Quick Navigation

Report Overview

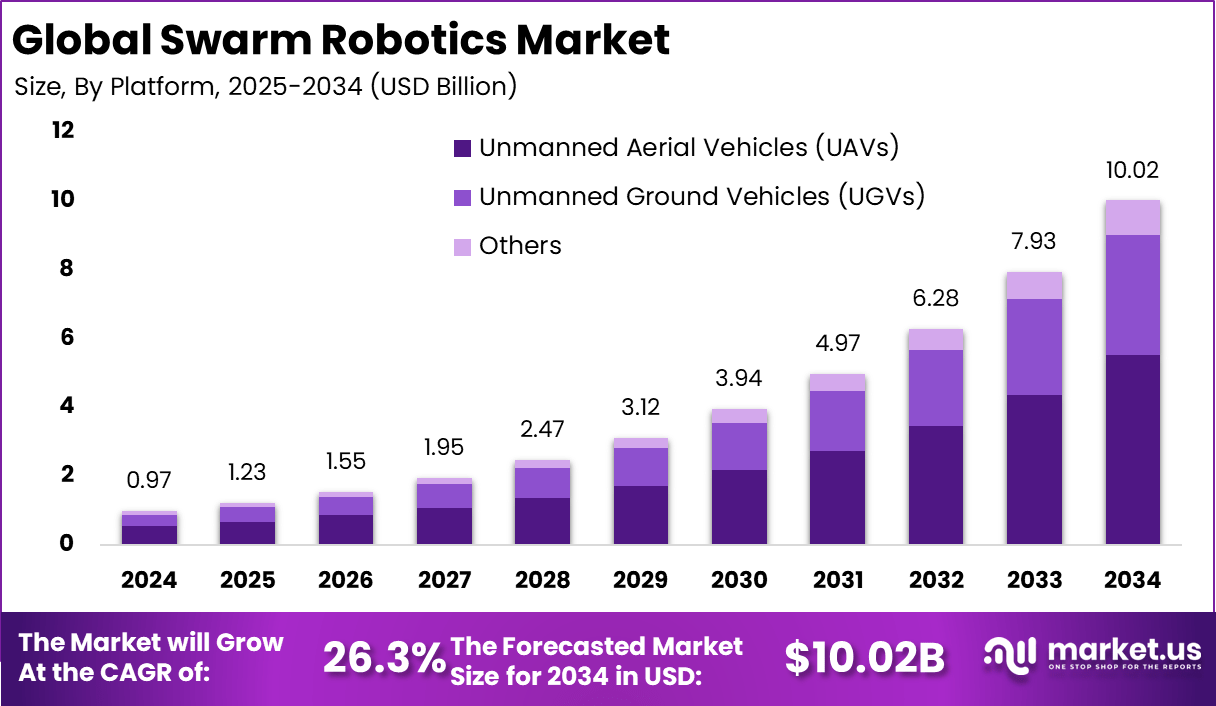

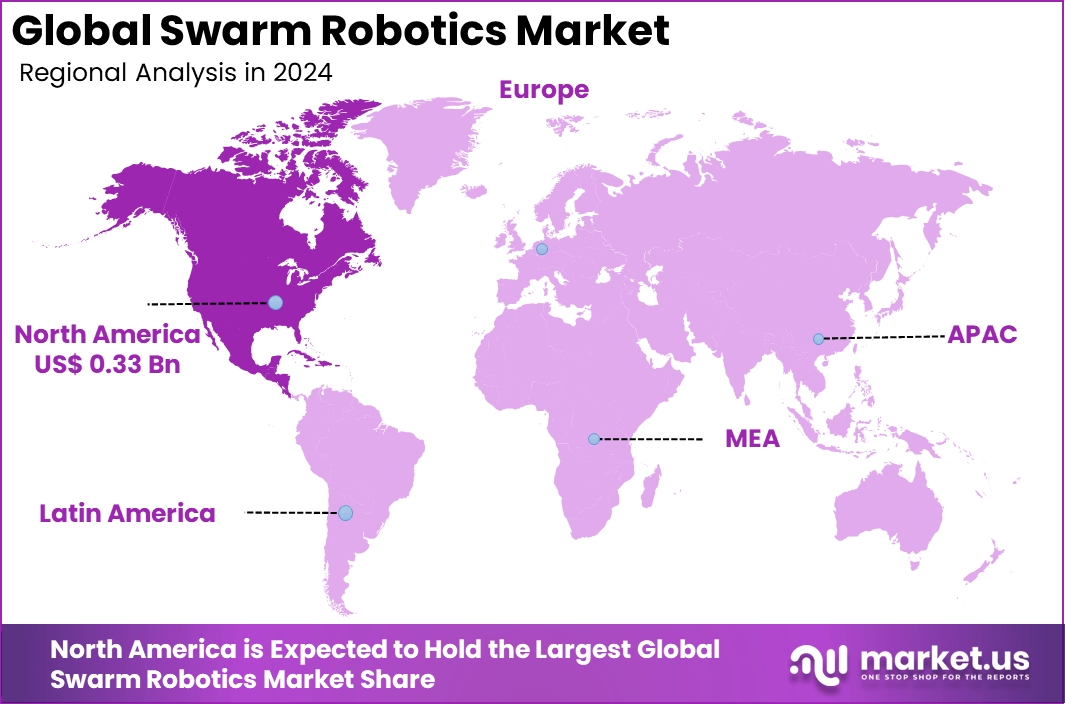

The Global Swarm Robotics Market size is expected to be worth around USD 10.02 billion by 2034, from USD 0.97 billion in 2024, growing at a CAGR of 26.3% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 35% share, holding USD 0.33 billion in revenue.

Swarm robotics refers to systems composed of numerous relatively simple robots that collaborate to achieve tasks through decentralized control, drawing inspiration from social insects like ants or bees. Core characteristics include fault tolerance, scalability, flexibility, and local sensing and communication capabilities without reliance on a central controller.

The global swarm robotics market is experiencing robust expansion driven by increasing automation, advancements in AI and IoT, and rising demand across sectors such as defense, agriculture, logistics, healthcare, and environmental monitoring. Top driving factors include the rising need for efficient, cost‑effective autonomous systems in defense (for surveillance, reconnaissance, and combat support), industrial automation, smart agriculture (e.g., crop monitoring), and last‑mile logistics.

Investment opportunities are emerging in platform development – especially unmanned aerial vehicles (UAVs), ground vehicles (UGVs), and underwater robots – plus swarm‑robotics‑as‑a‑service models, on‑demand deployment for logistics and defense, and expanded integration with IoT infrastructure. Business benefits are clear: enhanced operational efficiency through parallel tasking, lower labor needs, improved safety in hazardous environments, adaptability, and cost savings over centralized systems.

The regulatory landscape remains partly undefined, as standards for autonomous, collaborative robotics continue to evolve. Defense applications face export controls and military-use restrictions. UI safety, airspace navigation, and cross-border data regulations affect commercial deployment – especially in UAV and surveillance use cases.

For instance, in February 2025, researchers at UC Santa Barbara and TU Dresden developed swarm robots capable of autonomously assembling and reconfiguring themselves to perform complex tasks. This breakthrough demonstrates enhanced adaptability and coordination, paving the way for more versatile and resilient robotic systems applicable in manufacturing, search-and-rescue, and space exploration.

Key Takeaway

- In 2024, the Unmanned Aerial Vehicles (UAVs) segment led the global swarm robotics market, accounting for 55% of the total share, reflecting growing demand for autonomous aerial coordination in military and surveillance operations.

- The Drones segment dominated by securing a 62% market share in 2024, driven by increased deployment in both commercial and tactical scenarios requiring swarm intelligence.

- Security, Inspection, and Monitoring applications held the top position among use cases in 2024, capturing 31% of the market, supported by rising adoption in critical infrastructure monitoring and real-time threat assessment.

- Military & Defense emerged as the leading end-use sector, commanding a 40% market share in 2024, fueled by global investments in autonomous systems for combat support, reconnaissance, and tactical advantage.

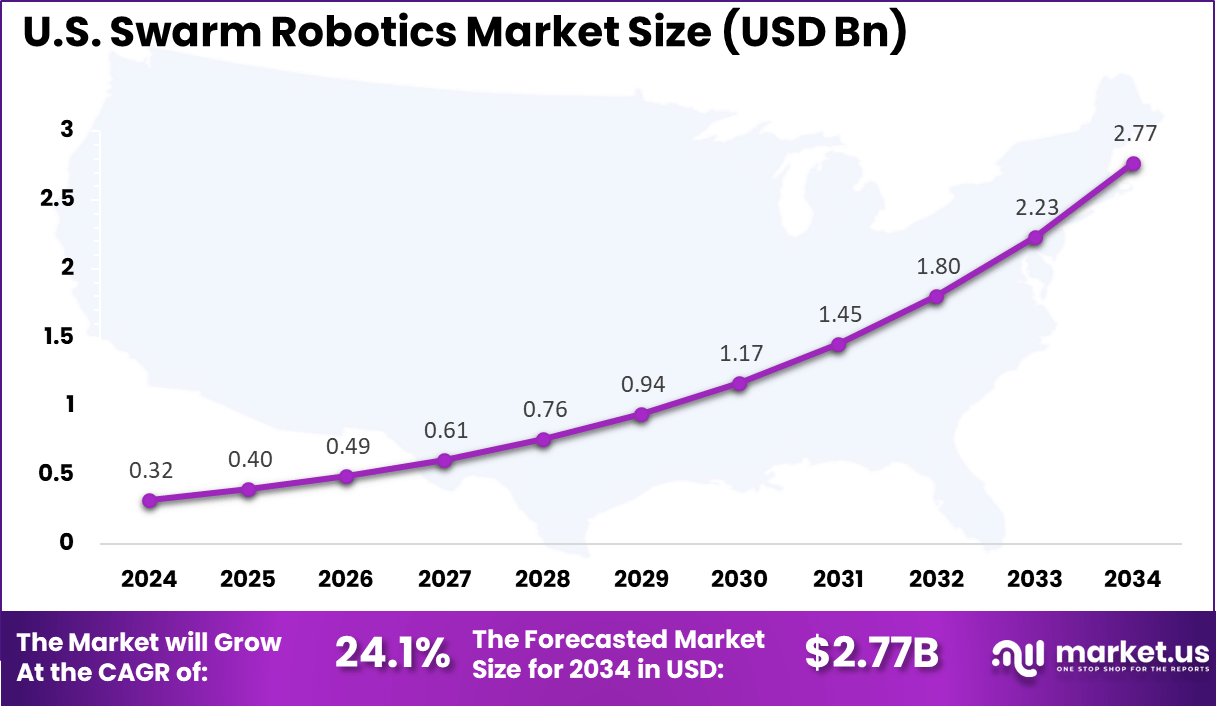

- The U.S. Swarm Robotics Market was valued at USD 0.32 Billion in 2024, with a modest but steady CAGR of 24.1%, signaling early-stage adoption and strategic experimentation across defense programs.

- North America retained a dominant role, holding over 35% of the global market share in 2024, bolstered by strong defense spending, advanced robotics infrastructure, and favorable government initiatives.

U.S. Swarm Robotics Market Size

The US Swarm Robotics Market is valued at approximately USD 0.32 Billion in 2024 and is predicted to increase from USD 0.94 Billion in 2029 to approximately USD 2.77 Billion by 2034, projected at a CAGR of 24.1% from 2025 to 2034.

A strong technological base, substantial investment in robotics and AI research, and active government support, particularly from the defense and emergency response sectors, are among the reasons for the rapidly expanding U.S. swarm robotic market size. Leading tech companies and research institutes drive innovation, while the increasing use of automation in various industries such as agriculture, logistics, and healthcare further encourages market growth.

For instance, in May 2024, the U.S. military deployed nano drone swarms for special operations missions, enhancing reconnaissance and tactical capabilities. These ultra-small drones operate collaboratively to gather intelligence in complex environments, offering real-time situational awareness while minimizing risk to personnel. This deployment underscores the strategic value of swarm robotics in modern warfare and special operations.

In 2024, North America held a dominant market position in the Global Swarm Robotics Market, capturing more than a 35% share, holding USD 0.33 billion in revenue. North America is a major player in the global swarm robotics market due to its advanced technological ecosystem, significant R&D investments, and strong presence of key industry players in both robotics and AI.

For instance, In May 2025, North American companies BigBear AI and Hardy Dynamics announced a collaboration to advance AI orchestration for U.S. Army drone swarm operations under Project Linchpin. This initiative focuses on enhancing autonomous coordination, real-time decision-making, and operational efficiency of drone swarms in complex military environments. The partnership reflects North America’s leadership in developing cutting-edge swarm robotics solutions for defense applications.

Platform Analysis

In 2024, the Unmanned Aerial Vehicles (UAVs) segment held a dominant market position, capturing more than a 55 % share. This leadership is attributed to several converging trends. First, the inherent agility and rapid deployment capabilities of aerial swarms have made UAVs the preferred choice across sectors such as defense, agriculture, and infrastructure inspection.

Their capacity to cover extensive areas quickly and gather high-resolution data has driven strong demand. Financial forecasts further reinforce this dominance, as UAV-based swarm systems benefit from sustained investments in drone technology and networked coordination, keeping that segment ahead of ground and other platforms.

For Instance, in January 2025, Norway’s Defence Research Establishment reported significant progress in UAV swarm technology, advancing autonomous coordination and control systems for military applications. These developments enhance the operational capabilities of drone swarms in surveillance, reconnaissance, and combat scenarios, emphasizing decentralized decision-making and resilience. Norway’s advancements contribute to the growing global momentum in swarm robotics for defense.

Type Analysis

In 2024, the Drones segment held a dominant market position, capturing a 62% share of the Global Swarm Robotics Market. Demand in this sector is driven primarily by the use of drone swarm technology for aerial military surveillance, border patrol, disaster management, and agricultural monitoring, where coordinated aerial operations provide greater efficiency with increased coverage.

Furthermore, government initiatives and significant investments in drone technology for both military and commercial purposes have established the drone segment as the primary market for the swarm robotics industry.

For instance, In January 2024, the Pentagon began testing next-generation AI-powered swarm drones and unmanned ships to enhance military capabilities. These systems leverage advanced autonomous coordination and real-time decision-making to operate collaboratively in contested environments. The initiative reflects the Pentagon’s strategic investment in swarm robotics to improve situational awareness, force multiplication, and mission adaptability in future warfare.

Application Analysis

In 2025, The Security, Inspection, and Monitoring segment held a dominant market position, capturing a 31% share of the Global Swarm Robotics Market. This dominance is due to the growing need for efficient, real-time surveillance and inspection solutions across critical infrastructure, industrial sites, and national borders.

By utilizing swarm robotics, it becomes easier to cover large or risky areas quickly and efficiently while also reducing operational costs and improving threat detection. Swarm-based monitoring has become more popular in the public and private sectors due to the integration of AI-driven analytics and modern sensor technologies, which have made it the preferred method for security and inspection tasks.

For Instance, in March 2025, HTXplains, Singapore’s Defence Technology Agency, showcased advancements in swarm robotics for security, inspection, and monitoring applications. Their innovative robotic swarms are designed to conduct autonomous surveillance, infrastructure inspection, and threat detection, improving operational efficiency and safety in complex environments.

End-Use Industry Analysis

In 2024, Military & Defense segment held a dominant market position, capturing more than a 40 % share. This leadership has been driven by the increasing reliance on autonomous systems to enhance battlefield operations while reducing risk to personnel.

Swarm robotics enables coordinated missions – such as surveillance, reconnaissance, and logistics – in contested or hazardous environments, offering strategic advantages through redundancy, adaptability, and real-time responsiveness.

Governments across North America, Europe, and Asia-Pacific have significantly increased defense budgets to support modernization programs, leading to accelerated procurement of unmanned systems that operate collaboratively. The result is a highly scalable and resilient force multiplier that is outperforming traditional single-platform systems

For Instance, in April 2024, Red Cat Holdings partnered with Sentien Robotics to develop advanced multidomain drone swarming capabilities across land, air, and sea. This collaboration aims to strengthen autonomous unmanned systems for defense and security applications, improving coordinated operations and situational awareness. The partnership reflects a growing interest in leveraging swarm robotics for complex, multi-environment missions that enhance national security and operational effectiveness.

Key Market Segments

By Platform

- Unmanned Ground Vehicles (UGVs)

- Unmanned Aerial Vehicles (UAVs)

- Others

By Type

- Drones

- Robots

- Others

By Application

- Security, Inspection, and Monitoring

- Mapping and Surveying

- Search & Rescue and Disaster Relief

- Supply Chain and Warehouse Management

- Others

By End-Use Industry

- Military & Defense

- Industrial

- Agriculture

- Healthcare

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Rising Demand for Automation and Efficiency

Swarm Robotics has gained a reputation for providing cost-effective and efficient solutions to complex tasks like exploration, search and rescue mission execution, environmental monitoring (including tracking), and precision agriculture. The combination of intelligence and adaptability makes it possible for robotic swarms to perform better than individual robots, particularly in highly unpredictable environments.

For instance, In September 2023, Meraque, a Malaysian startup, introduced its first autonomous ground vehicle (AGV) designed for plantation management, exemplifying the rising demand for automation and efficiency in agriculture. This development reflects the broader trend of adopting swarm robotics and autonomous systems to optimize labor-intensive tasks, increase precision, and reduce operational costs.

Restraint

Complexity in Coordination and Communication

Managing large-scale autonomous robot swarms requires the use of sophisticated communication protocols and control algorithms. Real-time coordination and task execution pose challenges in wireless technologies, primarily due to bandwidth constraints, latency, or interference. These technical barriers limit the operational reliability and scalability of mission-critical applications, and this restrains broader market adoption.

For instance, in October 2024, according to AZoRobotics, managing the complexity of coordination and communication remains a significant challenge in swarm robotics. Effective operation of large robot swarms requires sophisticated algorithms and robust communication protocols to ensure seamless interaction and task execution. Current limitations such as bandwidth constraints, latency, and interference hinder real-time coordination, impacting the reliability and scalability of swarm systems in dynamic environments.

Opportunities

Expansion into New Verticals

Beyond traditional sectors like food, defense, aviation, and aerospace, swarm robotics is increasingly being adopted in healthcare, emergency response, mining, construction, and oil and gas. Its ability to improve efficiency, safety, and precision in high-risk environments presents strong growth potential. Strategic market entry backed by customized technologies and regulatory support is expected to drive adoption in these emerging areas.

For instance, In April 2025, H2 Clipper introduced a patented swarm robotics innovation designed to transform manufacturing processes in the aviation and aerospace sectors. Their technology leverages coordinated robotic swarms to improve precision, efficiency, and scalability in complex assembly tasks. This breakthrough enables faster production cycles and reduced operational costs, positioning it as a key innovator in industrial automation for high-value manufacturing industries.

Challenges

Security and Ethical Concerns

The security and ethical concerns arise from the autonomous nature of swarm robotics, particularly in defense and critical infrastructure. The prevention of malicious interference or unintended consequences requires secure communication and operation. The effective management of these concerns through the use of strong governance frameworks and transparent stakeholder participation is crucial for sustainable market growth.

For instance, in November 2023, growing concerns emerged regarding the legal and ethical implications of AI-powered drones in warfare. Policymakers debated regulation, accountability, and compliance with international law. The risk of unintended escalation was a key focus. It shows the urgent need for clear governance frameworks as autonomous military systems advance.

Latest Trends

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming swarm robotics by enhancing robots’ coordination and autonomous decision-making capabilities. These technologies enable swarms to analyze real-time data, adjust to changing environments, and perform difficult tasks without human intervention. They significantly improve the efficiency, scalability, and resilience of swarm robotic systems, driving broader adoption across industries such as agriculture, logistics, and defense.

For instance, in January 2023, OffWorld announced it is accepting development contracts for new AI-powered swarm robots aimed at industrial and extraterrestrial applications. These autonomous robotic swarms are designed to operate collaboratively in challenging environments, such as mining on Earth and other planetary surfaces, enhancing efficiency and operational scalability. OffWorld’s initiative underscores the expanding role of swarm robotics powered by AI in both commercial and space exploration sectors.

Key Players Analysis

One of the leading players in the market, In February 2025, NASA advanced its research on swarm robotics by collaborating with Autonomous Robotics Ltd to develop intelligent robotic systems for space and terrestrial applications.

These autonomous swarms are designed to enhance exploration, maintenance, and construction tasks in space environments, leveraging advanced sensing and decision-making capabilities. This partnership highlights NASA’s commitment to integrating swarm robotics to support future missions and improve operational efficiency beyond Earth.

Top Key Players in the Market

- Hydromea

- Boston Dynamics

- SwarmFarm Robotics

- Sentinen Robotics

- Berkeley Marine Robotics Inc

- Swisslog Holding AG

- Swarm Technology

- Kion Group AG

- Farobot Inc.

- Unbox Robotics Pvt Ltd

- Barnstorm Agtech

- Ambots

- Autonomous Robotics Ltd

- Others

Recent Developments

- In February 2025, SwarmFarm Robotics, a pioneer in autonomous agricultural technology, established a new manufacturing facility in Queensland’s Darling Downs region. This expansion supports increased production of its ‘SwarmBots,’ designed to enhance precision farming through autonomous operation, improving crop yields and reducing environmental impact.

- In May 2025, researchers introduced a new generation of swarm robots that can physically link and coordinate tasks without centralized control. This breakthrough enhances flexibility and adaptability in critical applications like search-and-rescue, environmental monitoring, and construction. The innovation highlights a major leap in modularity and decentralized coordination within swarm robotics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 0.97 Bn |

| Forecast Revenue (2034) | USD 10.02 Bn |

| CAGR (2025-2034) | 26.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Platform (Unmanned Ground Vehicles (UGVs), Unmanned Aerial Vehicles (UAVs), Others), By Type (Drones, Robots, Others), By Application (Security, Inspection, and Monitoring, Mapping and Surveying, Search & Rescue and Disaster Relief, Supply Chain and Warehouse Management, Others), By End-Use Industry (Military & Defense, Industrial, Agriculture, Healthcare, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Hydromea, Boston Dynamics, SwarmFarm Robotics, Sentinen Robotics, Berkeley Marine Robotics Inc, Swisslog Holding AG, Swarm Technology, Kion Group AG, Farobot Inc., Unbox Robotics Pvt Ltd, Barnstorm Agtech, Ambots, Autonomous Robotics Ltd, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |