Quick Navigation

Report Overview

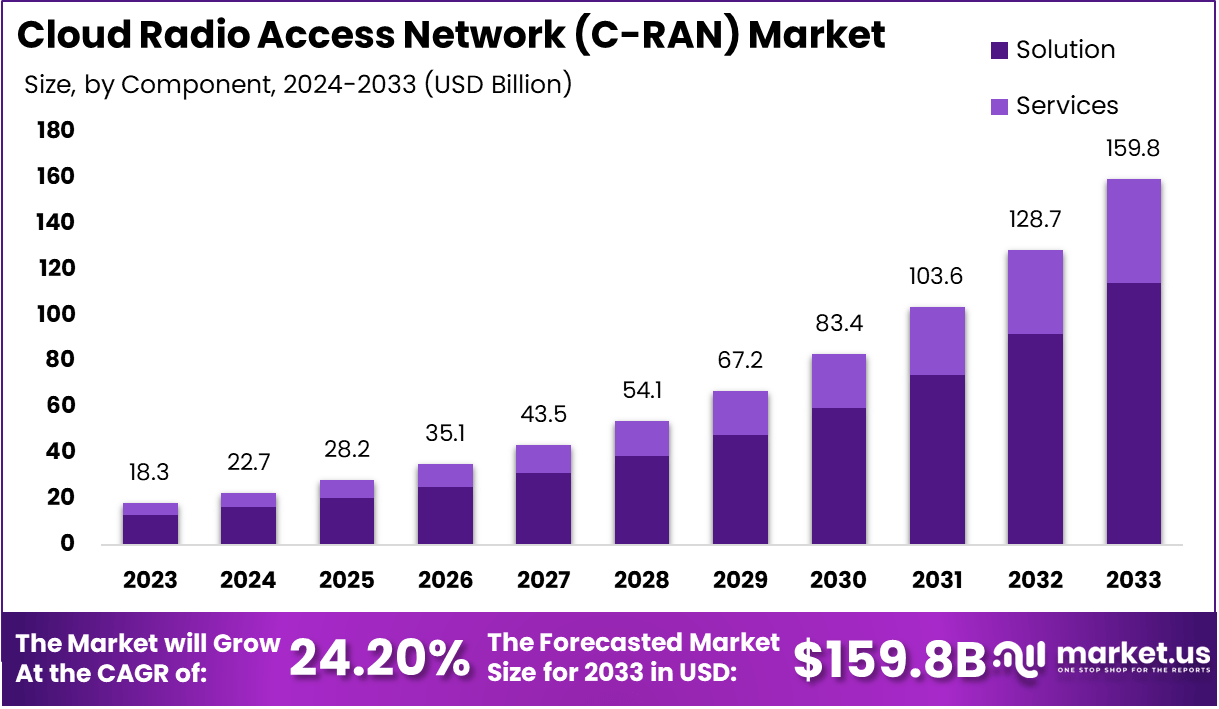

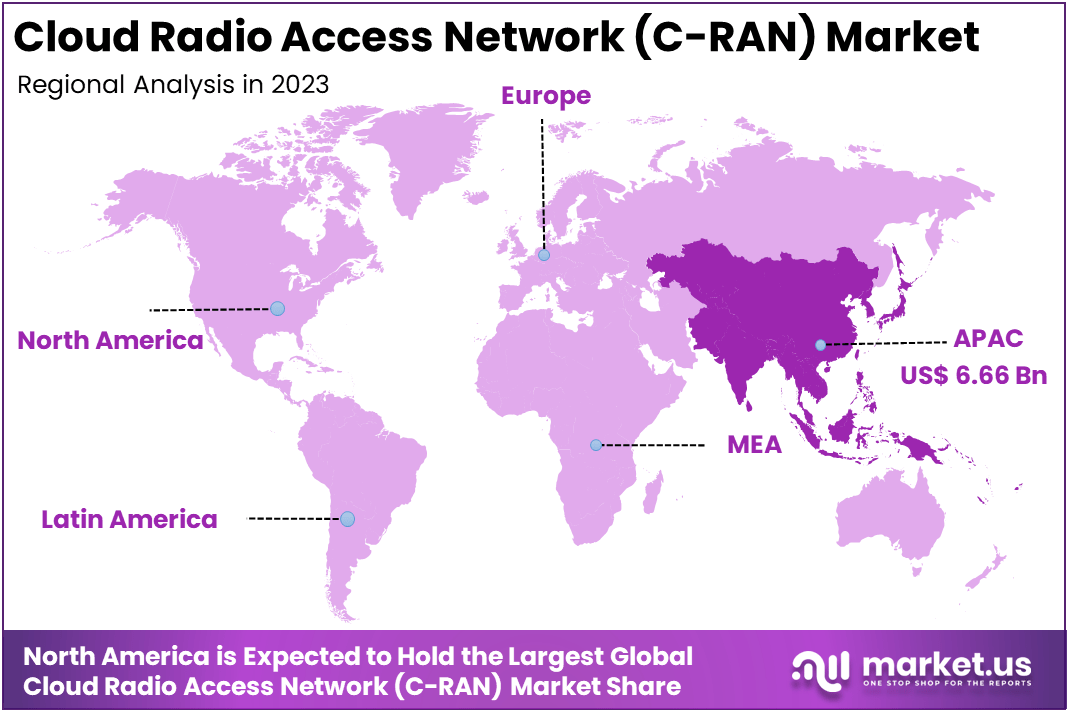

The Global Cloud Radio Access Network (C-RAN) Market size is expected to be worth around USD 159.8 Billion By 2033, from USD 18.3 Billion in 2023, growing at a CAGR of 24.20% during the forecast period from 2024 to 2033. In 2023, Asia-Pacific held a dominant market position, capturing more than a 36.4% share, holding USD 6.66 Billion in revenue.

Cloud Radio Access Network (C-RAN) is an innovative network architecture that aims to optimize the performance and cost-efficiency of mobile networks by centralizing the baseband processing units (BBU) in cloud data centers. Traditionally, the BBUs in mobile networks are located near the cell towers in decentralized base stations.

In contrast, C-RAN moves this processing capability to the cloud, enabling network operators to manage multiple remote radio heads (RRH) from a central location. This architecture improves scalability, reduces hardware costs, and facilitates the deployment of more flexible and adaptive network services.

C-RAN is especially beneficial in 5G networks, where high bandwidth and low latency are critical. By using cloud technologies, C-RAN enables better resource management, enhanced data throughput, and the ability to deploy virtualized network functions, supporting the evolving demands of modern telecommunications.

The C-RAN market is experiencing significant growth as telecommunications companies increasingly move towards 5G and beyond. This market refers to the deployment and adoption of Cloud Radio Access Network systems and associated services, which include hardware, software, and infrastructure solutions that facilitate the transition from traditional radio access networks to cloud-based models.

As operators look to upgrade their infrastructure to support the increased data traffic driven by the Internet of Things (IoT), mobile data usage, and 5G networks, the demand for C-RAN solutions continues to rise. These systems provide several benefits, including lower operational costs, improved energy efficiency, and enhanced network performance, which are critical factors driving market expansion.

One of the primary factors is the increasing demand for 5G technology. As mobile operators roll out 5G networks globally, C-RAN offers an efficient way to support the high-speed, low-latency requirements of 5G. Another driver is the cost efficiency associated with C-RAN architecture.

Centralizing baseband units in cloud data centers reduces the need for expensive, distributed infrastructure, enabling operators to save on capital and operational expenditures. Additionally, the growing demand for higher data capacity due to the explosion of connected devices, IoT, and multimedia content is pushing the adoption of C-RAN as it can handle the rising demand for bandwidth more effectively than traditional architectures.

The demand for C-RAN solutions is particularly strong in regions where mobile operators are aggressively expanding their 5G networks. North America and Asia-Pacific are expected to dominate the market due to the high investments in telecom infrastructure by companies such as Verizon, AT&T, China Mobile, and others.

In these regions, operators are deploying C-RAN to reduce latency and improve service delivery while managing the increasing load from mobile data consumption. Moreover, C-RAN’s ability to support network virtualization and cloud computing technologies is also driving its demand across industries, enabling telecommunications companies to adopt a more agile and scalable approach to network management.

The C-RAN market offers numerous opportunities for vendors and service providers. As 5G networks expand, the market for C-RAN is expected to grow exponentially, offering substantial revenue opportunities for companies involved in cloud computing, network equipment manufacturing, and telecommunications services.

Additionally, the integration of artificial intelligence (AI) and machine learning (ML) in C-RAN systems presents new opportunities for automating network management and optimizing traffic flow. This can lead to more efficient network operation, better quality of service, and improved customer experience. Furthermore, virtualization technologies offer opportunities for telecom operators to reduce costs while improving scalability, which is driving interest in C-RAN solutions.

Technological advancements are playing a crucial role in the growth of the C-RAN market. One significant trend is the integration of network slicing, which allows operators to partition a physical network into multiple virtual networks, each optimized for specific types of services or customers.

This is particularly beneficial in the context of 5G, where different applications, such as autonomous vehicles, smart cities, and healthcare, may require distinct network characteristics. Additionally, edge computing is being incorporated into C-RAN systems, allowing data processing to occur closer to the end user and improving latency.

Advancements in cloud-native technologies, such as containerization and orchestration platforms, also enhance the scalability and flexibility of C-RAN systems, allowing telecom providers to manage increasingly complex network environments efficiently.

In terms of deployment, over 60% of major telecom operators are implementing C-RAN as part of their 5G strategies, driven by the increasing demand for efficient network architectures to manage growing data traffic. For instance, China alone deployed over 800,000 5G base stations in the first half of 2023.

User data is also crucial in understanding the impact and adoption of C-RAN technology. As of late 2023, global mobile subscriptions reached approximately 8 billion, with more than 1 billion new subscriptions added in just the last 2 years, largely driven by increased smartphone penetration and demand for mobile broadband services. In addition, it is estimated that there are over 5 billion unique mobile users worldwide, highlighting the vast potential user base that C-RAN can serve.

Moreover, network traffic is expected to grow significantly; projections indicate that global mobile data traffic will reach around 77 exabytes per month by 2025, up from approximately 30 exabytes per month in 2020. This surge underscores the necessity for efficient network solutions like C-RAN to handle increased demand effectively.

Key Takeaways

- Market Growth: The global Cloud Radio Access Network (C-RAN) market is set to experience significant growth, expanding from USD 18.3 billion in 2023 to USD 159.8 billion by 2033, representing a robust CAGR of 24.20%.

- Dominant Component: The Solution segment holds the dominant share in the market with 71.5% in 2023, driven by the growing adoption of C-RAN solutions in 4G and 5G networks to enhance data traffic management and operational efficiency.

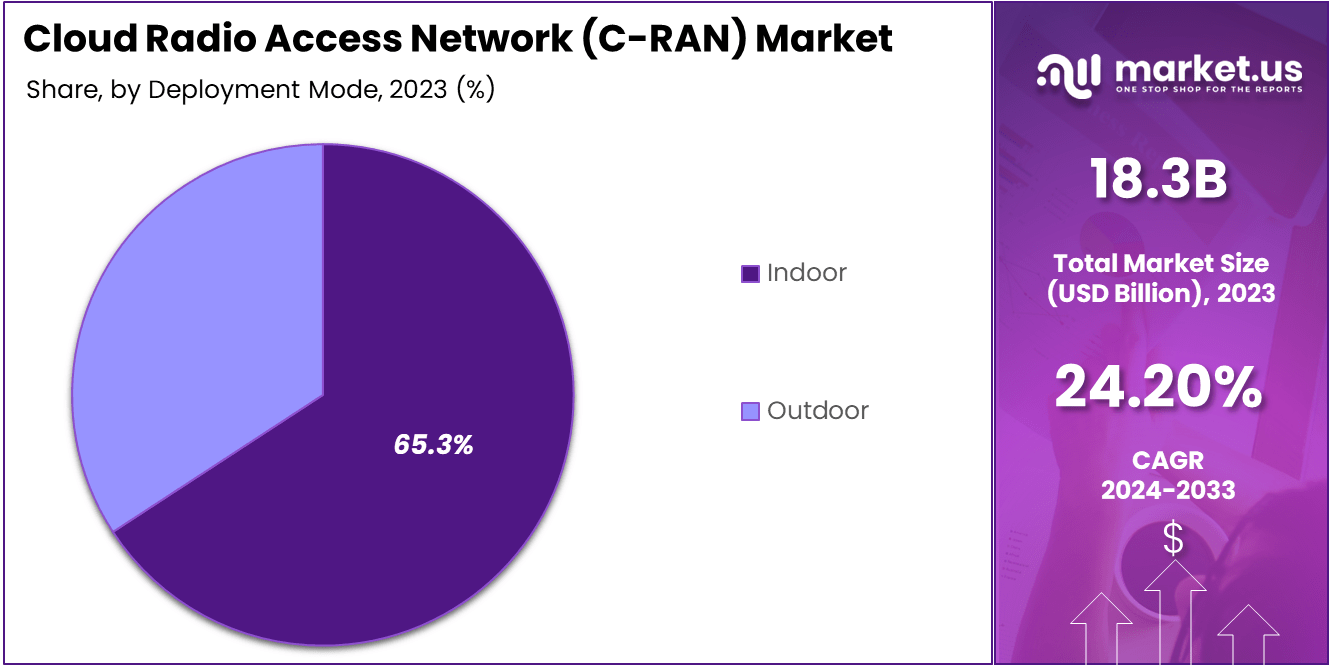

- Leading Deployment Mode: Indoor deployment dominates the market with a 65.8% share in 2023, reflecting the increasing demand for optimized indoor network performance and seamless connectivity within buildings, data centers, and enterprise environments.

- Most Adopted Architecture: The Centralized RAN architecture leads the market with a share of 64.1% in 2023, favored for its cost-effectiveness, reduced latency, and simplified management of wireless resources in dense urban areas.

- Key Network Type: The 4G network holds a significant share of 39.0% in 2023, driven by continued investments in 4G network upgrades as carriers prepare for 5G integration.

- Regional Dominance: Asia-Pacific holds the largest market share of 36.4% in 2023, driven by rapid 5G deployment and high demand for C-RAN solutions in countries like China, South Korea, and India.

By Component

In 2023, the Solution segment held a dominant market position, capturing more than a 71.5% share of the Cloud Radio Access Network (C-RAN) market. This dominance can be attributed to the increasing demand for integrated solutions that enable more efficient network management, especially in 4G and 5G environments.

Solutions such as baseband units, remote radio heads, and software tools are critical to the efficient functioning of C-RAN systems, as they optimize the use of network resources and enhance overall connectivity. The high adoption of C-RAN solutions is a direct response to the growing need for faster, more reliable mobile networks, particularly in urban areas and data-heavy applications.

The rise of 5G technology has further fueled the demand for C-RAN solutions. These solutions allow for centralized processing and resource sharing, which reduce operational costs and improve scalability.

As mobile data consumption continues to surge, mobile network operators are increasingly looking for solutions that can handle large volumes of data while maintaining low latency and high efficiency. This trend is expected to drive continued growth in the Solution segment, as companies strive to meet the growing demands of modern wireless communications.

Moreover, C-RAN solutions enable better energy management and cost efficiency, two key factors that contribute to their growing adoption. Network operators are under pressure to reduce energy consumption and improve return on investment, both of which can be achieved through centralized processing and virtualized solutions. As a result, the Solution segment is poised for continued dominance, particularly in regions transitioning to next-generation 5G networks.

By Deployment Mode

In 2023, the Indoor segment held a dominant market position, capturing more than a 65.8% share of the Cloud Radio Access Network (C-RAN) market. This dominance is primarily driven by the increasing demand for enhanced in-building connectivity, particularly in high-density areas such as office buildings, shopping malls, airports, and stadiums.

With the growing reliance on mobile data and the need for uninterrupted connectivity, businesses are investing in indoor C-RAN solutions to improve the user experience. These solutions enable efficient management of network resources within a confined space, offering a cost-effective way to meet the high data demands of indoor environments.

Indoor deployments are particularly crucial for the rollout of 5G technology, which promises to deliver faster speeds and lower latency. C-RAN’s centralized processing capabilities are well-suited to handle the complexities of high-frequency bands used in 5G, making it an ideal solution for ensuring seamless connectivity in indoor settings.

The demand for high-performance wireless communication inside buildings, along with the push towards enterprise digital transformation, has led to the widespread adoption of indoor C-RAN solutions. Another contributing factor is the scalability and flexibility that indoor C-RAN deployments offer. As businesses expand their networks, they require solutions that can be easily scaled to accommodate growing traffic without significant infrastructure overhauls.

Indoor C-RAN systems provide just that—centralized management that simplifies upgrades and expansions, all while reducing operational costs. This adaptability makes the Indoor segment a major driver of market growth, particularly in urban areas where mobile data traffic is growing rapidly.

By Architecture Type

In 2023, the Centralized RAN segment held a dominant market position, capturing more than a 64.1% share of the Cloud Radio Access Network (C-RAN) market. This dominance can be attributed to its ability to efficiently manage network traffic across large areas while minimizing hardware costs.

Centralized RAN (C-RAN) relies on a centralized baseband unit (BBU) that processes data for multiple remote radio heads (RRHs) spread across a wide area. This centralized approach enables operators to consolidate their infrastructure, leading to significant cost savings and simplified network management.

One of the primary drivers for the growth of Centralized RAN is its ability to support the high data throughput demands of modern mobile networks, particularly with the rollout of 4G and 5G technologies. The centralized architecture allows operators to dynamically allocate resources based on real-time network needs, making it highly adaptable and scalable.

This scalability is crucial for telecom operators who must continuously upgrade their networks to support increased traffic, especially with the surge in data consumption driven by mobile video, IoT, and cloud applications.

Additionally, Centralized RAN provides improved performance and energy efficiency. By centralizing baseband processing, operators can reduce the number of energy-hungry components in the network, leading to lower operational costs. The ability to consolidate equipment in fewer locations also reduces physical space requirements, making it an attractive option for urban environments where real estate is scarce and costly.

By Network Type

In 2023, the 4G segment held a dominant market position, capturing more than a 39.0% share of the Cloud Radio Access Network (C-RAN) market. This dominance can be attributed to the continued widespread adoption of 4G networks across both developed and emerging markets.

Despite the increasing focus on 5G technology, 4G remains the backbone of mobile networks globally, supporting a vast number of users and devices. The deployment of C-RAN in 4G networks helps telecom operators optimize their infrastructure and ensure efficient handling of the substantial traffic generated by mobile data usage.

One of the key reasons for the leading position of 4G in the C-RAN market is its widespread infrastructure already in place. Telecom operators have made significant investments in 4G networks, and the integration of C-RAN technology helps maximize the performance of these existing assets.

The flexibility and scalability offered by C-RAN allow operators to enhance network capacity and coverage, especially in high-density urban areas where data demand is consistently high. This has made 4G C-RAN solutions particularly attractive for operators looking to enhance the efficiency of their networks without a complete overhaul of existing infrastructure.

Furthermore, 4G networks are still experiencing substantial growth in terms of data traffic, especially in regions like Asia-Pacific, Latin America, and parts of Africa. The increasing use of mobile video, social media, and Internet of Things (IoT) devices has significantly boosted the demand for data services, making C-RAN a vital solution for handling traffic efficiently.

The ability of 4G C-RAN to provide low-latency and high-throughput services is helping telecom operators deliver a better user experience, which is driving its continued dominance in the market.

Key Market Segments

By Component

- Solution

- Services

By Deployment Mode

- Indoor

- Outdoor

By Architecture Type

- Centralized RAN

- Virtualized/Cloud RAN

By Network Type

- 2G/3G

- 4G

- 5G

Driving Factors

Increasing Demand for 5G Networks Driving C-RAN Market Growth

The growing demand for high-speed 5G connectivity is one of the key drivers fueling the Cloud Radio Access Network (C-RAN) market. As telecom operators worldwide are rolling out 5G networks, the need for more efficient, flexible, and scalable infrastructure has become critical. C-RAN provides the necessary architecture to support these demands, offering centralized management and virtualization of network resources.

With 5G expected to enable massive IoT (Internet of Things) deployments, smart cities, autonomous vehicles, and ultra-low latency applications, the infrastructure supporting these networks must be robust and adaptable. C-RAN’s ability to centralize the radio network’s baseband processing is seen as a highly effective solution for handling the complex data traffic generated by 5G applications.

Additionally, C-RAN’s cost-effectiveness and ease of scalability are particularly appealing to network operators as they move toward 5G. By centralizing the baseband functions, operators can deploy smaller, cheaper, and more energy-efficient remote radio heads (RRHs) at the edge, while using cloud-based software to handle the processing.

This helps operators manage the substantial costs associated with deploying new infrastructure. Furthermore, as the 5G rollout expands, the number of antennas and base stations required increases, making C-RAN a preferred architecture for managing these large-scale networks.

The widespread adoption of 5G technologies across several industries—especially healthcare, automotive, and manufacturing—is expected to continue to drive demand for C-RAN.

This demand will be further accelerated by the increasing number of connected devices that require higher bandwidth and faster data transfer speeds. As a result, the integration of C-RAN solutions will play a vital role in enabling the seamless performance of these 5G networks.

Restraining Factors

High Initial Investment and Deployment Costs

One of the key restraints in the growth of the Cloud Radio Access Network (C-RAN) market is the high initial investment and deployment costs associated with its implementation.

C-RAN, while offering long-term operational cost savings and scalability, requires a significant upfront investment in infrastructure, including hardware, software, and the necessary integration into existing network systems. For many telecom operators, especially in emerging markets, this can be a considerable financial burden.

Moreover, C-RAN often requires replacing or upgrading legacy equipment, which adds to the cost. Telecom providers in less developed regions may not have the financial resources to implement this next-generation infrastructure immediately, thus slowing the pace of adoption in those areas.

In many cases, network operators must balance their C-RAN investments with the existing requirements of 4G networks and the development of 5G infrastructure, allocating funds a complex challenge.

While the centralized nature of C-RAN brings operational efficiencies and cost savings in the long run, the complexity of network planning, site acquisition, and regulatory approvals also makes the deployment of C-RAN solutions a lengthy process.

These long deployment timelines can deter operators from quickly transitioning to C-RAN, especially when weighed against the competitive need to roll out 5G networks rapidly. Therefore, while C-RAN technology holds great potential, the financial and operational challenges tied to its deployment act as a significant restraint on its widespread adoption.

Growth Opportunities

Expansion of IoT and Smart Cities

The growing trend of IoT (Internet of Things) deployments and the development of smart cities present a significant opportunity for the Cloud Radio Access Network (C-RAN) market.

As more devices become connected and the demand for seamless, high-speed data transmission increases, C-RAN’s capabilities align perfectly with the infrastructure needs of IoT ecosystems. C-RAN offers centralized control and efficient resource allocation, which is crucial for supporting the large number of connected devices within IoT networks.

Smart cities, which rely heavily on sensors, surveillance cameras, traffic management systems, and other interconnected technologies, will drive the demand for robust, flexible, and scalable network solutions. C-RAN is ideal for such applications, as it allows telecom operators to manage the vast amounts of data generated by these devices in a more cost-effective manner.

The ability to deliver low-latency, high-bandwidth connectivity across a city’s infrastructure is a fundamental requirement for the effective functioning of smart cities, making C-RAN an attractive solution.

Moreover, the global push toward sustainability in urban infrastructure also provides an opportunity for C-RAN solutions. The decentralized nature of C-RAN’s architecture reduces the energy consumption of traditional base stations by enabling more efficient use of resources.

This makes C-RAN a more environmentally friendly option, helping cities and companies achieve their sustainability goals while maintaining high-performance networks. As IoT and smart city projects continue to grow, the adoption of C-RAN is expected to increase, positioning it as a key technology in the future of urban connectivity.

Challenging Factors

Network Complexity and Integration with Legacy Systems

One of the biggest challenges for the Cloud Radio Access Network (C-RAN) market is the complexity involved in integrating C-RAN architecture with existing legacy systems. While C-RAN offers significant benefits in terms of scalability and operational efficiency, telecom operators often face hurdles in retrofitting their existing networks with the new technology.

The transition to a centralized baseband processing system requires not only a shift in network architecture but also careful integration with the current network infrastructure, which can be a complex and time-consuming process.

Legacy systems were typically designed with a more decentralized architecture, making the shift to C-RAN challenging. Operators must ensure that existing hardware is compatible with the new C-RAN solutions, which may require significant upgrades.

Additionally, because C-RAN often relies on cloud-based technologies, operators must invest in the necessary IT infrastructure to support cloud computing at scale, which adds another layer of complexity to the transition.

Network operators also face challenges in terms of coordinating across multiple vendors, technologies, and regulatory environments when deploying C-RAN solutions, especially in regions with diverse regulatory requirements.

The coordination needed for such complex deployments can lead to delays and higher implementation costs. Therefore, despite the advantages of C-RAN, the integration process with legacy systems and the complexity of large-scale deployment remain significant challenges that could slow its widespread adoption.

Growth Factors

One of the primary growth factors for the Cloud Radio Access Network (C-RAN) market is the global shift towards 5G networks. Telecom operators are increasingly adopting C-RAN to address the challenges of handling high volumes of data traffic and improving network performance.

C-RAN allows for better spectrum utilization, cost reduction, and faster deployment, which are critical for managing the heavy demands of 5G and future wireless technologies. As countries expand their 5G infrastructure, the need for advanced network architectures like C-RAN will only intensify, driving the market forward.

Emerging Trends

A major emerging trend in the C-RAN market is the growing interest in virtualized and cloud-based RAN (vRAN) solutions. By virtualizing the RAN functions, telecom operators can significantly reduce hardware costs and improve network flexibility.

This trend aligns with the industry’s broader move towards cloud-native technologies, where software-based solutions replace traditional hardware. The convergence of C-RAN with other emerging technologies, such as edge computing and AI-powered network management, is also gaining momentum, enabling even greater performance and network optimization.

Business Benefits

For businesses, the adoption of C-RAN offers significant benefits, including improved operational efficiency, lower capital expenditure, and increased network scalability. C-RAN’s centralized architecture enables network operators to manage resources more effectively, ensuring smoother operations and faster service rollouts.

The ability to scale network capacity without major hardware upgrades also makes it a highly attractive solution for service providers looking to keep up with the increasing demand for faster and more reliable connectivity.

Regional Analysis

In 2023, Asia-Pacific held a dominant market position in the Cloud Radio Access Network (C-RAN) market, capturing more than a 36.4% share, equivalent to USD 6.66 billion in revenue. This regional leadership can largely be attributed to the rapid rollout of 5G networks and the increasing demand for advanced mobile infrastructure in countries such as China, India, Japan, and South Korea.

As the region continues to invest heavily in the expansion of next-generation mobile networks, telecom providers are turning to C-RAN technology to improve their operational efficiency, and network performance, and reduce costs. The flexibility and scalability offered by C-RAN solutions make them particularly attractive in high-density urban areas, where the demand for data traffic is highest.

The adoption of C-RAN in Asia-Pacific is also being propelled by the region’s increasing focus on technological innovation and the move towards smart cities. Governments and telecom operators are collaborating to deploy 5G networks as part of broader national strategies to enhance connectivity and digital transformation.

For example, China’s “Made in China 2025” initiative and India’s ambitious Digital India program are encouraging investments in telecom infrastructure, further driving the demand for C-RAN solutions. As a result, Asia-Pacific is expected to continue dominating the market in the coming years, accounting for a substantial share of the global revenue.

Furthermore, the rise of the Internet of Things (IoT) and Industry 4.0 applications is fostering the need for higher data speeds and lower latency, both of which can be effectively addressed by C-RAN technology.

The region is witnessing an explosion in IoT device deployments, contributing to increased data consumption and demanding more robust network infrastructures. The integration of 5G with C-RAN is therefore poised to fuel growth, making Asia-Pacific a key hub for the C-RAN market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Samsung Electronics is a key player in the Cloud Radio Access Network (C-RAN) market, continuously strengthening its position through strategic acquisitions, new product launches, and partnerships. In 2023, Samsung announced the expansion of its 5G portfolio with advanced C-RAN solutions designed to optimize network performance and reduce operational costs for telecom operators.

The company is heavily investing in 5G research and development to ensure its solutions support the growing demands for high-speed, low-latency mobile services. Samsung’s recent acquisitions in the telecommunications sector have bolstered its R&D capabilities, allowing the company to enhance its C-RAN offerings and accelerate the deployment of 5G networks worldwide.

Nokia has established itself as a leader in the global C-RAN market, driven by its strategic product launches and partnerships. In recent years, the company has been focused on providing end-to-end solutions for 5G deployment, including C-RAN technologies, which allow for more flexible, cost-effective, and scalable network management.

Nokia’s recent launch of its AirScale portfolio, which includes C-RAN architecture, positions it as a key player in the transition to 5G. The company has formed strong alliances with several telecom operators and equipment manufacturers to deploy C-RAN solutions that support 5G services.

Ericsson has been one of the front-runners in driving the adoption of C-RAN solutions globally. The company’s continued focus on 5G innovation and network automation through C-RAN technologies is central to its strategy.

Ericsson’s recent acquisitions, including its purchase of Cradlepoint, a leading provider of 5G-based wireless edge solutions, are part of its broader efforts to expand its C-RAN offerings and enhance its 5G capabilities. Additionally, Ericsson has been actively launching new products such as the Ericsson Radio System, which integrates C-RAN technology to improve network performance and reduce energy consumption.

Top Key Players in the Market

- Samsung Electronics Co., Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- NEC Corporation

- Mavenir

- Intel Corporation

- Cisco Systems, Inc.

- Qualcomm Technologies, Inc.

- Parallel Wireless

- Other Key Players

Recent Developments

- In 2023: Nokia introduced its AirScale Cloud Radio Access Network (C-RAN) portfolio, which is designed to support both 4G and 5G networks, enabling seamless transitions to next-generation technologies. This launch aims to address the growing demand for high-speed and low-latency networks, especially in urban and rural deployments.

- In 2023: Samsung expanded its 5G C-RAN solutions by incorporating Multi-Access Edge Computing (MEC) technology. This integration allows telecom operators to deploy edge computing capabilities closer to end-users, resulting in faster data processing and reduced network latency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 18.3 Bn |

| Forecast Revenue (2033) | USD 159.8 Bn |

| CAGR (2024-2033) | 24.20% |

| Largest Market | Asia Pacific |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Solution, Services), By Deployment Mode (Indoor, Outdoor), By Architecture Type (Centralized RAN, Virtualized/Cloud RAN), By Network Type (2G/3G, 4G, 5G) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Samsung Electronics Co., Ltd., Nokia Corporation, Telefonaktiebolaget LM Ericsson, NEC Corporation, Mavenir, Intel Corporation, Cisco Systems, Inc., Qualcomm Technologies, Inc., Parallel Wireless, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")