Quick Navigation

Report Overview

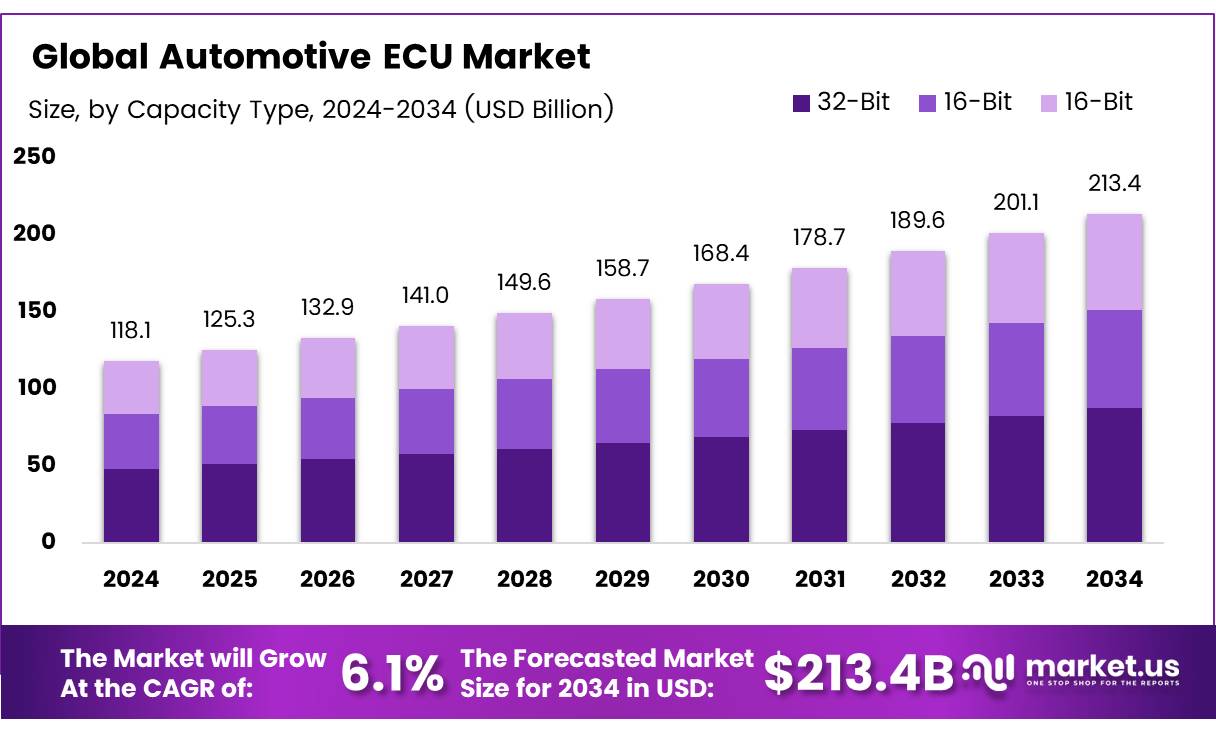

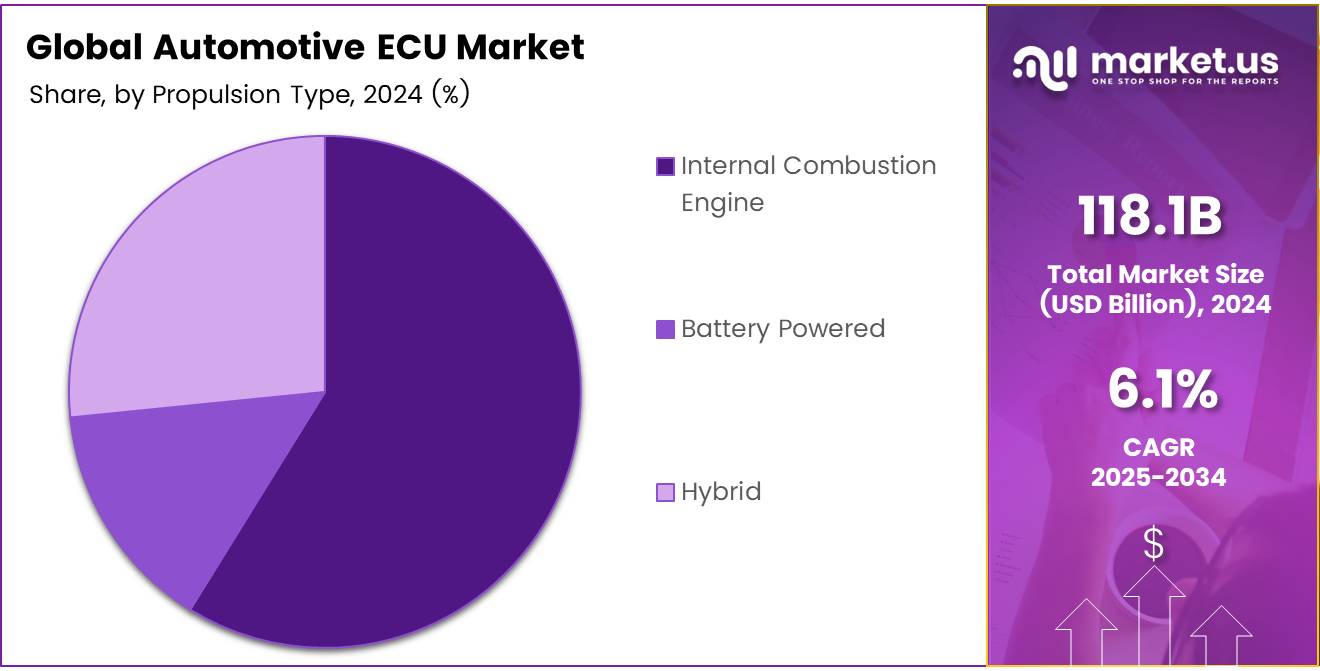

The Global Automotive ECU Market size is expected to be worth around USD 213.4 Billion by 2034, from USD 118.1 Billion in 2024, growing at a CAGR of 6.1% during the forecast period from 2025 to 2034.

An Automotive ECU (Electronic Control Unit) refers to a microprocessor-based embedded system that controls a specific function or set of functions in a vehicle. These units manage essential automotive functions like engine control, power steering, safety systems (e.g., airbags), braking systems (ABS), infotainment systems, and more. ECUs are integral to modern vehicles, making them smarter, more efficient, and safer.

The Automotive ECU Market is a rapidly growing segment within the automotive industry, driven by the continuous evolution of car technologies. The market is primarily fueled by the shift towards electric vehicles (EVs), autonomous driving, and advanced driver-assistance systems (ADAS), which require increasingly sophisticated ECUs. As more vehicles become connected, the demand for ECUs, particularly those focused on infotainment, telematics, and safety features, continues to rise.

According to Statistics, the United States was the second-largest importer of automotive products, with a value of approximately 327 billion USD in 2022. This reflects the robust demand for advanced automotive components, including ECUs, in key global markets.

The growth in this sector is further supported by the increasing semiconductor content in vehicles, as modern cars in the U.S. typically contain between 1,400 and 1,500 chips, with some advanced vehicles containing up to 3,000 chips, according to Applied Energy Systems.

The growth potential in the automotive ECU market remains strong, driven by the increasing reliance on electronic systems and the evolution of automotive technologies. The shift towards electric vehicles (EVs) and autonomous driving technologies is accelerating the demand for highly sophisticated ECUs.

As vehicles become more connected, the need for secure, reliable, and advanced ECUs to manage everything from infotainment to critical safety systems is essential. Moreover, there is an increasing demand for high-performance ECUs that can handle the complex data processing required for autonomous driving systems, energy-efficient vehicles, and connected vehicle features.

The opportunity for market players lies in the development of innovative ECUs that cater to these growing demands, particularly in areas like advanced driver assistance systems (ADAS), electric powertrains, and vehicle-to-everything (V2X) communication systems.

As the automotive industry moves towards greater automation and digitalization, the need for highly integrated and scalable ECUs will only increase. This trend offers a significant opportunity for manufacturers to lead the way in the production of specialized chips, processors, and controllers for various vehicle applications.

Governments around the world are heavily investing in the automotive sector, with a specific focus on electric vehicles, autonomous driving, and the development of safer, more environmentally friendly transportation. Various regulatory frameworks are also being introduced to support the transition to cleaner, safer, and more efficient vehicles, which indirectly benefits the automotive ECU market.

For instance, the European Union’s Green Deal and initiatives like the U.S. EV tax credit and infrastructure investments are encouraging automakers to adopt advanced ECUs for their vehicles. Additionally, stricter safety regulations and emissions standards are driving the adoption of more sophisticated ECUs to ensure compliance.

Key Takeaways

- The global Automotive ECU market is projected to reach USD 213.4 billion by 2034, growing at a 6.1% CAGR.

- The 32-bit ECU segment led the market in 2024, capturing 41.5% share due to its performance and cost-effectiveness.

- Passenger Cars dominated the market by vehicle type, holding 64.2% of the total market share in 2024.

- Powertrain applications led the Automotive ECU market with a 27.6% share in 2024, focusing on engine performance and fuel efficiency.

- ICE vehicles accounted for 72.2% of the Automotive ECU market in 2024, reflecting the ongoing dominance of internal combustion engines.

Capacity Type Analysis

32-Bit Automotive ECUs Lead with 41.5% Share in 2024, Driven by Cost-Effectiveness and Established Industry Adoption

In 2024, the 32-bit segment dominated the Automotive ECU (Electronic Control Unit) market by capacity type, capturing a significant 41.5% share. This dominance can be attributed to the 32-bit architecture’s balanced performance, cost-effectiveness, and widespread adoption across the automotive industry.

These ECUs are widely used in mid-range to high-performance vehicles, providing adequate processing power for applications such as engine control, infotainment systems, and safety features without driving up costs.

The 16-bit segment, while holding a smaller portion of the market, remains essential for basic automotive applications. Its simplicity and low production cost make it suitable for entry-level and budget-conscious vehicles, though it is less capable of supporting advanced features seen in higher-end models.

On the other hand, the 64-bit segment is gaining traction, especially in the high-end automotive market, as it supports complex functions like autonomous driving and advanced infotainment systems. Despite this, the 64-bit segment accounted for a comparatively smaller share in 2024, due to its higher cost and more specialized use cases.

Vehicle Type Analysis

Passenger Cars Lead the Automotive ECU Market with 64.2% Share in 2024, Driven by Consumer Demand and Versatility

In 2024, the Passenger Cars segment held a dominant market position in the By Vehicle Type Analysis of the Automotive ECU market, accounting for 64.2% of the total market share. This dominance is primarily driven by the high demand for passenger vehicles worldwide, coupled with the increasing adoption of advanced automotive technologies.

Automotive ECUs in passenger cars are used to control a variety of systems, including engine management, safety features, and infotainment, making them critical to the overall performance and user experience. The growing trend towards electric and hybrid vehicles, which require more sophisticated ECUs, further supports the segment’s growth.

The Commercial Vehicle segment, while holding a smaller share of the market, continues to play a crucial role, driven by the increasing need for efficiency, safety, and connectivity in trucks, buses, and other heavy-duty vehicles.

The demand for automotive ECUs in this segment is growing due to the need for improved fleet management, autonomous driving capabilities, and regulatory compliance in areas such as emissions control. However, the Commercial Vehicle segment accounted for a smaller share in 2024, due to lower overall vehicle production compared to passenger cars.

Overall, Passenger Cars continue to lead the market, benefiting from higher production volumes and ongoing technological advancements.

Application Analysis

Powertrain Dominates Automotive ECU Market with 27.6% Share in 2024, Fueling Efficiency and Performance Advancements

In 2024, the Powertrain application segment held a dominant position in the Automotive ECU market with a 27.6% share. This segment’s leadership is driven by the critical role of ECUs in optimizing engine performance, fuel efficiency, and emissions control.

With increasing consumer demand for fuel-efficient and environmentally-friendly vehicles, the importance of Powertrain ECUs has grown, particularly in electric and hybrid vehicle segments, which require sophisticated power management systems. The need for more precise control over engine operations and transmission systems also bolsters the growth of this segment.

The ADAS (Advanced Driver Assistance Systems) & Safety System segment follows closely, driven by the growing emphasis on safety and semi-autonomous driving technologies. As automakers implement features such as lane-keeping assist, collision avoidance, and adaptive cruise control, the demand for ECUs in ADAS and safety applications continues to rise. This segment is experiencing rapid growth, but still holds a smaller share compared to Powertrain.

Body Electronics, Infotainment, and Other application segments also contribute to the overall market, but with comparatively smaller shares. Body Electronics systems, such as lighting and climate control, and Infotainment systems are seeing steady adoption, driven by consumer demand for enhanced convenience and connectivity.

Propulsion Type Analysis

Internal Combustion Engine Leads the Automotive ECU Market with 72.2% Share in 2024, Driven by Legacy Adoption and Performance Needs

In 2024, the Internal Combustion Engine (ICE) propulsion type held a dominant position in the By Propulsion Type Analysis segment of the Automotive ECU market, accounting for 72.2% of the total market share. This dominance is primarily attributed to the continued widespread adoption of ICE vehicles globally, particularly in regions where electric vehicle (EV) infrastructure is still developing.

ICE vehicles remain the most common choice due to their proven performance, extensive fueling infrastructure, and lower upfront costs compared to electric and hybrid alternatives. The use of ECUs in ICE vehicles is critical for controlling engine functions, optimizing fuel efficiency, managing emissions, and enhancing overall performance, which sustains their market share.

The Battery-Powered segment, while holding a much smaller portion of the market, is growing steadily as electric vehicle adoption increases due to the rising demand for sustainable transportation solutions. EVs require specialized ECUs to manage power distribution, battery management systems, and charging processes, which is propelling the growth of this segment.

The Hybrid segment, combining elements of both ICE and electric propulsion, also contributes to market growth. While hybrids offer improved fuel efficiency and lower emissions compared to traditional ICE vehicles, they still account for a smaller share due to their higher cost and complex powertrain systems.

Despite the growth of electric and hybrid vehicles, ICE continues to dominate the automotive landscape, driven by legacy infrastructure and consumer familiarity.

Key Market Segments

By Capacity Type

- 32-Bit

- 16-Bit

- 64-Bit

By Vehicle Type

- Passenger Cars

- Commercial Vehicle

By Application

- Powertrain

- ADAS & Safety System

- Body Electronics

- Infotainment

- Others

By Propulsion Type

- Internal Combustion Engine

- Battery Powered

- Hybrid

Drivers

Rising Demand for Advanced Vehicle Features Fuels Automotive ECU Market Growth

The automotive ECU (Electronic Control Unit) market is experiencing significant growth, driven by the increasing demand for advanced vehicle features that improve safety, efficiency, and overall driving experience. Consumers are seeking vehicles with cutting-edge technologies such as autonomous driving capabilities, advanced infotainment systems, and improved driver-assistance features, all of which rely heavily on sophisticated ECUs.

Additionally, the rise in electric vehicle (EV) adoption is accelerating the need for specialized ECUs to manage complex systems like batteries, electric motors, and overall vehicle performance. As electric vehicles continue to replace traditional combustion engine models, automakers are relying more on advanced control units to optimize energy management and extend battery life. Furthermore, stringent global regulations regarding emissions and safety are pushing automakers to adopt more advanced ECU solutions.

Governments are implementing tighter emission standards and safety protocols, necessitating the development of ECUs that can better monitor and control engine performance, emissions, and safety features. These factors combined are accelerating the growth of the automotive ECU market, as manufacturers race to meet evolving consumer expectations and regulatory requirements.

Restraints

High Costs and Cybersecurity Risks Limit Automotive ECU Market Expansion

While the automotive ECU market is growing, several restraints are hindering its full potential. One of the primary challenges is the high cost of advanced ECU systems. As vehicles become more technologically sophisticated, ECUs must manage increasingly complex functions, from autonomous driving features to energy management in electric vehicles. This complexity often drives up the cost of ECUs, making vehicles more expensive for consumers.

For automakers, incorporating high-end ECUs into mass-produced vehicles may not always be financially viable, especially when targeting cost-sensitive markets. Additionally, as vehicles become more connected, the risk of cyberattacks on ECUs has become a growing concern. Modern vehicles rely on multiple ECUs working together, often with internet connectivity, creating vulnerabilities that hackers could exploit.

If a cyberattack targets an ECU, it could affect critical vehicle functions such as braking, steering, or engine control, posing serious safety risks. This increases the need for more robust cybersecurity measures, which further raises the overall cost of developing and implementing secure ECUs.

Both the high cost and the cybersecurity challenges are holding back market growth, as automakers must balance the demand for advanced features with the need to maintain vehicle affordability and safety. Overcoming these restraints will be essential for the future expansion of the automotive ECU market.

Growth Factors

Connected Car Technologies and Emerging Markets Open New Growth Avenues for Automotive ECUs

The automotive ECU market has exciting growth opportunities, driven by developments in connected car technologies, innovations in AI, and the expansion of vehicle sales in emerging markets. The rise of connected car ecosystems is creating numerous opportunities for advanced ECUs.

These vehicles rely on sophisticated control units to manage communication between various in-vehicle systems and external networks, allowing for features like real-time traffic updates, remote diagnostics, and over-the-air software updates. This growing demand for connectivity enhances the role of ECUs in modern vehicles, offering significant market potential.

Another promising area is the integration of artificial intelligence (AI) into automotive systems. AI can be used for predictive maintenance, improving vehicle management, and enhancing driver assistance features like collision avoidance and traffic prediction.

By incorporating AI into ECUs, automakers can deliver smarter, more efficient vehicles, further expanding the scope of ECU applications. Furthermore, as vehicle sales grow in developing regions, there is a significant opportunity for the automotive ECU market to penetrate these emerging markets.

Rising disposable incomes, increased urbanization, and a growing middle class in regions like Asia-Pacific, Latin America, and Africa are driving demand for vehicles, which in turn boosts the need for ECUs.

As automakers look to meet the needs of these expanding markets, they will increasingly rely on advanced ECUs to deliver competitive, feature-rich, and cost-effective vehicles. These growth opportunities—driven by connectivity, AI, and expanding markets—are shaping the future of the automotive ECU industry.

Emerging Trends

Wireless Connectivity and Smart Features Drive Automotive ECU Market Trends

The automotive ECU market is witnessing several important trends, largely driven by advancements in wireless connectivity, machine learning, and energy-efficient designs. One of the key trends is the increasing use of the Internet of Things (IoT) devices in vehicles, which is boosting the demand for ECUs capable of managing complex, wireless connections. IoT integration enables features like remote vehicle diagnostics, smart navigation, and real-time data sharing, all of which require advanced ECUs to function seamlessly.

Another significant trend is the incorporation of machine learning (ML) into automotive ECUs. By leveraging ML algorithms, ECUs can analyze large volumes of data from sensors and cameras to improve vehicle diagnostics, predict maintenance needs, and enhance operational efficiency. This ability to learn” from data allows for more responsive and intelligent vehicle systems, making the driving experience safer and more efficient. Additionally, there is a growing push toward lightweight and energy-efficient ECU designs.

Automakers are focusing on developing smaller, more compact ECUs that consume less power, helping to reduce overall vehicle weight and improve fuel efficiency—especially in electric vehicles. This trend aligns with the broader automotive industry’s focus on sustainability and eco-friendliness. Together, these trends—IoT integration, machine learning, and energy-efficient designs—are reshaping the automotive ECU market, driving demand for more advanced, smarter, and eco-friendly solutions in modern vehicles.”

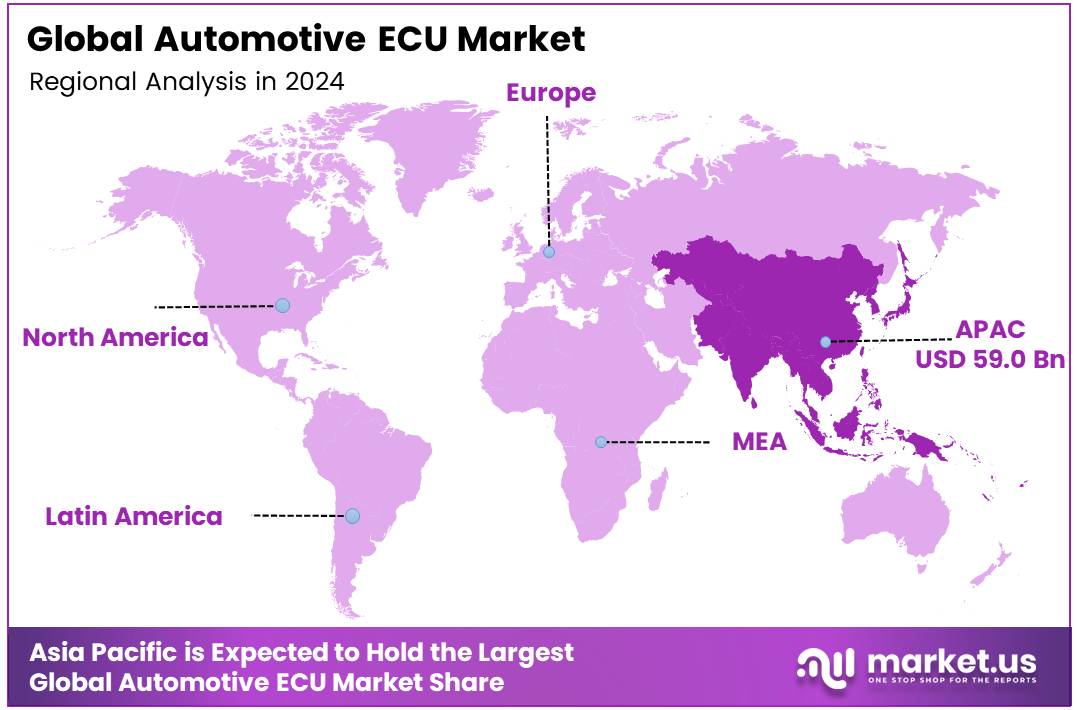

Regional Analysis

Asia Pacific leads the Automotive ECU market with a 50.3% share valued at USD 59 Billion

The Asia Pacific region dominates the global Automotive ECU market, holding a substantial market share of 50.3%, valued at USD 59 Billion. The region is anticipated to continue its leadership due to the robust automotive manufacturing sectors in countries like China, Japan, South Korea, and India.

The significant production of vehicles, including electric vehicles (EVs) and autonomous vehicles (AVs), in this region contributes to the growing demand for ECUs. Furthermore, the rapid adoption of advanced driver assistance systems (ADAS) and increasing consumer preferences for in-vehicle technologies such as infotainment, navigation, and connectivity are driving ECU integration in vehicles.

Regional Mentions:

North America holds the second-largest market share, attributed primarily to the United States and Canada, with a growing emphasis on vehicle safety technologies, emission regulations, and a high penetration of electric vehicles. The market in North America is expected to grow steadily at a CAGR of around 5.8% during the forecast period, driven by technological advancements and strong investment in automotive R&D.

Europe, another key market, accounts for a significant portion of the global ECU market. Germany, France, and Italy are major contributors, driven by the strong presence of luxury car manufacturers such as Mercedes-Benz, BMW, and Audi. The push for automotive electrification, along with stringent environmental regulations, is spurring demand for advanced ECUs capable of managing complex powertrains in electric and hybrid vehicles. Europe’s market is also growing due to ongoing advancements in autonomous driving technology and vehicle connectivity.

The Middle East & Africa is witnessing a relatively slow but steady growth in the Automotive ECU market, driven by increasing vehicle sales and government initiatives focused on smart city infrastructure and transportation. The presence of major automotive manufacturers and a growing appetite for premium vehicles in countries like the UAE and Saudi Arabia are key drivers.

Latin America exhibits moderate growth, with Brazil and Mexico being the primary markets. However, challenges like economic volatility and limited automotive production capabilities have tempered faster market expansion.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global Automotive ECU (Electronic Control Unit) market continues to be highly competitive, with a mix of established players and innovative newcomers driving growth and technological advancements.

Autoliv Inc. remains a leader in automotive safety systems, expanding its footprint in ECU production by focusing on airbag control units and advanced driver assistance systems (ADAS). Their strong R&D pipeline and strategic partnerships with automakers enable them to capitalize on the increasing demand for safety features in autonomous vehicles.

BorgWarner Inc. stands out due to its strong position in the electric vehicle (EV) powertrain sector. The company’s push toward electrification has positioned its ECUs as essential for the evolving needs of EVs, particularly in battery management systems and power electronics.

Panasonic Holdings Corporation and Robert Bosch GmbH continue to dominate with a wide range of ECU products, from infotainment systems to powertrain control units. Their investment in AI and connected car technologies ensures they remain at the forefront of innovation in vehicle control systems.

Valeo S.A. and Continental AG lead in providing ECUs for ADAS, autonomous driving, and electric vehicle solutions. Valeo’s integration of thermal management and sensor technologies is poised to strengthen its market position as vehicle electrification accelerates.

Denso Corporation, with its strong presence in automotive HVAC, engine control, and safety systems, remains a key player, while Hella KGaA Hueck & Co. continues to thrive through its lighting and electronic control solutions.

Hitachi Astemo Americas, Inc. and ZF Friedrichshafen AG round out the market with a focus on hybrid and electric vehicle control solutions, ensuring they meet the growing demand for sustainable automotive technologies.

These players are expected to enhance their market share by expanding product portfolios and investing in next-gen vehicle technologies, such as AI-driven ECUs, 5G connectivity, and more autonomous driving capabilities.

Top Key Players in the Market

- Autoliv Inc.

- BorgWarner Inc.

- Panasonic Holdings Corporation

- Robert Bosch GmbH

- Valeo S.A.

- Continental AG

- Denso Corporation

- Hella KGaA Hueck & Co.

- Hitachi Astemo Americas, Inc.

- ZF Friedrichshafen AG

Recent Developments

- In June 2024, RemotiveLabs successfully secured a €900k investment to fuel its expansion in the remote workforce management sector. The funding will enable the company to enhance its AI-driven solutions and scale operations globally.

- In November 2024, Vecmocon raised $10 million in the first phase of its Series A funding round to accelerate its innovative efforts in AI-powered software for the automotive industry. This investment will help the company expand its product offerings and scale its customer base.

- In November 2024, Marelli unveiled its cutting-edge AI-based Electronic Control Unit (ECU) designed for advanced engine and vehicle control in motorsport. The new ECU is set to enhance vehicle performance and enable real-time, data-driven decision-making for racing teams.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 118.1 Billion |

| Forecast Revenue (2034) | USD 213.4 Billion |

| CAGR (2025-2034) | 6.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Capacity Type (32-Bit, 16-Bit, 64-Bit), By Vehicle Type (Passenger Cars, Commercial Vehicle), By Application (Powertrain, ADAS & Safety System, Body Electronics, Infotainment, Others), By Propulsion Type (Internal Combustion Engine, Battery Powered, Hybrid) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Autoliv Inc., BorgWarner Inc., Panasonic Holdings Corporation, Robert Bosch GmbH, Valeo S.A., Continental AG, Denso Corporation, Hella KGaA Hueck & Co., Hitachi Astemo Americas, Inc., ZF Friedrichshafen AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |