Quick Navigation

Report Overview

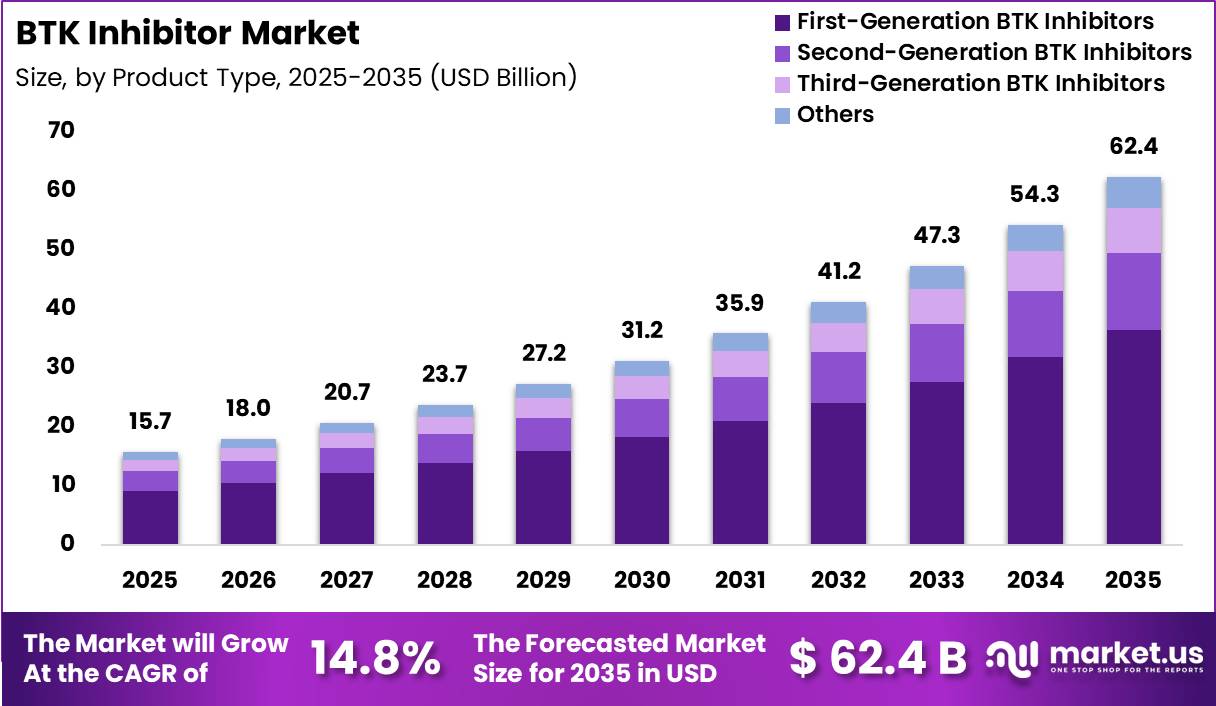

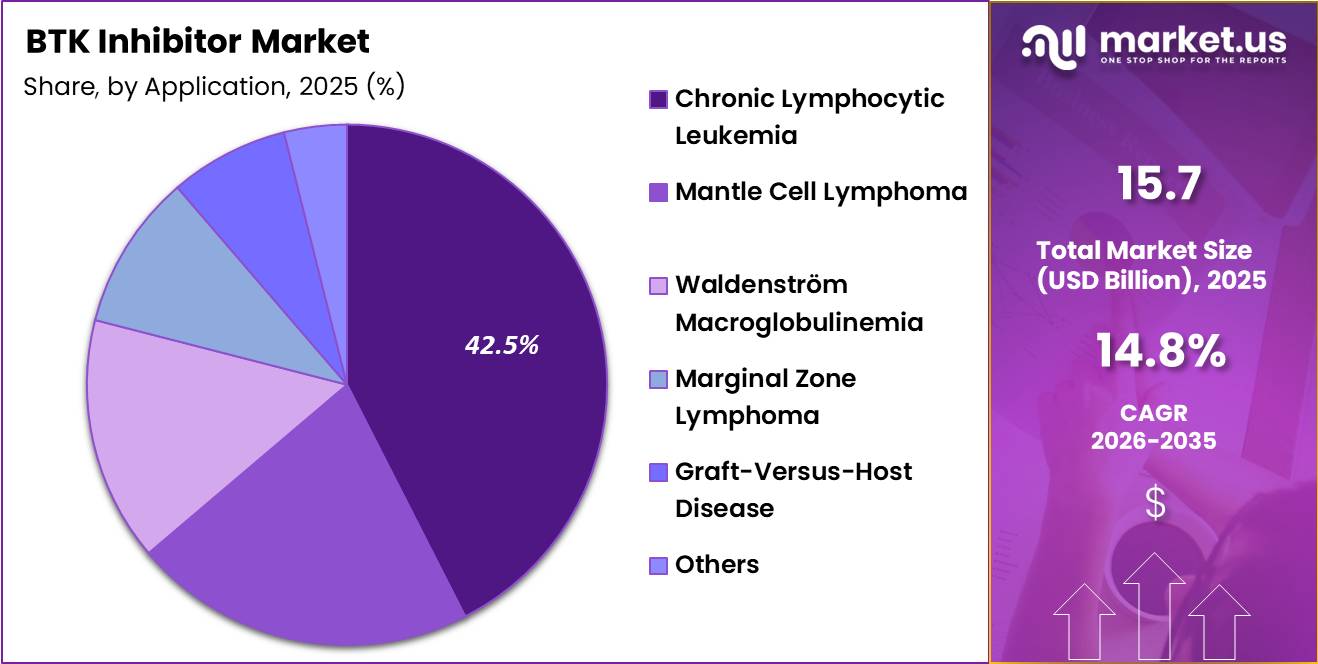

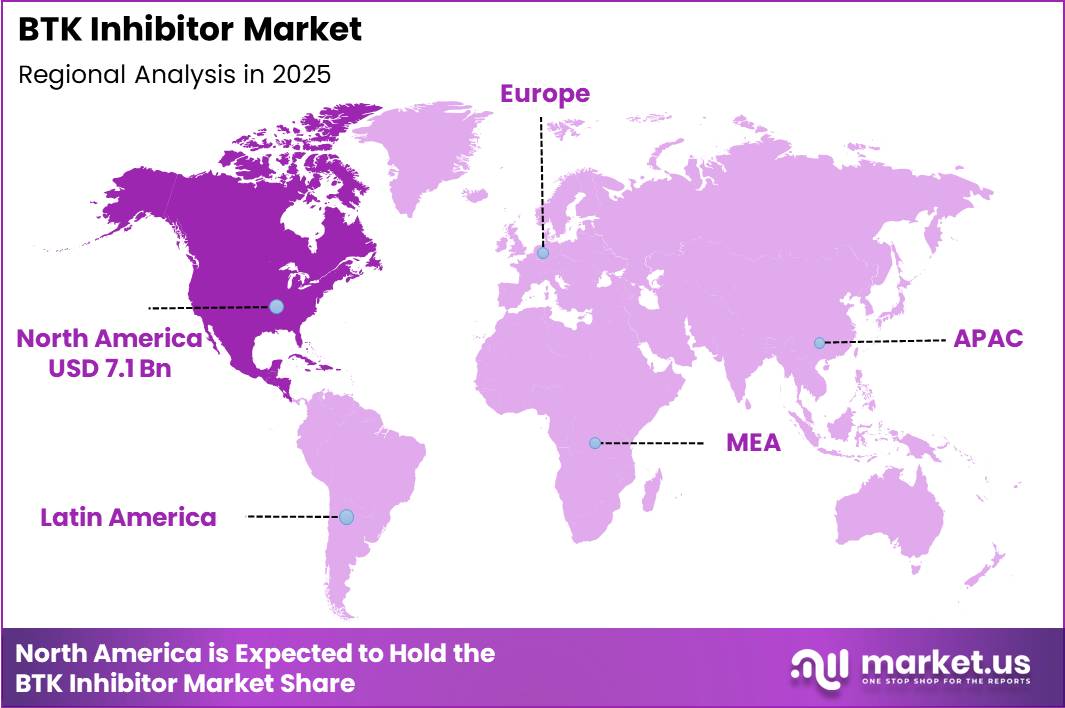

Global BTK Inhibitor Market size is expected to be worth around US$ 62.4 Billion by 2035 from US$ 15.7 Billion in 2025, growing at a CAGR of 14.8% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 45.5% share with a revenue of US$ 7.1 Billion.

The global BTK inhibitor market is witnessing substantial growth due to the rising prevalence of hematological malignancies and the increasing adoption of targeted cancer therapies. Bruton’s tyrosine kinase (BTK) inhibitors are targeted drugs that block the BTK enzyme involved in B-cell receptor signaling, thereby preventing the growth and survival of malignant B-cells.

These therapies are widely used in the treatment of chronic lymphocytic leukemia (CLL), mantle cell lymphoma (MCL), Waldenström macroglobulinemia (WM), and other autoimmune disorders. The growing burden of cancer worldwide continues to accelerate demand for advanced targeted therapeutics.

According to the World Health Organization (WHO) and the International Agency for Research on Cancer (IARC), approximately 20 million new cancer cases and 9.7 million cancer-related deaths were reported globally in 2022. Furthermore, nearly 53.5 million people were living within five years of a cancer diagnosis, while around one in five individuals are expected to develop cancer during their lifetime.

The increasing incidence of B-cell malignancies, particularly CLL and MCL, is significantly contributing to market expansion. BTK inhibitors such as ibrutinib, acalabrutinib, zanubrutinib, and emerging non-covalent inhibitors including pirtobrutinib are gaining strong clinical adoption due to improved efficacy and reduced disease progression.

In addition, advancements in precision medicine and biomarker-based therapies are encouraging the development of next-generation BTK inhibitors capable of overcoming resistance mutations such as C481S. Clinical findings published by the National Institutes of Health (NIH) demonstrated that pirtobrutinib achieved an overall response rate of 62% among patients with relapsed or refractory CLL/small lymphocytic lymphoma, while patients with C481-mutant disease showed a 75% response rate.

These developments highlight the growing therapeutic potential of BTK inhibitors in oncology treatment. Continuous research activities, expanding regulatory approvals, and increasing investments by pharmaceutical companies such as AbbVie, AstraZeneca, and Johnson & Johnson are further supporting global market growth.

Key Takeaways

- Market Size: Global BTK Inhibitor Market size is expected to be worth around US$ 62.4 Billion by 2035 from US$ 15.7 Billion in 2025.

- Market Share: The market growing at a CAGR of 14.8% during the forecast period from 2026 to 2035.

- Drug Type Analysis: First-Generation BTK Inhibitors are projected to dominate the market with a 58.5% share in 2025.

- Application Analysis: Chronic Lymphocytic Leukemia is expected to account for the largest market share of 42.5% in 2025.

- End User Analysis: Hospitals are anticipated to dominate the market with a 48.5% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 45.5% share with a revenue of US$ 7.1 Billion.

Drug Type Analysis

The BTK inhibitor market is segmented by drug type into First-Generation BTK Inhibitors, Second-Generation BTK Inhibitors, Third-Generation BTK Inhibitors, and Others. First-Generation BTK Inhibitors are projected to dominate the market with a 58.5% share in 2025, primarily driven by their extensive clinical adoption, strong therapeutic efficacy, and broad regulatory approvals across hematologic malignancies.

The widespread use of these inhibitors in chronic lymphocytic leukemia and mantle cell lymphoma treatment protocols has significantly supported segment growth. In addition, the availability of long-term clinical data and established physician familiarity continue to strengthen demand.

Second-Generation BTK Inhibitors are witnessing notable market expansion due to improved selectivity and reduced off-target adverse effects compared to first-generation therapies. Pharmaceutical companies are increasingly focusing on the development of advanced targeted therapies to improve patient outcomes.

Third-Generation BTK Inhibitors are expected to gain traction owing to their ability to address resistance mutations and enhance treatment effectiveness in relapsed or refractory cases. The Others segment includes pipeline molecules and combination therapies currently under clinical evaluation, contributing to future market opportunities through ongoing innovation and research activities.

Application Analysis

The BTK inhibitor market is segmented by application into Chronic Lymphocytic Leukemia, Mantle Cell Lymphoma, Waldenström Macroglobulinemia, Marginal Zone Lymphoma, Graft-Versus-Host Disease, and Others. Chronic Lymphocytic Leukemia is expected to account for the largest market share of 42.5% in 2025, supported by the increasing global prevalence of blood cancers and the rising adoption of targeted therapies.

The strong clinical effectiveness of BTK inhibitors in improving progression-free survival rates has accelerated their utilization in leukemia treatment. Furthermore, growing awareness regarding early diagnosis and availability of advanced oncology therapeutics continue to support segment expansion.

Mantle Cell Lymphoma represents a significant segment due to increasing regulatory approvals for BTK inhibitor-based therapies and rising demand for precision medicine approaches. Waldenström Macroglobulinemia is also experiencing steady growth driven by favorable clinical trial outcomes and improved treatment accessibility.

Marginal Zone Lymphoma applications are expanding as healthcare providers increasingly adopt targeted immunotherapy solutions for rare lymphatic disorders. The Graft-Versus-Host Disease segment is projected to witness growing adoption owing to ongoing research focused on immune-modulating therapies. The Others segment includes additional hematologic malignancies and autoimmune disorder applications currently under investigation.

End User Analysis

The BTK inhibitor market is segmented by end user into Hospitals, Specialty Clinics, Cancer Research Centers, and Others. Hospitals are anticipated to dominate the market with a 48.5% share in 2025, owing to the high volume of oncology patient admissions, availability of advanced treatment infrastructure, and strong presence of specialized hematology departments.

Hospitals remain the primary centers for diagnosis, administration, and monitoring of BTK inhibitor therapies, particularly for complex hematologic malignancies. Increasing investments in hospital-based cancer care facilities and rising patient preference for comprehensive treatment services further contribute to segment growth.

Specialty Clinics are witnessing substantial expansion due to the growing adoption of outpatient cancer treatment services and personalized therapeutic management. These facilities provide targeted care with reduced hospitalization requirements, improving patient convenience and treatment efficiency.

Cancer Research Centers also represent an important segment, supported by increasing clinical trial activities, drug development programs, and collaborative oncology research initiatives focused on next-generation BTK inhibitors. The Others segment includes ambulatory care centers and academic medical institutions that contribute to market growth through expanding oncology treatment capabilities and supportive healthcare infrastructure development across emerging economies.

Key Market Segments

By Drug Type

- First-Generation BTK Inhibitors

- Second-Generation BTK Inhibitors

- Third-Generation BTK Inhibitors

- Others

By Application

- Chronic Lymphocytic Leukemia

- Mantle Cell Lymphoma

- Waldenström Macroglobulinemia

- Marginal Zone Lymphoma

- Graft-Versus-Host Disease

- Others

By End User

- Hospitals

- Specialty Clinics

- Cancer Research Centers

- Others

Driving Factors

The growth of the BTK inhibitor market is primarily driven by the rising global burden of hematological malignancies, particularly chronic lymphocytic leukemia (CLL), small lymphocytic lymphoma (SLL), and non-Hodgkin lymphoma (NHL). BTK inhibitors target Bruton’s tyrosine kinase, a critical enzyme involved in B-cell malignancies, thereby improving treatment outcomes compared with traditional chemotherapy.

According to the American Cancer Society, approximately 79,320 new cases of non-Hodgkin lymphoma are expected in the United States in 2026, while nearly 19,970 deaths are projected from the disease. Increasing diagnosis rates among the aging population are supporting demand for targeted therapies.

Furthermore, regulatory approvals are accelerating market expansion. The U.S. FDA approved zanubrutinib for CLL/SLL in 2023 and approved acalabrutinib in combination with venetoclax for untreated CLL/SLL in 2026. Clinical evidence demonstrating superior progression-free survival and reduced toxicity compared with chemoimmunotherapy has encouraged adoption among oncologists. The increasing preference for oral targeted therapies and precision medicine approaches is further contributing to sustained market growth globally.

Trending Factors

A major trend observed in the BTK inhibitor market is the transition from first-generation inhibitors toward highly selective and non-covalent BTK inhibitors with improved efficacy and safety profiles. Earlier therapies such as ibrutinib were associated with adverse events including atrial fibrillation and bleeding complications, encouraging pharmaceutical innovation toward next-generation molecules. Recent FDA approvals of pirtobrutinib highlight this transition.

In 2025, the FDA granted traditional approval to pirtobrutinib for relapsed or refractory CLL/SLL patients previously treated with covalent BTK inhibitors. The BRUIN-CLL-321 clinical study included 238 patients and demonstrated significant therapeutic benefits in resistant disease populations. In addition, increasing research activity is expanding BTK inhibitor applications beyond oncology into autoimmune and neurological disorders such as multiple sclerosis.

Several clinical trials are evaluating brain-penetrant BTK inhibitors for neuroinflammatory diseases. The market is also witnessing combination therapy development, where BTK inhibitors are administered alongside BCL-2 inhibitors and monoclonal antibodies to improve survival outcomes. These advancements are strengthening the long-term clinical relevance of BTK inhibitors across multiple therapeutic areas.

Restraint

Despite strong clinical adoption, the BTK inhibitor market faces restraints associated with adverse drug reactions, treatment resistance, and high therapy costs. Long-term use of BTK inhibitors has been linked with cardiovascular toxicity, infections, bleeding events, and liver-related complications, which may limit patient compliance and physician preference. Safety concerns surrounding emerging BTK inhibitors have intensified regulatory scrutiny.

For example, the FDA issued a Complete Response Letter for tolebrutinib in 2025 due to severe drug-induced liver injury risks observed during clinical trials. Resistance mutations also remain a significant challenge. According to FDA data, around 77% of patients enrolled in the BRUIN trial had discontinued previous BTK inhibitor therapy because of refractory or progressive disease.

Additionally, BTK inhibitors are expensive targeted therapies, creating affordability concerns in low- and middle-income countries. The requirement for prolonged treatment duration further increases the economic burden on healthcare systems and patients. Patent exclusivity and limited generic competition continue to maintain premium pricing structures. These factors may restrict widespread accessibility and slow market penetration in cost-sensitive healthcare environments despite strong therapeutic demand.

Opportunity

Significant growth opportunities exist in the BTK inhibitor market due to expanding indications, rising investments in precision oncology, and increasing global cancer incidence. According to the International Agency for Research on Cancer (IARC), approximately 509,600 new non-Hodgkin lymphoma cases and 248,700 related deaths were reported globally in 2018. The growing patient pool creates long-term demand for advanced targeted therapies.

Opportunities are particularly strong in Asia-Pacific and emerging economies where cancer diagnosis infrastructure and access to innovative oncology medicines are improving rapidly. Pharmaceutical companies are increasingly focusing on combination regimens and next-generation BTK inhibitors capable of overcoming acquired resistance mutations.

Additionally, clinical research into autoimmune diseases and central nervous system disorders is broadening commercial potential beyond hematologic cancers. BTK inhibitors are being investigated for multiple sclerosis and inflammatory disorders, opening new therapeutic markets.

Regulatory agencies are also supporting accelerated approval pathways for innovative cancer therapies, enabling faster commercialization. The increasing adoption of biomarker-driven treatment selection and precision medicine strategies is expected to create substantial opportunities for personalized BTK inhibitor therapies over the coming decade.

Regional Analysis

In 2025, North America dominated the BTK Inhibitor Market, accounting for over 45.5% of the global share and generating revenue of approximately US$ 7.1 billion. The regional market growth is primarily supported by the high prevalence of hematologic malignancies, increasing adoption of targeted cancer therapies, and the strong presence of leading biopharmaceutical companies.

The United States represents the largest contributor within the region due to advanced healthcare infrastructure, favorable reimbursement policies, and extensive clinical research activities. In addition, rising investments in oncology drug development and the growing approval of novel BTK inhibitors are accelerating market expansion.

Canada is also witnessing steady growth owing to increasing awareness regarding precision medicine and improved access to advanced treatment options. Furthermore, the presence of established regulatory frameworks and continuous technological advancements in cancer therapeutics are expected to strengthen North America’s position in the global BTK inhibitor market throughout the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The BTK Inhibitor Market is highly competitive, with key players focusing on product innovation, strategic collaborations, and regulatory approvals to strengthen their market position. Major pharmaceutical companies such as Johnson & Johnson, AstraZeneca plc, AbbVie Inc., Bristol-Myers Squibb Company, and BeiGene Ltd. are actively investing in research and development activities to expand their oncology portfolios.

These companies are emphasizing the development of next-generation BTK inhibitors with improved efficacy and reduced side effects to address unmet clinical needs. Strategic partnerships, mergers, and acquisitions are also being adopted to enhance global market presence and accelerate drug commercialization.

In addition, increasing clinical trials for chronic lymphocytic leukemia, mantle cell lymphoma, and other hematologic malignancies are supporting market growth. Companies are further focusing on geographic expansion in emerging markets to increase patient access and strengthen revenue generation. Continuous innovation and strong regulatory pipelines are expected to intensify competition in the BTK inhibitor market over the forecast period.

Market Key Players

- Johnson & Johnson

- AbbVie Inc.

- AstraZeneca plc

- BeiGene, Ltd.

- Novartis AG

- Eli Lilly and Company

- Merck & Co., Inc.

- InnoCare Pharma

- Sunesis Pharmaceuticals

- Principia Biopharma

- Ono Pharmaceutical Co., Ltd.

- CELGENE (Bristol-Myers Squibb)

- TG Therapeutics, Inc.

- Others

Recent Developments

- January 2025 – Johnson & Johnson strengthened its neuroscience portfolio through the acquisition of Intracellular Therapies in a deal valued at approximately USD 14.6 billion. The transaction highlighted the company’s continued focus on expanding high-value specialty therapeutics and reinforced broader investment momentum across targeted therapy markets, including BTK inhibitor research and hematology innovation.

- March 2025 – Ono Pharmaceutical Co., Ltd. entered a global licensing agreement with Ionis Pharmaceuticals for sapablursen, an investigational therapy for polycythemia vera. The agreement included an upfront payment of USD 280 million with additional milestone-based payments, reflecting increasing strategic investments in hematology and immune-related treatment pipelines.

- July 2025 – AbbVie Inc. signed an exclusive global licensing agreement with Ichnos Glenmark Innovation for ISB 2001, a trispecific antibody candidate targeting oncology and autoimmune diseases. The collaboration demonstrated AbbVie’s aggressive expansion strategy in next-generation immunology and targeted therapies, areas closely aligned with BTK inhibitor market evolution.

- July 2025 – CELGENE parent company Bristol-Myers Squibb partnered with Bain Capital to establish a new immunology-focused company backed by USD 300 million in financing. The initiative was designed to accelerate the development of autoimmune disease therapies and strengthen BMS’s long-term immunology pipeline.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 15.7 Billion |

| Forecast Revenue (2035) | US$ 62.4 Billion |

| CAGR (2026-2035) | 14.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (First-Generation BTK Inhibitors, Second-Generation BTK Inhibitors, Third-Generation BTK Inhibitors, Others) By Application (Chronic Lymphocytic Leukemia, Mantle Cell Lymphoma, Waldenström Macroglobulinemia, Marginal Zone Lymphoma, Graft-Versus-Host Disease, Others) By End User (Hospitals, Specialty Clinics, Cancer Research Centers, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Johnson & Johnson, AbbVie Inc., AstraZeneca plc, BeiGene, Ltd., Novartis AG, Eli Lilly and Company, Merck & Co., Inc., InnoCare Pharma, Sunesis Pharmaceuticals, Principia Biopharma, Ono Pharmaceutical Co., Ltd., CELGENE (Bristol-Myers Squibb), TG Therapeutics, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |