Quick Navigation

Report Overview

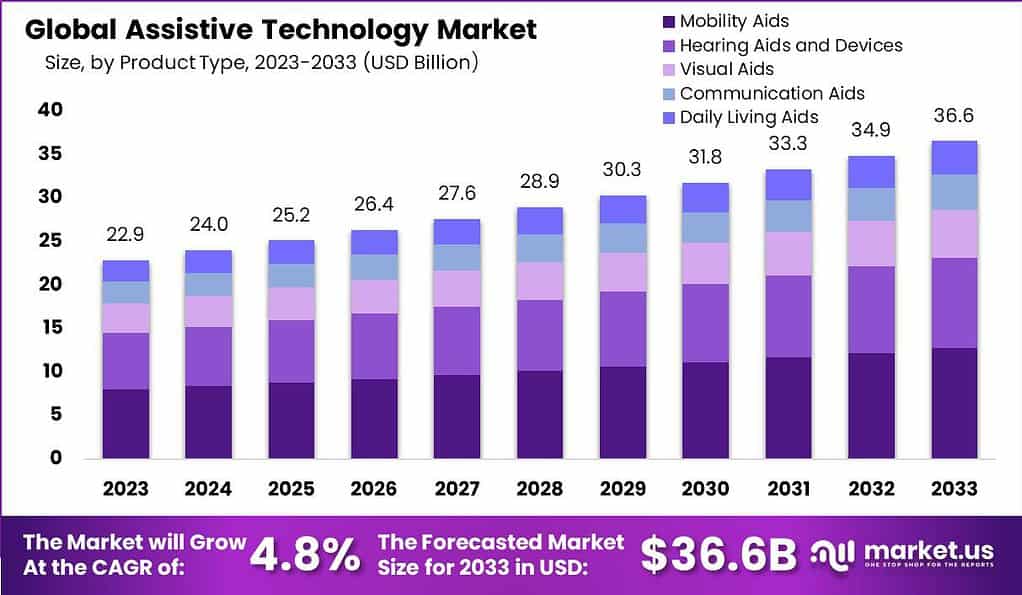

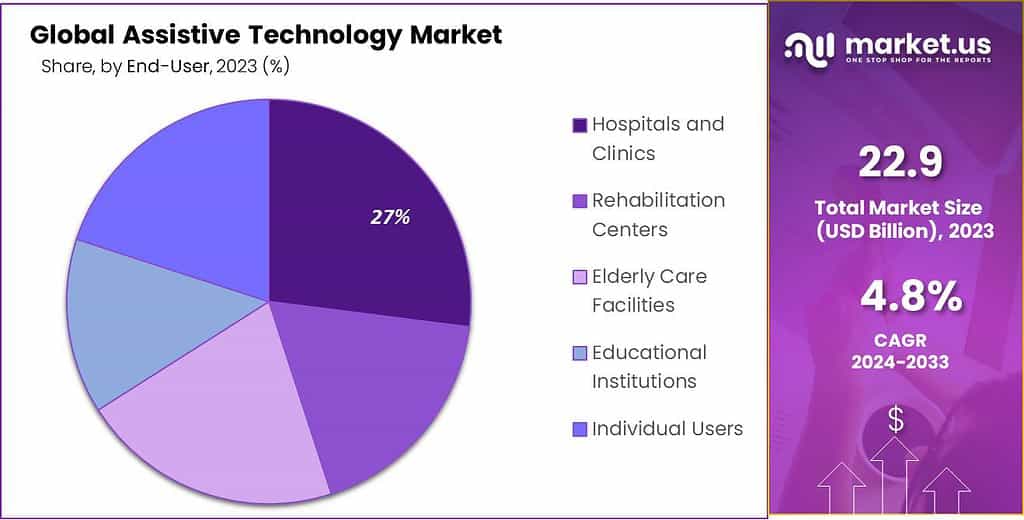

The Global Assistive Technology Market size is expected to be worth around USD 36.6 Billion by 2033, from USD 22.9 Billion in 2023, growing at a CAGR of 4.8% during the forecast period from 2024 to 2033.

Assistive technology refers to any device, equipment, software or system that enhances the functional capabilities of individuals with disabilities or limitations. It helps them perform tasks, increase their independence, and improve their overall quality of life. Assistive technology can assist people with various disabilities, including physical, sensory, cognitive, and developmental impairments.

The assistive technology market has experienced significant growth in recent years due to advancements in technology, increased awareness, and a growing aging population. The market includes both commercial products sold by manufacturers and custom solutions developed by assistive technology professionals.

Analyst Viewpoint

According to the World Health Organization (WHO), it is estimated that currently, 2.5 billion people require one or more assistive products, such as wheelchairs, hearing aids, or communication and cognition support apps. With a worldwide increase in the aging population and a surge in noncommunicable diseases, this figure is projected to surpass 3.5 billion by 2050, particularly affecting many older individuals who will require two or more assistive products as they age.

The assistive technology market is poised for substantial growth, driven by multiple driving factors and presenting abundant opportunities. The increasing prevalence of disabilities, coupled with a growing aging population, acts as a significant driver for market expansion.

Additionally, government initiatives promoting inclusivity and accessibility further bolster the market’s growth trajectory. Technological advancements play a crucial role in driving innovation within the market, leading to the development of more advanced and user-friendly assistive technology solutions.

Furthermore, the rising demand for personalized and customizable assistive devices opens up opportunities for market players to provide tailored solutions. With emerging economies focusing on improving healthcare infrastructure and increasing awareness about assistive technology, regions like Asia Pacific and Latin America offer untapped potential. Overall, the assistive technology market presents a promising landscape with ample driving factors and opportunities for market participants to meet the evolving needs of individuals with disabilities and enhance their overall well-being.

Key Takeaways

- The global Assistive Technology Market is projected to reach USD 36.6 billion by 2033, with a steady Compound Annual Growth Rate (CAGR) of 4.8% during the forecast period from 2024 to 2033.

- In 2023, the Mobility Aids segment emerged as the dominant player in the assistive technology market, capturing more than a 35% share.

- In 2023, the Hospitals and Clinics segment emerged as the dominant player in the assistive technology market, capturing more than a 27% share.

- In 2023, the Online Retailers segment emerged as the dominant player in the assistive technology market, capturing more than a 33% share.

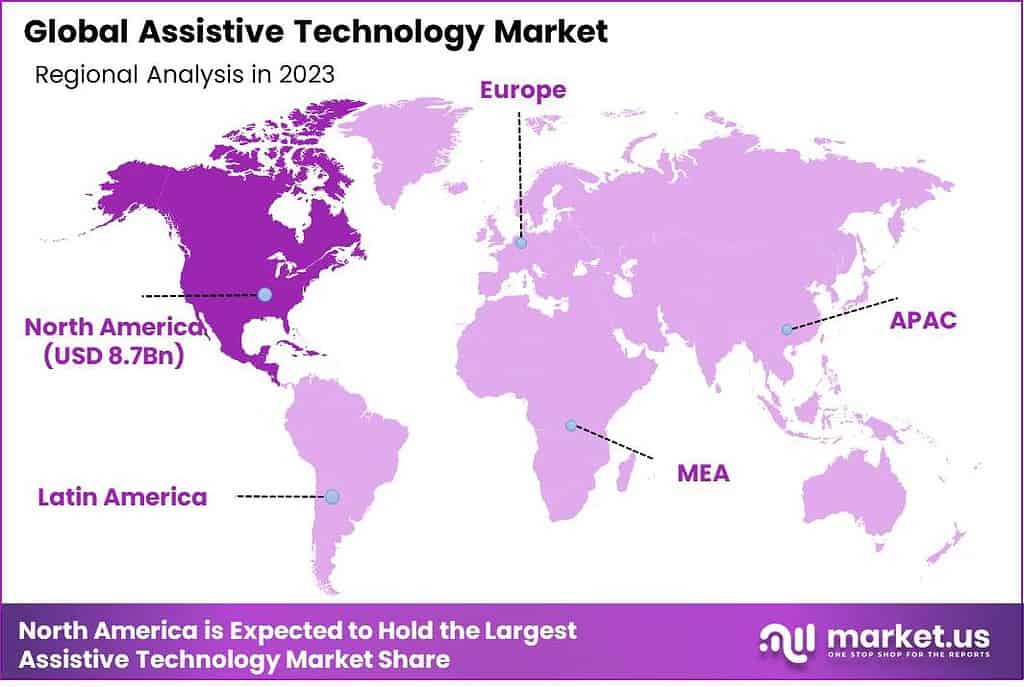

- In 2023, North America emerged as the dominant region in the global assistive technology market, capturing more than a 38% share.

Product Type Analysis

In 2023, the Mobility Aids segment emerged as the dominant player in the assistive technology market, capturing more than a 35% share. This segment encompasses various products such as wheelchairs, scooters, and walking aids like canes and crutches. Several factors contribute to the dominance of Mobility Aids in the market.

Firstly, the growing global aging population has significantly increased the demand for mobility aids. As individuals age, they may experience reduced mobility or physical disabilities, necessitating the use of assistive devices for independent movement. The rising prevalence of chronic conditions such as arthritis and musculoskeletal disorders further drives the demand for mobility aids.

Secondly, advancements in technology have led to the development of innovative and user-friendly mobility aids. Manufacturers are incorporating features such as lightweight materials, ergonomic designs, and enhanced maneuverability, thereby improving the overall user experience. These technological advancements have increased the adoption of mobility aids among individuals with mobility impairments.

Furthermore, government initiatives and favorable reimbursement policies have played a crucial role in promoting the use of mobility aids. Many countries have implemented programs to support the accessibility and affordability of assistive devices, making them more accessible to individuals in need. This has positively impacted the market growth of mobility aids.

Moreover, the increasing awareness about the importance of inclusive environments and equal opportunities for individuals with disabilities has propelled the demand for mobility aids. Governments, organizations, and advocacy groups are actively working to create barrier-free environments and improve accessibility in public spaces. This has further boosted the adoption of mobility aids as a means to enhance mobility and independence.

Overall, the Mobility Aids segment has dominated the assistive technology market due to the rising aging population, technological advancements, supportive government initiatives, and growing awareness about inclusivity. With ongoing research and development activities, it is expected that the market for mobility aids will continue to expand and offer innovative solutions to individuals with mobility impairments.

End-User Analysis

In 2023, the Hospitals and Clinics segment emerged as the dominant player in the assistive technology market, capturing more than a 27% share. This segment specifically caters to the needs of healthcare institutions such as hospitals and clinics. Several factors contribute to the dominance of Hospitals and Clinics in the market.

Firstly, hospitals and clinics serve as primary points of care for individuals with disabilities or mobility impairments. These healthcare facilities are equipped with specialized departments and professionals who assess, diagnose, and provide comprehensive care to patients requiring assistive technology. The wide range of assistive devices available in hospitals and clinics, coupled with expert guidance, makes them a preferred choice for individuals seeking assistive technology solutions.

Secondly, hospitals and clinics often have dedicated rehabilitation departments that specialize in providing therapy and rehabilitation services to patients with disabilities. These departments are equipped with state-of-the-art assistive technology devices and tools necessary for rehabilitation and recovery. The availability of such advanced devices and the expertise of healthcare professionals contribute to the dominant market position of Hospitals and Clinics.

Furthermore, hospitals and clinics frequently collaborate with assistive technology manufacturers and suppliers, ensuring a steady supply of the latest products. This cooperation enables healthcare facilities to offer a wide range of assistive technology options to patients, catering to their specific needs and preferences. The strong partnerships between hospitals/clinics and assistive technology providers contribute to the dominance of this segment in the market.

Moreover, the increasing prevalence of chronic diseases and disabilities has led to a higher demand for assistive technology in healthcare settings. Hospitals and clinics are the primary institutions where individuals seek medical attention and treatment for their conditions. Consequently, these settings become the natural choice for individuals to explore and obtain assistive technology solutions, further strengthening the market position of the Hospitals and Clinics segment.

Distribution Channel

In 2023, the Online Retailers segment emerged as the dominant player in the assistive technology market, capturing more than a 33% share. This segment specifically focuses on the distribution of assistive technology products through online retail platforms. Several factors contribute to the dominance of Online Retailers in the market.

Firstly, the convenience and accessibility offered by online retailers have significantly influenced the purchasing behavior of consumers. People can browse and purchase a wide range of assistive technology products from the comfort of their homes, without the need to physically visit a store. This convenience factor has propelled the popularity of online retailers, leading to their dominant market position.

Secondly, online retailers often offer a broader selection of assistive technology products compared to brick-and-mortar stores. They can source products from various manufacturers and suppliers, providing customers with a wide range of options to choose from. This extensive product availability has attracted consumers to online platforms, as they can find specific assistive technology devices that cater to their unique needs and preferences.

Furthermore, online retailers frequently provide detailed product information, customer reviews, and ratings, enabling shoppers to make informed purchasing decisions. The transparency and accessibility of information empower consumers to compare different products, assess their suitability, and select the most suitable assistive technology solution. This transparency and customer-centric approach have contributed to the dominance of the Online Retailers segment.

Moreover, online retailers often offer competitive pricing and discounts, making assistive technology products more affordable for consumers. They can leverage their online platform’s scalability and efficiency to reduce operational costs, resulting in cost savings that can be passed on to customers. The availability of competitive pricing and attractive discounts has been a significant driver for consumers to choose online retailers over other distribution channels.

Key Market Segments

Product Type

- Mobility Aids

- Wheelchairs

- Scooters

- Walking Aids (canes, crutches)

- Transfer Lifts

- Hearing Aids and Devices

- Hearing Aids

- Cochlear Implants

- Assistive Listening Devices

- Visual Aids

- Screen Readers

- Braille Displays

- Magnifiers

- Electronic Glasses

- Communication Aids

- Augmentative and Alternative Communication (AAC) Devices

- Speech Generating Devices

- Daily Living Aids

- Adaptive Kitchen and Dining Tools

- Adaptive Clothing and Dressing Aids

- Environmental Control Devices

End-User

- Hospitals and Clinics

- Rehabilitation Centers

- Elderly Care Facilities

- Educational Institutions

- Individual Users

Distribution Channel

- Online Retailers

- Specialty Assistive Technology Stores

- Hospitals and Clinics

- Government Agencies and NGOs

Driver

Increasing Aging Population

The increasing aging population is a significant driver for the growth of the assistive technology market. As the global population continues to age, there is a growing demand for technologies that can enhance the quality of life and independence of older adults.

Assistive technology plays a vital role in addressing the age-related challenges faced by the elderly, such as mobility issues, cognitive decline, and chronic health conditions. These technologies encompass a wide range of devices, including mobility aids, hearing aids, vision-enhancing tools, communication devices, and home automation systems. The rising aging population fuels the demand for assistive technology, as older adults seek innovative solutions to maintain their autonomy and improve their overall well-being.

Restraint

High Costs of Assistive Technology

Despite the growing demand, the high costs associated with assistive technology pose a significant restraint to market growth. Assistive devices often involve advanced technologies, specialized components, and extensive research and development. These factors contribute to the high manufacturing and development costs, which are ultimately passed on to the end-users.

Additionally, health insurance coverage and reimbursement policies for assistive technology can be limited and vary across different regions, making these devices inaccessible to many individuals who could benefit from them. The high costs create financial barriers for individuals, healthcare providers, and organizations, limiting the adoption and penetration of assistive technology in the market.

Opportunity

Technological Advancements

Technological advancements present a significant opportunity for the assistive technology market. Rapid progress in areas such as artificial intelligence, robotics, wearable devices, and sensor technology has led to the development of innovative assistive technologies. These advancements have enabled the creation of more sophisticated and user-friendly devices that can cater to specific needs and preferences.

For instance, smart home systems can be integrated with assistive technology to provide a seamless and personalized experience for individuals with disabilities or elderly individuals. These technological advancements not only enhance the functionality and performance of assistive devices but also contribute to reducing their costs over time. As technology continues to evolve, there is a vast potential for the development of new and improved assistive technologies that can address a broader range of disabilities and promote inclusivity.

Challenge

Regulatory Compliance

Regulatory compliance poses a significant challenge to the assistive technology market. The development and commercialization of assistive devices require adherence to various regulations and standards to ensure their safety, efficacy, and quality. These regulations may vary across different countries and regions, adding complexity to the process. Obtaining regulatory approvals and certifications can be time-consuming and costly, particularly for smaller manufacturers or startups in the industry.

Additionally, the evolving nature of technology often outpaces the development of regulations, creating a challenge for both manufacturers and regulatory bodies to keep up with the pace of innovation. Striking a balance between encouraging innovation and ensuring consumer safety remains a challenge in the regulatory landscape of the assistive technology market. It is crucial for manufacturers to stay abreast of the regulatory requirements and work closely with regulatory authorities to navigate these challenges and bring their products to market effectively.

Regional Analysis

In 2023, North America emerged as the dominant region in the global assistive technology market, capturing more than a 38% share. The demand for Assistive Technology in North America was valued at USD 8.7 billion in 2023 and is anticipated to grow significantly in the forecast period.

This regional dominance can be attributed to several key factors. Firstly, North America has a well-established healthcare infrastructure and is known for its advanced medical facilities and research capabilities. This strong healthcare system provides a conducive environment for the development and adoption of assistive technology. The presence of leading manufacturers, healthcare institutions, and research organizations in the region contributes to the market’s growth and dominance.

Secondly, the high prevalence of chronic diseases, aging population, and disability rates in North America drives the demand for assistive technology. The region has a significant population of elderly individuals who require assistive devices to improve their mobility and quality of life. Additionally, the increasing incidence of disabilities caused by factors such as accidents, injuries, and chronic conditions further fuels the demand for assistive technology solutions in North America.

Furthermore, North America is at the forefront of technological advancements and innovation. The region is home to numerous technology companies and startups that specialize in developing cutting-edge assistive technologies. The availability of advanced products and solutions, such as smart devices, wearable technology, and robotics, contributes to the dominance of North America in the assistive technology market.

Moreover, favorable government initiatives and reimbursement policies in North America support the adoption of assistive technology. Government agencies, healthcare authorities, and insurance providers in the region actively promote accessibility and inclusivity through various programs and policies. These initiatives facilitate the availability and affordability of assistive technology devices, further driving market growth in North America.

Additionally, North America has a strong consumer base with a high level of awareness and acceptance of assistive technology. The region’s population is receptive to technological advancements and has a culture of embracing innovation. This favorable consumer mindset, coupled with a higher disposable income, contributes to the widespread adoption of assistive technology products in North America.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The assistive technology market consists of several key players that contribute to its growth and development. These companies are at the forefront of designing, manufacturing, and distributing a wide range of assistive devices and solutions Analyzing key players in the Assistive Technology Market reveals a competitive landscape characterized by innovation, diversified product portfolios, and a commitment to improving the lives of individuals with disabilities and the aging population.

Top Key Players

- Sonova Holding AG

- GN Store Nord A/S

- William Demant Holding A/S

- Invacare Corporation

- Ottobock SE & Co. KGaA

- Drive DeVilbiss Healthcare

- MED-EL Medical Electronics

- Tobii Dynavox

- Cochlear Limited

- Enabling Devices LLC

- Permobil AB

- Freedom Scientific (VFO Group)

- Other Key Players

Recent Developments

- Body Vision Medical and Mediflex Partnership: On September 8, 2023, Body Vision Medical, a pioneer in AI-enhanced intraoperative imaging, entered into a distribution agreement with Mediflex, known for its innovative surgical devices. This partnership allows Body Vision Medical to distribute Mediflex’s Bronchoscope Stabilization System (BSS) globally, potentially enhancing the reach and impact of this advanced medical technology.

- Vuzix Corporation Expands into Japan: On June 14, 2023, Vuzix Corporation, a frontrunner in Smart Glasses and Augmented Reality (AR) technology, announced a significant distribution agreement with ASK Corporation, a prominent Japanese IT equipment distributor. This agreement was marked by a substantial initial purchase order from ASK Corporation, facilitating the entry of Vuzix’s cutting-edge products into the Japanese market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 22.9 Bn |

| Forecast Revenue (2033) | US$ 36.6 Bn |

| CAGR (2024-2033) | 4.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Mobility Aids Devices (Wheelchairs, Scooters, Walking Aids (canes, crutches)), Hearing Aids and Devices (Hearing Aids, Cochlear Implants, Assistive Listening Devices), Visual Aids (Screen Readers, Braille Displays, Magnifiers, Electronic Glasses), Communication Aids (Augmentative and Alternative Communication (AAC) Devices, Speech Generating Devices), Daily Living Aids (Adaptive Kitchen and Dining Tools, Adaptive Clothing and Dressing Aids, Environmental Control Devices)), By End-User (Hospitals and Clinics, Rehabilitation Centers, Elderly Care Facilities, Educational Institutions, Individual Users), By Distribution Channel (Online Retailers, Specialty Assistive Technology Stores, Hospitals and Clinics, Government Agencies and NGOs) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, and Rest of Europe; APAC- China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, and Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- South Africa, Saudi Arabia, UAE & Rest of MEA |

| Competitive Landscape | Sonova Holding AG, GN Store Nord A/S, William Demant Holding A/S, Invacare Corporation, Ottobock SE & Co. KGaA, Drive DeVilbiss Healthcare, MED-EL Medical Electronics, Tobii Dynavox, Cochlear Limited, Enabling Devices LLC, Permobil AB, Freedom Scientific (VFO Group), Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Assistive Technology (AT) refers to devices, equipment, or systems that enhance the functional capabilities of individuals with disabilities, enabling them to perform tasks that might otherwise be challenging.

The Global Assistive Technology Market size is expected to be worth around USD 36.6 Billion by 2033, from USD 22.9 Billion in 2023, growing at a CAGR of 4.8% during the forecast period from 2024 to 2033.

The market trend in assistive technology has been characterized by continuous innovation and technological advancements. There has been a notable shift towards more user-friendly and customizable solutions. Additionally, the integration of artificial intelligence and smart technologies to enhance the effectiveness of assistive devices has been a prominent trend.

The demand for assistive technology has been rising globally, driven by factors such as a growing aging population, increasing awareness and acceptance of assistive devices, and advancements in technology.

Sonova Holding AG, GN Store Nord A/S, William Demant Holding A/S, Invacare Corporation, Ottobock SE & Co. KGaA, Drive DeVilbiss Healthcare, MED-EL Medical Electronics, Tobii Dynavox, Cochlear Limited, Enabling Devices LLC, Permobil AB, Freedom Scientific (VFO Group), Other Key Players

In 2023, North America emerged as the dominant region in the global assistive technology market, capturing more than a 38% share.