Quick Navigation

Report Overview

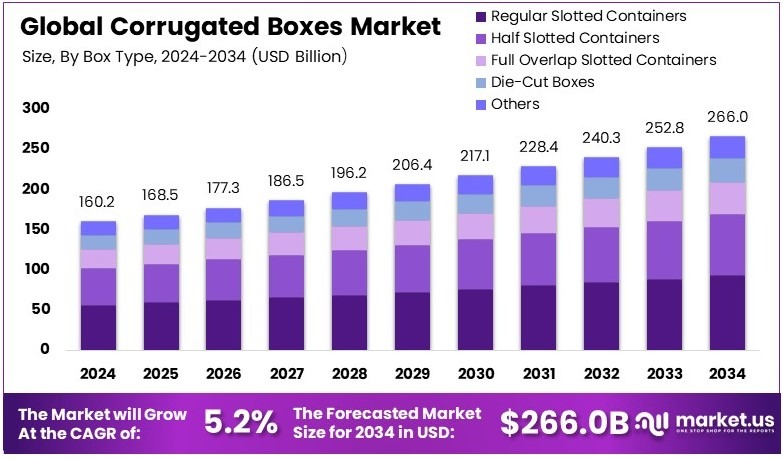

The Global Corrugated Boxes Market size is expected to be worth around USD 266.0 Billion by 2034, from USD 160.2 Billion in 2024, growing at a CAGR of 5.2% during the forecast period from 2025 to 2034.

Corrugated boxes are packaging containers made from layered cardboard. They are strong, lightweight, and used for shipping and storage. Their structure provides durability and protection. These boxes are widely used across industries like retail, e-commerce, food, and logistics for packaging goods safely and efficiently.

The corrugated boxes market includes companies producing and distributing these packaging solutions. Growth is driven by rising online shopping and demand for sustainable packaging. Companies focus on recyclable materials and custom solutions to meet business needs.

The corrugated boxes segment is growing due to rising online shopping. In 2023, global e-commerce sales reached $5.9 trillion. This figure is expected to cross $8 trillion by 2027. With more goods being shipped, the need for strong and lightweight packaging like corrugated boxes has increased sharply.

The corrugated boxes market remains highly competitive. Many companies offer similar products, creating pricing pressure. Even so, demand stays high. As per Supply Chain Beyond, $32 billion in returns occurred during a single holiday season, with 20%-30% linked to product damage. Corrugated packaging helps reduce such risks.

To reduce returns, brands are improving packaging design. For instance, fragile goods need about 3 inches of protective space in the box. Corrugated boxes make this possible without adding too much weight. Therefore, these boxes are used widely in electronics, glassware, and food delivery sectors.

Meanwhile, market saturation is rising in urban areas. However, brands that use recyclable materials or custom sizes can still stand out. Not to mention, smart packaging solutions that lower shipping costs offer an edge. These features appeal to both businesses and eco-aware consumers.

On a broader level, corrugated packaging supports global logistics and e-commerce efficiency. Locally, small retailers and food chains are using corrugated boxes for safer, branded deliveries. Cities with high delivery volume—like New York and Los Angeles—rely heavily on such packaging to reduce breakage and ensure customer satisfaction.

In the U.S., regulation is pushing packaging reforms. States like Minnesota passed laws requiring producers to manage packaging waste by 2031. This Extended Producer Responsibility (EPR) approach is gaining ground. Consequently, firms are now designing corrugated boxes with recyclability and lower material waste in mind.

Key Takeaways

- The Corrugated Boxes Market was valued at USD 160.2 billion in 2024 and is expected to reach USD 266.0 billion by 2034, with a CAGR of 5.2%.

- In 2024, Regular Slotted Containers (RSC) dominated the box type segment with 35.7%, due to their cost-effectiveness and versatility in packaging.

- In 2024, Double Wall corrugated boxes led the flute type segment with 48.3%, offering enhanced durability and strength.

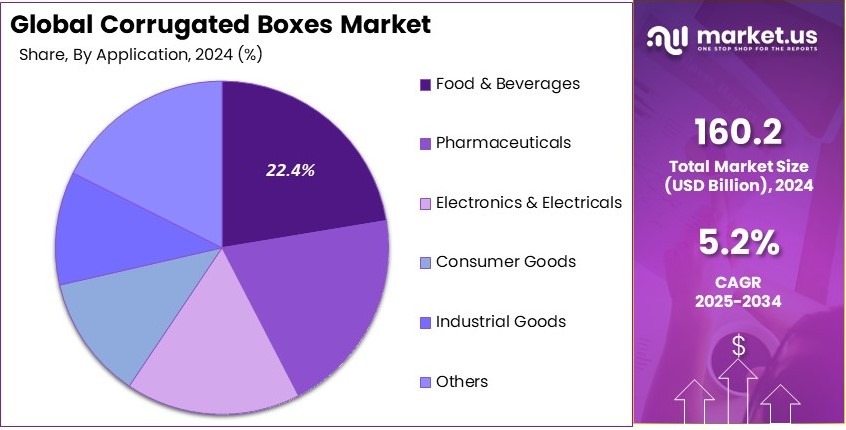

- In 2024, Food & Beverages was the dominant application segment with 22.4%, driven by increasing demand for sustainable and sturdy packaging.

- In 2024, Flexographic Printing held the largest share in the printing technology segment with 56.1%, due to its cost-effectiveness for high-volume production.

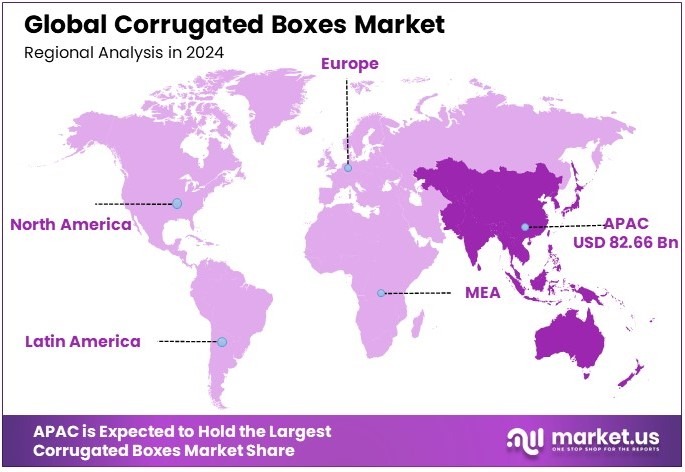

- In 2024, Asia Pacific dominated the market with 51.6% and USD 82.66 billion, supported by rapid industrialization and booming e-commerce in the region.

Type Analysis

Regular Slotted Containers (RSC) dominate with 35.7% due to their versatility and cost-effectiveness.

The corrugated boxes market can be segmented by box type, which includes Regular Slotted Containers (RSC), Half Slotted Containers (HSC), Full Overlap Slotted Containers (FOL), Die-Cut Boxes, and Others. The RSC segment holds a significant share due to its widespread use across various industries, attributed to its standard design that combines efficiency with material cost savings. The adaptability of RSC to accommodate a range of products securely makes it a preferred choice, especially in the shipping and logistics sectors.

The HSC type, which is utilized for heavier items, and the FOL type, known for extra strength and stacking capabilities, also contribute to the market, though to a lesser extent. Die-cut boxes offer customization for specific needs, adding value in niche markets such as electronics and gifts. The ‘Others’ category captures specialized types that cater to unique customer requirements.

Flute Type Analysis

Double Wall dominates with 48.3% due to its enhanced durability and protective capabilities.

In the flute type segment, Single Wall, Double Wall, and Triple Wall are key sub-segments. Double Wall corrugated boxes are the most dominant, favored for their robustness which is essential in protecting goods during transit, particularly in industries like electronics and home appliances where protection is crucial. This type provides an optimal balance between cost and performance, making it highly sought after in both domestic and international markets.

Single Wall flutes are commonly used for lighter items and offer cost advantages and flexibility. Triple Wall boxes, being the most durable, are reserved for very heavy or fragile items, but their higher cost limits their use to specific applications where extra strength is mandatory.

Application Analysis

Food & Beverages dominate with 22.4% due to increasing demand for sustainable packaging solutions.

Corrugated boxes are extensively used across various applications; the Food & Beverages, Pharmaceuticals, Electronics & Electricals, Consumer Goods, Industrial Goods, and Others form the primary market segments.

The Food & Beverages segment emerges as the leader, propelled by the growing need for safe and sustainable packaging. The shift towards organic and health-conscious food products has further driven the demand for eco-friendly and recyclable packaging, making corrugated boxes a preferred choice.

Pharmaceuticals also rely heavily on corrugated boxes for safe drug delivery, especially seen during the recent upsurge in medical supplies due to global health concerns. Electronics & Electricals require precision packaging for sensitive components, while Consumer and Industrial Goods segments leverage corrugated for its strength and adaptability.

Printing Technology Analysis

Flexographic Printing dominates with 56.1% due to its cost-efficiency and adaptability.

Printing technology applied to corrugated boxes includes Flexographic Printing, Digital Printing, Lithographic Printing, and Others. Flexographic printing holds the largest market share due to its efficiency in high-volume production and its ability to print on a wide variety of substrates. This method is particularly valued for delivering robust print quality at lower costs, making it ideal for standard corrugated box applications.

Digital printing, although more expensive, offers advantages in customization and shorter print runs, making it suitable for niche markets that require high-quality graphics. Lithographic printing provides superior print quality and is preferred for products requiring high visual appeal. The ‘Others’ category encompasses alternative printing technologies that cater to specific market needs, offering specialized solutions.

Key Market Segments

By Box Type

- Regular Slotted Containers (RSC)

- Half Slotted Containers (HSC)

- Full Overlap Slotted Containers (FOL)

- Die-Cut Boxes

- Others

By Flute Type

- Single Wall

- Double Wall

- Triple Wall

By Application

- Food & Beverages

- Pharmaceuticals

- Electronics & Electricals

- Consumer Goods

- Industrial Goods

- Others

By Printing Technology

- Flexographic Printing

- Digital Printing

- Lithographic Printing

- Others

Driving Factors

E-Commerce Expansion and Custom Packaging Drive Market Growth

The corrugated boxes market is expanding rapidly due to rising demand from e-commerce and direct-to-consumer (DTC) retail. Online retailers need packaging that is durable, easy to handle, and protects products during shipping. Corrugated boxes meet these needs perfectly. With the growth of platforms like Amazon, Shopify, and Etsy, brands are using more boxes than ever.

Sustainability is another major driver. Corrugated boxes are recyclable, which appeals to eco-conscious buyers and businesses. Companies are switching from plastic to paper-based boxes to reduce their carbon footprint and comply with environmental goals.

There is also growing demand for customizable and protective packaging. Fragile goods, electronics, and glassware need special inserts or strong, multi-layered boxes. Brands now offer custom-fit corrugated packaging to reduce damage during transit.

To meet rising demand, manufacturers are investing in automation and high-speed production lines. This helps reduce costs, increase output, and shorten delivery times. As the need for faster order fulfillment grows, these improvements are becoming essential.

Restraining Factors

Raw Material Costs and Supply Risks Restrain Market Growth

Despite strong demand, the corrugated boxes market faces several limiting factors. One major challenge is the volatility in raw material prices. Paper pulp and recycled paperboard costs can rise suddenly due to supply shortages, increased demand, or environmental regulations. These price swings reduce profit margins and make long-term pricing difficult for manufacturers.

Supply chain disruptions also affect production and distribution. Delays in sourcing paper, labor shortages, or transportation bottlenecks can halt or slow box manufacturing. Events like pandemics or geopolitical tensions often worsen these disruptions.

There is also increasing competition from flexible packaging options. These alternatives use less material, take up less space, and are often cheaper to produce. Some industries are switching to pouches or films for lightweight items, which reduces demand for boxes.

Lastly, there are regulatory pressures related to paper sourcing. Governments and environmental groups are tightening rules on deforestation and virgin paper use. This affects how manufacturers obtain raw materials and adds extra steps to ensure compliance.

Growth Opportunities

Lightweight Materials and Digital Printing Provide Opportunities

The corrugated boxes market has strong growth opportunities, especially through innovation in materials and printing technologies. One key area is the development of high-strength, lightweight boxes. These allow for lower shipping costs without sacrificing product safety. As shipping fees rise, brands prefer lighter packaging to cut logistics expenses.

Digital printing is also creating new opportunities. It allows companies to produce short-run, custom packaging with logos, colors, and marketing messages. This is especially useful for small businesses, seasonal products, or promotional campaigns. Fast turnaround and lower setup costs make digital printing ideal for on-demand packaging needs.

In emerging markets, industrial growth is driving higher demand for corrugated packaging. As more products are made and shipped across regions like Southeast Asia, Africa, and South America, local packaging needs are growing fast. This creates opportunities for manufacturers to expand operations and partner with regional suppliers.

Another area of innovation is coatings. Water-resistant and greaseproof corrugated boxes are gaining traction in food delivery, frozen foods, and industrial shipping. These coatings add durability without compromising recyclability. In short, lightweight design, digital printing, international expansion, and improved coatings offer significant potential. Companies that invest in these areas can reduce costs and meet the changing demands of modern packaging.

Emerging Trends

Branded Unboxing and Smart Packaging Are Latest Trending Factor

Several trends are shaping the future of the corrugated boxes market. One standout is the growing demand for printed and branded boxes. Businesses now focus on creating memorable unboxing experiences. From colorful designs to logo placement, packaging is now part of the customer journey, especially in fashion, cosmetics, and tech.

Subscription box services are fueling this trend. Companies like Birchbox and HelloFresh rely on unique, branded corrugated packaging to engage customers. These services require fresh, customized packaging each cycle, which increases demand for short-run, high-quality box production.

Technology is also becoming part of packaging. RFID tags and IoT-enabled labels are being added to boxes to improve tracking in the supply chain. This is especially useful in pharmaceuticals, electronics, and logistics, where real-time updates on delivery and condition are important.

Finally, circular economy goals are pushing the adoption of recycled and upcycled materials. Brands are now using 100% recycled paper or boxes made from post-consumer waste. Some even include returnable packaging options to reduce environmental impact.

Regional Analysis

Asia Pacific Dominates with 51.6% Market Share

Asia Pacific leads the Corrugated Boxes Market with a dominant 51.6% share, valued at USD 82.66 billion. This strong lead is driven by booming e-commerce, large-scale manufacturing, and growing demand for eco-friendly packaging in countries like China, India, and Japan. Rapid urbanization and consumer shifts toward online shopping are key forces behind this growth.

The region benefits from low-cost production, strong logistics networks, and high packaging consumption. China is a global manufacturing hub, using corrugated boxes heavily for electronics, garments, and consumer goods exports. India is seeing fast growth in packaged food and retail. Japan and South Korea emphasize sustainable packaging and automation, boosting box innovation.

Local dynamics such as fast delivery services, high mobile usage, and large rural-to-urban migration are reshaping packaging needs. Corrugated boxes meet requirements for strength, recyclability, and cost-effectiveness. Small and medium enterprises across Asia also use corrugated solutions due to their affordability and easy availability.

Looking ahead, Asia Pacific is expected to keep its lead. Rising demand from online grocery, electronics, and personal care brands will drive volume. Investments in smart packaging and recyclable materials will also shape the future of the corrugated boxes market in the region.

Regional Mentions:

- North America: North America remains a strong player in the corrugated boxes market, supported by established retail chains and growing online shopping. The U.S. focuses on automation and custom-designed packaging, especially for electronics, food, and healthcare products.

- Europe: Europe promotes eco-friendly corrugated packaging through strict recycling laws. Countries like Germany and France are pushing for lightweight, biodegradable packaging in food, beverage, and personal care industries.

- Middle East & Africa: The Middle East and Africa are steadily growing, supported by expanding trade and e-commerce. UAE and South Africa are leading regional development with increased investment in local packaging industries and logistics infrastructure.

- Latin America: Latin America is gaining momentum with growing demand from retail and agriculture. Brazil and Mexico use corrugated boxes for transporting fruits, vegetables, and FMCG products. Government support for local manufacturing helps sustain growth.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The corrugated boxes market is growing due to demand from e-commerce, retail, and food packaging. The top four companies—International Paper Company, WestRock Company, Packaging Corporation of America (PCA), and Georgia-Pacific LLC—hold strong positions in the U.S. and global markets.

International Paper Company is a leading supplier of fiber-based packaging. It has a large network of mills and converting plants. The company focuses on sustainable packaging and invests in recycling and renewable fiber solutions.

WestRock Company offers customized packaging solutions. It serves many industries including food, beverage, and healthcare. The company uses advanced technology for efficient production and aims to reduce environmental impact.

Packaging Corporation of America (PCA) is known for its high-quality boxes and strong customer service. It focuses on the domestic U.S. market and has a fast, flexible production system. PCA serves both small and large businesses with tailored packaging.

Georgia-Pacific LLC is part of Koch Industries. It has a strong presence in both containerboard and corrugated packaging. The company invests in automation and eco-friendly materials. It serves various sectors like food, electronics, and logistics.

These key players benefit from large production capacity, strong distribution networks, and wide customer bases. Their focus on sustainable practices and supply chain efficiency helps them stay competitive.

The top four companies lead the corrugated boxes market through high production scale, innovation in materials, and customer-focused services. Their long-term investments in sustainability and technology support market growth and meet rising demand from global supply chains.

Major Companies in the Market

- International Paper Company

- WestRock Company

- Packaging Corporation of America (PCA)

- Georgia-Pacific LLC

- Smurfit Kappa Group

- DS Smith Plc

- Pratt Industries, Inc.

- Mondi Group

- Cascades Inc.

- Oji Holdings Corporation

- Nine Dragons Paper Holdings Limited

- Stora Enso Oyj

- Rengo Co., Ltd.

Recent Developments

- International Paper and DS Smith: On October 2024, International Paper completed the acquisition of UK-based DS Smith and subsequently announced the closure of six facilities across North Carolina and Texas in the corrugated box segment as part of its integration strategy.

- Green Bay Packaging and SMC Packaging Group: On June 2024, Green Bay Packaging announced the acquisition of SMC Packaging Group, a corrugated box manufacturer based in Springfield, Missouri. This acquisition enhances the company’s vertical integration from forestland management to corrugated converting operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 160.2 Billion |

| Forecast Revenue (2034) | USD 266.0 Billion |

| CAGR (2025-2034) | 5.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Box Type (Regular Slotted Containers (RSC), Half Slotted Containers (HSC), Full Overlap Slotted Containers (FOL), Die-Cut Boxes, Others), By Flute Type (Single Wall, Double Wall, Triple Wall), By Application (Food & Beverages, Pharmaceuticals, Electronics & Electricals, Consumer Goods, Industrial Goods, Others), By Printing Technology (Flexographic Printing, Digital Printing, Lithographic Printing, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | International Paper Company, WestRock Company, Packaging Corporation of America (PCA), Georgia-Pacific LLC, Smurfit Kappa Group, DS Smith Plc, Pratt Industries, Inc., Mondi Group, Cascades Inc., Oji Holdings Corporation, Nine Dragons Paper Holdings Limited, Stora Enso Oyj, Rengo Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |