Global Dry-type Transformer Market Size, Share, And Industry Analysis Report By Technology (Cast Resin, Vacuum Pressure Impregnated), By Phase (Single, Three), By Voltage (Low, Medium, High), By Application (Industrial, Commercial, Utilities, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: December 2025

- Report ID: 168536

- Number of Pages: 215

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

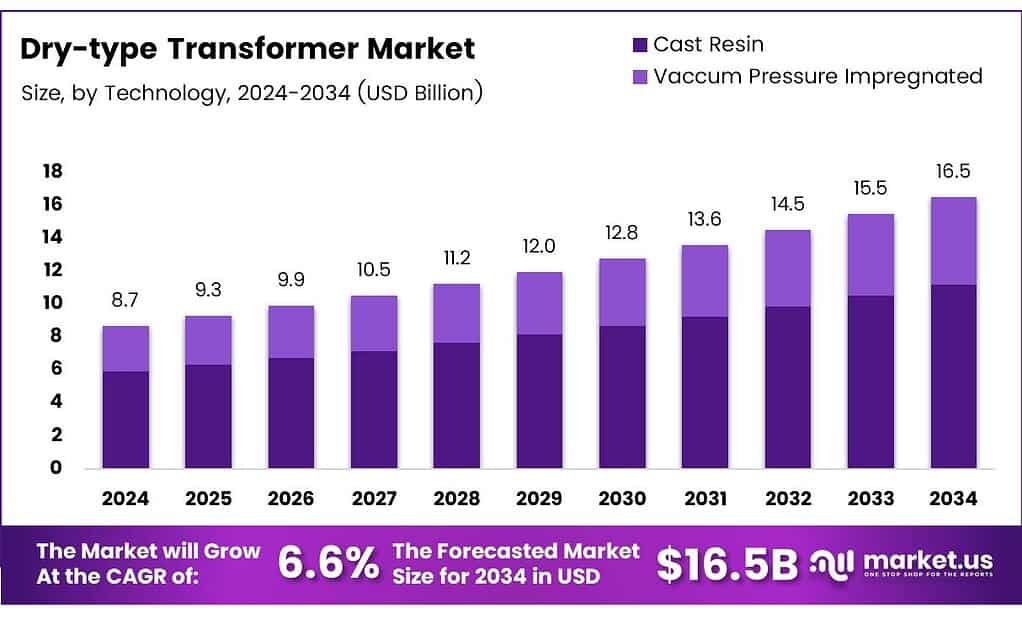

The Global Dry-type Transformer Market size is expected to be worth around USD 16.5 billion by 2034, from USD 8.7 billion in 2024, growing at a CAGR of 6.6% during the forecast period from 2025 to 2034.

The dry-type transformer market covers air-cooled electrical transformers without liquid insulation, used for safe indoor power distribution. These systems support voltage conversion across residential, commercial, and institutional facilities. Because they eliminate oil-related fire risks, they align well with modern building safety standards and urban electrification needs.

Dry-type transformers address rising safety expectations and space constraints in dense infrastructure environments. Consequently, demand grows steadily across hospitals, transit hubs, and residential complexes. Their low-maintenance design improves lifetime operating economics, helping asset owners reduce downtime and predictable replacement costs over long service cycles.

- A residential-grade dry-type voltage booster operates at 11,000/433 V with a 50 Hz three-phase design, ensuring stable indoor power distribution. Its copper core and double-winding structure enhance grid reliability, while natural air cooling supports safe operation up to 120°F. With around 99% efficiency and a weight of about 500 kg, these fire-safe, maintenance-free units are well-suited for hospitals and residential buildings.

Growth in the dry-type transformer market is supported by expanding electrification and increasing indoor load density. Moreover, healthcare infrastructure expansion and residential redevelopment accelerate adoption. Urban planners increasingly prefer non-flammable equipment, encouraging utilities and developers to specify dry-type units within distributed power and smart grid projects.

Key Takeaways

- The Global Dry-type Transformer Market is projected to grow from USD 8.7 billion in 2024 to USD 16.5 billion by 2034, registering a 6.6% CAGR.

- Cast Resin transformers dominate with a market share of 67.3% due to higher safety and indoor suitability.

- Three-phase dry-type transformers account for a leading share of 76.2%, driven by industrial and grid-level demand.

- Low-voltage transformers hold the largest share at 49.7%, supported by residential and commercial installations.

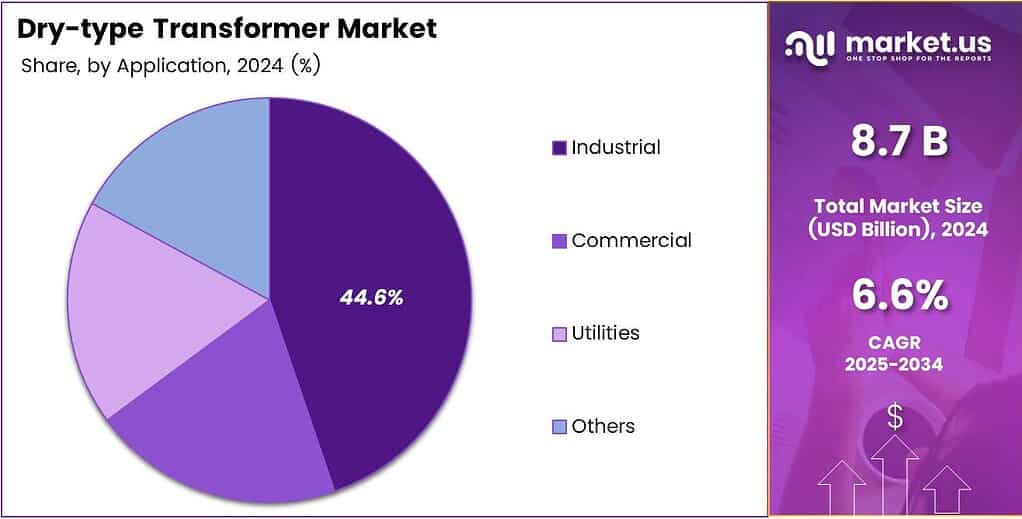

- The Industrial segment leads the market with a share of 44.6%, reflecting manufacturing and automation growth.

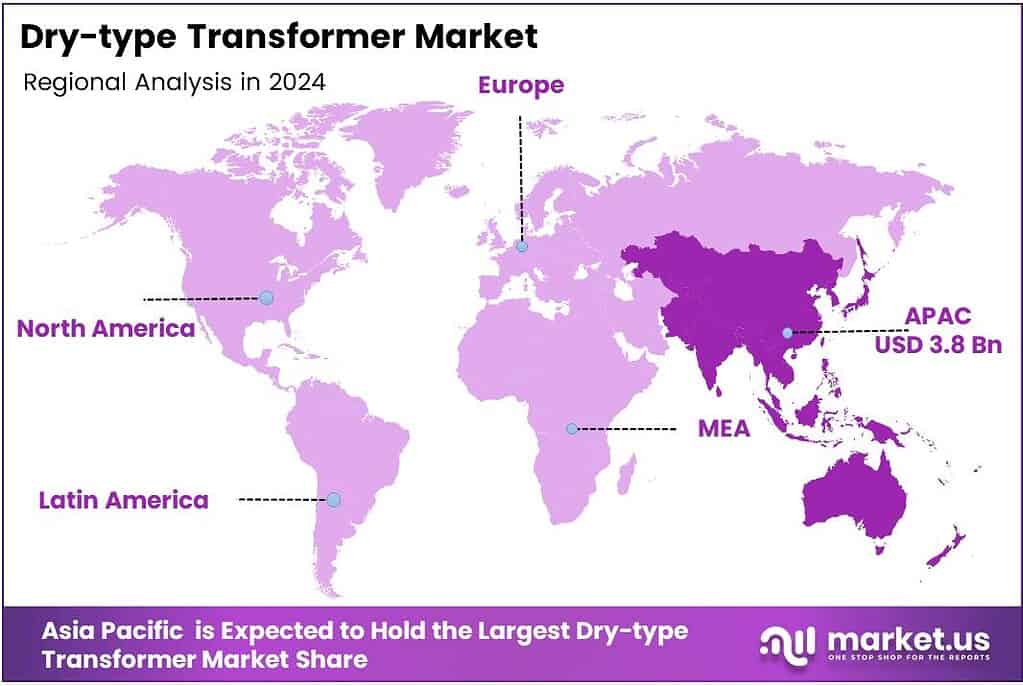

- Asia Pacific is the dominant regional market, accounting for a 43.9% share and valued at USD 3.8 billion in 2024

By Technology Analysis

Cast Resin dominates with 67.3% due to its safety, low maintenance, and strong indoor adoption.

In 2024, Cast Resin held a dominant market position in the By Technology Analysis segment of the Dry-type Transformer Market, with a 67.3% share. It is widely used in commercial buildings, metros, and hospitals because it is fire-resistant, moisture-proof, and environmentally safer. Moreover, its compact design supports urban infrastructure growth.

Vacuum Pressure Impregnated transformers continue to play an important role where cost control and proven reliability matter. They are preferred in controlled industrial environments due to their strong insulation and stable performance. Although adoption is slower, steady demand exists from manufacturing plants and legacy power systems.

By Phase Analysis

Three-phase dominates with 76.2% driven by industrial load demand and grid applications.

In 2024, Three Phase held a dominant market position in the By Phase Analysis segment of the Dry-type Transformer Market, with a 76.2% share. It supports high-capacity power distribution and is essential for factories, utilities, and data centers. Additionally, it improves efficiency and balances electrical loads.

Single-phase transformers serve smaller power needs in residential buildings, small offices, and light commercial areas. While limited in capacity, they remain essential for localized power distribution. Gradually, demand continues from rural electrification and low-load infrastructure projects.

By Voltage Analysis

Low Voltage dominates with 49.7% due to widespread use across residential and commercial facilities.

In 2024, Low Voltage held a dominant market position in the By Voltage Analysis segment of the Dry-type Transformer Market, with a 49.7% share. It is commonly installed in buildings, hospitals, and malls for safe power distribution. Its ease of installation further supports adoption. Medium Voltage transformers are essential for industrial plants and commercial complexes requiring efficient power transfer.

They offer a balance between capacity and safety. Adoption grows steadily as smart buildings and industrial automation expand. High-voltage transformers are mainly used by utilities and large infrastructure projects. Although limited in volume, they are critical for long-distance and high-load power networks, especially within grid modernization initiatives.

By Application Analysis

Industrial dominates with 44.6% supported by manufacturing expansion and stable power needs.

In 2024, Industrial held a dominant market position in the By Application Analysis segment of the Dry-type Transformer Market, with a 44.6% share. Industries favor dry-type units for safety, efficiency, and reduced fire risk. This trend strengthens with automation and plant expansion.

Commercial applications include offices, malls, airports, and hospitals, where safety and indoor installation matter. Demand continues to grow due to urban development and increased focus on energy-efficient buildings. Utilities rely on dry-type transformers for substations, renewable integration, and grid upgrades.

Their low maintenance and environmental safety support reliability-focused utility operations. Other applications, such as transportation hubs and institutional facilities, contribute niche demand. Gradually, growth comes from infrastructure modernization and public-sector construction projects.

Key Market Segments

By Technology

- Cast Resin

- Vacuum Pressure Impregnated

By Phase

- Single

- Three

By Voltage

- Low

- Medium

- High

By Application

- Industrial

- Commercial

- Utilities

- Others

Emerging Trends

Shift Toward Compact, Digital, and Eco-Friendly Power Equipment

One major trend in the dry-type transformer market is the move toward compact and space-saving designs. Manufacturers are developing smaller transformers with better thermal performance, making installation easier in crowded urban spaces. Digital monitoring is another emerging trend. Modern dry-type transformers now include sensors for temperature, load, and fault detection.

- This helps operators monitor performance in real time and reduce unexpected failures. Eco-friendly materials are also gaining attention. The Global renewable power capacity is projected to increase by about 4,600 GW between 2025 and 2030, which is roughly double the capacity added in the previous five years.

New insulation systems with lower environmental impact are being adopted to meet sustainability goals. These designs reduce emissions and support cleaner power systems. Finally, customization is increasing. End users now demand transformers tailored to specific voltage, space, and safety needs. This trend supports innovation and long-term competitiveness in the dry-type transformer market.

Drivers

Rising Focus on Electrical Safety and Fire Prevention Drives Adoption

The dry-type transformer market is mainly driven by the growing need for safe electrical equipment in buildings and industries. Unlike oil-filled transformers, dry-type units do not use flammable liquids. This makes them safer for places such as hospitals, data centers, metro stations, schools, and commercial buildings. Fire safety rules in many countries now prefer equipment with low fire risk, which supports steady demand for dry-type transformers.

Urbanization and construction activities also play a strong role. As more high-rise buildings, malls, and offices are built, safe indoor power distribution becomes necessary. Dry-type transformers can be installed close to load centers, which reduces power losses and improves efficiency.

Another driver is the expansion of renewable energy and smart grid projects. Solar rooftops, wind farms, and EV charging stations require reliable and compact transformers. Many utilities and industries prefer dry-type models because they need less maintenance and work well in dusty or humid conditions.

Restraints

Higher Initial Cost Compared to Oil-Filled Units Limits Adoption

One major restraint in the dry-type transformer market is the higher upfront cost. Dry-type transformers generally cost more than conventional oil-filled transformers of the same power rating. This price difference can discourage buyers in cost-sensitive markets, especially in developing regions.

Limited overload capacity is another challenge. Oil-filled transformers handle short-term overloads better due to effective heat dissipation. Dry-type transformers have stricter temperature limits, which can be a concern for heavy industrial applications or unstable power environments.

Size and weight can also be constraints at higher voltage levels. While dry-type transformers work well for low and medium voltage, they become bulkier at higher ratings. This limits their use in large utility-scale projects. In some regions, lack of awareness and technical familiarity also slow adoption.

Growth Factors

Expansion of Smart Cities and Green Buildings Creates New Opportunities

Growth opportunities for the dry-type transformer market are strongly linked to smart city and green building projects. Governments are promoting energy-efficient and low-risk electrical systems in new infrastructure. Dry-type transformers fit well with green building standards because they reduce fire risk, pollution, and maintenance needs.

Rapid growth in data centers is another key opportunity. Data centers require reliable power, low downtime, and high safety. Dry-type transformers are widely used inside data halls and substations to support critical loads. Industrial electrification also opens new doors.

Manufacturing plants are upgrading old electrical systems to improve safety and reduce operational risks. Dry-type transformers support a clean and stable power supply, making them suitable for modern factories. Rising investment in metro rail, airports, and electric vehicle charging networks further supports long-term growth opportunities.

Regional Analysis

Asia Pacific Dominates the Dry-type Transformer Market with a Market Share of 43.9%, Valued at USD 3.8 Billion

The Asia Pacific region leads the dry-type transformer market due to rapid urbanization, grid expansion, and rising electricity demand across developing economies. In 2024, the region accounted for a dominant 43.9% share, with the market valued at USD 3.8 billion, supported by heavy investments in renewable energy and industrial infrastructure. Strong government focus on power reliability, smart substations, and safety-driven transformer adoption continues to drive steady demand growth.

North America shows stable growth supported by aging grid modernization and rising demand from commercial buildings, healthcare facilities, and data centers. The region benefits from stricter fire-safety regulations and energy efficiency standards, increasing preference for dry-type transformers. Ongoing investments in renewable integration and distribution upgrades further support market expansion across utilities and industrial segments.

Europe’s market growth is closely linked to stringent environmental norms and strong adoption of low-emission electrical equipment. High investments in offshore wind, urban infrastructure renewal, and energy-efficient building retrofits sustain demand. The region also emphasizes transformer safety in dense urban zones, driving uptake across transport networks and public utility projects.

The U.S. market is driven by strong investments in power distribution upgrades, data centers, and electric vehicle charging infrastructure. Strict safety codes and energy efficiency regulations support wider adoption of dry-type transformers across commercial and institutional applications. Continued focus on grid resilience and clean energy integration maintains steady market momentum.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Below is an analyst viewpoint written in a professional market-research tone, focused strictly on the first four widely recognized key players in the global Dry-type Transformer Market in 2024, without citing external sources or adding any new company names.

Schneider Electric continues to play a critical role in shaping the dry-type transformer landscape through its strong focus on energy efficiency, building electrification, and safety-driven design. In 2024, the company’s dry-type portfolio aligns closely with rising adoption in commercial buildings, healthcare infrastructure, and data centers. Its emphasis on smart monitoring, compliance-ready insulation systems, and low-loss performance strengthens demand across regulated and urbanized markets.

Siemens maintains a solid presence in the dry-type transformer market by leveraging its deep engineering expertise and grid modernization capabilities. During 2024, Siemens’ dry-type transformers will remain well-positioned for industrial automation, renewable energy interconnections, and transport infrastructure. The company’s ability to integrate transformers with digital power systems supports utilities and industries seeking safer, maintenance-friendly alternatives to oil-filled units.

ABB holds a strong market position due to its wide application coverage and emphasis on sustainability-led power solutions. In 2024, ABB’s dry-type transformers are increasingly used in metro rail projects, smart cities, and renewable-heavy grids where fire safety and environmental compliance are critical. Its focus on compact design and thermal stability supports deployment in space-constrained urban settings.

Eaton continues expanding its relevance in the dry-type transformer market through demand from data centers, commercial facilities, and institutional buildings. In 2024, Eaton benefits from growing investments in power reliability and electrical safety standards. Its dry-type transformers are preferred for indoor installations, driven by durability, predictable lifecycle performance, and alignment with broader power-management solutions.

Top Key Players in the Market

- Schneider Electric

- Hammond Power Solution

- Siemens

- Eaton

- GE

- Hyosung Heavy Industries

- Kirloskar Electric Co. Ltd.

- Voltamp Transformer Limited

- ABB

- Bharat Heavy Electricals Limited

Recent Developments

- In 2025, Schneider Electric continues to list and promote dry-type transformers under its product categories, the Dry-Type Transformers range for various voltage and application needs. Its subsidiary Schneider Electric Infrastructure Ltd (SEIL) has announced a capacity expansion for transformer manufacturing.

- In 2025, Siemens Energy announced a large-scale investment plan: USD 2.3 billion to expand its global network of transformer and switchgear factories by 2028. The push ties with broader grid-infrastructure investment globally, for instance, expanding capacity to meet rising demand for large power transformers (LPTs).

Report Scope

Report Features Description Market Value (2024) USD 8.7 billion Forecast Revenue (2034) USD 16.5 billion CAGR (2025-2034) 6.6% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Technology (Cast Resin, Vacuum Pressure Impregnated), By Phase (Single, Three), By Voltage (Low, Medium, High), By Application (Industrial, Commercial, Utilities, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Schneider Electric, Hammond Power Solution, Siemens, Eaton, GE, Hyosung Heavy Industries, Kirloskar Electric Co. Ltd., Voltamp Transformer Limited, ABB, Bharat Heavy Electricals Limited Customization Scope Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Dry-type Transformer MarketPublished date: December 2025add_shopping_cartBuy Now get_appDownload Sample

Dry-type Transformer MarketPublished date: December 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Schneider Electric

- Hammond Power Solution

- Siemens

- Eaton

- GE

- Hyosung Heavy Industries

- Kirloskar Electric Co. Ltd.

- Voltamp Transformer Limited

- ABB

- Bharat Heavy Electricals Limited

Our Clients

- 168536

- December 2025