Global Blind Bolts Market Size, Share, Growth Analysis By Product Type (Heavy-Duty Blind Bolts, Thin-Wall Blind Bolts), By Material (Steel, Stainless Steel, Aluminum, Titanium, Composite Materials, Others), By Diameter (M8, M10, M12, M16, Others), By Grade (Grade 8.8, Grade 10.9, Grade 316), By End Use Industry (Automotive, Aerospace, Machinery and Equipment, Construction, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180927

- Number of Pages: 353

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

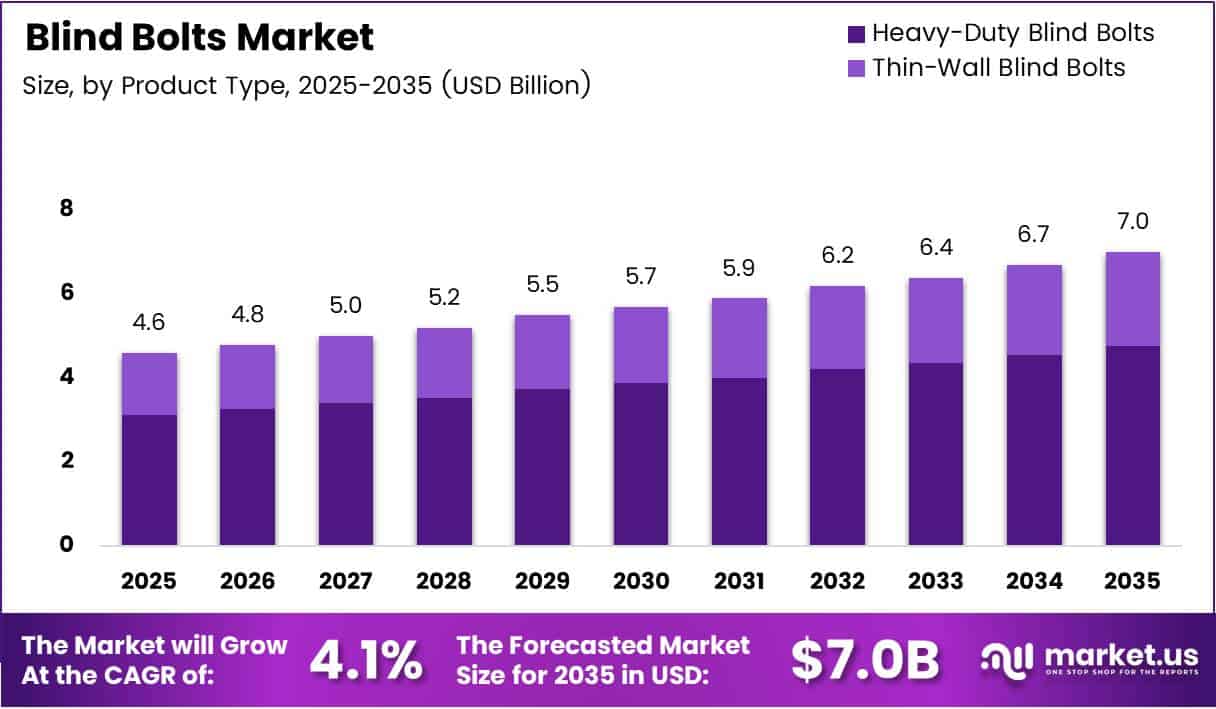

Global Blind Bolts Market size is expected to be worth around USD 7.0 Billion by 2035 from USD 4.6 Billion in 2025, growing at a CAGR of 4.1% during the forecast period 2026 to 2035.

Blind bolts are structural fasteners designed for one-sided installation in hollow sections, closed profiles, and limited-access assemblies. They eliminate the need for rear access, reducing assembly time and labor costs. This functional advantage makes them a preferred choice across aerospace, automotive, construction, and wind energy applications.

Aerospace manufacturers rely on blind bolts for airframe assembly where weight reduction and single-side access are non-negotiable requirements. The automotive sector uses them in lightweight body panels and chassis assemblies where conventional through-bolting is structurally impractical. Both end-use patterns reflect a structural shift toward precision fastening in weight-sensitive manufacturing.

Infrastructure construction and modular building projects drive adoption by requiring secure fastening in hollow structural sections and box columns. This demand comes from contractors who need certified structural connections without full beam access. Regulatory certification bodies, including ICC-ES, now formally evaluate and approve blind fastener systems for specific load categories.

Wind energy turbine assembly presents another expansion front. Blind bolts enable maintenance technicians to secure and replace components on turbine nacelles and towers from a single side. As wind installation volumes rise globally, the fastener supply chain supporting turbine OEMs stands to benefit directly.

In January 2024, PennEngineering acquired Sherex Fastening Solutions, adding blind rivet nut technology to its portfolio. This consolidation signals that large fastener groups are actively broadening their blind fastening capabilities, compressing the window for independent specialists to operate without facing acquisition or direct competition from integrated players.

According to the ICC-ES ESR-3330 regulatory evaluation report reissued in March 2025, M20 carbon steel Hollo-Bolt fasteners carry an available static tension LRFD load of 20,000 lbf. This certified load rating validates blind bolts for structural building applications — giving procurement teams in construction the compliance documentation they need to specify blind fasteners in governed projects.

According to the 2025 Lindapter UK catalogue, Hollo-Bolt connections received independent approval for fire resistance performance up to 120 minutes. Fire certification removes a major specification barrier in commercial construction, where passive fire performance governs fastener selection. This approval effectively expands the addressable market for structural blind bolts into regulated building segments.

Key Takeaways

- The Global Blind Bolts Market was valued at USD 4.6 Billion in 2025 and is forecast to reach USD 7.0 Billion by 2035.

- The market advances at a CAGR of 4.1% during the forecast period 2026 to 2035.

- Heavy-Duty Blind Bolts lead the Product Type segment with a 65.7% market share in 2025.

- Steel dominates the Material segment with a 45.6% share, reflecting cost and strength priorities across industrial buyers.

- The M10 diameter holds a 26.8% share in the Diameter segment, driven by broad applicability across automotive and machinery assemblies.

- Grade 8.8 leads the Grade segment with a 40.9% share, preferred for general structural applications.

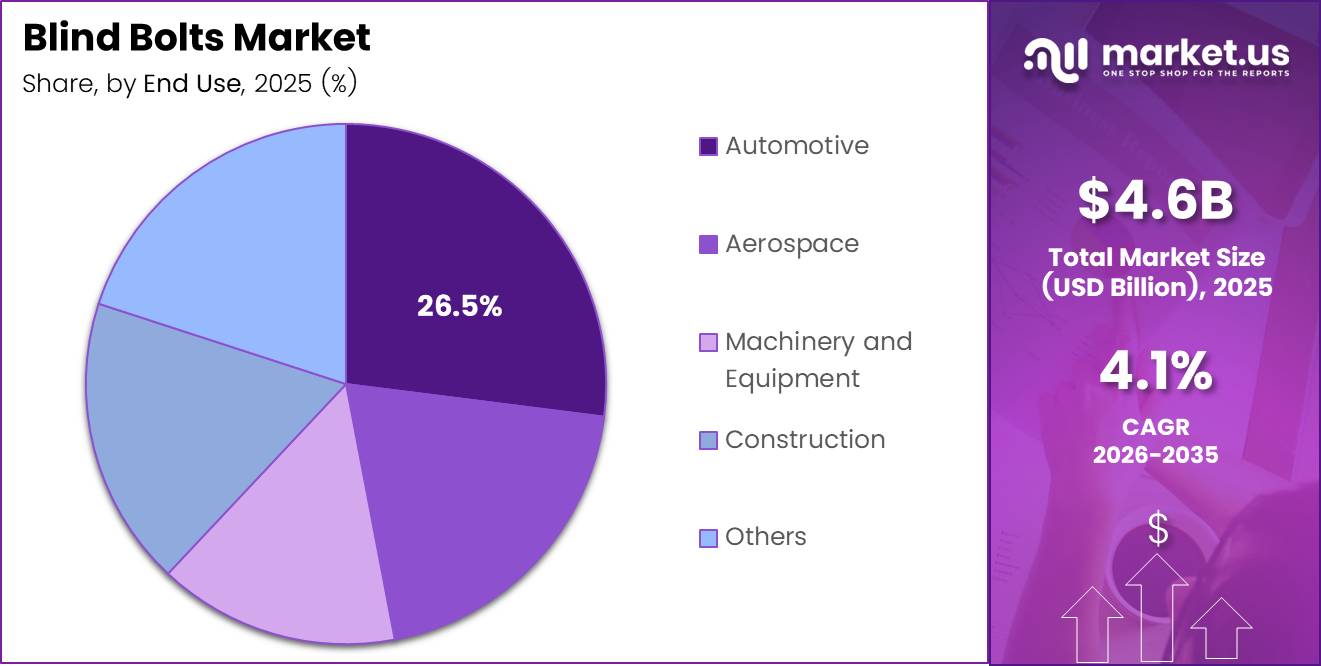

- The Automotive end-use industry accounts for 26.5% of market demand, the highest among all end-use segments.

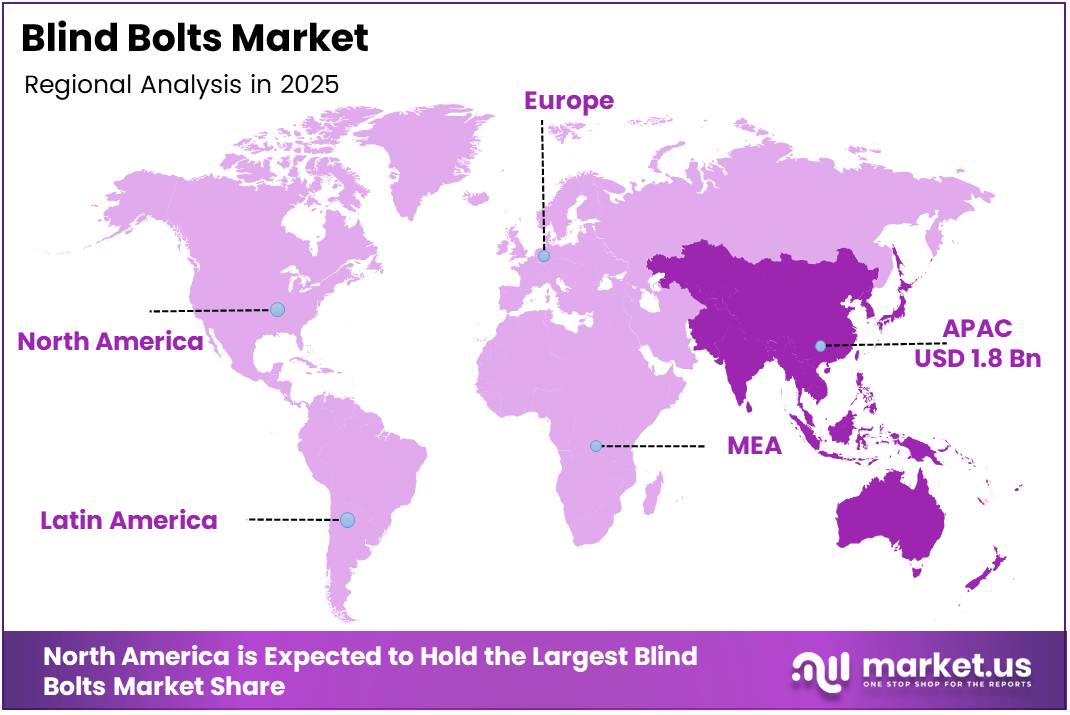

- Asia Pacific dominates regional demand with a 40.2% market share, valued at USD 1.8 Billion in 2025.

Product Type Analysis

Heavy-Duty Blind Bolts dominate with 65.7% due to structural load and certified performance requirements.

In 2025, Heavy-Duty Blind Bolts held a dominant market position in the By Product Type segment of the Blind Bolts Market, with a 65.7% share. According to the 2025 manufacturer technical data, HD M16 blind bolts carry a single shear capacity of 60.8 kN and a tension capacity of 69.6 kN. These certified load ratings make heavy-duty variants the only viable option for structural steel and load-bearing construction applications.

Thin-Wall Blind Bolts serve assemblies where material thickness and access constraints rule out heavier fastener profiles. According to the June 2025 manufacturer technical data sheet, carbon steel Thin-Wall variants achieve a minimum tensile strength of 690 N/mm², with a maximum clamping range of 5/16″ (16 mm). This combination of compact form and certified strength positions thin-wall fasteners as the preferred choice in hollow section cladding and lightweight panel assemblies.

Material Analysis

Steel dominates with 45.6% due to cost efficiency and broad structural compatibility.

In 2025, Steel held a dominant market position in the By Material segment of the Blind Bolts Market, with a 45.6% share. Steel offers the strongest price-to-performance ratio across general industrial and construction fastening applications. Its compatibility with standard coating systems — including zinc flake and hot-dip galvanizing — sustains its lead in procurement decisions where corrosion protection adds to base material value.

Stainless Steel carries a performance premium that justifies its higher unit cost in corrosive or hygienic environments. According to the June 2025 manufacturer technical data sheet, stainless steel (A2-70) Thin-Wall Blind Bolts achieve a minimum tensile strength of 700 N/mm². This marginal strength advantage over carbon steel, combined with corrosion resistance, makes stainless steel the material of choice in marine, food processing, and offshore structural applications.

Aluminum blind bolts address applications where weight reduction outweighs load-bearing requirements. Aerospace interior panels, automotive trim assemblies, and electronics enclosures represent the core demand base. Aluminum fasteners compete directly with titanium at the lightweight end of the product spectrum, but aluminum holds a significant cost advantage for non-structural assemblies.

Titanium blind bolts command the highest unit price in the material segment and serve the most demanding performance environments. Their adoption concentrates in aerospace primary structures and defense applications where strength-to-weight ratio and corrosion immunity at extreme temperatures are mandatory. The volume is small but the margin per unit is the highest across all material categories.

Composite Materials represent an early-stage but strategically significant segment in blind bolt manufacturing. As composite substrates become more common in aerospace and automotive body structures, demand for compatible fasteners — those that do not create galvanic corrosion at the joint — will require purpose-designed composite-compatible blind bolt variants.

Others in the material segment include specialist coated or alloyed fasteners for niche industrial and defense procurement. In July 2024, Bossard Group completed the acquisition of Dejond Fastening NV, a Belgian blind rivet nut manufacturer, reflecting growing industry interest in broadening blind fastening material and product portfolios to serve specialized procurement requirements.

Diameter Analysis

M10 dominates with 26.8% due to versatile applicability across mid-range structural assemblies.

In 2025, M10 held a dominant market position in the By Diameter segment of the Blind Bolts Market, with a 26.8% share. The M10 diameter fits the load and clearance requirements of automotive body assembly, machinery frames, and general construction fixings. Its position at the center of the industrial fastener size range means a single SKU can satisfy procurement across multiple end-use categories.

M8 blind bolts serve lighter-duty assembly applications in automotive interiors, electronics enclosures, and thin-panel construction. Their smaller diameter allows installation in tight-clearance sections where M10 tooling cannot fit. However, their load capacity limits restrict use to non-structural joints, keeping the M8 segment below the M10 in overall volume.

M12 blind bolts bridge the gap between general-purpose mid-range fastening and heavy structural connections. Construction contractors and machinery OEMs specify M12 where M10 falls short of required tension or shear loads. This segment benefits directly from construction project scale-up and the shift toward larger modular building formats.

M16 blind bolts operate at the structural end of the diameter range. According to the 2025 manufacturer technical data, a standard M16 blind bolt carries a tension capacity of 38.8 kN and shear capacity of 62.8 kN per NZS 3404. These capacities satisfy primary structural steel connection requirements, making M16 the go-to diameter for steel frame construction where one-side access is the only option.

Others in the diameter segment include M20 and above, which serve the most demanding structural and heavy industrial applications. According to ICC-ES ESR-3330 reissued in March 2025, M20 stainless steel Hollo-Bolt fasteners carry an available tension LRFD load of 23,040 lbf. This regulatory-grade performance certification opens the M20 segment to formally specified structural construction procurement.

Grade Analysis

Grade 8.8 dominates with 40.9% due to broad structural suitability and standard procurement availability.

In 2025, Grade 8.8 held a dominant market position in the By Grade segment of the Blind Bolts Market, with a 40.9% share. Grade 8.8 represents the standard structural bolt classification under EN ISO 898-1, covering the widest range of load-bearing applications in construction and machinery. Its universal availability in distribution networks and compatibility with standard torque tools make it the default specification for most industrial procurement teams.

Grade 10.9 blind bolts deliver higher tensile performance at a proportionally higher cost, targeting applications where joint preload and fatigue resistance are critical. Automotive chassis assemblies and aerospace secondary structures represent its primary end-use base. According to the June 2025 manufacturer technical data sheet, the Property Class 10.9 set screw achieves F_u = 1000 N/mm², confirming its suitability for dynamic loading environments.

Grade 316 corresponds to stainless steel grade classification, targeting corrosion-critical environments including marine, chemical processing, and food manufacturing. Its inclusion as a distinct grade segment — rather than a material subset — reflects growing procurement sophistication, where buyers specify both material and mechanical performance simultaneously for fasteners in aggressive service environments.

End Use Industry Analysis

Automotive dominates with 26.5% due to lightweight assembly mandates and high fastener volume per vehicle.

In 2025, Automotive held a dominant market position in the By End Use Industry segment of the Blind Bolts Market, with a 26.5% share. Vehicle lightweighting programs — targeting both combustion engine fuel economy and electric vehicle range extension — require fastening solutions that secure thin-wall panels and hollow profiles without adding weight or requiring bilateral access. Blind bolts solve both constraints simultaneously, giving them a structural role that conventional fasteners cannot fill.

Aerospace demand for blind bolts concentrates in airframe assembly, interior structures, and maintenance repair operations. One-sided access in fuselage sections and wing cavities makes conventional bolting impractical at scale. The aerospace segment prioritizes certified performance and material traceability over unit cost, which drives specification of premium titanium and high-grade stainless steel blind fasteners.

Machinery and Equipment manufacturers specify blind bolts across assembly lines, conveyor frames, and enclosure panels where production efficiency requires rapid single-side installation. This segment values tooling compatibility and dimensional standardization above all other factors. Procurement cycles are longer and more price-sensitive than aerospace, making Steel Grade 8.8 the dominant specification in machinery fastening.

Construction represents the segment with the strongest structural certification requirements. Blind bolts used in hollow section steel connections must satisfy national structural codes, fire resistance classifications, and seismic performance categories. According to ICC-ES ESR-3330 reissued in March 2025, Hollo-Bolt fasteners carry approval for all Seismic Design Categories A through F — a critical compliance milestone for commercial building specification teams.

Others include wind energy, railway, and defense applications. Wind turbine assembly benefits from single-side installation in nacelle and tower segments where scaffold-free access reduces maintenance cost. Railway and metro car manufacturers require vibration-resistant blind fastening to maintain joint integrity across high-cycle loading environments — a performance requirement that conventional bolt-and-nut systems struggle to sustain reliably.

Key Market Segments

By Product Type

- Heavy-Duty Blind Bolts

- Thin-Wall Blind Bolts

By Material

- Steel

- Stainless Steel

- Aluminum

- Titanium

- Composite Materials

- Others

By Diameter

- M8

- M10

- M12

- M16

- Others

By Grade

- Grade 8.8

- Grade 10.9

- Grade 316

By End Use Industry

- Automotive

- Aerospace

- Machinery and Equipment

- Construction

- Others

Drivers

Aerospace One-Side Access Requirements and Automotive Lightweighting Mandates Accelerate Blind Bolt Specification

Aerospace engineers specify blind bolts where fuselage, wing, and nacelle cavities prevent bilateral fastener access. This is not a preference — it is a structural constraint. In 2024, Howmet Aerospace continued developing new blind fastener products through its Huck product teams, with innovations planned across 2025 from its Telford facility. This active R&D pipeline confirms that aerospace-driven demand justifies sustained investment at the product development level.

Automotive lightweighting programs create a parallel pull for blind bolts at high unit volumes. According to market data, the Automotive end-use industry accounts for 26.5% of total blind bolt demand — the highest share across all end-use segments. Each vehicle platform in a lightweight assembly program consumes hundreds of blind fasteners, meaning even modest new model adoption translates into significant volume shifts for fastener suppliers.

Infrastructure and construction projects in limited-access environments compound this demand further. Hollow structural sections in steel-frame buildings require one-side fastening tools and certified blind bolt connections. As modular construction volumes grow, the number of hollow section joints per project multiplies — expanding the total addressable fastener count per building and rewarding suppliers who hold structural certification ahead of the competition.

Restraints

High Unit Costs and Limited Installation Expertise Constrain Adoption Among Small-Scale Manufacturers

Precision-engineered blind bolts carry a significant price premium over standard bolting systems. A conventional hex bolt costs a fraction of a certified structural blind bolt with equivalent load ratings. For small-scale manufacturers operating on tight assembly margins, this cost gap discourages substitution — even when the installation efficiency advantage is clear. Price sensitivity remains the primary adoption barrier below the enterprise procurement tier.

Installation expertise adds a second constraint layer. Blind bolt systems require calibrated tooling, correct hole preparation, and knowledge of torque and clamping specifications. According to the June 2025 manufacturer technical data sheet, carbon steel Thin-Wall Blind Bolts require minimum tensile strength of 690 N/mm² and specific clamping range compliance. Without trained installers, joint integrity cannot be guaranteed — and liability-conscious manufacturers avoid specification risk by defaulting to familiar conventional fasteners.

Together, these two restraints reinforce each other. Higher cost justifies training investment only at scale; small shops rarely cross that threshold. Consequently, blind bolt penetration remains concentrated in large-volume aerospace, automotive, and construction accounts. Vendors who address this gap through simplified tooling and accessible technical support will unlock a currently underserved segment of the market.

Growth Factors

Electric Vehicle Battery Systems, Railway Manufacturing, and Aerospace MRO Expansion Open New Volume Channels

Electric vehicle battery enclosures and lightweight chassis platforms require fastening solutions that secure thin-wall aluminum and composite sections without access to the rear face. This is structurally identical to the access constraints that made blind bolts standard in aerospace — and the transition to EV platforms effectively creates a new, high-volume automotive fastening category where blind bolt suppliers with aerospace-grade product credentials hold an immediate advantage.

Railway and metro car manufacturers prioritize single-side fastening for carriage assembly and interior fit-out, where structural access is limited and vibration resistance is mandatory. In September 2024, Bossard Group acquired Aero Negoce International, a French aerospace fastening distributor, directly strengthening its supply chain position in precision fastening for transport industries. This acquisition signals that distributors are actively building the network infrastructure to serve aerospace MRO and adjacent transport sectors at scale.

According to the 2025 Lindapter UK catalogue, use of Hollo-Bolts in the citizenM Hotel Seattle modular construction project reduced construction time by approximately 4 months — from 17 months with traditional methods to 13 months total. This documented efficiency gain gives procurement teams in modular construction a concrete business case for specifying blind bolts. Time savings at this scale translate directly into financing cost reduction and earlier revenue generation for developers.

Emerging Trends

Corrosion-Resistant Materials, Vibration-Resistant Designs, and Automated Installation Tools Redefine Blind Bolt Performance Standards

Titanium and stainless steel blind bolt variants now address the durability gap that previously limited blind fasteners in offshore, marine, and chemical processing environments. Carbon steel Hollo-Bolt variants, rated for performance down to -45°C per the 2025 Lindapter UK catalogue, extend the operational envelope into cold-climate infrastructure and Arctic-region construction. Suppliers who hold certified low-temperature and corrosion ratings gain immediate specification access to projects that conventional blind fasteners cannot enter.

Locking and vibration-resistant blind bolt designs respond directly to railway, wind turbine, and heavy machinery requirements where dynamic loading cycles loosen conventional fasteners over time. According to the 2025 Lindapter UK catalogue, the Hollo-Bolt HCF mechanism for M16 and M20 sizes produces over three times more clamping force than the standard Hollo-Bolt of equivalent size. This tripled clamping force fundamentally changes the fatigue performance of blind connections in high-vibration applications — reducing maintenance frequency and extending service life.

Automated blind bolt installation tooling shifts the efficiency calculus for industrial assembly lines. Manual installation introduces torque variability and human error at high production volumes. As automotive and aerospace OEMs move toward lights-out and semi-automated assembly formats, fastener systems that integrate with robotic tooling heads gain a structural preference over manually installed alternatives. Early movers in automated blind bolt tooling compatibility will capture the assembly automation wave before tool standardization locks in competing systems.

Regional Analysis

Asia Pacific Dominates the Blind Bolts Market with a Market Share of 40.2%, Valued at USD 1.8 Billion

Asia Pacific holds a 40.2% share of the global Blind Bolts Market, valued at USD 1.8 Billion in 2025. This position reflects the region’s concentration of automotive manufacturing, shipbuilding, and large-scale infrastructure investment — all of which generate high blind fastener volumes. China, Japan, South Korea, and India collectively operate the world’s densest cluster of automotive and heavy engineering plants, each requiring precision fastening at industrial scale.

North America Blind Bolts Market Trends

North America sustains demand through its aerospace manufacturing base and a construction sector that increasingly specifies certified structural connections. The ICC-ES ESR-3330 approval process — a U.S. regulatory pathway for structural fastener certification — provides North American construction buyers with a formal specification framework. This regulatory infrastructure gives certified blind bolt suppliers a clear entry point into the commercial building segment that less-certified competitors cannot access.

Europe Blind Bolts Market Trends

Europe’s demand centers on aerospace, automotive, and wind energy — three sectors where blind bolt adoption is structurally embedded, not discretionary. Germany’s automotive manufacturing cluster and France’s aerospace supply chain together represent the continent’s largest procurement base for precision blind fasteners. European EN structural standards and CE marking requirements create a compliance-driven specification environment that rewards suppliers with pre-certified product ranges.

Latin America Blind Bolts Market Trends

Latin America’s blind bolt demand connects directly to construction activity in Brazil and Mexico, where infrastructure investment drives steel structural framing volumes. Adoption of hollow section steel construction in commercial real estate and industrial facilities creates specification opportunities for structural blind bolt suppliers. However, price sensitivity in regional procurement slows the shift from conventional bolting to certified blind fastening systems.

Middle East and Africa Blind Bolts Market Trends

The Middle East drives demand through large-scale commercial and infrastructure construction projects in GCC countries, where steel-framed buildings and modular construction methods are standard formats. Extreme heat and corrosive desert environments create specification demand for zinc-flake and stainless steel blind bolt variants. Africa’s market remains nascent, with demand concentrated in South African industrial manufacturing and mining infrastructure.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Howmet Aerospace (Huck Fastening Systems) operates as the incumbent technology leader in aerospace blind fastening, with its Huck product line embedded in commercial and defense airframe assembly globally. Its vertical integration — from fastener design to aerospace-certified manufacturing — creates a procurement lock-in that commodity suppliers cannot replicate. The ongoing development of new blind fastener products at its Telford facility in 2024–2025 signals a deliberate strategy to defend share in the high-margin aerospace structural segment.

Stanley Black & Decker (Stanley Engineered Fastening) leverages its global distribution infrastructure and multi-category industrial tooling presence to serve automotive and general manufacturing buyers at scale. Its strategic advantage is breadth — the ability to supply blind fasteners alongside the installation tools and adjacent fastening products that OEM assembly lines require from a single vendor relationship. This bundled supply model reduces procurement complexity for large manufacturing accounts.

LISI Aerospace concentrates its positioning in aerospace-grade blind fastening, where material traceability, certification depth, and proximity to Airbus and Safran supply chains define competitive standing. The company’s European manufacturing base aligns with the geography of commercial aircraft production. Its narrow but deep specialization in aerospace fastening means it competes on performance qualification rather than price — a defensible position in a segment where certification switching costs are high.

Arconic Corporation brings material science expertise — particularly in aluminum alloys — to its blind fastening product range. Its structural aluminum blind bolts serve aerospace and automotive lightweighting programs where both the fastener and the substrate are aluminum. This material alignment gives Arconic a differentiated position in composite and aluminum-intensive assemblies, where galvanic corrosion compatibility between fastener and base material is a mandatory specification requirement.

Key Players

- Howmet Aerospace (Huck Fastening Systems)

- Stanley Black & Decker (Stanley Engineered Fastening)

- LISI Aerospace

- Arconic Corporation

- Bossard Group

- Lindapter International

- EFC International

- TR Fastenings

- Würth Group

- Ganesh Industries

- Allfast Fastening Systems

- Perfect Point EDM, Corp.

- Owlett-Jaton

- Other Key Players

Recent Developments

- January 2024 — PennEngineering acquired Sherex Fastening Solutions, adding blind rivet nut and associated blind fastening technology to its product portfolio. This move expanded PennEngineering’s capabilities in the blind fastening category and increased competitive pressure on independent blind rivet nut specialists.

- July 2024 — Bossard Group completed the acquisition of Dejond Fastening NV, a Belgian manufacturer and distributor of blind rivet nuts. The deal strengthened Bossard’s technical capabilities in blind fastening components and extended its European manufacturing and distribution footprint.

- January 2025 — Bossard Group completed the acquisition of the Ferdinand Gross Group, a German fastening technology distributor. This acquisition expanded Bossard’s commercial presence across Germany and Eastern Europe, adding distribution scale in one of the continent’s largest industrial fastener markets.

- September 2024 — Bossard Group acquired Aero Negoce International (ANI), a French aerospace fastening solutions distributor. The acquisition strengthened Bossard’s position in the aerospace fastener supply chain and positioned the group to capture demand from European aerospace MRO and OEM procurement programs.

- 2024 — Howmet Aerospace continued active development of new blind fastener products through its Huck product teams at HFS Telford, with planned product innovations expected through 2025. This sustained R&D investment reflects Howmet’s strategy to maintain technical leadership in aerospace-grade blind fastening ahead of new aircraft program procurement cycles.

Report Scope

Report Features Description Market Value (2025) USD 4.6 Billion Forecast Revenue (2035) USD 7.0 Billion CAGR (2026-2035) 4.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Heavy-Duty Blind Bolts, Thin-Wall Blind Bolts), By Material (Steel, Stainless Steel, Aluminum, Titanium, Composite Materials, Others), By Diameter (M8, M10, M12, M16, Others), By Grade (Grade 8.8, Grade 10.9, Grade 316), By End Use Industry (Automotive, Aerospace, Machinery and Equipment, Construction, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Howmet Aerospace (Huck Fastening Systems), Stanley Black & Decker (Stanley Engineered Fastening), LISI Aerospace, Arconic Corporation, Bossard Group, Lindapter International, EFC International, TR Fastenings, Würth Group, Ganesh Industries, Allfast Fastening Systems, Perfect Point EDM Corp., Owlett-Jaton, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Howmet Aerospace (Huck Fastening Systems)

- Stanley Black & Decker (Stanley Engineered Fastening)

- LISI Aerospace

- Arconic Corporation

- Bossard Group

- Lindapter International

- EFC International

- TR Fastenings

- Würth Group

- Ganesh Industries

- Allfast Fastening Systems

- Perfect Point EDM, Corp.

- Owlett-Jaton

- Other Key Players

Our Clients

- 180927

- Mar 2026