.

Security is a paramount concern for educational institutions, which handle sensitive student data. On-premises systems offer organizations full control over their security measures. Institutions can implement their own cybersecurity protocols and adhere strictly to regional compliance standards without relying on third-party cloud service providers. This level of control is crucial in regions with stringent data protection laws, ensuring that all compliance requirements are met directly and securely.

Moreover, on-premises deployment allows for greater customization to fit specific educational or administrative needs. Educational institutions often have unique requirements and integrating specific functionalities into an on-premises system can be more straightforward than with cloud-based solutions. This customization extends to integrating with legacy systems, which is a common scenario in long-established educational entities.

Lastly, the preference for on-premises systems also stems from their perceived reliability and performance stability. These systems do not depend on internet connectivity, which can be a critical factor in ensuring that educational activities are not disrupted due to connectivity issues. On-premises solutions provide the assurance that all educational tools and data are accessible at all times from the campus network, facilitating a seamless learning and administration experience.

Compliance Type Analysis

In 2024, the Data Privacy and Protection segment in the EdTech regulatory compliance market held a commanding market share, capturing more than 30.2%. This significant share is driven by the increasing global emphasis on data security and compliance with stringent regulations.

A major factor contributing to the dominance of this segment is the widespread enforcement of data protection laws across various regions, including the General Data Protection Regulation (GDPR) in Europe and the Family Educational Rights and Privacy Act (FERPA) in the United States. These regulations mandate strict standards for data privacy, compelling educational institutions and EdTech companies to prioritize robust compliance measures.

The rapid digital transformation in education has led to a surge in data generation, making data privacy and protection even more critical. Educational institutions are collecting extensive amounts of personal information, necessitating advanced security measures to protect this sensitive data from breaches and unauthorized access.

Moreover, the integration of technologies such as AI and machine learning in EdTech enhances the need for privacy safeguards, as these technologies can potentially expose personal data to new vulnerabilities. As such, EdTech companies are increasingly investing in compliance solutions that not only protect data but also ensure they are adhering to evolving global standards, thus maintaining trust and credibility in the digital education space.

This segment’s growth is also supported by technological advancements that simplify compliance with these complex regulations. AI-driven compliance tools, for example, are becoming essential for managing the scale and complexity of regulatory requirements that EdTech companies must navigate.

End User Analysis

In 2024, the K-12 Education segment of the EdTech regulatory compliance market held a dominant market position, securing more than 46% share. This prominence can largely be attributed to several key factors that are specific to the educational and technological needs of this segment.

Firstly, the K-12 sector has been at the forefront of integrating technology into the classroom, driven by initiatives to enhance educational access and equity, and to tailor learning experiences to individual student needs. This has necessitated a robust framework for compliance, especially in terms of data privacy, safeguarding student information, and adhering to educational standards, which are increasingly stringent as digital platforms become more embedded in K-12 education.

Moreover, the surge in digital learning tools and content tailored specifically for K-12 students has increased the demand for regulatory compliance solutions that can address the unique challenges of this sector. These solutions ensure that digital tools and content not only meet educational standards but also comply with local and international regulations concerning student data privacy and online safety.

Additionally, the K-12 market’s dominance is also propelled by significant investments from both public and private sectors aimed at upgrading educational technology infrastructures. This financial backing supports the adoption of new technologies and compliance solutions, ensuring that schools can safely and effectively integrate the latest educational technologies.

Key Market Segments

By Component

- Solution

- Learning Management System (LMS) compliance tools

- Data privacy and protection software

- Others

- Services

By Deployment Mode

- Cloud-Based

- On-Premises

By Compliance Type

- Data Privacy and Protection

- Accessibility Standards

- Content and Curriculum Compliance

- Cybersecurity Regulations

- Ethical Compliance

- Others

By End User

- K-12 Education

- Higher Education

- Business Institutions

Driver

Integration of Advanced Technologies in Education

The incorporation of cutting-edge technologies such as artificial intelligence (AI), machine learning (ML), and cloud computing within the educational sector is a significant driver for the EdTech regulatory compliance market. These technologies facilitate personalized learning, improve engagement through interactive content, and enhance the efficiency of educational processes.

As institutions increasingly adopt these technologies, the demand for compliance with data protection, accessibility standards, and other regulatory requirements grows. This ensures that educational technology products are safe and effective for all users. For instance, AI and ML are used to tailor educational content to the learning pace of individual students, which necessitates rigorous data handling and privacy measures.

Restraint

Resistance to Technology Adoption

Despite the benefits of EdTech, there remains a notable hesitation among some educational institutions and educators towards adopting new technologies. This resistance often stems from a lack of understanding and trust in new tools, the perceived complexity of integrating technology with traditional teaching methods, and concerns over job security for teachers.

Additionally, the initial cost of implementing technology-based learning solutions and the ongoing maintenance can be significant. These factors slow down the adoption rate of EdTech solutions, subsequently impacting the growth of the EdTech regulatory compliance market as fewer institutions engage with these technologies.

Opportunity

Global Expansion of EdTech Solutions

The global expansion of EdTech companies presents substantial opportunities, especially in emerging markets where educational technology is not yet saturated. Markets in Asia-Pacific, for example, are rapidly adopting EdTech solutions due to increasing internet penetration and a growing young population seeking quality education.

Regulatory frameworks in these regions are evolving to support online education, creating a demand for compliance solutions that can navigate various international standards and laws. This expansion is not only increasing the reach of EdTech companies but also diversifying the types of regulatory compliance services needed.

Challenge

Evolving Regulatory Landscapes

One of the major challenges in the EdTech regulatory compliance market is the continuously changing landscape of regulations across different regions. As digital education platforms become more prevalent, governments worldwide are updating and creating new laws to address the nuances of technology use in education.

Companies must stay informed and agile to comply with these ever-changing regulations, which can differ significantly from one country to another. This requires ongoing monitoring and adaptation, which can be resource-intensive. The rapid pace of technological advancements further complicates this challenge, as regulations often struggle to keep up with innovation.

Growth Factors

The EdTech market is experiencing significant growth, driven primarily by the increasing integration of technologies like artificial intelligence (AI) and machine learning across educational platforms. These technologies are enhancing personalized learning experiences and improving the efficacy of educational content, making education more accessible and engaging.

The rise of data analytics within EdTech is also pivotal, enabling educators to track progress and tailor educational strategies to individual needs more effectively. Moreover, the ongoing global shift towards digital and remote learning solutions, accelerated by the COVID-19 pandemic, continues to propel the market forward.

Emerging Trends

One of the most notable trends in the EdTech sector is the growing emphasis on mobile learning (M-learning) and immersive learning experiences through augmented reality (AR) and virtual reality (VR). These technologies are revolutionizing how educational content is delivered, providing interactive and engaging learning experiences that were not possible before.

Additionally, there is a significant push towards hybrid learning models, which blend traditional classroom settings with online resources to offer a more flexible learning environment. This trend is likely to persist as institutions seek to provide students with more adaptable learning options.

Impact of AI on EdTech

AI’s impact on the EdTech industry is profound, with AI-driven tools now common in personalized learning environments. These tools adapt learning materials to the needs of individual students, enhancing engagement and educational outcomes. AI technologies are also facilitating the automation of administrative tasks, allowing educational institutions to allocate more resources towards teaching and student support.

However, the deployment of AI in EdTech is not without challenges; it raises significant privacy and ethical concerns, particularly regarding the handling and security of student data. Ensuring these technologies are used responsibly and ethically is paramount to their successful integration into educational environments.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The analysis of key players in the EdTech Regulatory Compliance Market involves evaluating the major companies that influence the market dynamics through their products, services, innovations, and strategic initiatives. These players contribute significantly to shaping industry standards, regulatory frameworks, and technological advancements in the educational technology space

Instructure has been making waves in the EdTech space with its strategic acquisitions and product launches. In 2024, the company made a significant move by acquiring Parchment, the world’s largest academic credential management platform. This acquisition expands Instructure’s reach, allowing it to offer a comprehensive digital passport of achievement records for learners throughout their educational journey.

PowerSchool has been making significant strides in the K-12 EdTech market. In June 2024, the company announced it would be acquired by Bain Capital in a deal valued at $5.6 billion. This move to private ownership is expected to provide PowerSchool with more resources and flexibility to pursue its growth strategy.

List of Market Companies

- Workday, Inc.

- Instructure, Inc.

- OneTrust, LLC

- Blackboard Inc.

- Sai Global

- Microsoft Corporation

- PowerSchool

- Anthology Inc.

- Ellucian Company LLC

- Securly, Inc.

- Others

Updates From Key Players

- BYJU’S, the Indian EdTech unicorn, has been making significant strides in the global market. In January 2025, they announced a new initiative called “SafeLearn,” which aims to set industry standards for data protection and privacy in EdTech. This move came as BYJU’S expanded its presence in North America and Europe, where regulatory compliance is a top priorit.

- Blackboard, another giant in the EdTech space, made headlines in mid-2024 with its new “Compliance Assistant” tool. This AI-driven feature helps educational institutions navigate the complex landscape of EdTech regulations. It provides real-time updates on changing laws and offers customized compliance strategies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.7 Bn |

| Forecast Revenue (2034) | USD 17.7 Bn |

| CAGR (2025-2034) | 14.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Solution (Learning Management System (LMS) compliance tools, Data privacy and protection software, Others), Services), By Deployment Mode (Cloud-Based, On-Premises), By Compliance Type (Data Privacy and Protection, Accessibility Standards, Content and Curriculum Compliance, Cybersecurity Regulations, Ethical Compliance, Others), By End User (K-12 Education, Higher Education, Business Institutions) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Workday Inc., Instructure Inc. , OneTrust LLC, Blackboard Inc., Sai Global, Microsoft Corporation, PowerSchool, Anthology Inc., Ellucian Company LLC, Securly Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |