Quick Navigation

Market Overview

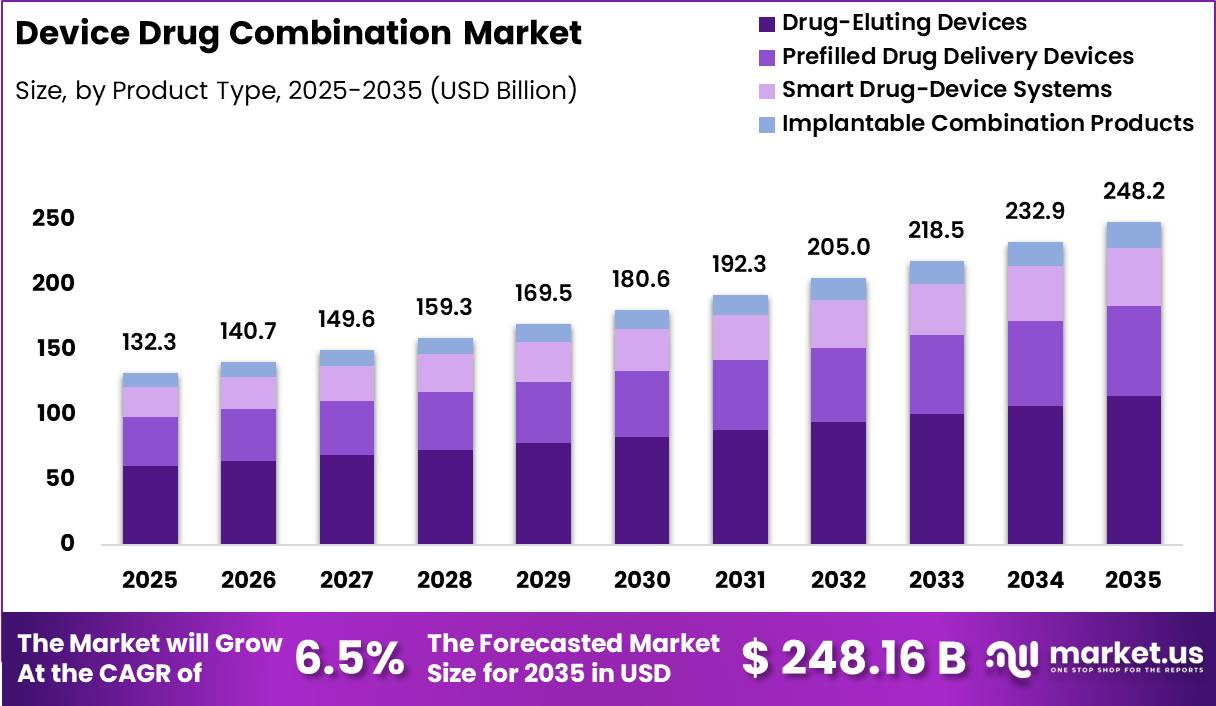

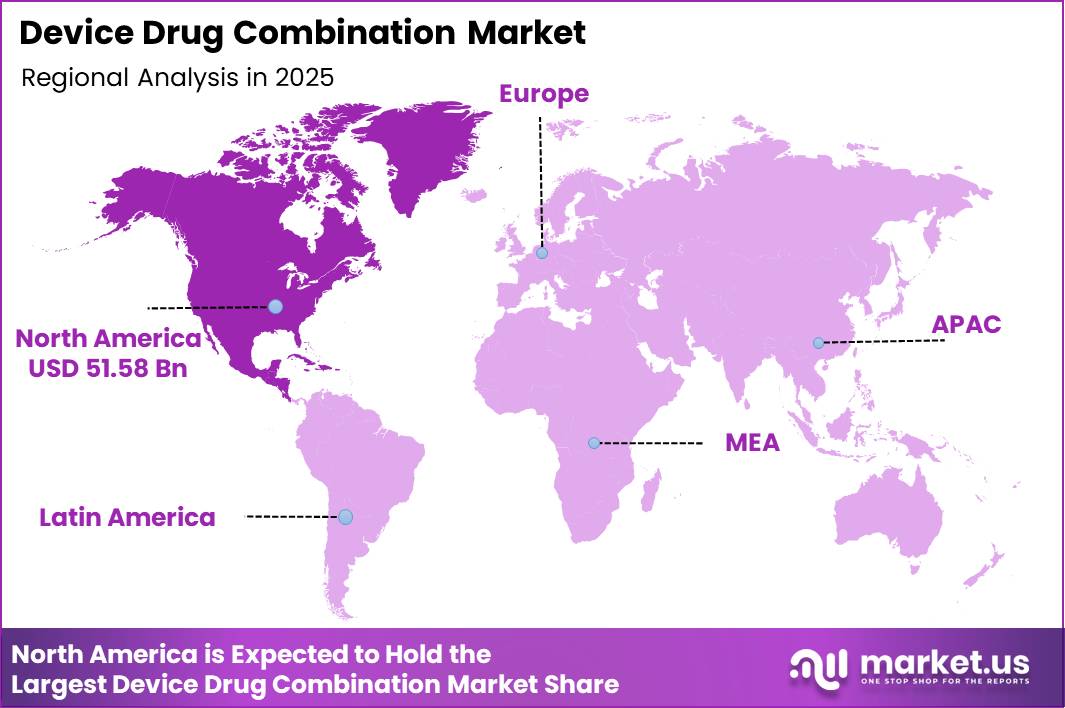

Global Device Drug Combination Market size is expected to be worth around US$248.16 Billion by 2035 from US$132.30 Billion in 2025, growing at a CAGR of 6.5% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 39.00% share with a revenue of US$51.59 Billion.

The Device-Drug Combination Market comprises regulated healthcare products that integrate a medical device with a pharmaceutical or biological component to achieve a unified therapeutic effect.

According to the U.S. Food and Drug Administration (FDA), a combination product includes entities in which a drug and device are physically or chemically combined, co-packaged, or separately packaged but labelled for use together, as defined under 21 CFR §3.2. Common examples include drug-eluting coronary stents, prefilled injection systems, insulin delivery pens, inhalers, and transdermal drug-delivery patches.

Regulatory oversight is coordinated by the FDA’s Office of Combination Products, which assigns a lead review centre based on the product’s primary mode of action while integrating requirements from drug, device, and biologics frameworks.

FDA documentation indicates that combination products represent approximately 30% of novel therapeutic submissions reviewed in recent years, reflecting rapid clinical adoption across cardiovascular disease, diabetes management, oncology, and respiratory care.

In the European Union, combination products are jointly regulated under medical device and medicinal product legislation, with scientific coordination provided by the European Medicines Agency (EMA). The EMA’s operational guidance emphasises safety, performance, and post-market surveillance alignment for products incorporating both medicinal and device constituents.

The growing prevalence of chronic diseases, such as diabetes, affecting over 537 million adults globally, according to the World Health Organisation, continues to support demand for integrated delivery systems that enhance dosing accuracy, adherence, and patient outcomes.

Overall, the Device-Drug Combination Market plays a critical role in advancing precision therapy, patient-centric design, and next-generation treatment modalities within regulated healthcare systems worldwide.

Key Takeaways

- Market Size: The Global Device Drug Combination Market size was US$132.3 billion in 2025. The market is estimated to grow to US$248.16 billion by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 6.5%.

- Product Type: Drug-Eluting Devices has the largest market share, accounting for 46% of total sales.

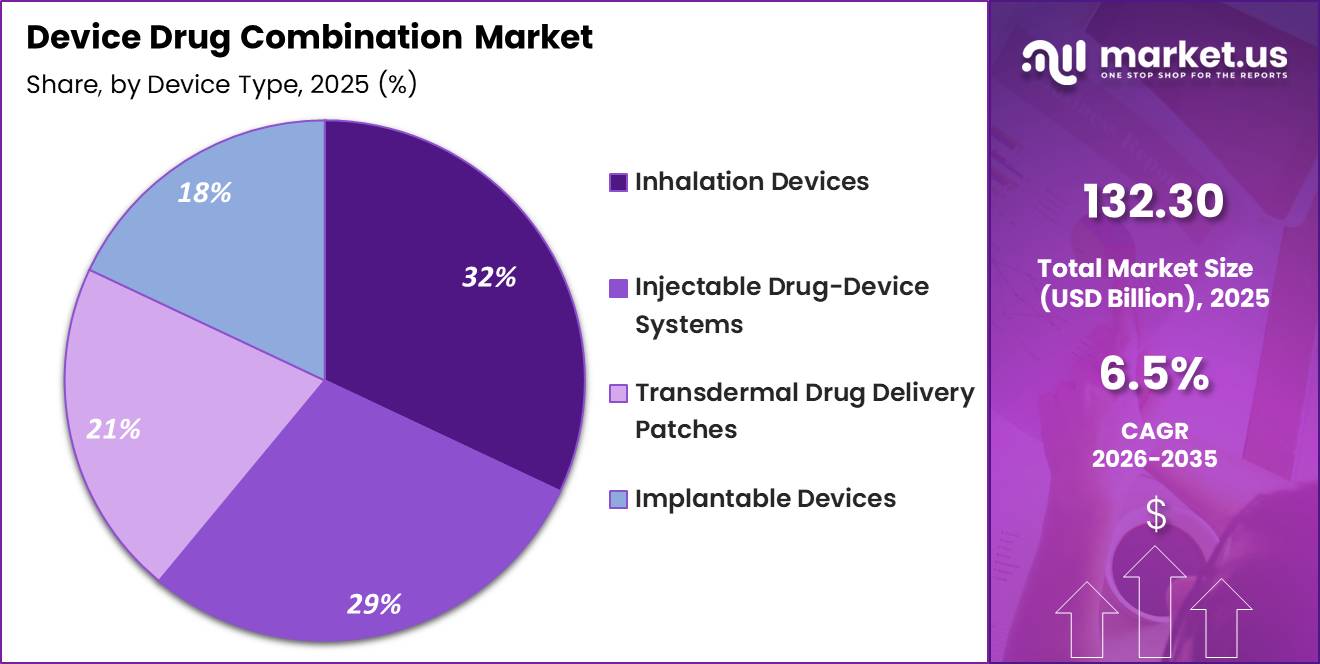

- Device Type: Inhalation Devices dominate the segment, accounting for 32% of total revenue.

- Therapeutic Area: Cardiovascular Diseases leads the segment, accounting for 26% of total revenue.

- End User: Hospitals lead the segment, accounting for 44% of total revenue.

- Technology: Controlled Drug Release Systems dominate the segment, accounting for 41% of total revenue.

- Distribution Channel: Hospital Procurement dominates the segment, accounting for 52% of total revenue.

- Regional: North America is the dominant regional market, accounting for 39% of global sales.

Product Type Analysis

The Drug–Device Combination Market by product type is led by Drug-Eluting Devices, which dominate with a 46.00% market share in 2025. Their leadership is driven by strong clinical evidence supporting localised drug delivery with reduced systemic side effects, particularly in cardiovascular stents, orthopaedic implants, and oncology-related interventions. These products enhance therapeutic efficacy while lowering complication and restenosis rates, making them widely adopted in hospital-based procedures.

Prefilled Drug Delivery Devices account for 28.00% of the market, supported by growing demand for convenience, dosing accuracy, and reduced contamination risk. Their use is expanding rapidly in biologics, vaccines, and chronic disease management, especially in outpatient and home care settings.

Smart Drug-Device Systems, holding 18.00%, represent a high-growth segment due to the integration of sensors, connectivity, and digital adherence monitoring. These systems are increasingly used in diabetes, respiratory, and neurology care, aligning with the shift toward personalised medicine.

Implantable Combination Products, though smaller at 8.00%, address complex long-term therapies and benefit from advances in biomaterials and sustained-release technologies, supporting gradual adoption in speciality therapeutic areas.

Device Type Analysis

By device type, Inhalation Devices lead the Drug–Device Combination Market with a 32.00% market share in 2025, driven by the rising prevalence of respiratory disorders and the effectiveness of pulmonary drug delivery. These devices enable rapid onset of action and high patient compliance, particularly in asthma, COPD, and emerging biologic inhalation therapies.

Injectable Drug–Device Systems follow closely with 29.00%, reflecting their critical role in biologics, vaccines, oncology drugs, and autoimmune treatments. Auto-injectors and pen injectors are widely adopted due to ease of use, safety features, and compatibility with self-administration models.

Transdermal Drug Delivery Patches, accounting for 21.00%, benefit from steady demand in pain management, hormonal therapies, and neurological conditions. Their non-invasive nature and ability to deliver controlled doses over extended periods improve adherence and reduce dosing variability.

Implantable Devices, holding 18.00%, support long-term and precision therapies, particularly in cardiovascular and neurology applications. Growth in this segment is reinforced by technological improvements in miniaturisation, biocompatibility, and extended drug-release mechanisms.

Therapeutic Area Analysis

Therapeutic area segmentation shows Cardiovascular Diseases as the largest contributor, capturing 26.00% of the market in 2025. Drug–device combinations such as drug-eluting stents and implantable infusion systems are widely used to reduce restenosis and improve long-term patient outcomes, reinforcing this segment’s dominance.

Oncology represents a significant and rapidly expanding segment, driven by localised chemotherapy delivery systems, implantable drug reservoirs, and precision-targeted therapies that minimise systemic toxicity.

Diabetes continues to be a core growth area due to widespread adoption of insulin pumps, smart injectors, and continuous drug delivery platforms that support glycemic control and patient self-management.

Respiratory Diseases benefit from advanced inhalation systems and combination therapies that improve lung deposition and treatment adherence, particularly in chronic conditions.

Neurology, though comparatively smaller, is gaining traction through implantable pumps and controlled-release systems for pain management and neurodegenerative disorders. Collectively, these therapeutic areas reflect the market’s shift toward targeted, long-term, and patient-centric treatment strategies.

End User Analysis

Among end users, Hospitals dominate the Drug–Device Combination Market with a 44.00% market share in 2025. This leadership is supported by high procedural volumes, access to advanced infrastructure, and the concentration of complex combination therapies requiring clinical oversight. Hospitals also serve as primary adopters of implantable and high-value drug–device products.

Ambulatory Surgical Centres (ASCs) are gaining momentum as cost-effective alternatives for minimally invasive procedures. Their growing procedural capabilities and shorter patient stays make them increasingly attractive for injectable and short-term combination therapies.

Homecare Settings represent a fast-growing segment due to rising chronic disease prevalence and the shift toward self-administration. Devices such as prefilled injectors, smart delivery systems, and wearable pumps support this trend by enabling safe and effective treatment outside traditional facilities.

Speciality Clinics play a critical role in oncology, cardiology, and neurology care, where specialised drug–device combinations are frequently prescribed. Overall, end-user segmentation highlights decentralisation of care and increasing reliance on user-friendly, outpatient-compatible combination products.

Technology Analysis

From a technology perspective, Controlled Drug Release Systems lead the market with a 41.00% share in 2025. These systems are essential for maintaining therapeutic drug levels over extended periods, improving efficacy while reducing dosing frequency and side effects. They are widely used in cardiovascular implants, transdermal patches, and implantable pumps.

Targeted Drug Delivery Technologies form a key growth segment, focusing on directing drugs precisely to diseased tissues. This approach enhances treatment outcomes, particularly in oncology and neurology, by minimising off-target effects and improving therapeutic precision.

Nanotechnology-Based Systems, though smaller in current share, are emerging as a transformative technology. Nanocarriers, nanoparticles, and nano-enabled implants enable enhanced bioavailability, controlled release, and cellular-level targeting. Adoption is supported by ongoing innovation in materials science and pharmaceutical engineering.

Together, these technologies illustrate the market’s evolution toward precision medicine, sustained delivery, and improved patient safety, positioning advanced delivery platforms as a central driver of long-term market expansion.

Distribution Channel Analysis

In distribution channels, Hospital Procurement dominates with a 52.00% market share in 2025, reflecting hospitals’ role as primary purchasers of high-cost and procedure-based drug–device combinations. Centralised procurement systems, long-term supplier contracts, and regulatory oversight reinforce this channel’s leadership.

Speciality Pharmacies account for a growing portion of distribution, particularly for complex therapies requiring cold-chain management, patient education, and adherence monitoring. Their role is critical in oncology, neurology, and biologics-based combination products.

Online Pharmacies are gradually expanding due to increased digital healthcare adoption and demand for home-delivered therapies, especially for chronic disease management and refill-based combination products.

Direct Manufacturer Sales remain important for high-value implantable systems and customised solutions, allowing manufacturers to maintain clinical engagement and training support. Overall, distribution channel segmentation reflects a balance between institutional dominance and emerging decentralised access models driven by digital health and home care trends.

Key Market Segments

By Product Type

- Drug-Eluting Devices

- Prefilled Drug Delivery Devices

- Smart Drug-Device Systems

- Implantable Combination Products

By Device Type

- Inhalation Devices

- Injectable Drug-Device Systems

- Transdermal Drug Delivery Patches

- Implantable Devices

By Therapeutic Area

- Cardiovascular Diseases

- Oncology

- Diabetes

- Respiratory Diseases

- Neurology

By End User

- Hospitals

- Ambulatory Surgical Centres

- Homecare Settings

- Specialty Clinics

By Technology

- Controlled Drug Release Systems

- Targeted Drug Delivery

- Nanotechnology-Based Systems

By Distribution Channel:

- Hospital Procurement

- Specialty Pharmacies

- Online Pharmacies

- Direct Manufacturer Sales

Driver

Novel therapy pipeline converting into device-led launches

A key driver of combination products is the continuous flow of new speciality and rare disease therapies that increasingly require or transition toward integrated delivery systems for usability, precision, and differentiation.

In 2025, the FDA’s Centre for Drug Evaluation and Research approved 46 novel drugs, following 50 approvals in 2024, with more than half designated as orphan drugs, highlighting strong momentum in biologics and targeted therapies where delivery design is commercially critical.

Even when these therapies launch in simpler formats, they often evolve toward device-enabled delivery through lifecycle strategies that expand into home or outpatient settings and improve patient adherence.

This creates a pipeline-coupled demand structure in which each new therapy can generate requirements for customised packaging, injection devices, human factors validation, and post-market support systems.

As a result, value creation extends beyond the drug itself into engineering services, device design transfer, validation workflows, and long-tail consumables, making the combination-product ecosystem more resilient and structurally growth-oriented than markets driven only by installed-base replacement.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 and biologic self-injection scale-up | +2.1% | North America core, EU, Japan, China urban corridors | Short term (≤ 2 years) |

| Regulatory convergence for combination products | +1.0% | North America core, EU, UK spill-over | Medium term (2-4 years) |

| Sterile fill-finish and device assembly capacity build-out | +1.3% | US and EU demand centres, India and broader APAC manufacturing corridors | Short term (≤ 2 years) |

| Shift to home-care delivery formats | +1.4% | North America core, Western Europe, and developed APAC | Medium term (2-4 years) |

| Higher-value device mix: wearable, connected, adherence-enabled | +0.9% | North America core, EU, selective APAC adoption | Medium term (2-4 years) |

| Novel therapy pipeline converting into device-led launches | +1.1% | US launch market, EU follow-on, global speciality care spill-over | Medium term (2-4 years) |

Challenegs

Dual-Framework Compliance Load

Device–drug combination products face a persistent structural compliance burden because they must satisfy overlapping regulatory systems for drugs and medical devices simultaneously, creating coordination complexity rather than outright market barriers.

Regulatory frameworks such as the FDA’s Office of Combination Products manage jurisdiction assignment and coordinated review across centres, while in the EU, integral and co-packaged products must comply with MDR requirements for the device component alongside full medicinal product dossiers.

This dual-track system significantly increases development and documentation workload across design controls, usability validation, extractables and leachables studies, complaint handling systems, and pharmacovigilance integration.

In practical terms, this adds an estimated 6–12 months to late-stage development cycles for more complex delivery systems and increases program management and quality assurance costs by 8–14% per asset.

As a result, companies are increasingly shifting toward integrated regulatory platforms with shared technical files, standardised change-control processes, and earlier cross-agency engagement to reduce rework risk and improve lifecycle efficiency across drug-device combination portfolios.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Dual-framework compliance load | -1.4% | North America core, EU regulatory hubs | Medium term (2-4 years) |

| Notified body review congestion | -1.1% | EU regulatory hubs, UK spillover markets | Medium term (2-4 years) |

| Sterile injectable component tightness | -1.6% | U.S. injectable base, EU fill-finish clusters, APAC export corridors | Medium term (2-4 years) |

| Biomanufacturing talent deficits | -1.2% | U.S. biologics centres, EU advanced therapy hubs, LMIC expansion zones | Long term (≥ 4 years) |

| Human-factors redesign cycles | -0.9% | Home-care markets in North America, EU5, Japan | Short term (≤ 2 years) |

| Supplier traceability fragmentation | -1.0% | APAC logistics corridors, North America core, EU sourcing networks | Medium term (2-4 years) |

Opportunity

IV-to-SC Site-of-Care Switch

A key future growth opportunity in drug-device combinations is the deliberate shift of therapies from intravenous administration in infusion centres to subcutaneous self-administration or home-based delivery. This transition is not just a convenience upgrade but a structural reconfiguration of care delivery, reimbursement flow, and provider economics, as more biologics move from medical benefit billing toward pharmacy benefit models.

Advances in autoinjectors and wearable injectors are enabling this migration across high-cost therapeutic areas such as immunology, neurology, oncology, supportive care, and neurodegeneration.

Converting even 10–15% of infusion-eligible patients to subcutaneous formats can significantly reduce administration costs per treatment episode, eliminate chair time, and improve patient convenience while also supporting higher treatment persistence of around 3–5%.

The strongest adoption potential is in the U.S., EU, and Japan, where payer pressure on hospital-based biologics is increasing, and home-administration infrastructure is already well developed, making this shift a strategic opportunity to capture value through improved adherence, reduced site-of-care costs, and expanded patient access.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Obesity platform conversion | +2.4% | North America core, EU5, Gulf, urban APAC | Short term (≤ 2 years) |

| IV-to-SC site-of-care switch | +2.1% | North America, the EU, and Japan | Short term (≤ 2 years) |

| Smart connected injectors | +1.6% | North America, the EU, Korea, and Japan | Medium term (2-4 years) |

| Wearable large-volume biologics | +1.9% | U.S., Germany, Nordics, China tier-1 | Medium term (2-4 years) |

| Dual-chamber lifecycle roll-ups | +1.3% | U.S., EU, Japan, Singapore | Medium term (2-4 years) |

| Microneedle adjacency expansion | +1.5% | APAC emerging, U.S., UK, selected EU | Long term (≥ 4 years) |

Restraint

Reimbursement and adoption friction

The final restraint is commercial rather than technical: many device drug combinations offer clinically meaningful convenience but still struggle to secure rapid reimbursement uplift when the economic value proposition is split across pharmacy budgets, medical-benefit billing, and site-of-care savings that accrue to different stakeholders.

In practice, this means manufacturers often face 12–24 months of post-approval market access work to prove that higher unit prices are offset by lower administration burden, reduced nursing time, fewer dosing errors, or better adherence, and that evidence bar rises further in Europe where HTA scrutiny and hospital procurement discipline are tighter.

The modelled impact is a 1.1 % point drag on CAGR because premium delivery formats see slower than expected penetration, gross-to-net concessions widen by 3–6 % points in competitive categories, and providers defer switching from standard formulations until real-world outcomes data or workflow savings are strong enough to justify formulary disruption.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pathway complexity | -2.1% | North America core, EU, Japan | Medium term (2-4 years) |

| MDR Article 117 bottlenecks | -1.6% | EU core, UK-linked supply chains | Short term (≤ 2 years) |

| Injectable component shortages | -1.9% | U.S., EU, India, APAC export hubs | Short term (≤ 2 years) |

| Cost inflation and tariffs | -1.4% | U.S.-China corridor, EU, global OEM bases | Medium term (2-4 years) |

| Quality remediation risk | -1.3% | North America core, EU, and contract manufacturing hubs | Medium term (2-4 years) |

| Reimbursement and adoption friction | -1.1% | U.S., EU5, selective APAC premium markets | Long term (≥ 4 years) |

Regional Analysis

In 2025, North America led the Device–Drug Combination Market, accounting for over 39.00% of global share and generating approximately US$ 51.59 billion in revenue. This dominance is primarily supported by the strong presence of advanced healthcare infrastructure in the United States, high adoption of innovative combination products, and a well-established regulatory framework for combination therapies.

Widespread use of drug-eluting cardiovascular devices, smart injectors, and biologics-device platforms, along with high healthcare spending per capita, continues to reinforce regional leadership.

Europe represents the second-largest regional market, driven by aging demographics, rising chronic disease burden, and strong uptake of implantable and controlled-release drug–device products. Countries such as Germany, France, and the UK benefit from universal healthcare systems and consistent investment in medical technology innovation.

The Asia-Pacific region is the fastest-growing, supported by expanding patient populations, improving access to healthcare, and rising adoption of combination therapies in China, Japan, and India. Growth is further accelerated by increasing local manufacturing and government healthcare initiatives.

Meanwhile, Latin America and the Middle East & Africa remain emerging markets, where gradual improvements in healthcare infrastructure and regulatory harmonisation are expected to drive steady long-term adoption of device–drug combination technologies.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Competitive advantage in the global drug-device combination market is achieved through integrated capabilities in pharmaceutical and medical device development, as well as regulatory expertise in navigating approval pathways for combination products under FDA and EMA frameworks.

Additionally, having a robust manufacturing infrastructure that supports the production of precision drug-eluting and controlled-release devices at a commercial scale is essential.

Leading manufacturers prioritise several strategic initiatives, including continued investment in the development of smart drug-device systems that integrate digital connectivity and dosing monitoring capabilities.

They also focus on expanding targeted and nanotechnology-based drug delivery platforms for applications in oncology and chronic disease management, alongside developing transdermal and inhalation devices that enhance patient adherence by simplifying administration.

Strong procurement relationships with hospitals, coupled with investments in speciality pharmacy and direct manufacturer sales channels, serve as critical competitive differentiators for manufacturers catering to both acute hospital-based and chronic homecare treatment pathways across cardiovascular, oncology, diabetes, and respiratory disease categories.

Top Key Players

- Medtronic

- Johnson & Johnson

- Becton Dickinson and Company

- Boston Scientific

- Abbott Laboratories

- Bayer AG

- Novartis AG

- Pfizer Inc.

- Roche Holding AG

- Merck & Co.

- AstraZeneca

- 3M Health Care

- GE HealthCare

- Siemens Healthineers

- Terumo Corporation

- Other Key Players

Recent Developments

- In January 2026, Medtronic launched an expanded line of drug-eluting cardiovascular devices featuring enhanced controlled-release coating technology. This new line is aimed at hospital cardiology departments that are seeking to improve long-term patient outcomes in coronary intervention procedures.

- In February 2026, Becton Dickinson and Company introduced a new smart prefilled drug delivery system that integrates digital dose tracking capabilities. This system is targeted at home care and speciality clinic settings for managing chronic disease treatment regimens that require adherence monitoring.

- In March 2026, Boston Scientific expanded its portfolio of targeted drug delivery devices for oncology applications. This expansion is designed for hospital and ambulatory surgical centre buyers who are looking for localised therapeutic delivery systems that minimise systemic side effects.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 132.30 Billion |

| Forecast Revenue (2035) | US$ 248.16 Billion |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Drug-Eluting Devices, Prefilled Drug Delivery Devices, Smart Drug-Device Systems, Implantable Combination Products), By Device Type (Inhalation Devices, Injectable Drug-Device Systems, Transdermal Drug Delivery Patches, Implantable Devices), By Therapeutic Area (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology), By End User (Hospitals, Ambulatory Surgical Centers, Homecare Settings, Specialty Clinics), By Technology (Controlled Drug Release Systems, Targeted Drug Delivery, Nanotechnology-Based Systems), By Distribution Channel (Hospital Procurement, Specialty Pharmacies, Online Pharmacies, Direct Manufacturer Sales) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Medtronic, Johnson & Johnson, Becton Dickinson and Company, Boston Scientific, Abbott Laboratories, Bayer AG, Novartis AG, Pfizer Inc., Roche Holding AG, Merck & Co., AstraZeneca, 3M Health Care, GE HealthCare, Siemens Healthineers, Terumo Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |