Quick Navigation

Report Overview

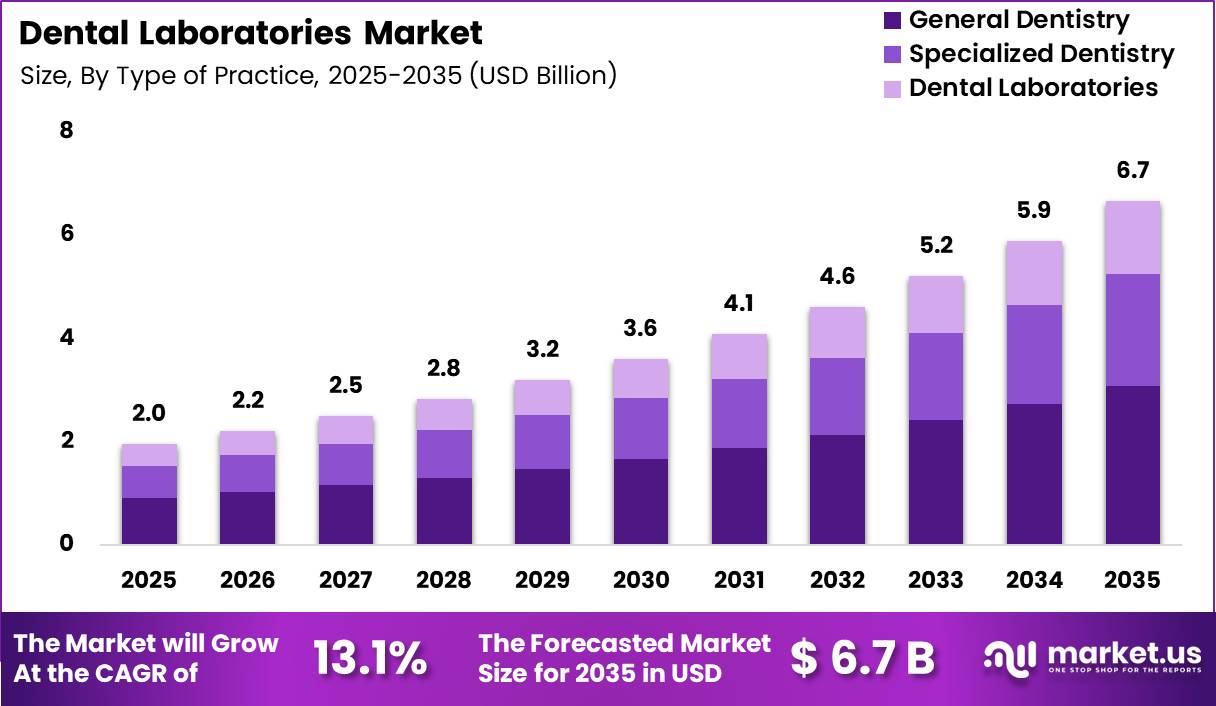

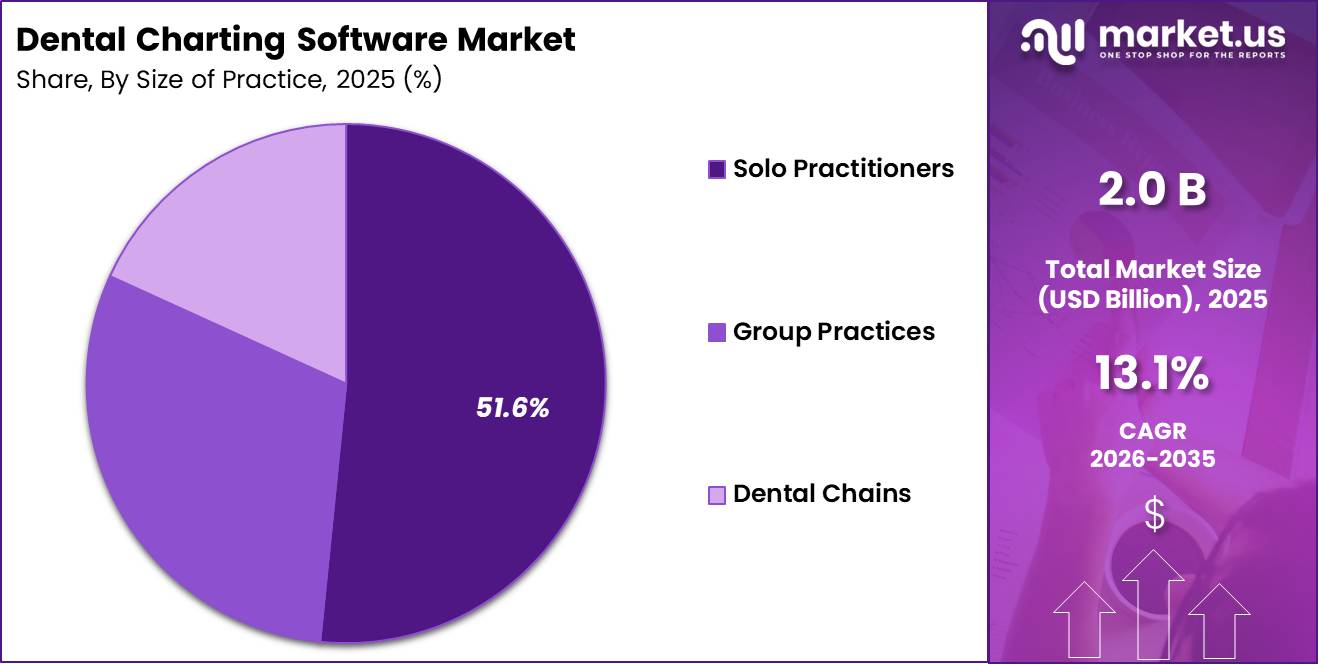

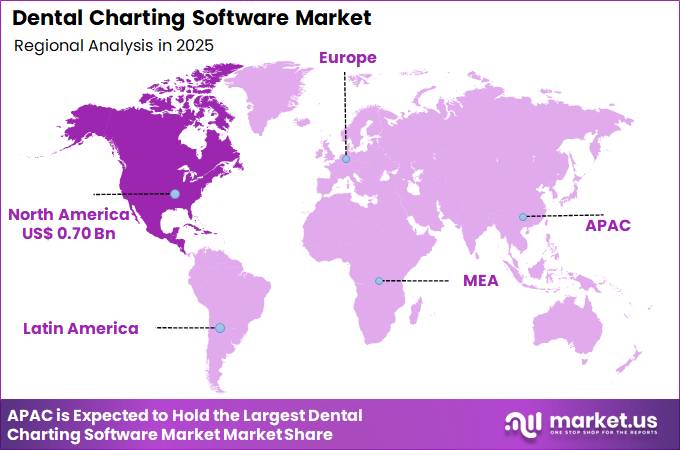

Global Dental Charting Software Market size is expected to be worth around US$ 6.7 Billion by 2035 from US$ 2.0 Billion in 2025, growing at a CAGR of 13.1% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 35.80% share with a revenue of US$ 0.70 Billion.

Dental charting software helps dental professionals digitally track, record, and manage patients’ oral health data, including history, diagnoses, procedures, and treatment plans, using features like tooth numbering, visual charts, and annotations. This shift from paper-based to electronic health records (EHR) in dentistry boosts practice efficiency, reduces errors, and improves care delivery.

The global market for dental software, encompassing charting tools, shows strong growth driven by digitalization in healthcare and demand for better patient care. In the U.S., adoption of electronic dental records reached 52% by 2012 for clinical support, with higher rates among younger dentists, females, and group practices, though barriers like cost and usability persist. A 2024 American Dental Association survey indicated nearly 74% of individuals seek digital health services such as electronic charting for oral health management.

Integration of AI, machine learning, and analytics enhances diagnostic accuracy, treatment planning, and patient outcome predictions in these tools. Cloud-based solutions are gaining traction, with the global cloud-based dental practice management software market valued at USD 721 million in 2023 and projected to grow at 11.4% CAGR through 2030, offering remote access, scalability, and lower infrastructure costs.

Challenges include high initial setup costs for hardware, software, and training, particularly for small practices in emerging markets, alongside data privacy risks from cybersecurity threats and breaches. Opportunities arise from tele-dentistry expansion and government initiatives, such as India’s CollabDDS pilot for digital dental diagnosis in colleges via national networks. The WHO supports digital oral health tools, like mobile technologies, to complement prevention efforts amid rising disease burdens.

Key Takeaways

- Market Size: Global Dental Charting Software Market size is expected to be worth around US$ 6.7 Billion by 2035 from US$ 2.0 Billion in 2025.

- Market Share: The market growing at a CAGR of 13.1% during the forecast period from 2026 to 2035.

- Type of Practice: In 2025, the general dentistry segment is estimated to account for 46.2% of the total market share.

- Size of Practice: The dental charting software market is predominantly led by solo practitioners, accounting for 51.6% of the market share in 2025.

- Deployment Mode Segmentation: In 2025, the cloud-based segment is projected to hold 42.8% of the market share.

- Regional Analysis: In 2025, North America led the market, achieving over 35.80% share with a revenue of US$ 0.70 Billion.

Type of Practice Segmentation Analysis

The dental charting software market, when segmented by type of practice, demonstrates a clear dominance of general dentistry due to its broad patient base and high procedural volume. In 2025, the general dentistry segment is estimated to account for 46.2% of the total market share, supported by the widespread need for routine procedures such as examinations, cleanings, and restorative treatments.

The consistent patient inflow and repetitive clinical workflows have increased the reliance on digital charting solutions to enhance operational efficiency and patient record accuracy. Additionally, the integration of digital tools in general practices has been accelerating due to the need for streamlined documentation and regulatory compliance.

The specialized dentistry segment represents the second-largest share, driven by the growing demand for advanced treatments in orthodontics, periodontics, and oral surgery. These practices require highly customized charting functionalities to manage complex cases, thereby fostering adoption.

Meanwhile, dental laboratories form a smaller yet steadily growing segment, where software is utilized for prosthetic tracking and workflow coordination. The expansion of digital dentistry and CAD/CAM integration is expected to further support growth across specialized and laboratory segments.

Size of Practice Segmentation Analysis

Based on practice size, the dental charting software market is predominantly led by solo practitioners, accounting for 51.6% of the market share in 2025. This dominance is attributed to the large number of independent dental clinics globally, where cost-effective and easy-to-use charting solutions are preferred.

Solo practitioners increasingly adopt digital platforms to improve patient data management, reduce administrative burden, and enhance clinical efficiency. The affordability and scalability of modern software solutions further support adoption within this segment.

Group practices represent a significant and growing segment, driven by the need for centralized data management and collaborative workflows across multiple practitioners. These setups benefit from integrated systems that enable real-time data sharing and coordinated patient care.

Additionally, dental chains are emerging as a high-growth segment due to the expansion of corporate dentistry and dental support organizations. These entities require enterprise-level software solutions capable of handling multi-location operations, standardized reporting, and large patient databases. The increasing consolidation of dental services is expected to strengthen demand within group practices and dental chains over the forecast period.

Deployment Mode Segmentation Analysis

The market segmentation by deployment mode indicates a strong shift toward flexible and scalable digital infrastructure. In 2025, the cloud-based segment is projected to hold 42.8% of the market share, driven by advantages such as remote accessibility, lower upfront costs, and automatic software updates.

Cloud deployment enables seamless data sharing across multiple devices and locations, which is particularly beneficial for modern dental practices seeking operational efficiency and improved patient engagement.

Web-based solutions also maintain a notable presence, offering accessibility through browsers without requiring extensive installations. These systems are often preferred by small to mid-sized practices seeking cost-effective deployment with moderate flexibility. In contrast, on-premises solutions continue to be utilized by organizations prioritizing data control and security, particularly in regions with strict data regulations.

However, their adoption is gradually declining due to higher maintenance costs and limited scalability. Overall, the transition toward cloud-enabled ecosystems is expected to remain a key growth driver in the dental charting software market.

Key Market Segments

By Type of Practice

- General Dentistry

- Specialized Dentistry

- Dental Laboratories

By Size of Practice

- Solo Practitioners

- Group Practices

- Dental Chains

By Deployment Mode

- Cloud-based

- Web-based

- On-premises

Driving Factors

The growth of the dental charting software market is strongly driven by the increasing adoption of electronic dental records (EDRs) and broader digital health systems. Evidence from the Agency for Healthcare Research and Quality indicates that electronic dental record systems improve clinical decision-making and adherence to treatment guidelines, particularly for patients with complex conditions.

Adoption levels have reached significant thresholds; approximately 77% of dental clinics implemented EDR systems, although only 58% used fully certified systems, highlighting ongoing digital transition. Additionally, computerization in dental practices has expanded from 11% in 1984 to over 85% by 2009, reflecting a long-term structural shift toward digital workflows.

Government-backed digital health initiatives and regulatory frameworks have further encouraged providers to shift from paper-based records to digital charting systems to enhance patient safety and operational efficiency. The ability of dental charting software to reduce documentation errors, standardize clinical records, and support data-driven treatment planning is considered a primary factor accelerating its integration into modern dental practices globally.

Trending Factors

A key trend shaping the dental charting software market is the rapid transition toward cloud-based and integrated healthcare systems. Data indicates that over 80% of dental practices now operate on cloud-based platforms, reflecting a clear movement away from on-premise infrastructure. This shift is aligned with broader digital health strategies promoted by public health bodies, including interoperability and real-time data access initiatives.

Furthermore, more than 87% of dental practices are using electronic dental record systems, demonstrating near-universal digital adoption in developed healthcare ecosystems. Integration with electronic health records (EHRs) has emerged as a defining trend, enabling seamless sharing of patient information across medical and dental domains, which enhances continuity of care.

Healthcare authorities emphasize interoperability standards to support coordinated treatment and population health management. In addition, cloud-based dental charting software enables remote access, automatic updates, and scalability, which are particularly beneficial for multi-location dental service organizations. This trend is expected to continue as healthcare systems prioritize digital transformation, data standardization, and improved patient engagement through integrated software ecosystems.

Restraining Factors

Despite strong adoption, the dental charting software market faces notable restraints related to cost, technical complexity, and data security concerns. High initial investment remains a significant barrier, particularly for small and independent dental practices, where capital expenditure for software implementation and maintenance can be substantial.

Studies indicate that cost and cost–benefit concerns were among the leading barriers to adoption, limiting full-scale deployment of electronic dental records. Additionally, integration challenges persist, as many dental clinics operate legacy systems that are difficult to align with modern digital platforms.

Approximately 40% of practices still rely on outdated systems that resist integration, leading to inefficiencies such as duplicate data entry and workflow disruptions. Data privacy and cybersecurity risks also represent a critical restraint, as healthcare systems must comply with strict regulations to protect patient information.

The need for continuous staff training and technical support further increases operational burden. These constraints collectively slow adoption in smaller practices and emerging markets, despite the recognized benefits of digital dental charting solutions.

Opportunity

Significant opportunities exist in the dental charting software market, particularly through the expansion of digital healthcare infrastructure and underserved practice segments. Public healthcare initiatives promoting health information technology adoption provide a strong foundation for future growth.

For instance, studies supported by the Agency for Healthcare Research and Quality highlight the role of digital records in improving care quality and outcomes, especially in publicly funded programs such as Medicaid. Despite high adoption in advanced markets, disparities remain; smaller and specialized practices show lower adoption rates, with some segments having 67% lower likelihood of adopting digital systems compared to larger practices. This gap represents a substantial untapped market.

Additionally, the increasing prevalence of cloud-based solutions reduces infrastructure costs, making software more accessible to smaller clinics. Emerging markets, where paper-based systems are still common, offer further growth potential.

The integration of advanced technologies such as artificial intelligence, predictive analytics, and tele-dentistry into charting platforms is expected to create new value propositions, supporting preventive care and personalized treatment planning while expanding the overall addressable market.

Regional Analysis

North America dominates the dental charting software market, accounting for approximately 35.80% of global revenue, valued at around US$ 0.70 billion. Market expansion in this region is supported by high awareness of dental care, strong adoption of advanced technologies, and well-established regulatory frameworks.

The increasing need for efficient dental practice management systems has driven demand, particularly in the United States, which serves as the primary revenue contributor. The presence of advanced healthcare infrastructure, coupled with widespread adoption of digital tools and AI-enabled solutions, continues to strengthen regional market positioning.

Europe represents nearly 30% of the global market and is experiencing steady growth. This expansion is attributed to rising dental health awareness, increasing prevalence of oral diseases, and supportive government initiatives promoting digital healthcare integration. Countries such as Germany, the United Kingdom, and France are key contributors, where innovation, partnerships, and technological advancements are enhancing practice efficiency and patient engagement.

Asia-Pacific holds around 20% of the market share and is emerging as a high-growth region. Growth is driven by improving healthcare infrastructure, rising disposable income levels, and increasing awareness of oral health. Countries such as China and India are leading adoption, with market participants focusing on cost-effective and user-friendly software solutions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The dental charting software market is characterized by a fragmented competitive landscape, where both established global companies and emerging regional players operate actively. Key participants such as ABELSoft Inc., Bestosys, CD Newco, LLC, ClearDent, and Good Methods Global Inc. focus on offering cost-effective and user-friendly solutions, mainly targeting small and mid-sized dental practices. These companies emphasize customization, cloud-based deployment, and ease of integration to strengthen their market presence.

On the other hand, major players including Henry Schein, Inc. (Dentrix), Patterson Dental Supply, Inc., Planet DDS, Solutionreach, Inc., Open Dental Software, IDENTALSOFT, and XLDent hold a strong position due to their advanced product portfolios, strong distribution networks, and brand recognition. For instance, Dentrix benefits from a large installed base and integrated practice management features, while Planet DDS focuses on cloud-based platforms for large dental groups.

Overall, competition is driven by technological innovation, cloud adoption, and service differentiation, with companies increasingly investing in AI integration, patient management tools, and real-time data capabilities to gain competitive advantage in the market.

Market Key Players

- ABELSoft Inc.

- Bestosys

- CD Newco, LLC

- ClearDent

- Good Methods Global Inc.

- Henry Schein, Inc. (Dentrix)

- IDENTALSOFT

- Open Dental Software

- Patterson Dental Supply, Inc.

- Planet DDS

- Solutionreach, Inc.

- XLDent

- Others

Recent Developments

- January 2026 – Planet DDS: Planet DDS reported that it closed 2025 with strong expansion among large DSOs, deeper leadership bench strength, and increased third-party recognition, reinforcing its position as a leading cloud platform for multi-location dental groups.

- January 2026 – Solutionreach, Inc.: Solutionreach highlighted multiple new product enhancements on its patient-engagement platform, including upgrades to automated communication, insurance verification, and workflow tools, aimed at helping dental organizations work smarter at scale.

- March 2025 – Curve Dental: Curve Dental launched an AI-powered analytics module within its cloud dental platform, giving practices real-time insight into patient trends, appointment efficiency, and treatment outcomes, which raised the competitive bar for analytics and reporting expected from dental charting and practice software vendors.

- March 2026 – Henry Schein, Inc.: Henry Schein One unveiled the next era of Dentrix Ascend for DSOs and growth-focused practices, introducing new integrated packages built on an AI-driven, agentic platform architecture to improve revenue performance and efficiency for complex dental organizations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 2.0 Billion |

| Forecast Revenue (2035) | US$ 6.7 Billion |

| CAGR (2026-2035) | 13.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type of Practice(General Dentistry, Specialized Dentistry, Dental Laboratories) By Size of Practice(Solo Practitioners, Group Practices, Dental Chains) By Deployment Mode(Cloud-based, Web-based, On-premises) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | ABELSoft Inc., Bestosys, CD Newco, LLC, ClearDent, Good Methods Global Inc., Henry Schein, Inc. (Dentrix), IDENTALSOFT, Open Dental Software, Patterson Dental Supply, Inc., Planet DDS, Solutionreach, Inc., XLDent, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |