Global Beet Pulp Pellets Market Size, Share, And Industry Analysis Report By Product (Pressed, Wet, Dried, Ensiled), By Category (Molassed Pellets, Non-Molassed Pellets), By Animal Type (Dairy Cattle, Beef Cattle, Equine, Swine, Poultry), By Trade Flow (Direct Sales, Modern Trade, Specialty Store, Departmental Store, Convenience Store, Online Retailers), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178317

- Number of Pages: 331

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

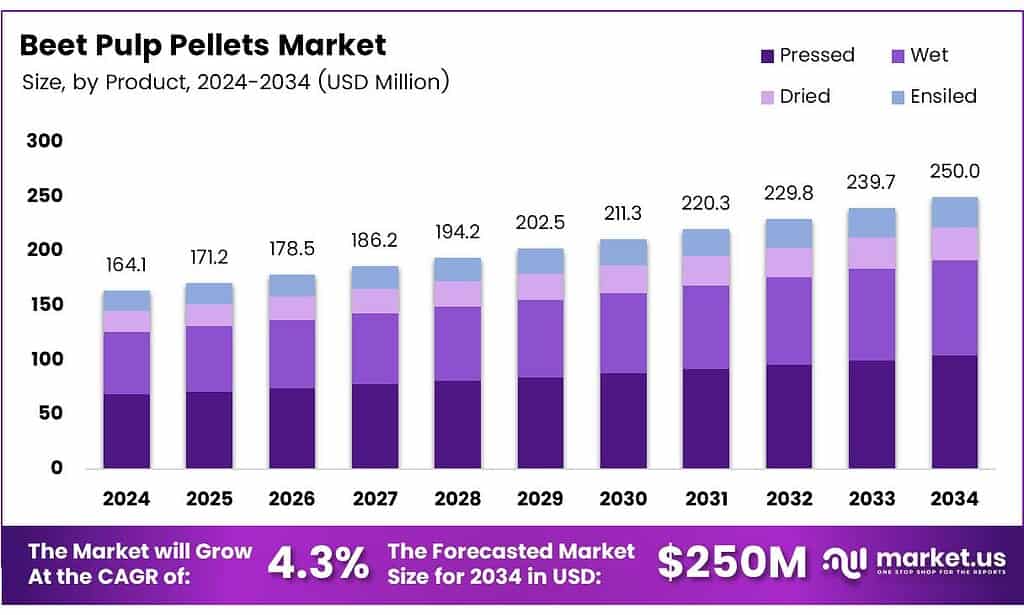

The Global Beet Pulp Pellets Market size is expected to be worth around USD 250.0 million by 2034 from USD 164.1 million in 2024, growing at a CAGR of 4.3% during the forecast period 2025 to 2034.

Beet pulp pellets are a co-product of the sugar beet processing industry. Manufacturers compress dried or pressed sugar beet pulp into dense pellets. These pellets serve as a high-fiber, low-starch feed ingredient for dairy cattle, beef cattle, horses, and other livestock. Their digestibility and palatability make them a preferred choice in commercial feed formulations.

The market occupies a meaningful position within the broader animal nutrition industry. Feed manufacturers, dairy farms, and equine operations consistently demand this ingredient for its rumen-health benefits. Moreover, the product’s compatibility with both conventional and specialty livestock diets expands its commercial applicability across multiple animal categories.

- The Südzucker Group reported consolidated revenues of €9,694 million in FY2024/25, reflecting the scale of beet processing operations that generate beet pulp as a key co-product. This production volume directly supports consistent pellet supply availability across global markets.

- Nordzucker recorded sales revenues of €2.770 billion in FY2024/25, reinforcing the significant role European sugar producers play in co-product supply chains. These financial benchmarks highlight the commercial scale behind beet pulp pellet production and its growing relevance to global animal feed markets.

Government policies across Europe and North America support sustainable agri-food processing. Regulatory frameworks encourage the utilization of co-products from sugar manufacturing, reducing waste and improving resource efficiency. Consequently, beet pulp pellet production benefits directly from policy incentives tied to circular agriculture and feed safety standards.

Investment in sugar beet crushing infrastructure continues to grow across key production regions. European sugar processors are expanding processing capacity to ensure a steady supply of raw beet pulp for pellet manufacturing. Additionally, North American producers are upgrading drying and pelletizing facilities to meet rising domestic and export demand.

Key Takeaways

- The Global Beet Pulp Pellets Market is valued at USD 164.1 million in 2024, to reach USD 250.0 million by 2034, growing at a CAGR of 4.3%.

- The Pressed pellets dominate with a 38.4% market share in 2025.

- The Molassed Pellets hold the largest share at 63.5% in 2025.

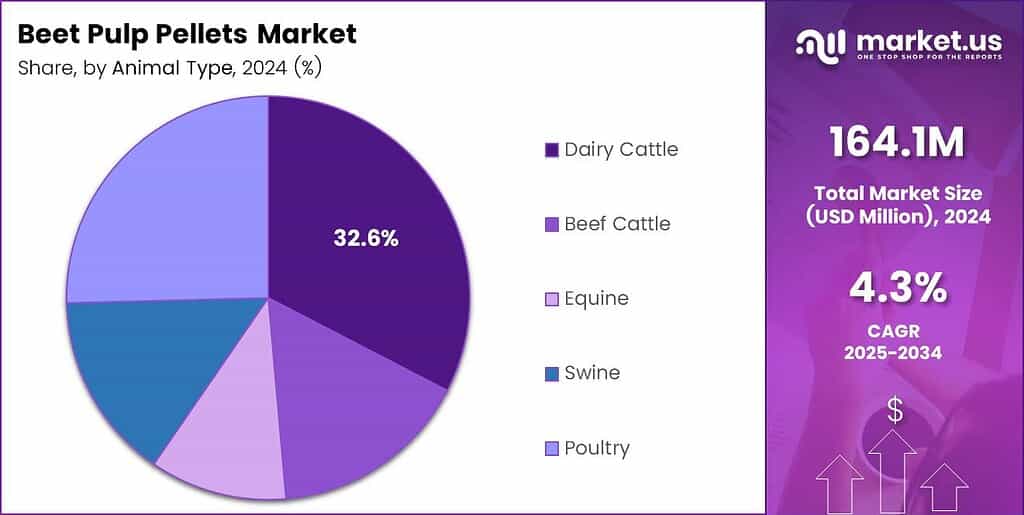

- The Dairy Cattle leads with a 32.6% share in 2025.

- Direct Sales dominates with a 43.7% share in 2025.

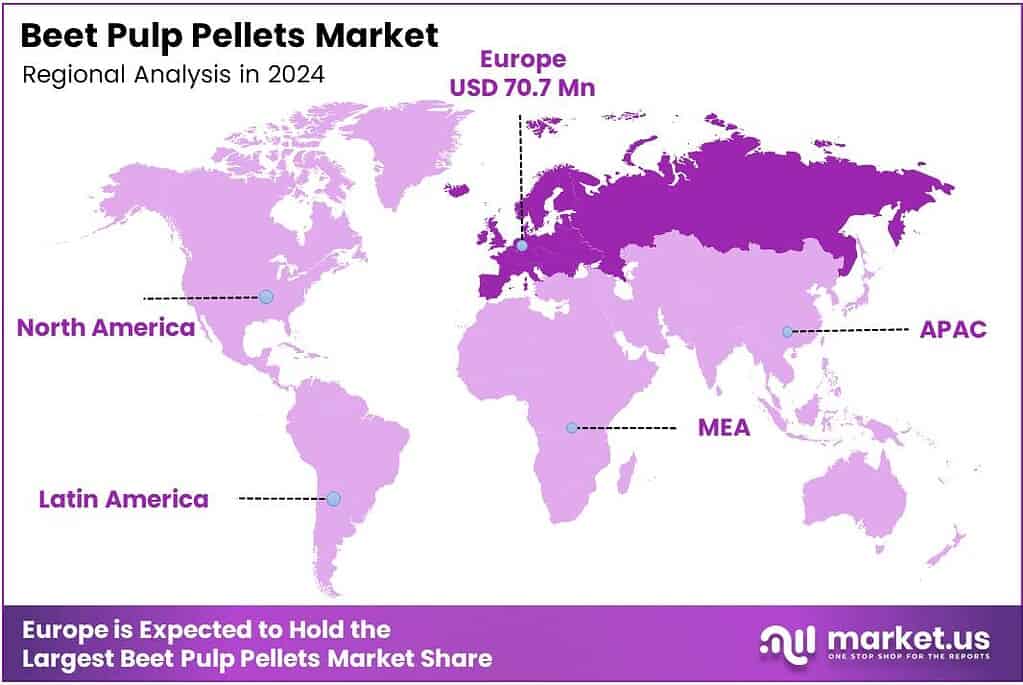

- Europe leads all regions with a 43.1% market share, valued at USD 70.7 million in 2025.

By Product Analysis

Pressed pellets dominate with 38.4% due to cost efficiency and wide livestock application.

In 2025, Pressed beet pulp pellets held a dominant market position in the by-product segment of the Beet Pulp Pellets Market, with a 38.4% share. Feed manufacturers prefer pressed pellets because they offer a cost-effective balance between moisture retention and nutritional density. Dairy and beef cattle operations widely adopt this format due to its handling and consistent fiber delivery.

Wet beet pulp represents a fresh-market alternative primarily used in proximity to sugar processing plants. Livestock producers in Europe favor wet pulp for immediate feeding due to its high palatability and low processing cost. However, short shelf life limits its transport radius and broader commercial use beyond local farm networks.

Dried beet pulp pellets command strong demand in export-oriented supply chains. Processors dry pulp to reduce moisture and extend shelf life, enabling long-distance transport across international markets. Additionally, dried pellets integrate seamlessly into compound feed formulations, supporting their consistent adoption by large-scale commercial feed manufacturers globally.

Ensiled beet pulp serves as a fermented feed option suited for high-throughput dairy operations. Farmers store ensiled pulp in bunker or bag silos for seasonal feeding programs. Consequently, this format supports winter feeding strategies in temperate climates where fresh forage availability declines significantly during colder months.

By Category Analysis

Molassed Pellets dominate with 63.5% due to high palatability and energy content.

In 2025, Molassed Pellets held a dominant market position in the By Category segment of the Beet Pulp Pellets Market, with a 63.5% share. Molasses addition enhances the palatability and energy value of beet pulp pellets significantly. Dairy cattle and equine operators prefer molassed variants because they encourage consistent intake and improve overall feed acceptance across animal categories.

Non-Molassed Pellets serve a distinct and growing segment of health-focused livestock feeding programs. Equine nutritionists and veterinarians recommend non-molassed options for horses requiring low-sugar, low-starch diets. Moreover, swine and specialty livestock producers adopt non-molassed pellets to manage metabolic health and maintain precise control over dietary carbohydrate levels.

By Animal Type Analysis

Dairy cattle dominate with 32.6% due to high-fiber rumen support requirements.

In 2025, Dairy Cattle held a dominant market position in the By Animal Type segment of the Beet Pulp Pellets Market, with a 32.6% share. High-producing dairy cows require digestible fiber sources to support rumen function and sustain milk yield. Feed nutritionists consistently include beet pulp pellets in total mixed rations to balance energy density and fiber content effectively.

Beef Cattle producers incorporate beet pulp pellets as an energy and fiber supplement in finishing and backgrounding diets. The pellets support weight gain while maintaining digestive health in feedlot environments. Additionally, their low dustiness and uniform size improve bunk management and reduce feed wastage in large-scale beef operations.

Equine nutritionists widely endorse beet pulp pellets as a forage extender and conditioning feed for horses. The low glycemic index and high digestible fiber content make these pellets especially suitable for performance horses and senior animals. Furthermore, veterinary endorsement of low-starch diets continues to drive adoption across competitive equestrian markets.

Swine and Poultry represent emerging and niche segments within the beet pulp pellets market. Swine producers use pellets to promote gut health and reduce digestive disturbances in intensive systems. Poultry applications remain limited but are expanding as researchers explore beet fiber’s role in improving intestinal microbiota and litter quality in broiler and layer operations.

By Trade Flow Analysis

Direct Sales dominate with 43.7% due to established processor-to-farm supply relationships.

In 2025, Direct Sales held a dominant market position in the By Trade Flow segment of the Beet Pulp Pellets Market, with a 43.7% share. Sugar processors and co-product manufacturers sell directly to large dairy farms, feed mills, and livestock operations through long-term supply agreements. This channel reduces intermediary costs and ensures product traceability from processing plant to farm gate.

Modern Trade and Specialty Store channels serve mid-sized and premium-focused livestock operations. Equine supply retailers and specialty feed stores stock branded beet pulp pellet products targeting performance horse owners and hobby farmers. These channels emphasize product quality, packaging, and nutritional labeling to attract health-conscious animal owners in suburban and peri-urban markets.

Departmental stores, Convenience Store, and Online Retailers are expanding as alternative distribution points for packaged beet pulp pellets. E-commerce platforms particularly benefit small-scale buyers seeking flexible order quantities and doorstep delivery. Consequently, digital retail is reshaping purchasing behavior among equine and companion animal owners seeking convenient access to specialty feed products.

Key Market Segments

By Product

- Pressed

- Wet

- Dried

- Ensiled

By Category

- Molassed Pellets

- Non-Molassed Pellets

By Animal Type

- Dairy Cattle

- Beef Cattle

- Equine

- Swine

- Poultry

By Trade Flow

- Direct Sales

- Modern Trade

- Specialty Store

- Departmental Store

- Convenience Store

- Online Retailers

Emerging Trends

Sustainability, Premiumization, and New Applications Shape the Beet Pulp Pellets Market

Beet pulp pellet producers are adopting biomethane and energy-efficient drying systems to reduce their carbon footprint. In 2025, Nordzucker Holding AG rolled out biogas from beet pulp at its Danish factories to power the sugar beet processing campaign. This circular energy model supports Scope 1 and 2 emission reductions and signals broader adoption across European processing sites.

Feed manufacturers are developing low-dust, uniform-coated pellet formats to improve barn air quality and handling efficiency. These upgraded product specifications reduce respiratory risks for both animals and farm workers. Moreover, premium pet food formulators are incorporating beet pulp pellets as a natural digestive fiber, expanding the product’s addressable market beyond traditional livestock categories.

The equine segment is growing rapidly, driven by veterinary endorsement of low-glycemic forage replacement diets. Horse owners and performance equine nutritionists increasingly favor beet pulp pellets over high-starch alternatives. Additionally, innovation in non-GMO, organic, and nutrient-enriched pellet variants is gaining traction among sustainable livestock operators seeking clean-label feed ingredients.

Drivers

Rising Livestock Nutrition Demand and Reliable Co-Product Supply Drive Beet Pulp Pellet Market Growth

Intensive dairy systems worldwide demand high-digestible fiber sources to sustain milk yield and support rumen health. Beet pulp pellets deliver a consistent fiber profile that dairy nutritionists rely on in total mixed ration formulations. Consequently, rising global dairy production volumes directly translate into sustained and growing demand for this co-product feed ingredient.

- Expanding sugar beet crushing capacities across Europe and North America ensure reliable pellet supply. Südzucker operates approximately 100 production locations in 31 countries, supporting a vast co-product output network. This scale of processing infrastructure guarantees consistent beet pulp availability, which underpins long-term supply security for feed manufacturers and livestock producers globally.

Climate-driven forage shortages are accelerating pellet adoption in drought-prone livestock regions. Farmers facing reduced hay and silage availability turn to beet pulp pellets as a reliable forage substitute. Moreover, the rising preference for low-starch, palatable pellets in equine conditioning diets further broadens the market’s demand base beyond primary ruminant applications.

Restraints

Supply Volatility and Competitive Fiber Alternatives Limit Beet Pulp Pellet Market Expansion

Intense competition from low-cost alternative fiber sources limits beet pulp pellet market penetration in key feed markets. Soy hulls and citrus pulp offer comparable digestible fiber content at competitive prices in North America and parts of Asia. Feed formulators readily substitute these alternatives when beet pulp prices rise, creating price sensitivity that constrains demand growth during supply-constrained periods.

- Heavy supply volatility stemming from sugar beet acreage fluctuations poses a significant challenge for the market. Farmers adjust beet cultivation based on global sweetener prices, directly affecting raw material availability for pellet production. The Südzucker Sugar segment recorded an operating result of €-13 million in FY2024/25, highlighting how segment-level stress can constrain co-product output volumes and pricing stability.

Logistics and storage requirements add operational complexity for both producers and buyers. Wet and pressed beet pulp formats require careful handling and rapid consumption to avoid spoilage. Therefore, smaller livestock operations in regions lacking adequate storage infrastructure often hesitate to commit to large-volume pellet procurement, limiting market penetration among fragmented buyer segments.

Growth Factors

Asia-Pacific Expansion, Export Contracts, and Specialty Feed Innovation Accelerate Market Growth

Rapid dairy herd expansion across Asia-Pacific is unlocking new high-volume demand channels for beet pulp pellets. Countries such as China and India are scaling commercial dairy operations to meet rising domestic milk consumption. Additionally, aquaculture pilots exploring beet fiber as a digestive supplement represent an emerging application that could materially expand the product’s addressable market across the region.

- Tereos reported other capital expenditure of €219 million in FY2024/25, up from €139 million in FY2023/24, reflecting higher discretionary investment in processing assets. This type of capacity investment by major sugar processors directly supports the expansion of beet pulp co-product output volumes needed to serve growing global feed demand across new trade corridors.

Development of specialized swine, poultry, and camel rations leveraging gut-health benefits opens new regional markets. The shift toward nutrient-enriched, non-GMO, and organic pellet variants supports premium positioning in sustainable livestock operations. The proliferation of multi-year export contracts and vertical integration strategies is widening the global trade footprint of beet pulp pellet suppliers across emerging economies.

Regional Analysis

Europe Dominates the Beet Pulp Pellets Market with a Market Share of 43.1%, Valued at USD 70.7 Million

Europe leads the global beet pulp pellets market with a 43.1% share, valued at USD 70.7 million in 2025. The region’s dominance reflects its massive sugar beet processing infrastructure spanning Germany, France, Belgium, and Poland. Major processors, including large-scale EU sugar groups, operate extensive crushing and pelletizing facilities that supply both domestic livestock operations and international export markets.

North America represents a significant and mature market for beet pulp pellets, supported by active sugar beet cultivation in states such as Michigan, Minnesota, and North Dakota. Feed mills and dairy cooperatives drive consistent domestic demand. Moreover, the region’s well-developed direct sales infrastructure enables efficient distribution from processors to large commercial livestock operations across the United States and Canada.

Asia Pacific is the fastest-growing regional market, driven by expanding dairy herds, rising feed imports, and growing awareness of high-fiber livestock nutrition. China and India lead demand growth as commercial dairy operations scale rapidly to meet protein consumption needs. Additionally, aquaculture and specialty livestock sectors are beginning to explore beet pulp pellets as a functional feed ingredient across the region.

The Middle East and Africa market is developing steadily, supported by growing import activity for livestock feed ingredients. Gulf Cooperation Council countries import substantial volumes of processed feed co-products to support intensive dairy and meat production in arid environments. Camel and dairy cattle feeding programs in the GCC represent niche but growing demand channels for beet pulp-based nutritional products.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Südzucker AG is the largest sugar producer in Europe and a primary global supplier of beet pulp co-products, including dried and pressed pellets. The group operates approximately 100 production locations across 31 countries. Its Sugar segment generated revenues of €3,876 million in FY2024/25, directly anchoring co-product availability for international feed markets despite a challenging year for sugar economics.

Nordzucker Holding AG is a major European sugar and co-product producer with operations across Scandinavia, Central Europe, and Australia. The group reported sales revenues of €2.770 billion in FY2024/25. In 2025, Nordzucker deployed biogas produced from its own beet pulp at Danish factories, marking a circular energy milestone that also highlights the strategic value of beet pulp in its operational sustainability agenda.

Tereos Group operates as a diversified agro-industrial cooperative with a strong presence in sugar beet and starch processing across Europe, Brazil, and Africa. Tereos reported adjusted EBITDA of €801 million in FY2024/25. The group’s multi-continent processing footprint supports consistent beet pulp pellet co-production and positions Tereos as a key supplier to both European livestock markets and international export channels.

AGRANA Beteiligungs-AG is a Central European processor of sugar, starch, and fruit products with active beet processing operations in Austria and Central Europe. AGRANA reported revenues of €3,514.0 million in FY2024/25. The company employs approximately 8,980 full-time employees across its operations, supporting significant beet-based co-product output that contributes to regional beet pulp pellet supply across European feed markets.

Top Key Players in the Market

- Sūdzucker AG

- Nordzucker Holding AG

- Tereos Group

- Michigan Sugar Beet Growers Inc.

- AGRANA Beteiligungs-AG

- Pfeifer & Langen GmbH & Co. KG

- Sucden Group

- Western Sugar Cooperative

- Midwest Agri-Commodities

- LaBudde Group, Inc.

Recent Developments

- In 2025, High-performance natural fiber refined from sugar beet pulp (a traditional animal feed or energy byproduct) via a patented, chemical-free process. It serves as a wood-fiber alternative (up to 40% replacement in kraft paper, cartonboard, and containerboard) while improving stability.

- In 2025, Nordzucker Holding AG’s Danish factories now use biogas produced from their own beet pulp for energy in the 2025/2026 sugar beet processing campaign (first-time rollout). Investigating expansion to other European sites. This supports Scope 1+2 emission reductions and circular use of pulp (previously mainly feed).

Report Scope

Report Features Description Market Value (2024) USD 164.1 Million Forecast Revenue (2034) USD 250.0 Million CAGR (2025-2034) 4.3% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Pressed, Wet, Dried, Ensiled), By Category (Molassed Pellets, Non-Molassed Pellets), By Animal Type (Dairy Cattle, Beef Cattle, Equine, Swine, Poultry), By Trade Flow (Direct Sales, Modern Trade, Specialty Store, Departmental Store, Convenience Store, Online Retailers) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Sūdzucker AG, Nordzucker Holding AG, Tereos Group, Michigan Sugar Beet Growers Inc., AGRANA Beteiligungs-AG, Pfeifer & Langen GmbH & Co. KG, Sucden Group, Western Sugar Cooperative, Midwest Agri-Commodities, LaBudde Group, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Beet Pulp Pellets MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Beet Pulp Pellets MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Sūdzucker AG

- Nordzucker Holding AG

- Tereos Group

- Michigan Sugar Beet Growers Inc.

- AGRANA Beteiligungs-AG

- Pfeifer & Langen GmbH & Co. KG

- Sucden Group

- Western Sugar Cooperative

- Midwest Agri-Commodities

- LaBudde Group, Inc.

Our Clients

- 178317

- February 2026