Quick Navigation

Report Overview

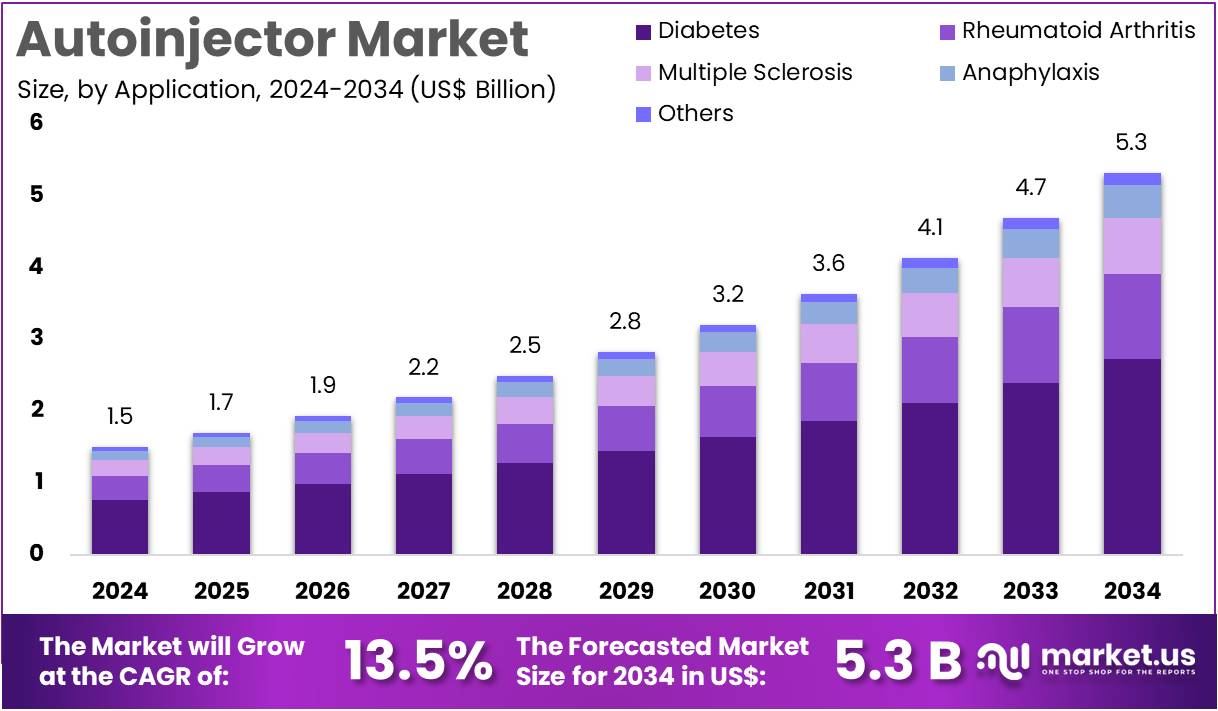

The Global Autoinjector Market Size is expected to be worth around US$ 5.3 Billion by 2034, from US$ 1.5 Billion in 2024, growing at a CAGR of 13.5% during the forecast period from 2025 to 2034.

The Autoinjector Market is experiencing significant growth fueled by the increasing global incidence of chronic conditions necessitating injectable therapies, such as the estimated 537 million adults living with diabetes worldwide in 2021 according to the International Diabetes Federation (IDF). Autoinjectors, engineered for ease of self-administration and precise dosing, are crucial for enhancing patient adherence to these treatments, particularly in homecare settings which accounted for over 60% of the chronic disease management market in 2022.

The escalating adoption of biologics, whose global sales reached US$ 367 billion in 2021, many of which are formulated for autoinjector delivery, further propels market expansion. Technological advancements are continuously improving device safety, usability, and connectivity features. The growing emphasis on patient empowerment in chronic disease management and the development of novel injectable drug formulations compatible with autoinjector systems are expected to sustain the robust growth of the autoinjector market.

Key Takeaways

- In 2023, the market for autoinjector generated a revenue of US$ 1.5 billion, with a CAGR of 13.5%, and is expected to reach US$ 5.3 billion by the year 2033.

- The product type segment is divided into disposable and reusable, with disposable taking the lead in 2023 with a market share of 61.5%.

- Considering application, the market is divided into rheumatoid arthritis, diabetes, multiple sclerosis, anaphylaxis, and others. Among these, diabetes held a significant share of 51.2%.

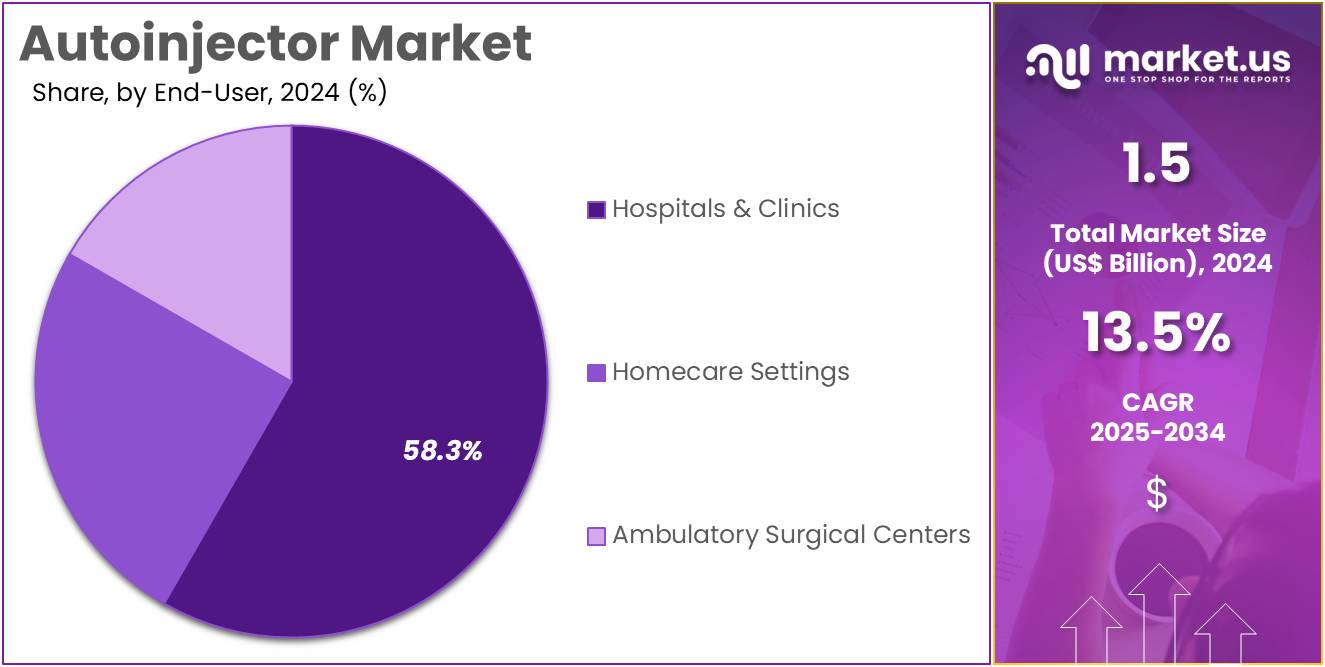

- Furthermore, concerning the end-user segment, the market is segregated into hospitals & clinics, homecare settings, and ambulatory surgical centers. The hospitals & clinics sector stands out as the dominant player, holding the largest revenue share of 58.3% in the autoinjector market.

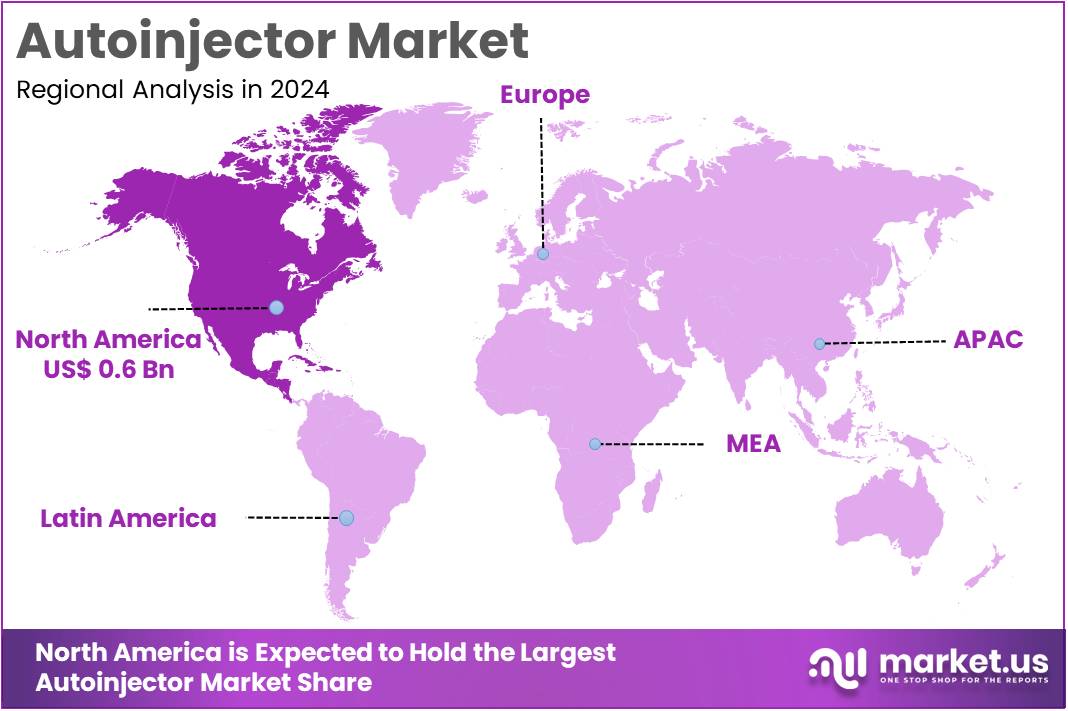

- North America led the market by securing a market share of 42.1% in 2023.

Product Type Analysis

The disposable segment led in 2024, claiming a market share of 61.5% owing to their convenience, eliminating the risk of cross-contamination, a significant concern highlighted in a 2022 study on infection control in home healthcare published in the American Journal of Infection Control. The pre-filled, single-use nature of these devices negates the need for patient maintenance, aligning with the increasing trend towards simplified medication management.

The escalating number of pharmaceutical companies choosing disposable autoinjector formats for their injectable drug launches, with over 80% of new injectable biologics in 2023 utilizing disposable devices, further solidifies this segment’s dominance. Their ease of handling and integrated safety mechanisms contribute significantly to their popularity for patient self-administration across various chronic conditions.

Application Analysis

The diabetes held a significant share of 51.2%. The significant global burden of diabetes, with the IDF projecting a continued increase in prevalence, necessitates reliable and convenient insulin delivery. Autoinjectors have become a cornerstone of diabetes management, improving adherence to insulin regimens, which a 2021 study in Diabetes Care linked to better glycemic control.

The development of advanced insulin analogs and biosimilars specifically formulated for autoinjector delivery, accounting for over 60% of the insulin market by volume in 2023, further bolsters this segment. Features like integrated dose counters and safety needles in diabetes autoinjectors enhance their utility and patient acceptance.

End-User Analysis

The hospitals and clinics segment exhibited a remarkable growth rate, capturing a revenue share of 58.3%. These healthcare settings are essential for the early diagnosis and treatment of chronic diseases that require injectable medications. In hospitals and clinics, healthcare professionals introduce patients to autoinjector devices and train them on proper usage. A high volume of patients initiating injectable therapies contributes significantly to the dominance of this segment. Moreover, the presence of established procurement processes for medical devices further strengthens their leadership position.

Hospitals and clinics also play a vital role in ongoing patient education and management of injectable therapies. They are crucial in helping patients transition toward self-administration using autoinjectors in homecare or outpatient settings. Regular follow-ups and patient support programs organized by hospitals encourage better compliance and familiarity with autoinjectors. These factors not only promote immediate use but also influence the long-term adoption of autoinjectors. As a result, hospitals and clinics continue to be a key driver for growth in the autoinjector market.

Key Market Segments

By Product Type

- Disposable

- Reusable

- Prefilled

- Empty

By Application

- Rheumatoid Arthritis

- Diabetes

- Multiple Sclerosis

- Anaphylaxis

- Others

By End-user

- Hospitals & Clinics

- Homecare Settings

- Ambulatory Surgical Centers

Drivers

Increasing Prevalence of Chronic Diseases Requiring Injectable Medications is Driving the Market

The escalating global prevalence of chronic diseases necessitating injectable therapies is a primary driver for the Autoinjector Market. The World Health Organization (WHO) reported in 2023 that non-communicable diseases (NCDs), including diabetes, autoimmune disorders, and various forms of cancer often treated with injectable biologics, account for 71% of all deaths globally.

Specifically, the prevalence of rheumatoid arthritis was estimated at around 0.5-1% of the adult population worldwide in a 2022 study published in Nature Reviews Rheumatology, a significant portion of whom require self-administered injections via autoinjectors. Similarly, the number of individuals diagnosed with multiple sclerosis globally was estimated at 2.8 million in 2021. The increasing incidence of these conditions, coupled with advancements in injectable drug therapies, directly fuels the demand for convenient delivery systems like autoinjectors.

Restraints

Need for Improved Patient Convenience and Adherence is Driving Adoption

The growing emphasis on patient-centric care and the critical need to enhance adherence to prescribed injectable medications are significant drivers for the Autoinjector Market. Autoinjectors offer a user-friendly alternative to traditional syringes, simplifying the self-injection process and reducing anxiety, as highlighted in a 2021 patient preference study published in the Journal of Pharmaceutical Sciences.

Improved adherence to medications for chronic conditions, facilitated by the convenience of autoinjectors, has been linked to better clinical outcomes and reduced healthcare costs, as demonstrated in a 2022 health economics study published in Value in Health. The portability and discreetness of autoinjectors enable patients to manage their conditions more effectively in their daily lives, further driving their adoption across various therapeutic areas.

Opportunities

Technological Advancements Focusing on Safety and Ease of Use are Creating Growth Opportunities

Continuous technological advancements in autoinjector design are creating substantial growth opportunities within the market. Innovations aimed at enhancing safety, such as automatic needle retraction mechanisms to prevent accidental needle-stick injuries (integrated into over 60% of new autoinjector designs in 2023), are increasing user confidence.

Features focused on ease of use, including ergonomic designs and clear visual and auditory feedback for dose delivery (present in over 70% of marketed autoinjectors in 2024), are improving patient compliance, particularly among elderly or dexterity-impaired individuals. The emergence of connected or smart autoinjectors, which can track dosage and provide adherence data to patients and healthcare providers (adoption rates increased by 30% between 2022 and 2024), represents another significant growth avenue by enabling remote monitoring and personalized treatment management.

Impact of Macroeconomic / Geopolitical Factors

The Autoinjector Market in 2025 is influenced by macroeconomic factors affecting healthcare spending and market access. Economic growth in key regions, particularly in developed countries with established healthcare infrastructure, typically supports greater adoption of advanced drug delivery systems like autoinjectors. However, economic downturns can lead to increased price sensitivity and potential limitations in healthcare budgets, impacting the uptake of higher-priced devices.

Government healthcare policies, including reimbursement frameworks for medical devices and pharmaceuticals, significantly shape market dynamics. Favorable reimbursement policies for autoinjector-administered medications can directly drive market growth by reducing the financial burden on patients and healthcare providers.

Geopolitical factors, such as trade policies, tariffs on medical device components (including plastics, metals for springs, and specialized needles), and international supply chain disruptions, can affect manufacturing costs and the availability of autoinjectors globally. Fluctuations in currency exchange rates can also impact the profitability of international sales for autoinjector manufacturers.

The recent US tariff policies implemented in April 2025 have specific implications for the Autoinjector Market. Data from the United States International Trade Commission (USITC) indicates that a significant portion of medical device components, including those used in autoinjectors, are imported. Tariffs on these imported materials and parts could lead to increased manufacturing costs for US-based autoinjector producers.

Furthermore, the imposition of tariffs might incentivize manufacturers to explore alternative sourcing options or relocate production, potentially causing disruptions in the supply chain. The possibility of retaliatory tariffs from other countries on US-made autoinjectors could also negatively impact the export competitiveness of US manufacturers in the global market. The long-term consequences will depend on the duration and scope of these tariffs and the strategic responses of companies within the autoinjector supply chain.

Latest Trends

Stringent Regulatory Requirements and Safety Concerns May Restrain Market Growth

Stringent regulatory requirements imposed by authorities like the US Food and Drug Administration (FDA) and the European Medicines Agency (EMA) regarding the safety, efficacy, and usability of autoinjectors can present restraints to market growth. Compliance with these complex guidelines, which often involve extensive testing and documentation, can increase the time and cost associated with product development and market approval.

Furthermore, ongoing concerns about the risk of injection-site reactions and the proper disposal of sharps necessitate the incorporation of robust safety features and comprehensive user training, adding to the manufacturing complexity and potentially the cost of autoinjectors. The need for continuous post-market surveillance and adherence to evolving regulatory standards also requires ongoing investment from manufacturers, which can impact overall market dynamics.

Regional Analysis

North America is leading the Autoinjector Market

North America dominated the market with the highest revenue share of 42.1% owing to the high prevalence of chronic diseases and its advanced healthcare infrastructure. According to the Centers for Disease Control and Prevention (CDC) data from 2023, over 37 million adults in the US have diabetes, and approximately 1.5 million adults have rheumatoid arthritis, both key application areas for autoinjectors.

The region’s well-established healthcare system, with comprehensive insurance coverage for medical devices and a strong presence of key pharmaceutical and medical device companies, facilitates the widespread adoption of autoinjectors. The increasing focus on patient self-management, coupled with the availability of a wide range of innovative disposable autoinjector products, further strengthens North America’s market leadership.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing burden of chronic diseases and growing investments in healthcare infrastructure. The International Diabetes Federation (IDF) reported in 2021 that the Asia Pacific region has the highest number of adults living with diabetes globally, exceeding 290 million.

Improving healthcare access and affordability, coupled with a rising awareness of the benefits of self-administration, are driving the market for autoinjectors. Increasing adoption of biologics for autoimmune diseases and the expansion of home healthcare services are also contributing to the significant growth potential of the Autoinjector Market in Asia Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the autoinjector market are focusing heavily on innovation and strategic partnerships. Significant investments are being made in research and development to create safer, more user-friendly, and connected devices. These advancements are aimed at improving patient adherence and overall experience.

Collaborations with pharmaceutical companies remain critical for ensuring device compatibility with a wide range of injectable medications. Furthermore, the co-development of integrated drug-device solutions is helping companies strengthen their market positions and meet the evolving needs of healthcare providers and patients.

Expanding global manufacturing and distribution networks is a major strategy adopted by market leaders. A particular focus is being placed on high-growth emerging markets, where the prevalence of chronic diseases is steadily increasing. Companies are actively entering these regions to capitalize on the rising demand for autoinjectors. By strengthening their international presence, firms aim to achieve better market penetration, reduce production costs, and improve supply chain efficiencies. These efforts are positioning them to gain a competitive advantage in a rapidly expanding healthcare landscape.

Ypsomed AG, headquartered in Burgdorf, Switzerland, is a prominent player specializing in autoinjector development and manufacturing. The company offers a wide range of customizable autoinjector platforms tailored to different therapeutic needs. Strategic partnerships with leading pharmaceutical companies have played a key role in their success. Ypsomed emphasizes innovation, patient convenience, and high-quality manufacturing processes. Their 2023 financial report revealed a significant increase in revenue from their delivery systems division, underlining the strong market demand and their effective business strategies.

Top Key Players in the Autoinjector Market

- Ypsomed

- SHL Medical AG

- Owen Mumford

- Eli Lilly

- Biogen Idec

- Amgen

- Altaviz

- AbbVie

Recent Developments

- In March 2024, Ypsomed decided to sell its insulin pen needle and blood glucose monitoring businesses to MTD Group. This strategic decision enables Ypsomed to refocus its efforts on developing smart pumps and autoinjectors. The company intends to invest USD 111 million to expand its Solothurn production facility, and this transition will maintain employment until the close of 2024. Ypsomed will continue its role as a contract manufacturer until mid-2025.

- In October 2023, Altaviz introduced the AltaVISC auto-injector platform, engineered to enhance the delivery of high-viscosity and high-volume biologics. This innovative platform employs Pico-cylinders to control temperature and gas composition, ensuring accurate and efficient administration. The device is optimized for various drug formulations, including delicate biologics, with an emphasis on improving the experience for patients using the technology at home.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.5 billion |

| Forecast Revenue (2034) | US$ 5.3 billion |

| CAGR (2025-2034) | 13.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Disposable and Reusable (Prefilled and Empty)), By Application (Rheumatoid Arthritis, Diabetes, Multiple Sclerosis, Anaphylaxis, and Others), By End-user (Hospitals & Clinics, Homecare Settings, and Ambulatory Surgical Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ypsomed, SHL Medical AG, Owen Mumford, Eli Lilly, Biogen Idec, Amgen, Altaviz, and AbbVie. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |