Global Commercial Unmanned Aerial Systems Market Size, Share, Industry Analysis Report By Product (Fixed wing UAV, Rotary blade UAV, Hybrid UAV, Nano UAV), By Application (Agriculture, Retail, Energy, Media and Entertainment, Construction, Government, Others), By Region, Global Opportunity Analysis, Future Outlook and Industry Trends Forecast 2025-2034

- Published date: Sept. 2025

- Report ID: 158211

- Number of Pages: 265

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Insight Summary

- Analysts’ Viewpoint

- Role of Generative AI

- Government-led Investments

- Regional Focus: North America

- By Product: Fixed Wing UAVs

- By Application: Retail

- Emerging Trends

- Growth Factors

- Latest Announcements

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

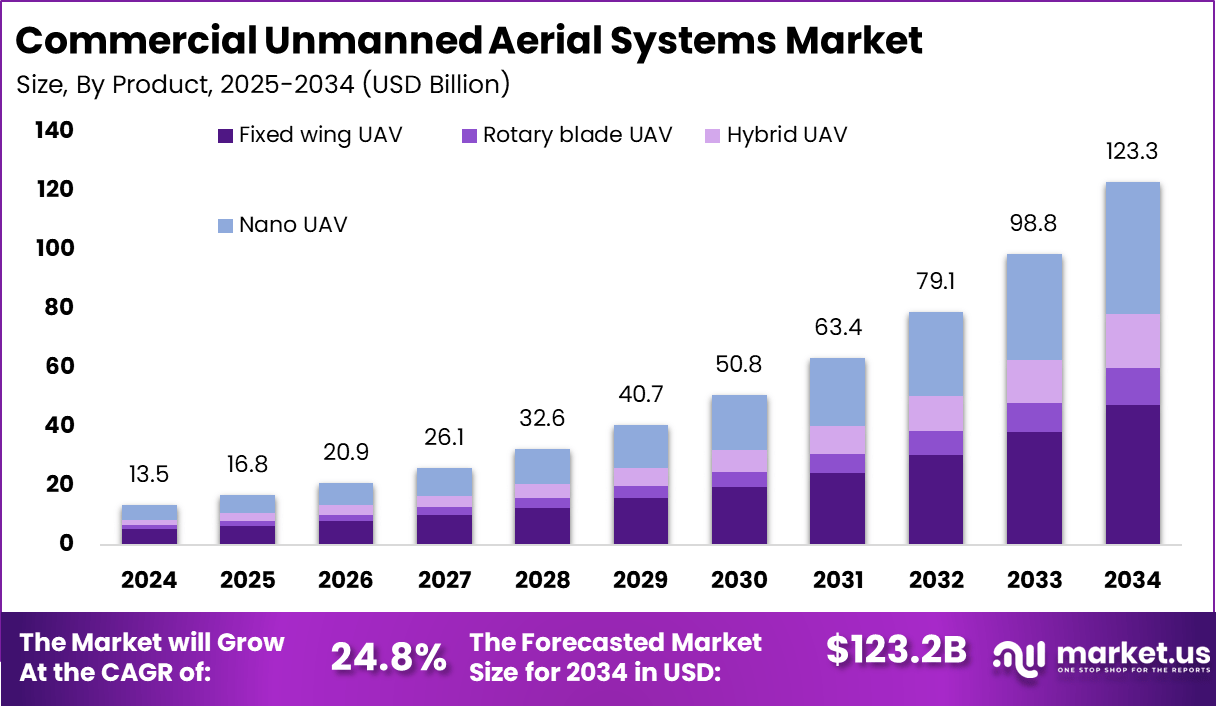

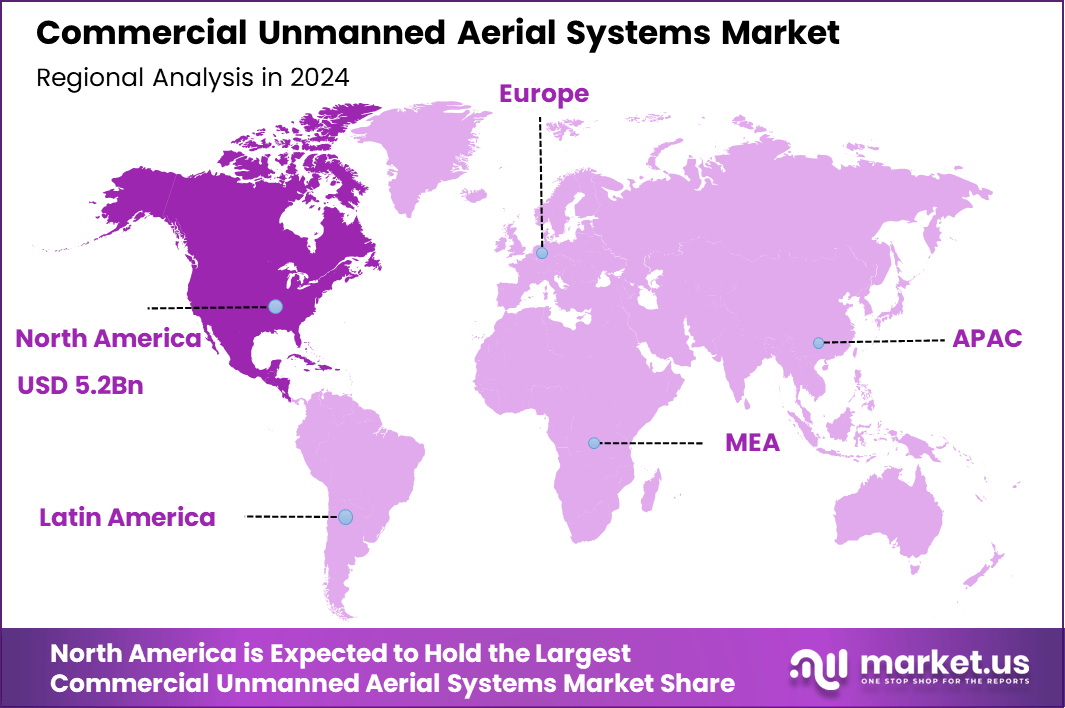

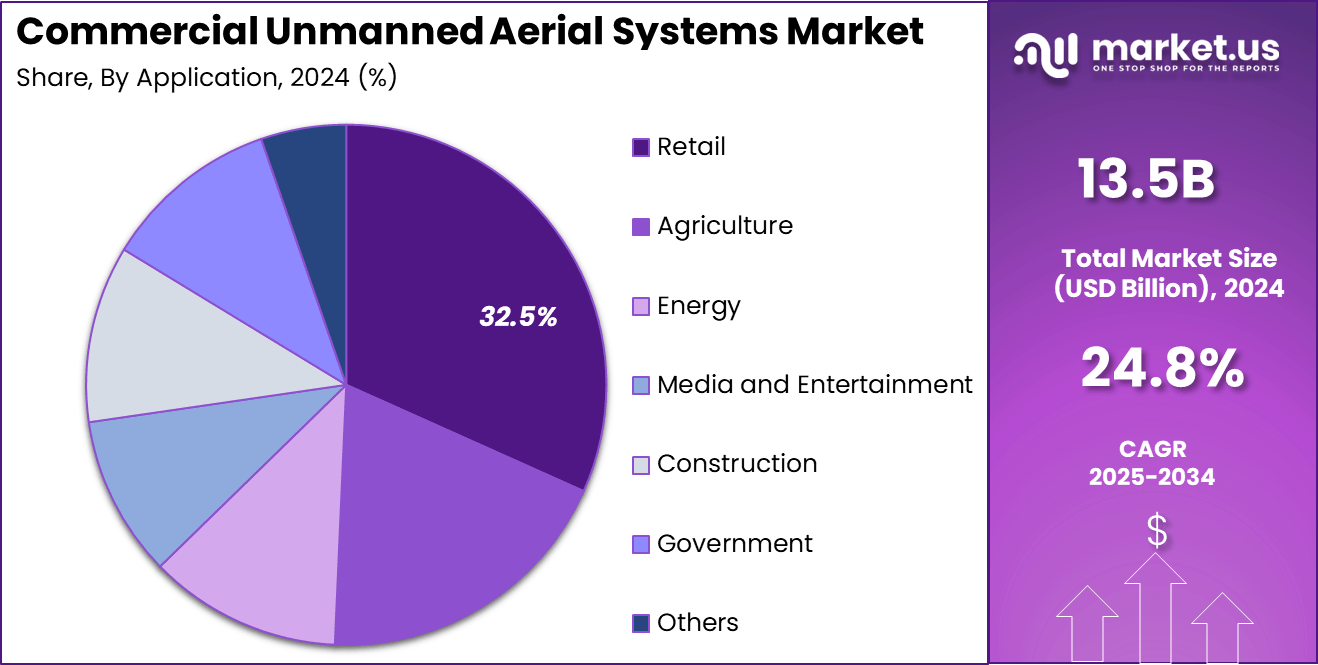

The Global Commercial Unmanned Aerial Systems Market size is expected to be worth around USD 123.3 Billion By 2034, from USD 13.5 billion in 2024, growing at a CAGR of 24.8% during the forecast period from 2025 to 2034. In 2024, North America held a dominan market position, capturing more than a 39.2% share, holding USD 5.2 Billion revenue.

The Commercial Unmanned Aerial Systems (UAS) market is growing steadily as businesses and various industries increase their reliance on drones to improve efficiency and data collection. These systems, which operate autonomously or through remote control, are used widely in sectors like agriculture, construction, delivery, surveillance, and infrastructure inspection.

Top driving factors for this market include advancements in drone technology such as longer battery life and better sensors, along with increased affordability. The integration of artificial intelligence and machine learning allows these drones to navigate autonomously and analyze data on the fly, boosting their usefulness and appeal.

According to Sci-Tech Today, the global drone sector is seeing rapid expansion with more than 4,000 organizations worldwide and 15,000 in China actively engaged. Military drones remain the largest contributor, accounting for 48.6% of total revenue, while rotary blade drones lead by technology type, capturing 62.4% of the market share.

In terms of applications, the real estate and construction sectors dominate with 26.4% of total revenue, highlighting drones’ value in aerial imaging, surveying, and project monitoring. Geology and mining represent a steady 6% to 6.5% share, a level expected to continue over the next five years as industries adopt drones for exploration and resource management.

Regionally, China led the drone industry in 2024, generating USD 1.394 billion in revenue. Its leadership is supported by large-scale adoption across commercial, industrial, and defense applications, combined with strong domestic manufacturing and government backing. This positions China as the most influential market for drones globally.

Demand analysis shows rapid adoption mainly in agriculture for precision farming, construction for site monitoring, and logistics for delivery services. UAVs reduce labor costs and increase safety by performing dangerous or hard-to-reach tasks. Their ability to provide detailed aerial views and precise data reduces the need for manual inspections and speeds up decision-making processes, driving demand further.

Key Insight Summary

- By product, Fixed Wing UAVs dominated the market with a 38.6% share.

- By application, the Retail segment led with 32.5% share.

- North America held the largest regional share at 39.2%.

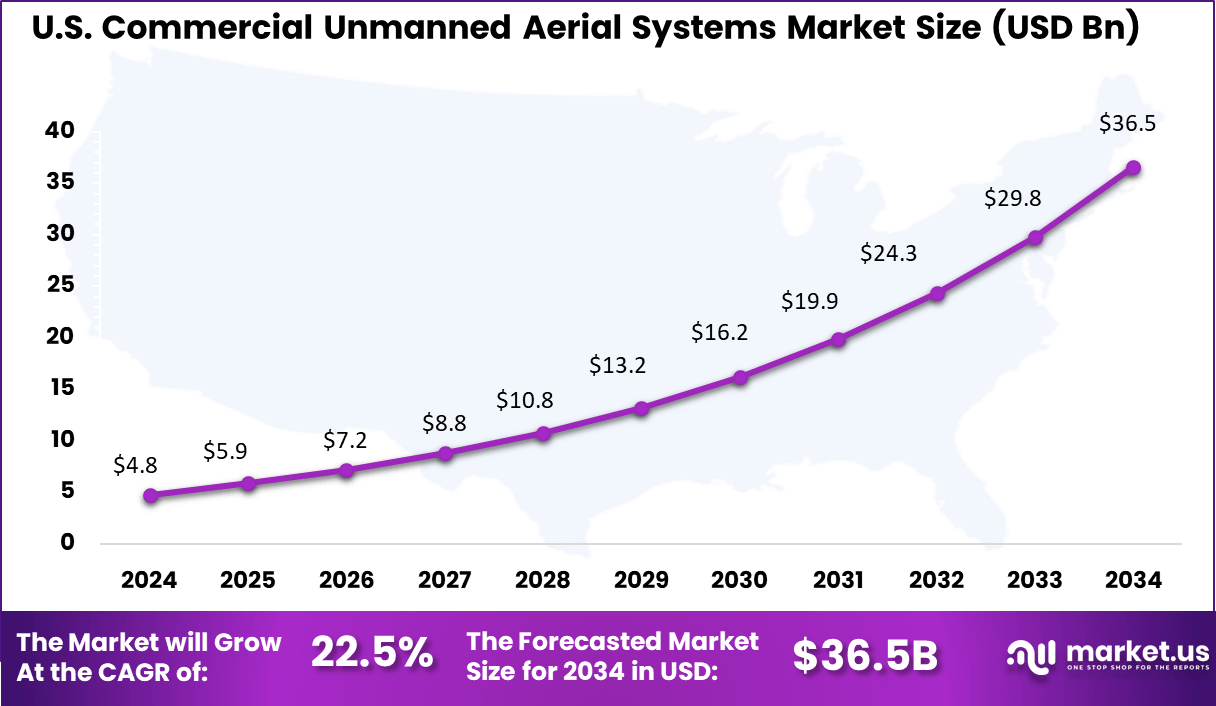

- The U.S. market was valued at USD 4.48 Billion in 2024, expanding at a strong CAGR of 22.5%.

Analysts’ Viewpoint

Increasing adoption of technologies such as AI-driven navigation systems, high-resolution imaging like LiDAR, and extended battery capacity are key to the expanding use of commercial UAS. These technologies enable longer and more efficient flight operations, better obstacle detection, and richer data capture, which are critical reasons enterprises choose to adopt drone solutions over traditional methods.

Investment opportunities in this market are growing as companies recognize the potential for automation and cost savings. Investments focus on R&D to improve drone functionality, integration with software platforms for data management, and development of specialized UAVs tailored to specific industries.

Business benefits from adopting commercial UAS include enhanced productivity, improved safety for human workers, and access to real-time, accurate data that supports better decisions. These systems also help companies reduce operational costs, streamline workflows, and add value by performing tasks faster and at lower risks compared to manual alternatives.

Role of Generative AI

Generative AI plays an increasingly vital role in commercial unmanned aerial systems, improving autonomous flight and decision-making capabilities. Recent studies show that generative AI enhances drone navigation accuracy by approximately 25% and improves object tracking precision by 40%.

This means drones equipped with generative AI can autonomously maneuver through complex environments more reliably and conduct surveillance or inspections with better quality. AI-driven code generation has accelerated drone software development by 20 times faster than traditional methods, supporting quicker innovation in autonomous operations.

Government-led Investments

Aspect Details Statistics Funding Rounds Major funding for drone manufacturers aligned with federal contracts $47 million in Series A funding for Firestorm Labs; €160 million financing for Quantum Systems Legislative Acts One Big Beautiful Bill Act allocations for drone industrial base and autonomy testing $1.4 billion for small UAS industrial base; $2.1 billion for medium unmanned vessel development; $250 million for digital autonomy test environments Policy Priorities Executive orders prioritizing US-made drones and eVTOL pilot programs 40% surge in stock prices of US drone tech firms since early 2025 Law Enforcement Use Increase in public safety drone deployments in various states 260%+ increase in law enforcement drone deployments in Minnesota over several years State Funding State-level drone infrastructure and modernization allocations $7.5 million allocated by Michigan for drone infrastructure projects Market Revenue and Growth US drone market revenue and growth trajectory Approximately $25 billion revenue in 2024 with strong 2025 momentum Regional Focus: North America

North America accounts for about 39.2% of the commercial unmanned aerial systems market, largely supported by advanced drone infrastructure, regulatory frameworks that are evolving to accommodate commercial UAVs, and a strong presence of technology adoption across industries.

The region has become a hub for developing drone-enabled solutions in sectors such as construction, agriculture, media, and security, making UAVs more integrated into business operations. Continuous investments into air traffic management systems for drones are also helping strengthen the ecosystem across North America.

A key driver for North American adoption has been the proactive role of regulators and industry stakeholders in shaping consistent rules for commercial UAV usage. This clarity has encouraged businesses to adopt drones with more confidence, particularly in inspection-heavy industries like energy and telecommunications.

Country Spotlight: United States (4.48 bn market size)

The United States represents a significant share within North America, with its commercial UAV market valued at around 4.48 billion. This dominance stems from large-scale applications across agriculture, construction, mining, logistics, and media, where UAV platforms are deployed to improve efficiency, reduce costs, and enhance data-driven decision making.

The country’s strong innovation ecosystem, with research centers and universities leading advancements in autonomy and communication technologies, further supports UAV adoption. Additionally, the United States benefits from a well-defined legal and operational framework that is progressively adapting to the rising demand for drone solutions.

Industry stakeholders, policymakers, and developers are actively working together to ensure safe integration of drones into commercial airspace. These collective efforts have positioned the U.S. as a global leader in UAV adoption, setting benchmarks for how commercial drones can transform industrial operations at scale.

By Product: Fixed Wing UAVs

In 2024, fixed wing UAVs accounted for 38.6% of the commercial unmanned aerial systems market, reflecting their strong suitability for long-range operations and endurance flights. Their aerodynamic design allows them to cover larger distances on minimal power, making them indispensable for applications like agricultural mapping, border surveillance, and infrastructure inspection.

This efficiency, combined with their ability to operate over wide terrains, positions them as a preferred choice for enterprises that need reliable and large-scale data collection. The adoption of fixed wing UAVs continues to grow as industries demand high-quality geospatial and operational data.

Equipped with advanced sensors, imaging technology, and communication systems, these drones bring precise data-driven insights to operators. Although they require dedicated launch and landing spaces, their strength lies in efficiency and coverage, which makes them highly effective for mapping and surveying large landscapes where speed and endurance are critical.

By Application: Retail

In 2024, the retail application segment represented 32.5% of the commercial UAV market, showing the rising role of drones in logistics and customer service. UAV technology has been transformative in tackling last-mile delivery challenges by reducing delivery times and ensuring accessibility even in remote areas.

Retailers, especially those focusing on e-commerce growth, benefit from UAVs’ ability to ease supply chain tension and enhance delivery speed, creating notable interest across online and offline players alike. Beyond logistics, retail companies are actively exploring the use of drones for things like live promotions, surveying warehouse inventory, and engaging customers through new experiences.

Their potential to lower operational costs and enhance efficiency is expected to make UAV integration more common across retail ecosystems. As regulations develop further, drones have the potential to redefine how modern businesses interact with their customers and manage supply chain processes.

Emerging Trends

Emerging trends in commercial UAS emphasize AI integration with 5G connectivity for real-time data processing and drone-to-cloud communication. The remote operation drone segment accounts for roughly 44.3% of total commercial drone activity in 2025, reflecting widespread adoption for real-time inspection and monitoring in sectors like energy, agriculture, and logistics.

Swarm technology is gaining ground, enabling coordinated drone fleets for tasks such as environmental monitoring and search-and-rescue. Technologies extending battery life and increasing payload capacity remain growth drivers, facilitating longer missions and heavier equipment transport. Integration of AI-powered image analysis tools is improving data collection efficiency by up to 35%, supporting more accurate agricultural monitoring and infrastructure surveys.

Growth Factors

Growth factors for commercial UAS include escalating adoption in industries like construction, agriculture, and public safety. For instance, drones are expected to reduce inspection costs by 20% and increase operational speeds by 15%, boosting productivity in agriculture and infrastructure management.

Regulatory bodies are progressively approving beyond visual line of sight operations, which significantly broadens commercial use cases. Investments in drone software development and AI-enhanced autonomous functions have increased by more than 30% in the last year, reflecting rising confidence in commercial applications.

Latest Announcements

Latest announcements from industry events in 2025 highlight new commercial drone models with modular payloads and extended flight times of up to 90 minutes. Emergency response drones now feature AI-powered autonomous decision-making that can reduce response times by nearly 30% during disaster assessments.

AI integration with unmanned traffic management systems is advancing quickly, enabling safer urban drone operations with real-time conflict detection. Strategic collaborations between AI providers and drone manufacturers have accelerated development cycles by 20%, fostering faster deployment of next-generation autonomous systems. These advances ensure drones are becoming more integral to critical infrastructure and public services.

Key Market Segments

By Product

- Fixed wing UAV

- Rotary blade UAV

- Hybrid UAV

- Nano UAV

By Application

- Retail

- Agriculture

- Energy

- Media and Entertainment

- Construction

- Government

- Others

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Expanding Industrial Applications

The growing adoption of commercial unmanned aerial systems across multiple industries is a key driver of market growth. Sectors such as agriculture, construction, surveying, and infrastructure inspection increasingly use these systems to improve efficiency and data accuracy.

This versatility allows commercial UAS to perform tasks like aerial imaging, crop spraying, site mapping, and real-time monitoring, which were previously more costly or difficult to execute. The demand for efficient aerial data collection is fueling investments and adoption in these industries, pushing the market forward steadily.

Technological advancements, including enhanced battery life, sensor precision, and AI-enabled functionalities, have further boosted performance, allowing longer flight times and safer operations. As industries realize the cost-saving and productivity benefits from integrating UAS into their workflows, the commercial market’s growth momentum continues to build. This widespread utility is a foundational growth driver for the sector.

Restraint

Regulatory and Security Limitations

Strict government regulations on drone operations pose a notable restraint on the commercial UAS market. Variations in rules across countries regarding flight altitude, permissible zones, pilot licensing, and visual line-of-sight requirements restrict operational flexibility.

Compliance with such regulatory frameworks often increases the time and cost burden on businesses adopting UAS technology. Additionally, concerns related to data privacy and national security, especially involving camera-equipped drones, lead some governments to impose stringent restrictions or bans on drones from specific manufacturers.

These regulatory complexities create uncertainty and slow down large-scale commercial deployment. Companies and operators must navigate diverse and evolving guidelines, complicating cross-border operations and limiting market expansion speed. Without a harmonized framework, regulations remain a significant market growth barrier.

Opportunity

Integration with AI and Data Analytics

One of the most promising opportunities in the commercial UAS market is the growing integration of artificial intelligence and advanced data analytics. AI-enabled drones can collect and process complex datasets in real time, providing actionable insights for industries like agriculture (precision farming), construction (progress tracking), energy (infrastructure inspection), and logistics (route optimization).

This integration enhances UAS functionalities, transforming them from mere data collectors into intelligent operational tools. As AI technologies mature, there is potential for broader autonomous capabilities, allowing drones to perform complex missions with minimal human oversight.

This advancement is opening new use cases in areas such as asset management, emergency response, and automated delivery services, expanding the addressable market substantially. Companies that innovate and develop workflow-optimized, AI-integrated UAS will likely capture significant market share going forward.

Challenge

Technological and Public Perception Barriers

Despite advances, technology limitations like battery life and reliable communication links continue to challenge the commercial UAS market. Limited flight duration restricts longer missions and can affect operational efficiency.

Ensuring secure and robust command and control systems is crucial to prevent unauthorized access and cyber threats, which increases complexity and cost. Public skepticism around privacy and safety also hinders acceptance. Concerns about surveillance misuse, data security breaches, and potential accidents with drones create resistance among communities and regulators.

This challenge requires transparent usage policies and stringent security standards. Overcoming these technological and perception barriers is essential for achieving widespread adoption and realizing the commercial potential of unmanned aerial systems.

Competitive Analysis

The commercial unmanned aerial systems market is led by DJI Innovations, which dominates with its wide portfolio of drones for both consumer and enterprise use. Its strengths in affordability, imaging capabilities, and strong global distribution make it the most influential player. Other firms such as Parrot SA, Yuneec Holding, Draganfly, and EHang are also expanding adoption in areas like photography, surveying, logistics, and urban mobility.

Defense-linked companies including BAE Systems, Elbit Systems, Israel Aerospace Industries, Textron, General Dynamics, and Turkish Aerospace Industries are increasingly entering the commercial space. Their expertise in aerospace and defense supports the development of drones with high endurance, long-range communication, and strong security features, catering to industries such as energy, mining, and infrastructure.

Specialized players like AeroVironment, Aurora Flight, Challis Heliplane UAV, Prox Dynamics, SAIC, and Boeing contribute to niche applications through fixed-wing and hybrid designs. These solutions are particularly suited for agriculture, logistics, and environmental monitoring, ensuring diversity in the market and fueling growth across multiple industry sectors.

Top Key Players in the Market

- AeroVironment Inc.

- Aurora Flight

- BAE Systems plc

- Challis Heliplane UAV Inc.

- DJI Innovations

- Draganfly, Inc.

- EHang

- Elbit Systems Ltd.

- General Dynamics Corporation

- Israel Aerospace Industries

- Parrot SA

- Prox Dynamics AS

- SAIC

- Textron Inc.

- The Boeing Company

- Turkish Aerospace Industries Inc.

- Yuneec Holding Ltd.

- Others

Recent Developments

- In September 2025, Envirotech Vehicles announced successful development of an American-made heavy-lift drone capable of carrying up to 1,500 lbs, targeting agriculture and wildfire protection applications. This represents a breakthrough in payload capacity for commercial UAS, expanding their use in critical environmental missions.

- In August 2025, ideaForge introduced the Q6V2 GEO UAV designed for geospatial intelligence applications. The UAV features modular payloads, survey-grade accuracy, and suitability for all-terrain operations, underlining the trend toward high-precision and data-driven commercial drone solutions.

- In May 2025, Airbus U.S. Space & Defense entered a strategic partnership with L3Harris Technologies to develop the MQ-72C Logistics Connector, an unmanned variant of the UH-72 Lakota helicopter, aimed at flexible logistics missions in contested environments. This partnership highlights increased focus on modular, open-systems UAS capable of diverse mission adaptability.

Report Scope

Report Features Description Market Value (2024) USD 13.5 Bn Forecast Revenue (2034) USD 123.3 Bn CAGR(2025-2034) 24.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Product (Fixed wing UAV, Rotary blade UAV, Hybrid UAV, Nano UAV), By Application (Agriculture, Retail, Energy, Media and Entertainment, Construction, Government, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape AeroVironment Inc., Aurora Flight, BAE Systems plc, Challis Heliplane UAV Inc., DJI Innovations, Draganfly, Inc., EHang , Elbit Systems Ltd., General Dynamics Corporation, Israel Aerospace Industries, Parrot SA, Prox Dynamics AS, SAIC, Textron Inc., The Boeing Company, Turkish Aerospace Industries Inc., Yuneec Holding Ltd., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Commercial Unmanned Aerial Systems MarketPublished date: Sept. 2025add_shopping_cartBuy Now get_appDownload Sample

Commercial Unmanned Aerial Systems MarketPublished date: Sept. 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- AeroVironment Inc.

- Aurora Flight

- BAE Systems plc

- Challis Heliplane UAV Inc.

- DJI Innovations

- Draganfly, Inc.

- EHang

- Elbit Systems Ltd.

- General Dynamics Corporation

- Israel Aerospace Industries

- Parrot SA

- Prox Dynamics AS

- SAIC

- Textron Inc.

- The Boeing Company

- Turkish Aerospace Industries Inc.

- Yuneec Holding Ltd.

- Others

Our Clients

- 158211

- Sept. 2025