Quick Navigation

Report Overview

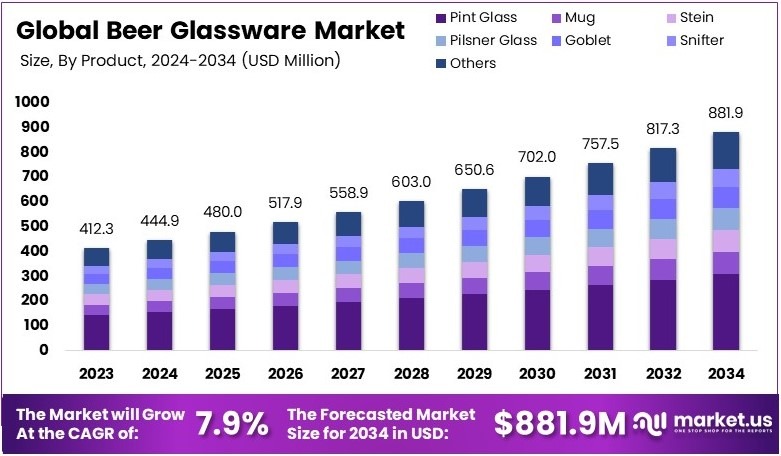

The Global Beer Glassware Market size is expected to be worth around USD 881.9 Million by 2034, from USD 412.3 Million in 2024, growing at a CAGR of 7.9% during the forecast period from 2025 to 2034.

Beer glassware refers to the various types of glasses used for drinking beer, such as pint glasses, steins, and tulips. These glasses are designed to enhance the beer-drinking experience by optimizing aroma, flavor, and carbonation. They vary in shape and size based on the type of beer.

The beer glassware market focuses on the production and distribution of beer glasses and related products. It includes the design, manufacturing, and sale of different types of beer glasses for both home use and commercial settings, driven by consumer preferences and the growing beer industry worldwide.

The beer glassware market is experiencing steady growth due to rising beer consumption and demand for premium drinkware. Glassware manufacturers are introducing a variety of specialized products to cater to this demand.

The key growth factors driving the beer glassware market include the growing popularity of craft beers, which require distinct glassware for optimal taste and presentation. The rising trend of beer culture is pushing consumers to seek personalized and high-quality glassware. Moreover, premium glassware not only enhances the drinking experience but also offers decorative appeal, contributing to demand in both commercial and residential settings.

Despite this growth, market saturation is occurring in some regions, particularly in developed countries where demand is stabilizing. Nevertheless, the market remains highly competitive, with established brands and new entrants vying for market share. Companies are differentiating themselves by offering innovative designs, eco-friendly options, and functional glassware for specific beer types, such as pilsners, stouts, and IPAs.

On a broader scale, the beer glassware market contributes to the overall beer industry by enhancing the consumer experience. Additionally, locally, it provides opportunities for businesses such as restaurants, bars, and breweries to differentiate themselves through high-quality glassware. Beer glassware also plays a significant role in marketing, with branded glassware being a popular promotional item.

Key Takeaways

- The Beer Glassware Market was valued at USD 412.3 Million in 2024, and is expected to reach USD 881.9 Million by 2034, with a CAGR of 7.9%.

- In 2024, Pint Glass dominated the product type segment with 35.2%, widely favored for its standard use across pubs and breweries.

- In 2024, Glass led the material segment with 55.5%, due to its transparency and aesthetic appeal for serving beer.

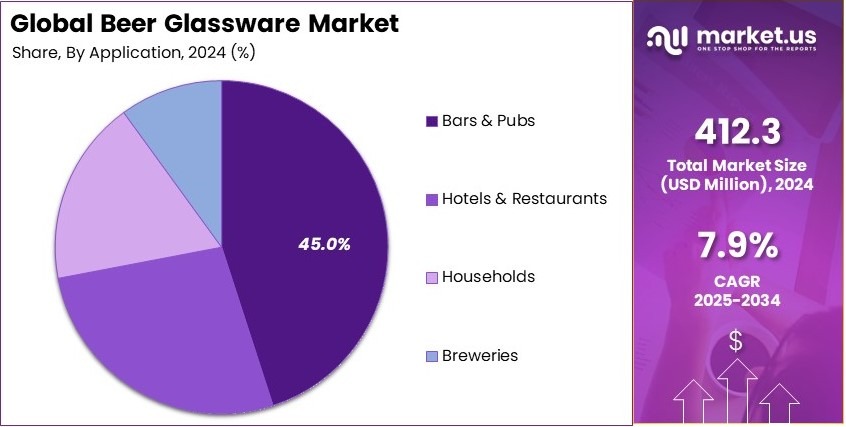

- In 2024, Bars & Pubs held the largest share in application with 45.0%, owing to high consumption volume and varied glassware usage.

- In 2024, Offline Sales dominated the distribution channel with 60.2%, supported by institutional bulk procurement from restaurants and pubs.

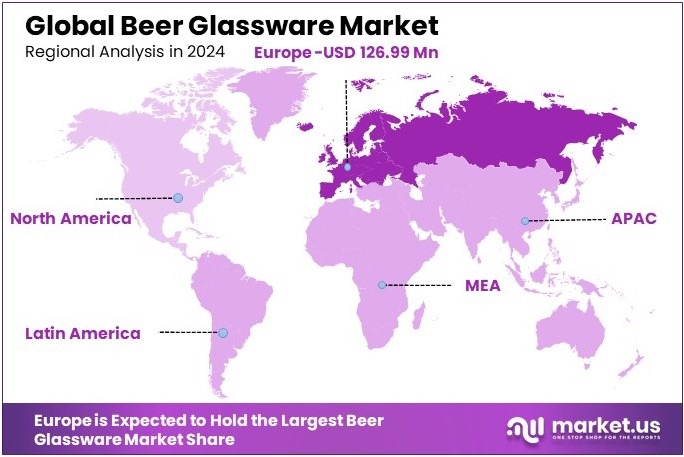

- In 2024, Europe led the market with 30.8% share, valued at USD 126.99 Million, attributed to traditional beer culture and tourism.

Product Type Analysis

Pint Glass dominates with 35.2% due to its popularity in bars and restaurants.

The beer glassware market is divided into several product types, including pint glasses, mugs, steins, pilsner glasses, goblets, snifters, tulip glasses, weizen glasses, and others. Among these, the pint glass holds the largest market share, accounting for 35.2%. This dominance is driven by the wide use of pint glasses in bars, restaurants, and pubs, where they are the standard glassware for serving beer.

Their versatile design makes them suitable for a wide range of beer types, from lagers to ales, making them a favorite among consumers. As an example, pint glasses are often used in popular chains like The BrewDog, where customers enjoy their beers in this universally accepted style.

Other types of glassware, such as mugs and steins, also play significant roles. Mugs are often preferred for their traditional appeal, especially in casual or home settings, while steins are popular in regions with a strong beer culture, like Germany.

These types of glasses are generally used in more specific contexts or cultural settings, contributing to a smaller share of the market. Glassware such as pilsner glasses and goblets are typically used for specialty beers, catering to a niche but important segment. These glasses are valued for their ability to enhance the aroma and flavor of particular beer styles.

Material Analysis

Glass dominates with 55.5% due to cost-effectiveness and traditional appeal.

The material segment of the beer glassware market includes glass, crystal, plastic, stainless steel, and others. Glass is the dominant material, holding a share of 55.5%. This is primarily because of its cost-effectiveness, wide availability, and traditional appeal.

Glass is the most commonly used material in beer glassware because it preserves the flavor and appearance of beer. It’s also easy to clean and maintain, making it a preferred choice for both consumers and businesses. For instance, bars and restaurants frequently use glass beer mugs and pint glasses because they are durable, cost-effective, and reliable for high-volume serving.

Crystal, while more expensive, is gaining popularity in premium beer glassware. Crystal glassware provides a higher level of clarity and a refined aesthetic, making it ideal for high-end establishments and collectors. Plastic beer glasses, on the other hand, are lightweight and durable, making them suitable for outdoor settings or events.

However, plastic glasses are less common for high-quality beer, as they do not offer the same drinking experience as glass or crystal. Stainless steel glasses, though less common, are increasingly popular in certain segments, such as for outdoor or camping use, due to their durability and insulation properties.

Application Analysis

Bars & Pubs dominate with 45.0% due to high beer consumption.

In the application segment, bars and pubs dominate the market with a share of 45.0%. This is because these establishments serve large volumes of beer daily and require durable, functional, and appealing glassware.

Bars and pubs often use pint glasses, mugs, and steins, which can withstand high traffic and frequent use while maintaining the quality of the beer served. The ambiance of bars and pubs is also enhanced by the glassware, with some establishments investing in custom or branded glassware to create a unique customer experience.

Hotels and restaurants also contribute to the market, but they account for a smaller share compared to bars and pubs. The glassware in these settings is often more varied, as establishments may use specialty glassware such as pilsner glasses or goblets for certain beer styles. Households, while important, represent a smaller portion of the market.

Consumers purchasing beer glassware for home use tend to buy glassware for specific occasions or personal preferences. Breweries, although a smaller segment, play a key role in promoting certain glassware types, often using specific glasses to showcase their craft beers. Breweries tend to invest in high-quality, branded glassware to enhance their products’ presentation.

Distribution Channel Analysis

Offline sales dominate with 60.2% due to traditional purchasing habits.

The distribution channel segment includes online and offline sales. Offline sales dominate with 60.2% of the market share. This is largely due to the traditional way customers purchase beer glassware in physical stores.

Many consumers prefer to see and feel the products before purchasing, especially when it comes to choosing the right beer glass for specific occasions. Retail stores, such as department stores and specialty kitchenware shops, allow customers to inspect the quality and design of glassware, which is an important factor in their purchasing decision.

On the other hand, online sales are growing rapidly, driven by the convenience of e-commerce. Consumers can now browse a wide range of beer glassware styles and brands from the comfort of their homes. The growing trend of online shopping, particularly on platforms like Amazon and specialty sites, is contributing to the expansion of online sales.

For instance, many customers now purchase glassware sets for home use or as gifts online, appreciating the ease of having products delivered directly to their doorsteps. While offline sales are still dominant, online sales are expected to continue growing as more consumers seek convenience and variety in their purchases.

Key Market Segments

By Product Type

- Pint Glass

- Mug

- Stein

- Pilsner Glass

- Goblet

- Snifter

- Tulip

- Weizen Glass

- Others

By Material

- Glass

- Crystal

- Plastic

- Stainless Steel

- Others

By Application

- Bars & Pubs

- Hotels & Restaurants

- Households

- Breweries

By Distribution Channel

- Online

- Offline

Driving Factors

Craft Beer Culture Drives Market Growth

The rising consumption of craft beer has significantly boosted the demand for specialized beer glassware. Craft beer enthusiasts often seek glasses that enhance the unique flavors and aromas of their beverages. This trend has led to an increased preference for specific glass types, such as tulip glasses and IPA glasses, which are designed to improve the beer-drinking experience.

Along with this, there is growing awareness of how the shape of a glass affects the aroma and taste of beer. This knowledge has driven consumers to invest in glasses that are specifically tailored to different beer styles.

Furthermore, the expansion of pubs, bars, and breweries, many of which offer branded glassware, is fueling the growth of this market. Branded glasses not only enhance the customer experience but also serve as a marketing tool, strengthening brand identity.

The rise in home bars and beer tasting events also contributes to the market’s growth. As more consumers host tasting events or create dedicated beer spaces at home, the demand for high-quality, specialized glassware increases. Together, these factors are driving the beer glassware market, as both commercial establishments and individual consumers recognize the value of using the right glass to improve their beer experience.

Restraining Factors

Fragility and Preference for Cans Restrain Market Growth

Several factors are restraining the growth of the beer glassware market. First, the risk of breakage and short product lifespan in commercial environments is a major concern. Glassware used in bars and restaurants is at high risk of damage, leading to frequent replacements and added costs. This makes some businesses hesitant to invest in premium glassware.

Additionally, many consumers still prefer cans and bottles for casual and outdoor beer consumption. The convenience and portability of cans and bottles often outweigh the desire for glassware, especially in settings like picnics or tailgate parties.

High inventory and shipping costs are also challenges in the beer glassware market. Due to the fragility of glass, shipping costs are higher, and businesses may hesitate to stock large quantities of glassware due to storage and handling concerns.

Regulatory limitations on alcohol branding in some countries further limit the ability of manufacturers to design unique glassware for promotional purposes. These factors create barriers for companies in expanding their product reach, as the risks and costs associated with glassware are a deterrent for both businesses and consumers.

Growth Opportunities

Innovation and Collectibles Provide Opportunities

The beer glassware market offers several opportunities for growth, driven by product innovation and consumer demand for unique items. The launch of glassware collections co-branded with craft breweries presents a significant opportunity. As breweries continue to grow in popularity, offering custom-designed glassware can enhance brand identity while meeting consumer demand for collectible items.

Furthermore, there is rising interest in beer glass sets that serve as collectibles or gifts. These sets often appeal to consumers who view glassware as a way to celebrate their passion for beer, making them a lucrative product segment.

Additionally, the development of dishwasher-safe and shatter-resistant glass materials offers an opportunity for market players to create more durable and user-friendly products. Consumers are increasingly looking for glassware that can withstand frequent use and cleaning without breaking.

The use of laser-etched nucleation points in glasses is another opportunity. This feature enhances carbonation effects, making the beer experience even more enjoyable. By focusing on innovation, convenience, and collectibility, companies can tap into growing consumer preferences, creating new products that cater to the evolving demands of the market.

Emerging Trends

Specialized Glassware and Design Trends Are Latest Trending Factors

In recent years, the demand for specialized beer glasses has grown significantly, with specific types of glasses such as tulip, pilsner, and IPA glasses becoming increasingly popular. These glasses are designed to enhance the flavor profile of specific beer types, making them a preferred choice for craft beer enthusiasts.

Along with this, there is a rise in artisanal and hand-blown beer glass designs. Consumers are seeking unique, one-of-a-kind glasses that reflect their personal taste and appreciation for craftsmanship. Etched or frosted glass is also gaining popularity for its aesthetic appeal. These designs not only look attractive but also provide functional benefits, such as better grip and improved beer presentation.

Additionally, there is a growing consumer preference for stackable and space-saving glassware. With more people setting up home bars or limited kitchen space, stackable glasses offer a practical solution while maintaining style. These trends show that beer glassware is no longer just a functional item but a way for consumers to express their style and enhance their drinking experience.

Regional Analysis

Europe Dominates with 30.8% Market Share

Europe holds a dominant 30.8% share and valuation of USD 126.99 Millionin the beer glassware market. This significant market presence is fueled by the region’s rich beer culture, strong tradition of brewing, and a high demand for both premium and functional glassware. Countries like Germany, Belgium, and the UK are at the forefront, contributing to Europe’s leadership in the global beer glassware industry.

Europe’s dominance in the beer glassware market is driven by its long history of beer brewing and consumption. The region has a high number of breweries, pubs, and restaurants, all of which demand high-quality glassware. Additionally, Europeans often prefer specialized glassware to enhance the drinking experience, such as Pilsner glasses, steins, and goblets, which are tailored to specific beer types. The region’s focus on premium beer experiences drives the demand for unique and decorative glassware.

Europe’s market dynamics are influenced by cultural factors and local preferences. Countries like Germany and Belgium, known for their beer heritage, drive the demand for specialized beer glassware in both the residential and commercial sectors. Furthermore, strict quality regulations and consumer preferences for high-end, durable glassware have boosted the sales of premium beer glasses. In contrast, in the UK, the use of pint glasses is widespread, contributing to their significant market share in Europe.

Regional Mentions:

- North America: North America holds a significant share in the beer glassware market, driven by the popularity of craft beer. The U.S. and Canada are seeing a rise in beer glass demand, with a focus on innovation and unique designs.

- Asia Pacific: The beer glassware market in Asia Pacific is expanding rapidly, especially in countries like Japan and China, where beer culture is growing. The demand for glassware is increasing as beer consumption rises in urban areas.

- Middle East & Africa: In the Middle East and Africa, the beer glassware market is still emerging. With a growing number of breweries and increasing beer consumption, demand for glassware is expected to rise in the coming years.

- Latin America: Latin America’s beer glassware market is growing steadily, driven by increasing beer consumption and the rise of craft breweries, particularly in countries like Brazil and Mexico. The demand for quality glassware is increasing as beer culture expands.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The Beer Glassware Market is highly competitive, with leading players such as Libbey Inc., Arc International, Rastal GmbH & Co. KG, and Fiskars Group at the forefront of the industry. These companies have established themselves as top producers of glassware for breweries, restaurants, and households, each offering a variety of innovative and high-quality products.

Libbey Inc. stands out as one of the largest and most well-known companies in the beer glassware market. With a long history in the glassware industry, Libbey offers a wide range of beer glasses, including pint glasses, steins, and goblets. The company is recognized for its strong brand reputation, product durability, and innovative designs, making it a preferred choice for both commercial and residential customers.

Arc International is another leading player in the market, known for its high-quality glassware and commitment to design excellence. The company’s beer glass collection includes a variety of options tailored to different types of beer. Arc International is particularly known for its focus on creating elegant and functional glassware that enhances the drinking experience, contributing to its strong presence in the global market.

Rastal GmbH & Co. KG specializes in premium beer glassware, offering sophisticated designs that cater to craft breweries and high-end establishments. The company’s glasses are widely used by beer connoisseurs and professional brewers alike. Rastal’s commitment to quality and unique glass designs helps it maintain a solid foothold in the competitive beer glassware market.

Fiskars Group, with its expertise in household products, plays a key role in the beer glassware sector. The company’s strong distribution network and diverse product offerings, which include functional and aesthetically pleasing beer glasses, have made it a trusted name in the market. Fiskars’ focus on quality and design continues to drive its growth and market share in the industry.

These four companies are integral to the success and growth of the beer glassware market, leading through innovation, quality, and strong brand presence.

Major Companies in the Market

- Libbey Inc.

- Arc International

- Rastal GmbH & Co. KG

- Fiskars Group

- Eagle Glass Deco

- Lifetime Brands

- Ngwenya Glass

- Ocean Glass

- Borosil

- Anchor Hocking LLC

Recent Developments

- Ardagh Glass Packaging: On January 2025, Ardagh Glass Packaging-North America (AGP-North America), a division of Ardagh Group, expanded its 12oz Heritage glass beer bottle portfolio by introducing two new bottles: flint (clear) glass with a pry-off closure and amber (brown) glass with a twist-off closure. These additions offer craft brewers enhanced design flexibility and branding opportunities.

- England Football Fans: On June 2024, during Euro 2024 in Cologne, England football fans expressed surprise and bemusement over the traditional 200ml Kölsch beer glasses, likening them to “Champagne flutes.” The smaller serving size led to fans having to order more rounds to match their usual drinking habits. Kölsch, a beer style exclusive to Cologne, is traditionally served in these slender glasses to maintain freshness.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 412.3 Million |

| Forecast Revenue (2034) | USD 881.9 Million |

| CAGR (2025-2034) | 7.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Pint Glass, Mug, Stein, Pilsner Glass, Goblet, Snifter, Tulip, Weizen Glass, Others), By Material (Glass, Crystal, Plastic, Stainless Steel, Others), By Application (Bars & Pubs, Hotels & Restaurants, Households, Breweries), By Distribution Channel (Online, Offline) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Libbey Inc., Arc International, Rastal GmbH & Co. KG, Fiskars Group, Eagle Glass Deco, Lifetime Brands, Ngwenya Glass, Ocean Glass, Borosil, Anchor Hocking LLC, Corelle Brands, LLC, Oneida Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |