Global Bioimpedance Devices Market By Product Type (Multi-frequency, Dual-frequency and Single-frequency), By Modality (Wired and Wireless), By Application (Whole-body and Segmental), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178389

- Number of Pages: 344

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

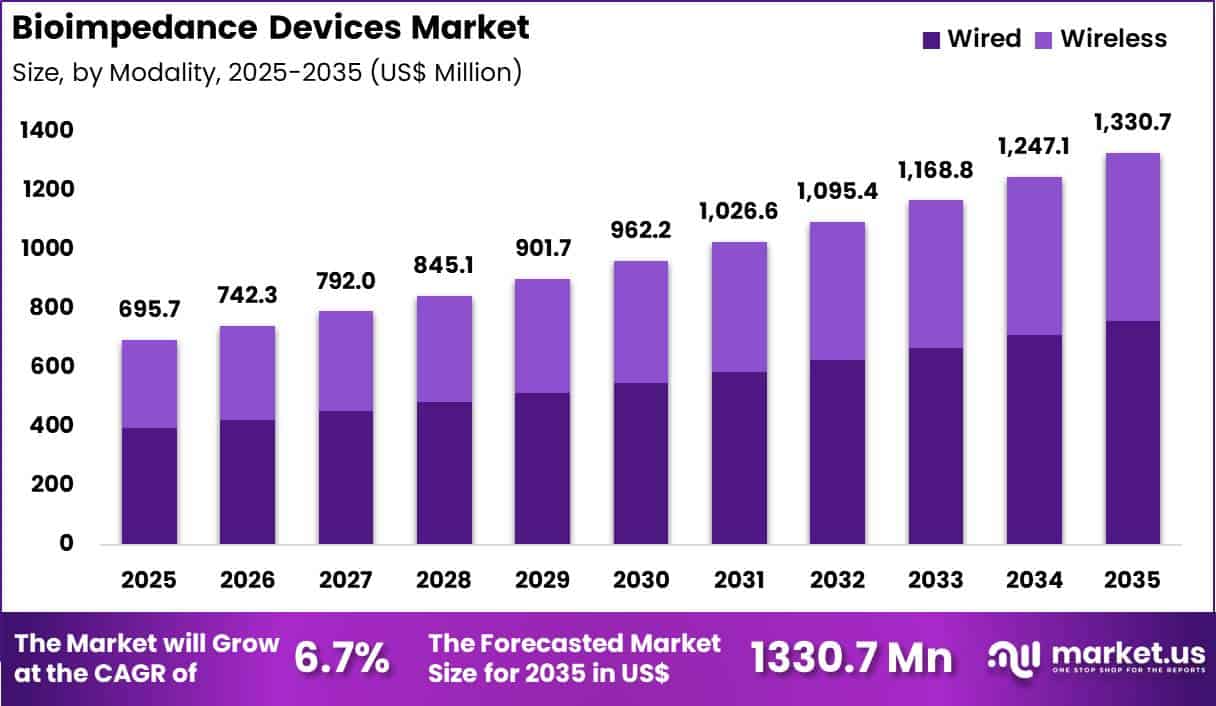

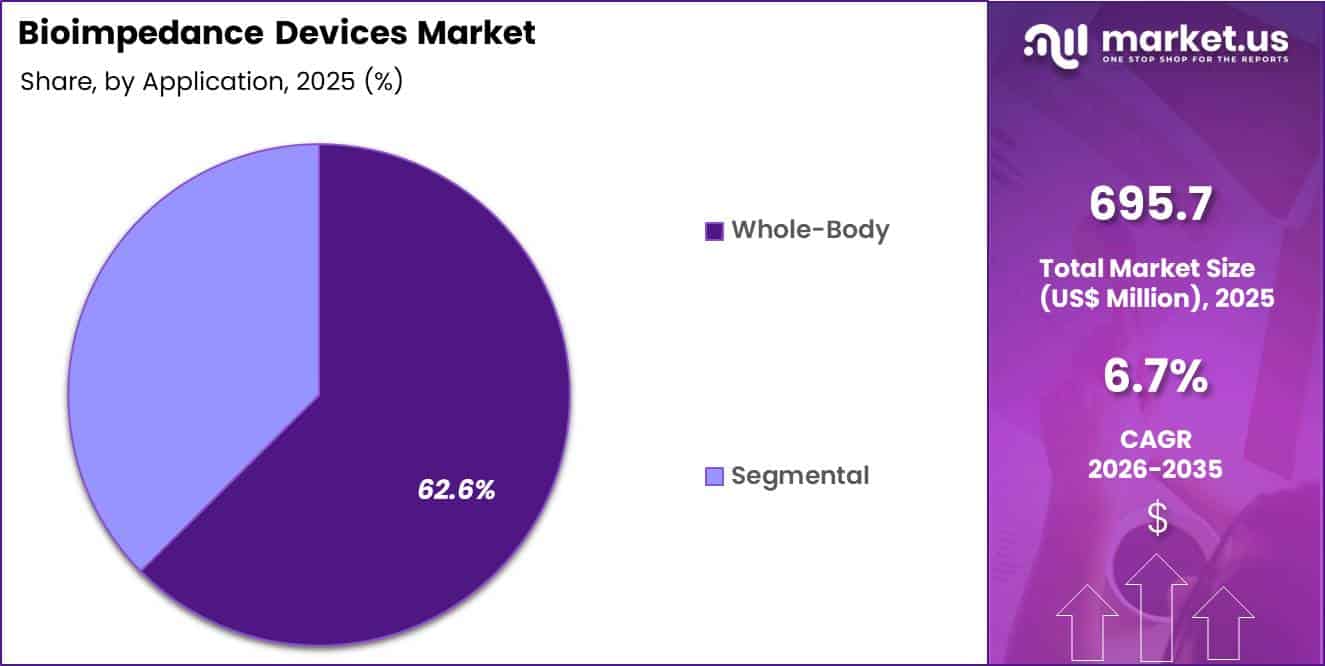

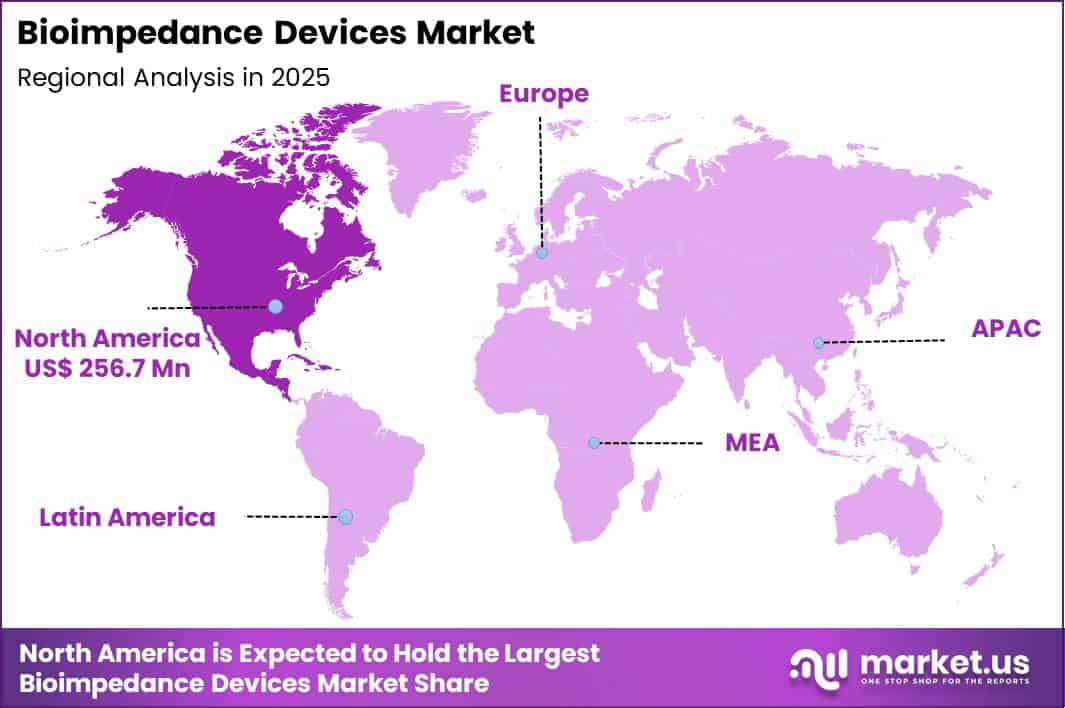

The Global Bioimpedance Devices Market size is expected to be worth around US$ 1330.7 Million by 2035 from US$ 695.7 Million in 2025, growing at a CAGR of 6.7% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 36.9% share with a revenue of US$ 256.7 Million.

Increasing awareness of body composition’s critical role in managing chronic diseases and optimizing athletic performance propels the bioimpedance devices market as clinicians and fitness professionals seek accurate, non-invasive tools for real-time physiological assessment.

Physicians increasingly rely on bioimpedance analyzers to evaluate fluid status in heart failure patients, guiding diuretic therapy and preventing hospital readmissions through precise extracellular and intracellular water measurements. These devices support nutritional monitoring in oncology and critical care, where practitioners track lean body mass changes to adjust feeding protocols and improve recovery outcomes.

Sports scientists apply multi-frequency bioimpedance spectroscopy to assess muscle hydration and fat distribution in elite athletes, informing training regimens and injury prevention strategies. Clinicians also utilize the technology in lymphedema management, quantifying limb volume shifts to evaluate treatment efficacy and tailor compression therapies.

Manufacturers pursue opportunities to integrate bioimpedance sensors into wearable patches and smart scales, expanding applications in home-based chronic disease management where patients self-monitor fluid balance and body composition between clinical visits.

Developers advance AI-enhanced platforms that deliver personalized insights, broadening utility in metabolic research and preventive wellness programs. These innovations facilitate seamless data integration with electronic health records, streamlining workflows for multidisciplinary teams.

Opportunities emerge in veterinary applications for monitoring fluid status in large animals and in research settings for studying sarcopenia in aging populations. Recent trends emphasize multi-frequency and segmental analysis combined with cloud connectivity, positioning bioimpedance devices as essential tools for precision health monitoring across clinical, fitness, and wellness environments.

Key Takeaways

- In 2025, the market generated a revenue of US$ 695.7 Million, with a CAGR of 6.7%, and is expected to reach US$ 1330.7 Million by the year 2035.

- The product type segment is divided into multi-frequency, dual-frequency and single-frequency, with multi-frequency taking the lead with a market share of 48.9%.

- Considering modality, the market is divided into wired and wireless. Among these, wired held a significant share of 57.2%.

- The application segment is segregated into whole-body and segmental, with the whole-body segment leading the market, holding a revenue share of 62.6%.

- North America led the market by securing a market share of 36.9%.

Product Type Analysis

Multi-frequency devices contributed 48.9% of growth within product type and led the bioimpedance devices market due to their superior ability to differentiate between intracellular and extracellular fluid compartments. Clinicians and researchers prefer multi-frequency systems because they provide more accurate body composition and hydration analysis across diverse patient groups.

Hospitals rely on detailed impedance profiling for managing renal disorders, heart failure, and critical care fluid balance. Higher analytical precision strengthens clinical decision-making and outcome monitoring.

Growth strengthens as demand increases for advanced nutritional assessment and chronic disease management tools. Multi-frequency technology supports comprehensive evaluation in oncology and sports medicine.

Expanding clinical evidence validates its diagnostic reliability compared to single-frequency models. Healthcare providers prioritize precision measurement in complex cases. The segment is expected to remain dominant as accurate body composition assessment becomes central to patient management strategies.

Modality Analysis

Wired systems accounted for 57.2% of growth within modality and dominated the bioimpedance devices market due to their stability, signal consistency, and integration with hospital infrastructure. Clinicians favor wired configurations because they reduce data transmission interference and support reliable measurement during inpatient monitoring. Hospitals deploy wired systems in dialysis units and intensive care settings where precision remains critical. Established clinical workflows further reinforce preference for wired connectivity.

Growth continues as healthcare facilities invest in dependable diagnostic infrastructure. Wired systems support seamless integration with existing monitoring equipment and electronic records. Maintenance simplicity and predictable performance strengthen procurement decisions.

Training familiarity among clinical staff also supports sustained use. The segment is anticipated to maintain leadership as institutional environments prioritize measurement accuracy and operational reliability.

Application Analysis

Whole-body applications generated 62.6% of growth within application and emerged as the leading segment due to the widespread use of comprehensive body composition assessment in clinical and wellness settings. Physicians rely on whole-body impedance analysis to evaluate hydration status, muscle mass, and fat distribution in a single procedure.

Chronic disease management programs incorporate whole-body monitoring to track long-term patient progress. Rising interest in preventive health and fitness assessment increases utilization across demographics.

Growth accelerates as obesity and metabolic disorders become more prevalent globally. Nutrition counseling and rehabilitation programs adopt whole-body measurements to tailor interventions. Sports performance centers also rely on comprehensive data for training optimization.

Broader awareness of body composition beyond weight metrics strengthens demand. The segment is projected to remain dominant as holistic health assessment continues to gain importance in both medical and consumer health contexts.

Key Market Segments

By Product Type

- Multi-frequency

- Dual-frequency

- Single-frequency

By Modality

- Wired

- Wireless

By Application

- Whole-body

- Segmental

Drivers

Increasing prevalence of chronic kidney disease is driving the market.

The growing number of patients with chronic kidney disease has substantially increased the need for bioimpedance devices to monitor fluid status and body composition accurately. Improved screening programs have led to earlier identification of CKD cases requiring regular fluid assessment. Healthcare providers rely on these devices during dialysis to optimize ultrafiltration and prevent complications.

The correlation between CKD progression and fluid imbalance underscores the importance of precise measurement tools. Government health agencies track rising CKD cases to guide resource allocation in nephrology departments. Bioimpedance spectroscopy offers non-invasive, real-time data that supports better clinical decisions.

National registries document the expanding patient population, prompting wider adoption of these technologies. Key manufacturers are enhancing device sensitivity to meet the demands of dialysis centers. This driver fosters integration of bioimpedance in standard renal care protocols.

According to the Centers for Disease Control and Prevention, approximately 37 million adults in the United States had chronic kidney disease as reported in recent surveillance data covering the early 2020s.

Restraints

High device and operational costs are restraining the market.

The elevated pricing of professional-grade bioimpedance analyzers restricts their acquisition by smaller clinics and outpatient facilities. Complex multi-frequency sensors and calibration requirements add to manufacturing expenses passed on to end-users. Many healthcare settings face budget limitations that delay replacement of older equipment.

Regulatory compliance for medical-grade accuracy increases validation and maintenance costs. In public health systems, procurement often favors lower-cost alternatives despite reduced precision. Providers may limit usage to high-priority cases to control operational spending. This restraint is particularly evident in resource-limited regions with constrained reimbursement.

Industry efforts to develop more affordable models have progressed slowly due to quality standards. Despite clinical advantages, economic factors slow broader implementation across diverse care settings. Consequently, cost barriers continue to limit market penetration in non-specialized environments.

Opportunities

Strong revenue growth from clinical bioimpedance solutions is creating growth opportunities.

The consistent increase in sales of bioimpedance devices for clinical applications signals significant potential for expanded use in nephrology and cardiology. Improved financial performance enables investments in next-generation sensors and software integration. Healthcare collaborations facilitate wider distribution and training programs for medical staff.

Strategic partnerships with dialysis providers support customized solutions for fluid management. The substantial revenue base amplifies funding for research into new clinical indications. Policy advancements in chronic disease management strengthen infrastructure for device adoption.

ImpediMed reported total revenue of A$ 6.6 million in 2022, rising to A$8.5 million in 2023. This growth reflects rising demand for SOZO devices in oncology and lymphoedema applications. This opportunity aligns with efforts to enhance non-invasive monitoring in outpatient and home settings. Focused expansions can capture additional share in high-growth clinical segments.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the bioimpedance devices market through hospital spending patterns, research budgets, and wellness segment demand. Inflation and higher interest rates increase costs for electronic components, logistics, and financing, which slows equipment upgrades in clinics and fitness centers. Geopolitical tensions disrupt supplies of sensors, circuit boards, and specialty materials, creating procurement uncertainty and longer lead times.

Current US tariffs on imported electronics and finished medical devices raise production and distribution expenses, which compresses margins and complicates pricing strategies. These pressures affect smaller manufacturers and limit adoption in price sensitive markets. On the positive side, trade exposure supports domestic assembly, supplier diversification, and closer quality control.

Growing focus on body composition monitoring, renal care assessment, and sports performance sustains clinical and consumer interest. With efficient sourcing, software integration, and broader application reach, the market remains positioned for steady and confident growth.

Latest Trends

Launch of consumer-grade wearable bioimpedance devices is a recent trend in the market.

In 2024, the introduction of wearable bioimpedance mats and integrated smart scales has expanded access to body composition analysis beyond clinical settings. These devices combine multi-frequency technology with smartphone connectivity for convenient home monitoring. Manufacturers have prioritized user-friendly designs and accurate algorithms validated against clinical standards.

Consumer adoption has accelerated for fitness tracking and nutritional planning applications. Amazfit launched its Body Composition Analyzer Mat in March 2024, integrating bioimpedance with the Amazfit Balance wearable for comprehensive health metrics. This development targets wellness enthusiasts seeking daily insights into muscle mass and hydration.

The trend emphasizes seamless data synchronization with health apps for personalized recommendations. Regulatory pathways have supported clearance for non-medical wellness use. Industry collaborations refine sensor accuracy for diverse body types. These innovations position wearable bioimpedance as a key advancement in preventive health monitoring.

Regional Analysis

North America is leading the Bioimpedance Devices Market

North America accounted for a 36.9% share of the Bioimpedance Devices market in 2024, supported by rising demand for noninvasive body composition and fluid status monitoring across clinical and wellness settings. Hospitals increasingly adopted impedance based systems to assess fluid balance in cardiac and renal patients, improving early intervention decisions. Sports medicine centers and weight management clinics expanded use of body composition analyzers to guide personalized treatment plans.

Growth in preventive healthcare awareness encouraged consumers to track fat mass, muscle mass, and hydration levels more consistently. Integration with digital health platforms enhanced real time data sharing between patients and providers. Academic research in oncology and lymphedema management also strengthened clinical adoption.

A relevant supporting indicator comes from the Centers for Disease Control and Prevention, which reported in 2023 that about 37 million Americans live with chronic kidney disease, highlighting sustained clinical need for reliable fluid assessment technologies.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Bioimpedance Devices market in Asia Pacific is expected to grow steadily during the forecast period as healthcare systems focus on chronic disease monitoring and preventive health programs. Governments promote early screening for cardiovascular and metabolic disorders to reduce long term treatment costs.

Fitness centers and wellness chains expand advanced body composition analysis services to meet rising consumer interest in health tracking. Hospitals integrate impedance based monitoring into dialysis and heart failure management protocols. Growing middle class populations increase spending on personal health technologies.

Local manufacturers introduce cost competitive analyzers that broaden market reach. A verifiable signal of regional health demand appears in 2023 data from the World Health Organization, which confirmed that cardiovascular diseases remain the leading cause of death globally, reinforcing the need for accurate fluid and body composition monitoring across Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the bioimpedance devices market grow by refining sensor accuracy, expanding multi-frequency analytics, and enhancing software interfaces that help clinicians and researchers capture more actionable body composition and fluid status insights. They also strengthen value propositions by integrating connectivity with electronic health records and cloud-based dashboards that support longitudinal tracking and remote patient management.

Firms pursue strategic partnerships with hospitals, sports science centers, and wellness platforms to embed their solutions into broader care and performance programs, which expands use cases beyond traditional clinical settings. Geographic expansion into Europe, North America, and rising Asia Pacific markets diversifies revenue streams and taps growing demand for preventive health technologies.

InBody Co., Ltd. exemplifies a specialized bioimpedance technology company with a wide range of body composition analyzers, strong global distribution channels, and coordinated commercialization strategies that align device capabilities with evolving healthcare and fitness priorities.

The company advances its competitive stance through disciplined investment in product innovation, targeted collaborations, and a customer-centric approach that translates practical insights into measurable adoption and loyalty.

Top Key Players

- InBody

- Tanita

- seca

- Bodystat

- Maltron International

- Omron Healthcare

- RJ-L Systems

- Fresenius Medical Care

- Withings

- Hologic

Recent Developments

- In 2025, InBody Co., Ltd. reported revenue of 226.6 billion KRW, approximately US$ 168 million, for the twelve months ended September 30. The company attributed this performance to growing global adoption of its professional body composition analyzers, which apply multi-frequency bioelectrical impedance technology to deliver detailed assessments of metabolic status and fluid distribution across clinical, research, and premium fitness environments.

- In 2025, Omron Corporation announced that its Healthcare division generated net sales of 801.8 billion JPY, roughly US$ 5.25 billion, for the year. The division’s results were supported by expanding demand for bioimpedance-based body composition monitors and connected health devices, alongside a strategic emphasis on data-enabled home monitoring solutions that allow individuals to track metrics such as body fat composition and visceral fat levels.

Report Scope

Report Features Description Market Value (2025) US$ 695.7 Million Forecast Revenue (2035) US$ 1330.7 Million CAGR (2026-2035) 6.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Multi-frequency, Dual-frequency and Single-frequency), By Modality (Wired and Wireless), By Application (Whole-body and Segmental) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape InBody, Tanita, seca, Bodystat, Maltron International, Omron Healthcare, RJ-L Systems, Fresenius Medical Care, Withings, Hologic Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Bioimpedance Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Bioimpedance Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- InBody

- Tanita

- seca

- Bodystat

- Maltron International

- Omron Healthcare

- RJ-L Systems

- Fresenius Medical Care

- Withings

- Hologic

Our Clients

- 178389

- Feb 2026