Quick Navigation

Report Overview

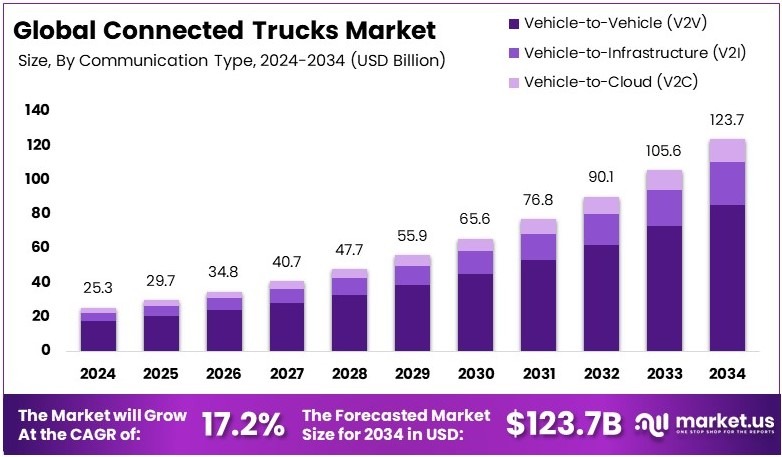

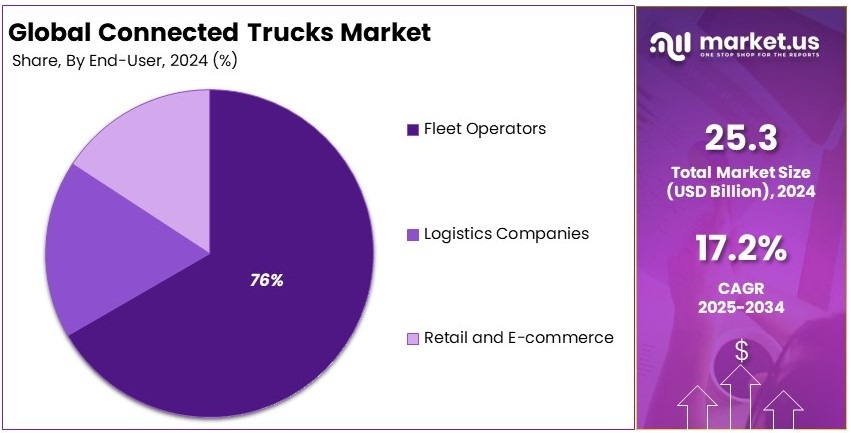

The Global Connected Trucks Market size is expected to be worth around USD 123.7 Billion by 2034, from USD 25.3 Billion in 2024, growing at a CAGR of 17.2% during the forecast period from 2025 to 2034.

Connected trucks are commercial vehicles equipped with advanced technology. They use sensors, internet connectivity, and data analytics to improve operations. These trucks provide real-time information on vehicle performance, safety, and routes. They aim to increase efficiency, reduce downtime, and enhance logistics management in transport industries.

The connected trucks market covers the industry around smart trucking technology. It includes manufacturers, suppliers, and service providers of connectivity solutions. The market offers products like telematics, IoT devices, and software platforms. It serves fleet operators looking to optimize their vehicles with data-driven insights and improved connectivity.

The trucking industry plays a vital role in the U.S. economy, responsible for transporting 72.6% of all freight by weight. In 2022, this sector generated $940.8 billion in revenue, accounting for 80.7% of the nation’s total freight bill. Connected trucks are now emerging as key tools to enhance operational efficiency and safety in this critical industry.

Connected trucks offer significant opportunities for growth in the trucking sector. As of 2022, the U.S. had over 8.4 million people employed in trucking, with small businesses dominating the landscape. Nearly 95.8% of trucking companies operate fleets of 10 or fewer trucks. These trucks, equipped with advanced connectivity, can significantly improve logistics and fleet management, driving efficiency across the board.

Trucks are essential for trade, particularly with neighboring countries. In 2022, trucks moved 61.9% of ground freight between the U.S. and Canada and 83.5% with Mexico, transporting goods worth $948 billion. Government regulations and investments in smart transportation can further boost the efficiency and safety of these vital trade routes, showcasing the broad and local impacts of connected truck technology on the industry.

Key Takeaways

- The Connected Trucks Market was valued at USD 25.3 Billion in 2024, and is expected to reach USD 123.7 Billion by 2034, with a CAGR of 17.2%.

- In 2024, Vehicle-to-Vehicle (V2V) Communication dominates the communication type segment with 69%, showcasing its pivotal role in truck connectivity.

- In 2024, Fleet Management Services lead the service type segment with 72%, emphasizing the growing reliance on digital fleet solutions.

- In 2024, Light Commercial Vehicles (LCVs) dominate the vehicle type segment with 63%, reflecting their widespread adoption in connected solutions.

- In 2024, Fleet Operators dominate the end-user segment with 76%, indicating their significant influence on market demand.

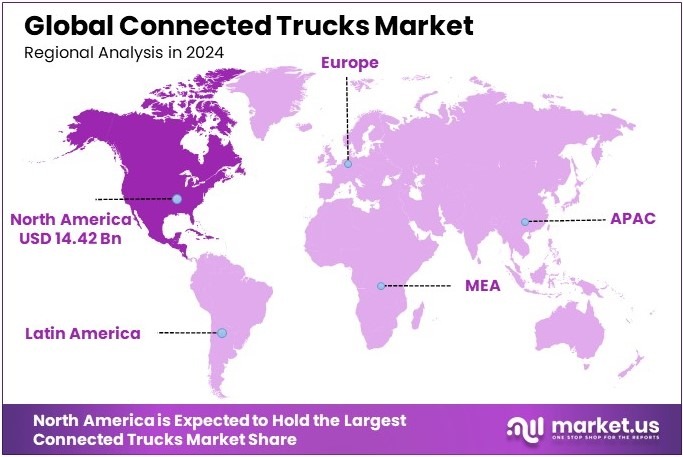

- In 2024, North America leads the regional market with 57% and a value of USD 14.42 Bn, underscoring its strategic importance in the connected trucks sector.

Communication Type Analysis

Vehicle-to-Vehicle (V2V) Communication dominates with 69% due to its crucial role in enhancing road safety and traffic efficiency.

The Connected Trucks Market is revolutionizing the way vehicles interact on the road, with Communication Types being a pivotal component. Within this segment, Vehicle-to-Vehicle (V2V) Communication emerges as the leading sub-segment, holding a significant 69% of the market.

The high adoption rate of V2V technology is primarily due to its capability to increase road safety and traffic efficiency by allowing trucks to communicate and share vital information about speed, road conditions, and traffic.

Other forms of communication include Vehicle-to-Infrastructure (V2I) and Vehicle-to-Cloud (V2C). V2I communication is essential for enhancing intelligent traffic management by allowing trucks to interact with road sensors and traffic signals, thereby improving navigation and reducing congestion.

V2C communication connects trucks directly to cloud-based services, enabling enhanced data collection and analytics, which supports better fleet management and operational efficiency.

Service Type Analysis

Fleet Management Services dominate with 72% due to their importance in optimizing operational efficiency and reducing costs.

In the Connected Trucks Market, Service Types play a crucial role in managing the efficiency and productivity of truck operations. Among these, Fleet Management Services hold the dominant position with 72%, reflecting their comprehensive utility in providing real-time monitoring, vehicle tracking, and operational scheduling, which are vital for optimizing fleet operations and reducing overhead costs.

The segment also includes Remote Diagnostics, Over-the-Air (OTA) Updates, and Driver Assistance Services. Remote Diagnostics are pivotal in maintaining vehicle health by providing early warnings of potential mechanical failures.

OTA Updates keep the truck’s software up-to-date without the need to visit a service center, enhancing convenience and reducing downtime. Driver Assistance Services improve road safety by assisting drivers in navigation and maneuvering, which is crucial for preventing accidents.

Vehicle Type Analysis

Light Commercial Vehicles (LCVs) dominate with 63% due to their versatility in urban and rural settings.

The Vehicle Type segment of the Connected Trucks Market is essential, with Light Commercial Vehicles (LCVs) accounting for a dominant 63% share. This predominance is driven by the flexibility and efficiency of LCVs, which are ideal for both urban and rural applications, meeting diverse logistical and delivery needs.

Heavy Commercial Vehicles (HCVs) also form a substantial part of the market, utilized primarily for long-haul and large-scale transport tasks. Though they have a smaller share compared to LCVs, HCVs are integral for transporting bulk goods across long distances, playing a crucial role in global trade and commerce.

End-User Analysis

Fleet Operators dominate with 76% due to their direct involvement in the management and utilization of connected truck technologies.

In the End-User segment, Fleet Operators are the primary market drivers, holding a 76% share. Their significant involvement is due to the direct benefits they gain from using connected truck technologies, such as improved fleet management, enhanced safety features, and optimized logistical operations, which are crucial for maintaining competitiveness in the transport sector.

Other notable end-users include Logistics Companies and Retail and E-commerce businesses. Logistics companies heavily rely on connected trucks for efficient route planning and cargo management, while Retail and E-commerce sectors use these technologies to enhance delivery services and customer satisfaction by ensuring timely and safe product deliveries.

Key Market Segments

By Communication Type

- Vehicle-to-Vehicle (V2V) Communication

- Vehicle-to-Infrastructure (V2I) Communication

- Vehicle-to-Cloud (V2C) Communication

By Service Type

- Fleet Management Services

- Remote Diagnostics

- Over-the-Air (OTA) Updates

- Driver Assistance Services

By Vehicle Type

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

By End-User

- Fleet Operators

- Logistics Companies

- Retail and E-commerce

Driving Factors

Connected Trucks Market Growth Driven by IoT and 5G Advancements

The Connected Trucks Market sees robust growth driven by various innovative factors. Increasing adoption of IoT in automotive applications is a key driver.

This trend enables trucks to share vital data in real-time, improving safety and efficiency. Rising demand for fleet management solutions also fuels market expansion. Fleet operators seek connected technologies to track vehicles, reduce fuel costs, and optimize routes.

Growth of autonomous vehicle technologies further spurs the market. Autonomous trucks promise higher productivity and reduced human error. Advancements in 5G connectivity enhance communication systems significantly. With faster, more reliable networks, trucks can transmit large amounts of data quickly, boosting operational efficiency.

These factors collectively create a dynamic environment for market growth. For example, a logistics company might invest in connected trucks to streamline operations and lower costs. The synergy of IoT, fleet management, autonomy, and 5G connectivity ensures that the market evolves rapidly, offering new opportunities for manufacturers and service providers.

Restraining Factors

Economic and Regulatory Challenges Restrain Market Growth

The Connected Trucks Market is not without its challenges. Data privacy and cybersecurity concerns in connected systems are significant hurdles. Companies worry about protecting sensitive information from cyber threats. Limited infrastructure for supporting advanced connectivity in developing regions also impedes growth. Without proper networks, connected trucks cannot perform optimally.

Lack of standardization in connected vehicle protocols creates another challenge. Different manufacturers and systems may not work well together, causing compatibility issues. Resistance to adoption among traditional fleet operators slows the market further. Many operators are hesitant to invest in new technology due to perceived risks or lack of understanding.

These factors restrict market expansion and complicate deployment. For example, a fleet manager in a developing region might face infrastructure limitations that hinder the effective use of connected trucks. The combination of cybersecurity risks, infrastructural gaps, protocol inconsistencies, and resistance delays broader market acceptance.

Growth Opportunities

Innovation Provides Opportunities

Development of autonomous connected trucks promises seamless operations and reduced downtime. These vehicles can operate continuously, gathering data for improved performance. Expansion of V2G (Vehicle-to-Grid) solutions for energy management offers another growth avenue. Trucks can balance energy loads and even supply energy back to the grid when idle.

Increasing use of big data analytics for fleet optimization is transforming operations. By analyzing collected data, companies can reduce costs and improve decision-making. Integration of AI and machine learning for predictive insights further enhances efficiency. Predictive maintenance and route optimization reduce unexpected breakdowns and fuel consumption.

For instance, a company using predictive AI might detect potential engine issues before they cause downtime. V2G solutions might allow a fleet to save on energy costs while supporting the grid. These innovations open new revenue streams and operational efficiencies.

Emerging Trends

Smart Trends Are Latest Trending Factor

Emerging trends are reshaping the Connected Trucks Market and setting new industry benchmarks. Adoption of digital twins for fleet performance simulation is becoming widespread.

Digital twins allow operators to model truck behavior in virtual environments, improving planning and efficiency. Growth in electrification of connected trucks for sustainability is another key trend. Electric trucks powered by smart technology appeal to eco-conscious fleets seeking to reduce emissions.

Use of augmented reality in driver assistance and maintenance is on the rise. AR can guide drivers through repairs or optimize their routes in real-time. Increasing focus on over-the-air (OTA) updates for software ensures that trucks remain current without the need for physical service visits.

These trends impact the market by driving efficiency, sustainability, and user convenience. For example, an operator might use digital twins to simulate maintenance schedules and avoid breakdowns. Electric trucks with AR support can make fleets safer and greener. OTA updates keep systems secure and up-to-date effortlessly.

Regional Analysis

North America Dominates with 57% Market Share

North America leads the Connected Trucks Market with an impressive 57% share, totaling USD 14.42 billion. This dominance is driven by the region’s advanced logistics and transportation infrastructure, coupled with a strong focus on innovation and technology adoption in the automotive sector.

The region’s market leadership is underpinned by widespread adoption of telematics and fleet management solutions, which are critical for operational efficiency in logistics. Additionally, the presence of major automotive and technology companies facilitates rapid advancements and adoption of connected truck technologies.

The future influence of North America in the global Connected Trucks Market is expected to strengthen further. As the demand for more efficient and sustainable transportation solutions grows, North America is poised to lead with ongoing investments in smart transportation and IoT integrations, likely increasing its market share even more.

Regional Mentions:

- Europe: Europe holds a substantial share in the Connected Trucks Market, supported by strong regulatory frameworks promoting safety and environmental sustainability. Innovations in connectivity and autonomous driving technologies are particularly robust in this region.

- Asia Pacific: The Asia Pacific region is rapidly growing in the Connected Trucks Market, driven by expanding logistics networks and increasing technological adoption. Countries like Japan and South Korea are forefront in integrating advanced connectivity solutions in commercial vehicles.

- Middle East & Africa: Middle East and Africa are experiencing gradual growth in the Connected Trucks Market. Investments in infrastructure and an increasing focus on logistics and transport automation are key factors driving this growth.

- Latin America: Latin America’s Connected Trucks Market is developing, with increasing adoption of fleet management and GPS tracking solutions. The growth is spurred by the need for more efficient transportation and reduction in operational costs.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The Connected Trucks Market is dominated by major players such as Daimler AG, Volvo Group, Scania AB, and PACCAR Inc. These companies are at the forefront due to their advanced technological integrations, comprehensive fleet solutions, and global market presence.

Daimler AG is a pioneer in the automotive industry, leading with its Mercedes-Benz trucks that incorporate cutting-edge connectivity technologies for enhanced logistic efficiency and safety. The company’s strong emphasis on innovation drives its leadership in the connected trucks sector.

Volvo Group is recognized for its commitment to sustainability and safety. Their connected trucks are equipped with the latest in vehicle communication, autonomous driving technology, and emission reduction systems, making them a top choice for businesses aiming to reduce their environmental impact while improving fleet management.

Scania AB focuses on delivering customized transport solutions that include connected services for optimizing fuel efficiency and minimizing downtime. Their trucks are equipped with smart systems that help in real-time monitoring and management, appealing to a wide range of commercial uses.

PACCAR Inc. offers robust vehicle design and connected services through its Kenworth, Peterbilt, and DAF lines. Their trucks are known for durability, reliability, and advanced fleet management features that cater to the rigorous demands of freight and logistics operators.

These industry leaders are driving the Connected Trucks Market towards higher efficiency and greater integration of IoT technologies, with ongoing innovations aimed at improving transport logistics, safety, and operational effectiveness on a global scale.

Major Companies in the Market

- Daimler AG

- Volvo Group

- Scania AB

- PACCAR Inc.

- Navistar International Corporation

- MAN SE

- Hino Motors, Ltd.

- Isuzu Motors Limited

- Tata Motors

- Ashok Leyland

- BYD Auto Co., Ltd.

- Nikola Corporation

- Rivian Automotive, LLC

Recent Developments

- Sennder and C.H. Robinson’s European Operations: On July 2024, German digital freight firm Sennder acquired the European logistics operations of U.S.-based C.H. Robinson. This acquisition is expected to double Sennder’s revenue to €1.4 billion ($1.5 billion), enhancing its appeal to small transport companies and shippers across Europe.

- Roadrunner Transportation Systems: On November 2024, Roadrunner Transportation Systems secured significant investment from a consortium led by CEO Chris Jamroz and investor Ted Kellner, acquiring over 80% of the company. With this new capital, Roadrunner plans to re-enter the mergers and acquisitions space, focusing on less-than-truckload (LTL) targets aligned with its operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 25.3 Billion |

| Forecast Revenue (2034) | USD 123.7 Billion |

| CAGR (2025-2034) | 17.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Communication Type (Vehicle-to-Vehicle, Vehicle-to-Infrastructure, Vehicle-to-Cloud), By Service Type (Fleet Management Services, Remote Diagnostics, Over-the-Air Updates, Driver Assistance Services), By Vehicle Type (Light Commercial Vehicles, Heavy Commercial Vehicles), By End-User (Fleet Operators, Logistics Companies, Retail and E-commerce) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Daimler AG, Volvo Group, Scania AB, PACCAR Inc., Navistar International Corporation, MAN SE, Hino Motors, Ltd., Isuzu Motors Limited, Tata Motors, Ashok Leyland, BYD Auto Co., Ltd., Nikola Corporation, Rivian Automotive, LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |