Quick Navigation

Report Overview

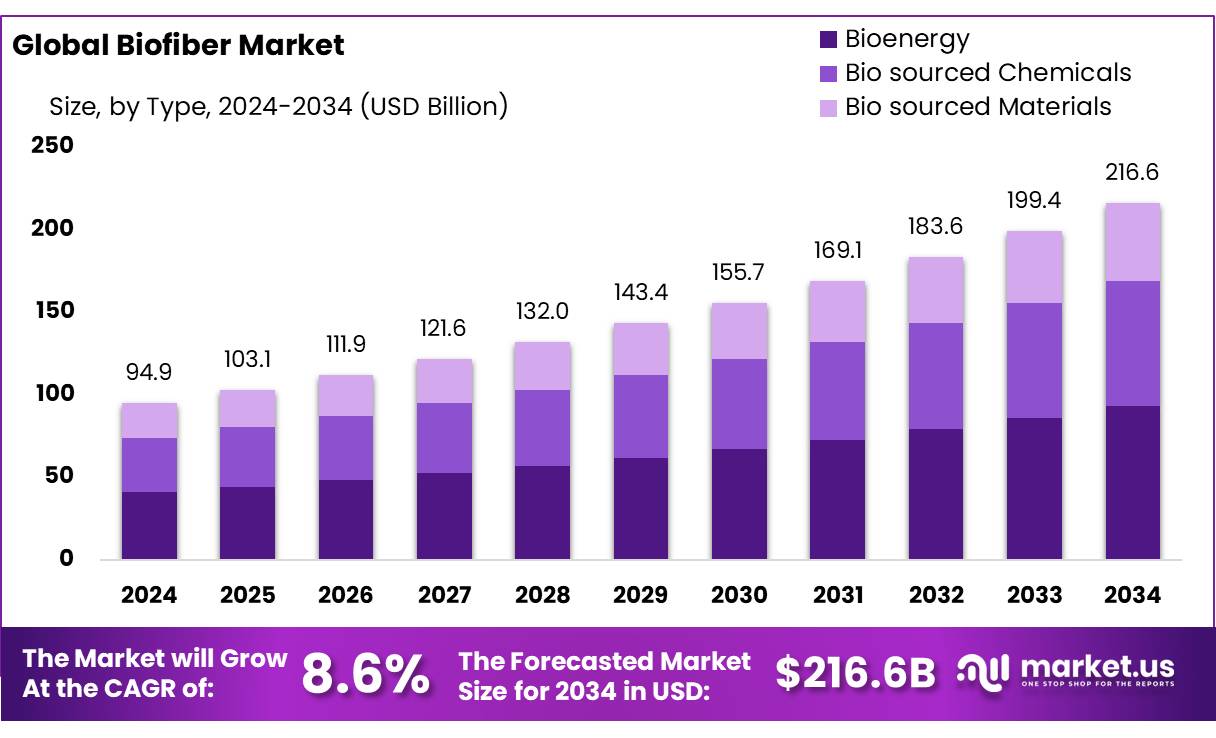

The Global Biofiber Market size is expected to be worth around USD 216.6 Bn by 2034, from USD 94.9 Bn in 2024, growing at a CAGR of 8.6% during the forecast period from 2025 to 2034.

The global biofiber market refers to the production, utilization, and commercial activities surrounding bio-based fibers, which are derived from natural sources like plants, animals, and minerals. Biofibers are increasingly being used in a wide range of industries including textiles, automotive, construction, packaging, and medical applications, owing to their environmental benefits over synthetic fibers. The growing demand for sustainable and eco-friendly materials has triggered a shift towards biofiber-based alternatives, as industries seek to reduce their environmental footprint and adhere to government regulations on sustainability.

Among the various types of biofibers, plant-based fibers, such as cotton, jute, hemp, and flax, hold a substantial market share, accounting for more than 60% of the global market. The automotive industry is one of the leading end-users of biofibers, particularly in the production of lightweight composite materials for vehicle components. Additionally, textiles and packaging are significant application segments, which are expected to grow substantially due to rising demand for sustainable consumer goods.

Governments worldwide are introducing stricter environmental regulations that push industries to adopt sustainable practices. For example, the European Union’s Circular Economy Action Plan encourages the use of sustainable materials in product manufacturing, fostering demand for biofibers. The increasing adoption of biofibers, such as hemp, flax, and bamboo, in textile production will continue to rise, driven by consumer demand for organic, sustainable clothing.

Key Takeaways

- Biofiber Market size is expected to be worth around USD 216.6 Bn by 2034, from USD 94.9 Bn in 2024, growing at a CAGR of 8.6%.

- Bioenergy segment of the biofiber market held a dominant position, capturing more than a 43.4% share.

- Mechanical Processing in the biofiber market held a dominant position, capturing more than a 37.8% share.

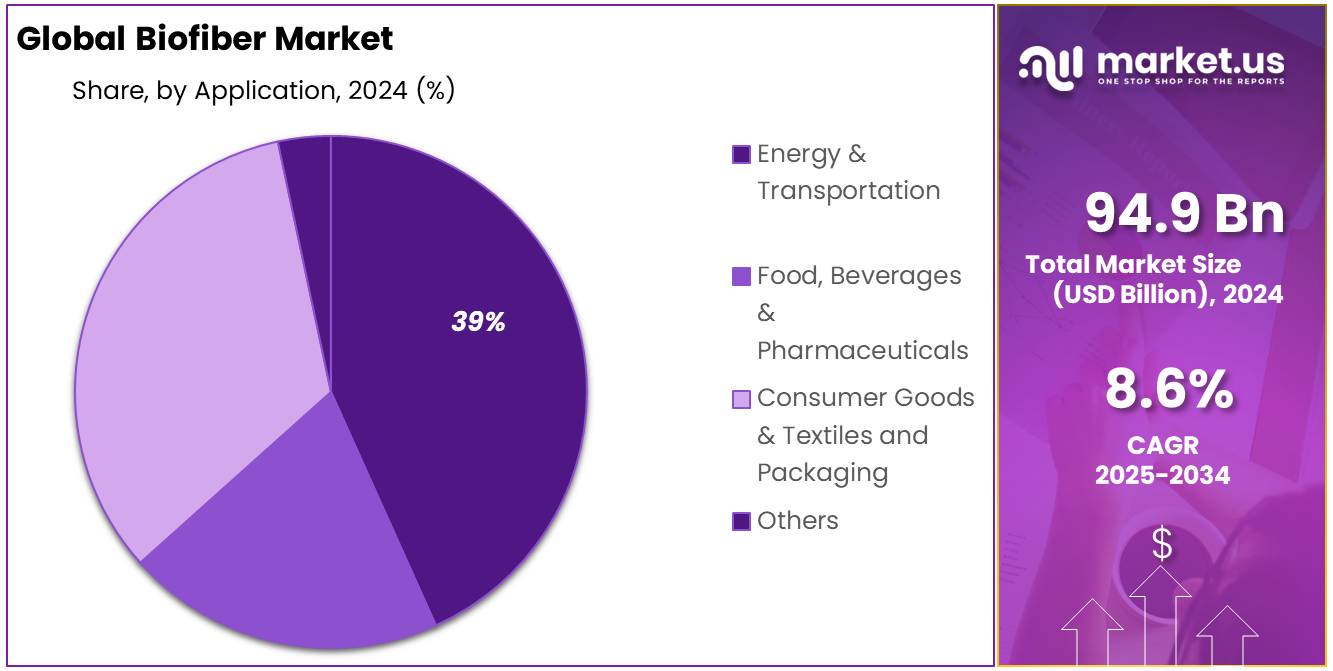

- Energy & Transportation segment of the biofiber market held a dominant position, capturing more than a 39.2% share.

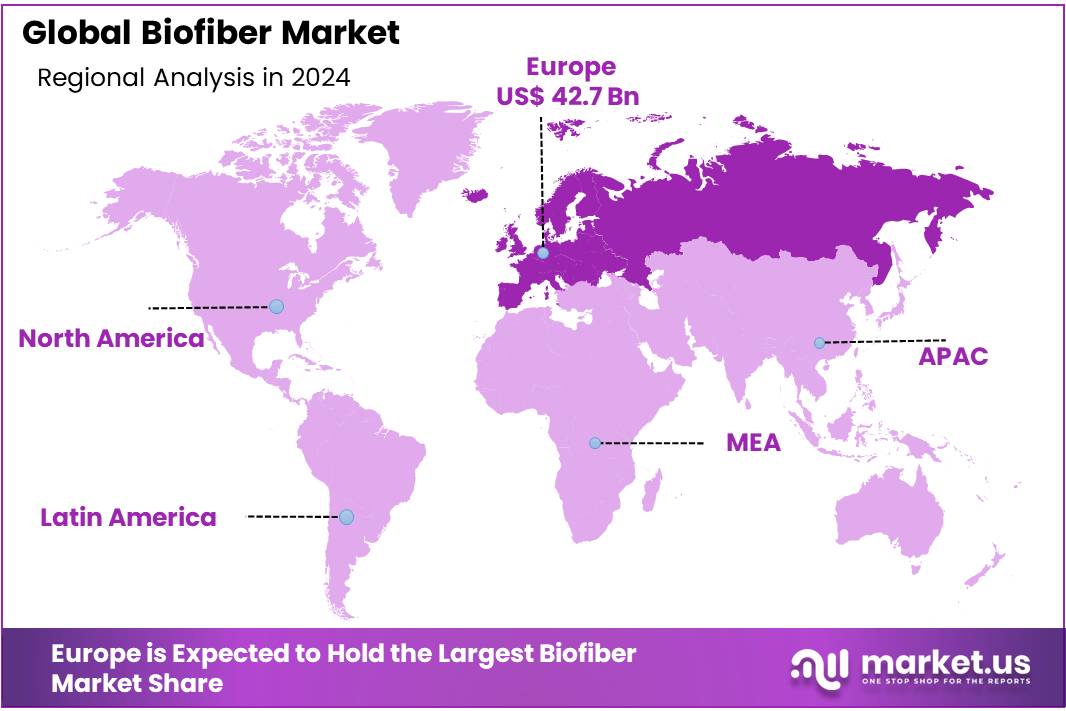

- Europe as the dominating region, holding a substantial 45.1% market share, equating to approximately USD 42.7 billion.

Ву Туре

In 2024, the Bioenergy segment of the biofiber market held a dominant position, capturing more than a 43.4% share. This segment has experienced significant growth due to increasing global demand for renewable energy sources as a means to reduce carbon footprints and mitigate the effects of climate change. Bioenergy, derived from biological sources, is pivotal in the transition towards more sustainable energy systems.

The segment of Bio-sourced Chemicals also plays a crucial role in the market, focusing on replacing conventional petrochemicals with more sustainable, bio-based alternatives. These chemicals are used in a wide array of products, including plastics, lubricants, and solvents, contributing to reduced environmental impact and enhanced biodegradability.

Meanwhile, Bio-sourced Materials include polymers and composites derived from plant fibers, which are increasingly used in industries such as automotive, construction, and textiles. These materials offer significant environmental benefits, such as lower greenhouse gas emissions and reduced reliance on fossil resources.

By Processing Method

In 2024, Mechanical Processing in the biofiber market held a dominant position, capturing more than a 37.8% share. This method, favored for its efficiency and cost-effectiveness, involves physical methods to extract fibers from plants without altering their natural composition. Industries such as textiles and composites widely adopt mechanical processing to retain the strength and durability of natural fibers, making it a preferred choice for manufacturing environmentally friendly products.

Chemical Processing, another key segment, utilizes chemicals to break down plant materials and extract fibers. This method is crucial for producing finer and more uniform fibers, which are essential in applications requiring high material consistency like in the production of bio-plastics and non-woven textiles.

Biological Processing, which involves the use of enzymes or other biological agents to extract fibers, is gaining traction due to its eco-friendliness and ability to maintain the integrity of fibers. This method is particularly important in the paper and pulp industries, where the demand for less chemically intensive processes is increasing.

By Application

In 2024, the Energy & Transportation segment of the biofiber market held a dominant position, capturing more than a 39.2% share. This sector primarily utilizes biofibers for bioenergy applications such as biofuel production and biocomposites for automotive parts. The growing emphasis on reducing carbon emissions and reliance on fossil fuels has significantly driven the adoption of biofibers in manufacturing and energy sectors, aligning with global sustainability targets.

The Food, Beverages & Pharmaceuticals segment leverages biofibers for various applications, including dietary fiber enhancement in functional foods, biodegradable packaging solutions, and as excipients in pharmaceutical formulations. This segment benefits from the increasing consumer demand for natural and sustainable products, which in turn boosts the use of biofibers.

Consumer Goods & Textiles is another significant application area, where biofibers are integrated into products ranging from eco-friendly clothing to biodegradable consumer goods. The market growth in this segment is propelled by the rising awareness among consumers about the environmental impacts of synthetic fibers and plastics, thus shifting preference towards sustainable alternatives.

Packaging segment, which uses biofibers to create sustainable packaging solutions, is gaining traction as businesses and consumers alike seek to reduce the environmental footprint of their packaging materials. The drive towards reducing plastic waste has particularly accentuated the need for innovative, bio-based packaging options that can effectively replace conventional materials.

Key Market Segments

Ву Туре

- Bioenergy

- Bio sourced Chemicals

- Bio sourced Materials

By Processing Method

- Mechanical Processing

- Chemical Processing

- Biological Processing

- Others

By Application

- Energy & Transportation

- Food, Beverages & Pharmaceuticals

- Consumer Goods & Textiles and Packaging

- Others

Drivers

Increasing Demand for Sustainable Packaging Solutions

One of the primary drivers for the growth of the biofiber market is the escalating demand for sustainable packaging solutions across various industries, particularly in food and beverages. This surge is largely fueled by consumer preferences shifting towards environmentally friendly products and the global push for sustainable manufacturing practices.

Significant contributions to this trend come from large food organizations aiming to reduce their environmental footprint. For instance, companies like Nestlé and Unilever have committed to making 100% of their packaging recyclable or reusable by 2025, driving the need for bio-based packaging materials such as biofibers. These commitments are not just corporate decisions but are also responses to regulatory pressures. For example, the European Union’s directive on single-use plastics pushes for a substantial reduction in plastic waste, encouraging the use of biodegradable and compostable materials like biofibers.

Moreover, governmental initiatives across the globe support the development and adoption of sustainable materials. The U.S. Department of Agriculture (USDA) promotes biobased products through its BioPreferred program, which prioritizes the purchase of biobased products, including those made from biofibers, for federal agencies and contractors. This program not only supports the biofiber market but also assures consumers about the safety and sustainability of these products.

The combination of consumer demand, corporate sustainability goals, and supportive government policies creates a robust environment for the growth of the biofiber market. This trend is expected to continue, as the benefits of sustainable packaging—such as reduced environmental impact and enhanced brand image—are increasingly recognized by consumers and businesses alike. This driving factor is crucial in propelling the biofiber market forward, making biofibers a key component in the transition towards greener packaging solutions.

Restraints

High Cost of Production

One of the major restraining factors in the biofiber market is the high cost of production associated with bio-based materials. Biofibers are derived from natural or agricultural sources, which can be more expensive to process compared to synthetic fibers. This price disparity is often due to the advanced technology required to extract and refine biofibers and the lower economies of scale in bio-based production methods.

For instance, companies in the food industry that are transitioning towards sustainable packaging often face higher initial costs. This shift can be financially challenging, particularly for small to medium-sized enterprises (SMEs) that operate with tighter budgets. Despite the environmental benefits, the economic implications can deter companies from adopting biofiber-based solutions. This economic challenge is underscored by a report from the Food and Agriculture Organization (FAO), which highlights the need for cost-effective sustainable materials to meet global sustainability targets without imposing undue financial burdens on producers.

Government initiatives have been crucial in attempting to mitigate these costs. Programs such as the USDA’s BioPreferred program, which I mentioned earlier, aim to increase the purchase and use of biobased products. These initiatives are designed to help reduce the cost disparity over time by fostering market growth and improving production technologies through subsidies and grants.

Despite these efforts, the high cost of production remains a significant barrier. This factor not only affects the competitive pricing of biofiber-based products in the market but also limits the widespread adoption and scalability of such solutions. Addressing these cost issues is essential for the biofiber industry to grow and compete effectively with traditional synthetic materials.

Opportunity

Expansion into Biodegradable Products

A significant growth opportunity in the biofiber market is the expansion into biodegradable products, particularly within the food and beverage industry. As consumer awareness and regulatory pressures increase regarding environmental sustainability, the demand for biodegradable packaging and products has surged. This trend is not only driven by consumer preference but also by new regulations aimed at reducing plastic waste.

Leading food organizations and industries are actively seeking alternatives to traditional plastics to align with global sustainability goals. For instance, major companies in the food sector, such as McDonald’s and Starbucks, have committed to transitioning to fully sustainable packaging solutions by 2025. These commitments are part of a broader industry trend towards reducing the environmental impact of packaging and enhancing corporate social responsibility profiles.

Governments worldwide are supporting this shift through initiatives and regulations that promote the use of environmentally friendly materials. The European Union, for example, has implemented strict guidelines that mandate reductions in single-use plastics, which directly encourages the adoption of biodegradable biofibers in packaging. Similarly, the United States has seen an increase in local and state regulations that favor biodegradable and compostable products, providing a fertile legislative environment for the growth of bio-based materials.

This pivot towards biodegradable products represents a substantial growth avenue for the biofiber industry. By capitalizing on the increasing legislative and consumer demand for sustainable products, companies in the biofiber sector can expand their market share and contribute to a more sustainable global economy. This move not only opens up new business opportunities but also plays a crucial role in the global effort to reduce pollution and protect natural ecosystems.

Trends

Integration of Nanotechnology in Biofiber Production

A major trend emerging in the biofiber market is the integration of nanotechnology, particularly in the development of enhanced biofiber materials for the food packaging industry. This technological advancement is geared towards improving the mechanical and barrier properties of biofibers, making them more competitive with traditional synthetic materials. Nanotechnology allows for the manipulation of biofibers at the molecular level, which can significantly enhance their functionality by making them lighter, stronger, and more resistant to moisture and air.

Leading food organizations are recognizing the potential of nano-enhanced biofibers to revolutionize packaging. For example, companies like PepsiCo and Nestlé are exploring biodegradable packaging solutions that incorporate nanotechnology to extend the shelf life of their products while reducing environmental impact. These efforts are supported by increasing consumer demand for sustainable packaging options that do not compromise food quality or safety.

Government initiatives also play a critical role in supporting this trend. Agencies such as the U.S. Environmental Protection Agency (EPA) and the European Food Safety Authority (EFSA) are facilitating research and approval processes for nano-enhanced biofibers, ensuring they meet safety standards before reaching the market. These efforts are crucial for maintaining public trust and acceptance of nanotechnology in consumer products.

The application of nanotechnology in biofiber production represents a significant growth opportunity, offering a way to meet both consumer expectations and regulatory requirements for sustainability and safety. As this trend continues to develop, it promises to open up new avenues for innovation within the biofiber industry, potentially leading to broader applications beyond food packaging, such as in textiles and medical devices. This integration marks a pivotal step towards more sustainable and functional materials in various industries.

Regional Analysis

In 2024, the biofiber market sees Europe as the dominating region, holding a substantial 45.1% market share, equating to approximately USD 42.7 billion. This leadership stems primarily from Europe’s advanced regulatory frameworks which promote environmental sustainability and bioeconomy. The European Union’s stringent environmental policies drive the adoption of bio-based and biodegradable materials across various industries, including packaging, automotive, and textiles.

North America also represents a significant portion of the biofiber market, driven by increasing environmental awareness among consumers and supportive governmental policies. The United States and Canada are pioneering the use of biofibers in energy, particularly bioenergy and biofuel sectors, leveraging the region’s extensive agricultural output as a source of raw materials.

The Asia Pacific region is witnessing rapid growth in the biofiber market, fueled by industrialization and the escalating need for sustainable materials. Countries like China and India are leading this expansion, with their vast agricultural sectors providing ample biofiber resources. This region’s market growth is also bolstered by increasing governmental initiatives aimed at reducing reliance on synthetic fibers.

The Middle East & Africa, along with Latin America, although smaller in market share, are emerging as significant players in the biofiber market. These regions are exploring biofibers’ potential in diverse applications, from construction to textile industries, driven by economic diversification efforts and increasing foreign investment in sustainable technologies.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In the biofiber market, several key players are driving innovation and growth across various regions and applications. NatureWorks, Dupont, and BASF are among the frontrunners, leveraging their expertise in chemical engineering and material science to develop advanced biofibers used in everything from packaging to automotive components. These companies are at the forefront of the push towards biodegradable and renewable materials, responding to both environmental concerns and consumer demand for sustainable products.

Another set of important contributors includes Cargill, Novamont, and Lenzing AG, which specialize in producing bio-based materials that serve a range of industries, including textiles and consumer goods. Lenzing, for example, is known for its eco-friendly fibers like Tencel and modal, which are derived from wood cellulose and are popular in the fashion industry for their sustainability and comfort. Meanwhile, companies like Neste Oil Rotterdam and ADM are pivotal in the bioenergy sector, focusing on converting agricultural outputs into biofuels and energy sources, thus supporting the energy sector’s shift away from fossil fuels.

Lastly, newer entrants like Kingfa and Mitsubishi are making significant strides in integrating biofibers into more traditional industries like construction and electronics, showcasing the versatility and broad potential of biofibers. Alongside these are specialized players like Renewable Energy Group and Enviva, which focus on specific niches within the biofiber market, such as biodiesel production and wood pellet manufacturing, respectively. Together, these companies not only contribute to the market’s growth but also its diversification, driving innovation in sustainable materials across the globe.

Top Key Players

- NatureWorks

- Dupont

- BASF

- Cargill

- Novamont

- Lenzing AG

- Neste Oil Rotterdam

- ADM

- Infinita Renovables

- Arkema

- Braskem

- Kingfa

- Mitsubishi

- Sofiproteol

- Medors

- Marseglia Group

- Glencore

- Louis Dreyfus

- Renewable Energy Group

- RBF Port Neches

- Ag Processing

- Elevance

- Marathon Petroleum Corporation

- Graanul Invest Group

- Enviva

- Pinnacle

Recent Developments

In 2024 NatureWorks, launched a new high-heat PLA product, Ingeo 2600, which offers improved melt strength and toughness suitable for a range of applications from food packaging to automotive parts.

In 2024 BASF, has introduced a new bio-based polyurethane with a 30% biofiber content, specifically designed for the footwear industry, demonstrating the company’s commitment to expanding the application range of biofibers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 94.9 Bn |

| Forecast Revenue (2034) | USD 216.6 Bn |

| CAGR (2025-2034) | 8.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | Ву Туре (Bioenergy, Bio sourced Chemicals, Bio sourced Materials), By Processing Method (Mechanical Processing, Chemical Processing, Biological Processing, Others), By Application (Energy And Transportation, Food, Beverages And Pharmaceuticals, Consumer Goods And Textiles and Packaging, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | NatureWorks, Dupont, BASF, Cargill, Novamont, Lenzing AG, Neste Oil Rotterdam, ADM, Infinita Renovables, Arkema, Braskem, Kingfa, Mitsubishi, Sofiproteol, Medors, Marseglia Group, Glencore, Louis Dreyfus, Renewable Energy Group, RBF Port Neches, Ag Processing, Elevance, Marathon Petroleum Corporation, Graanul Invest Group, Enviva, Pinnacle |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |