Quick Navigation

Report Overview

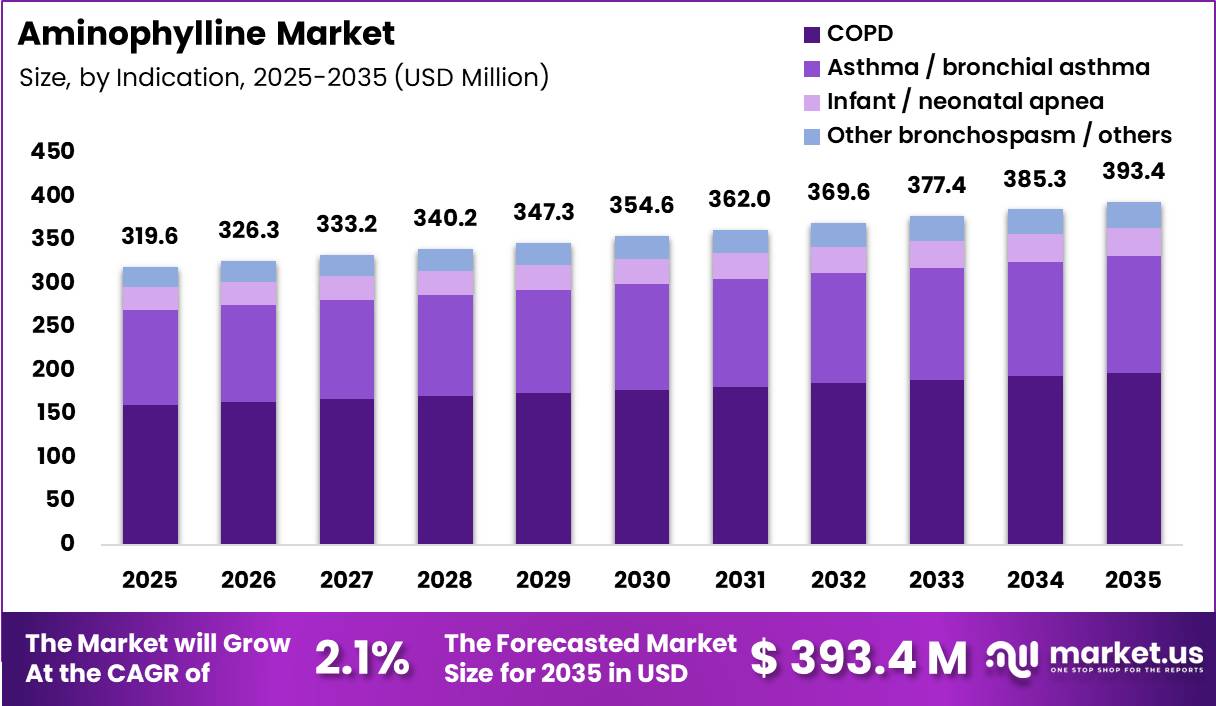

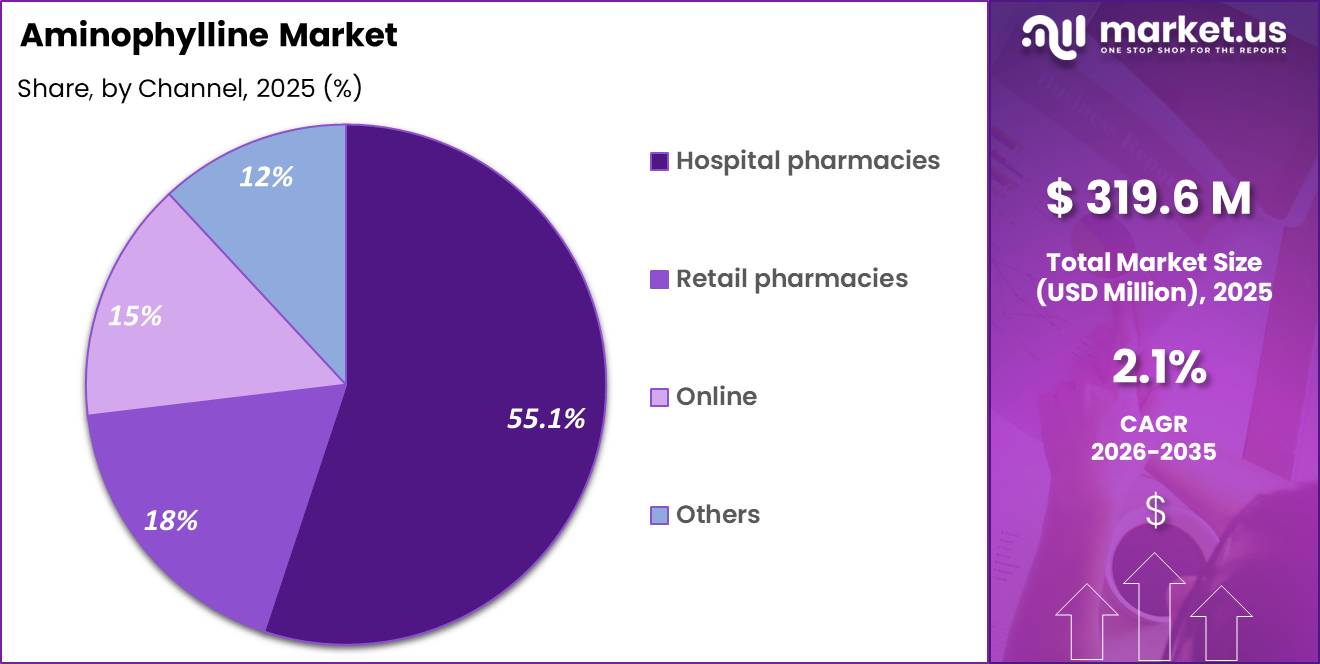

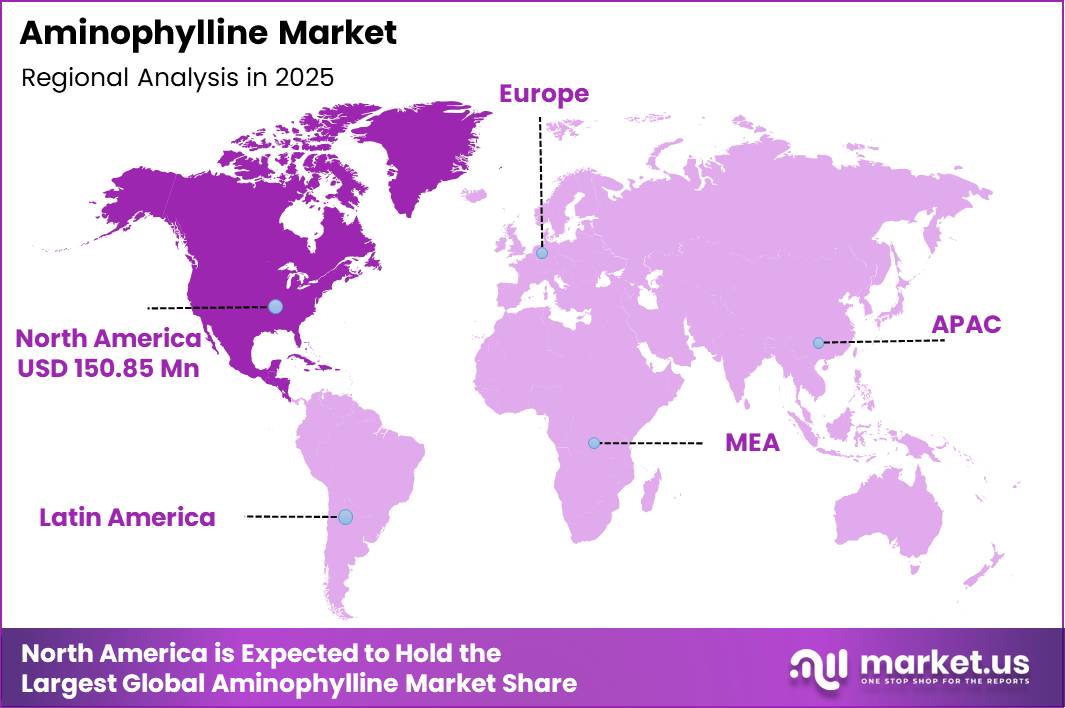

Global Aminophylline Market size is expected to be worth around US$ 393.4 Million by 2035 from US$ 319.6 Million in 2025, growing at a CAGR of 2.1% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 47.2% share with a revenue of US$150.9 Million.

The Aminophylline market is a global pharmaceutical sector encompassing a methylxanthine bronchodilator which is a compound of theophylline and ethylenediamine administered to patients with COPD, asthma, infant apnea, and related bronchospastic conditions to relieve airway obstruction and improve respiratory function.

Rising global incidence of severe chronic obstructive pulmonary disease and acute asthma episodes acts as the primary driving factor. The market is growing due to the immediate therapeutic necessity for low-cost, effective emergency interventions in critical care units as confirmed by WHO, COPD causing 3.4 million deaths in 2023 by WHO, 2024.

- Aminophylline is confirmed as FDA-approved to treat reversible airway obstruction due to asthma and other chronic lung diseases, with NIH StatPearls identifying therapeutic drug concentration monitoring as critical to avoiding toxicity from its narrow therapeutic index by NIH, 2025.

The global market scope includes vital treatments with respect to oral tablet forms and injectable liquids. Capacity segmentations include low dose 100 mg tablets as well as high concentration 250 mg injections in ampoule form. Injectable forms account for the most rapidly growing element of demand since of increased emergency department visits.

The future market will be dependent on automation processes with respect to the exact monitoring of serum levels to avoid any toxic effects of therapy. The integration of artificial intelligence will help to establish accurate algorithms with respect to dosing through predictive means. AI-based therapeutic drug monitoring systems are currently used within hospital pharmacies.

Key Takeaways

- Market Size: Global Aminophylline Market size is expected to be worth around US$ 393.4 Million by 2035 from US$ 319.6 Million in 2025.

- Market Share: The market growing at a CAGR of 2.1% during the forecast period from 2026 to 2035.

- Indication Analysis: COPD is identified as the dominant indication, accounting for 50.2% of the market in 2025, driven by the high global burden of chronic obstructive pulmonary disease and aminophylline’s continued use in low- and middle-income country hospital settings.

- Route Analysis: Parenteral route is confirmed as the dominant route of administration at 56.4%, reflecting aminophylline’s primary use as an intravenous agent in acute bronchospasm and COPD exacerbation management across hospital settings.

- Product Type Analysis: Branded aminophylline products lead the product type segment at 72.1%, supported by established regulatory approvals and institutional formulary positions across North American and European hospital pharmacies.

- Channel Analysis: Hospital pharmacies account for the largest channel share at 55.1%, reflecting aminophylline’s predominant use in supervised inpatient and emergency care settings requiring therapeutic drug monitoring.

- Regional Analysis: North America holds the largest regional share at 47.2%, underpinned by FDA approval, established hospital formulary inclusion, and continued use in ICU and acute respiratory care settings.

Indication Analysis

COPD Represents the Dominant Segment in the Market.

In 2025, COPD accounted for a leading 50.2% share of the Aminophylline market, this dominance is driven by the progressive nature of chronic obstructive pulmonary disease requiring sustained bronchodilation to improve airflow limitations. For instance, severe emphysema and chronic bronchitis patients depend heavily on continuous xanthine-derivative therapy when long-acting beta-agonists fail to manage daily dyspnea.

Asthma / Bronchial Asthma is the fastest-growing indication segments in the aminophylline market, driven by the rising global prevalence of respiratory disorders, particularly in urban and low- and middle-income regions. Increasing exposure to air pollution, allergens, and occupational irritants, along with improved diagnosis rates, is contributing to higher patient numbers.

In several healthcare settings, especially where advanced therapies are limited, aminophylline continues to be used as a cost-effective option for managing severe and acute asthma cases.

By Route

Parenteral Represents the Dominant Route of Administration.

In 2025, parenteral administration accounted for a leading 56.4% share of the Aminophylline market by route, this dominance is driven by the clinical demand for immediate, 100% systemic bio-availability during acute respiratory failure.

For instance, status asthmaticus crises require immediate, controlled intravenous infusions to bypass gastrointestinal absorption delays and quickly relax smooth muscle tissue. Due to aminophylline’s primary clinical application as an intravenous bronchodilator in acute respiratory emergencies including severe COPD exacerbations, acute severe asthma, and bronchospasm where rapid systemic delivery is required and oral administration is not clinically feasible. Intravenous aminophylline is administered under strict therapeutic drug monitoring given its narrow therapeutic index.

Oral tablets / capsules are the fastest-growing route of administration segment. Sustained-release oral theophylline and aminophylline tablet formulations are used for long-term maintenance management of COPD and chronic asthma particularly in low- and middle-income country markets where inhaled therapies are less accessible or affordable.

Between 2026 and 2035, oral aminophylline tablet demand is projected to grow alongside expanding COPD disease management programmes across Asia Pacific and Africa, where cost-effective oral maintenance bronchodilators remain clinically relevant.

By Product Type

Branded Aminophylline Products Represent the Dominant Segment in the Market

In 2025, branded aminophylline products accounted for a leading 72.1% share of the Aminophylline market by product type, due to their established regulatory approvals, institutional formulary positions across North American and European hospital pharmacies, and the clinical preference for branded reference products in therapeutic drug monitoring protocols where product bioequivalence consistency is considered clinically important.

Hospital formulary committee preferences, therapeutic drug monitoring protocol requirements, regulatory approval status, and brand equity accumulated through long-term institutional use are the primary structural determinants of branded product segment leadership.

Generic aminophylline products are the fastest-growing product type segment across the forecast period. Progressive patent expiry across aminophylline formulations and the cost containment priorities of hospital pharmacy systems are driving generic substitution across both parenteral and oral administration formats

By Channel

Hospital Pharmacies Are Mostly Utilized in the Market.

In 2025, hospital pharmacies accounted for a leading 55.1% share of the Aminophylline market by channel, due to aminophylline’s primary clinical application in acute and intensive care settings requiring intravenous administration, therapeutic drug monitoring, and supervised dosing protocols that are institutionally managed within hospital pharmacy systems.

Intravenous administration requirements, therapeutic drug monitoring infrastructure, hospital formulary management policies, and the acute care clinical setting of aminophylline’s primary indications are the structural determinants of hospital pharmacy channel dominance.

Online pharmacy channels, representing a small current share, are the fastest-growing distribution segment for oral aminophylline tablet and solution formulations driven by expanding e-pharmacy regulation and infrastructure across Asia Pacific and Latin America, where digital pharmacy platforms are extending access to oral maintenance respiratory medications for chronic COPD and asthma management patients beyond traditional retail pharmacy reach.

E-pharmacy regulatory framework development, smartphone penetration, and consumer adoption of digital health and pharmacy services across emerging markets are the primary growth catalysts.

Key Market Segments

By Indication

- COPD

- Asthma / bronchial asthma

- Infant / neonatal apnea

- Other bronchospasm / others

By Route

- Parenteral

- Oral tablets / capsules

- Oral solutions

- Other injectable routes

By Product Type

- Branded aminophylline products

- Generic aminophylline products

- API

By Channel

- Hospital pharmacies

- Retail pharmacies

- Online

- Others

Drivers

Therapeutic drug monitoring and protocolized dosing adoption

Aminophylline’s narrow therapeutic window is usually presented as a restraint, but in tertiary hospitals it can also act as a driver by making the product usable within controlled protocols instead of eliminating it outright. NIH-linked references note adult therapeutic theophylline concentrations are typically 10 to 20 mcg/mL, toxicity risk rises above 20 mcg/mL, post-loading levels should be checked after IV initiation, and infusion monitoring may occur every 12 to 24 hours once stabilized; These requirements fit best in higher-acuity centers with pharmacy oversight, lab support, and standardized dosing pathways.

That means demand concentrates in institutions able to operationalize serum monitoring, weight-based infusion adjustment, and toxicity surveillance, which supports a smaller but more defensible revenue pool with better utilization discipline and lower abandonment risk.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute severe asthma rescue demand in hospital settings | +1.4% | North America core, EU hospital systems, APAC urban tertiary centers, Middle East spill-over | Short term (≤ 2 years) |

| COPD exacerbation burden and older-adult admissions | +1.1% | North America core, EU core, China and Southeast Asia corridors, LMIC spill-over | Medium term (2-4 years) |

| Low-cost adjunct positioning in resource-constrained care | +1.6% | South Asia, Sub-Saharan Africa, parts of Latin America, public-hospital APAC corridors | Medium term (2-4 years) |

| Injectable legacy supply continuity and formulary retention | +0.9% | U.S. hospital market, EU institutional channels, MENA and Africa tender markets | Short term (≤ 2 years) |

| Therapeutic drug monitoring and protocolized dosing adoption | +0.7% | North America academic centers, EU tertiary hospitals, advanced APAC centers | Medium term (2-4 years) |

| Respiratory risk intensification from smoking, pollution, and infection | +1.2% | China, India, Southeast Asia, Middle East, selected U.S. and EU high-burden pockets | Long term (≥ 4 years) |

Challenges

Aging Batch API Capacity as a Structural Efficiency Drag

Aging batch based aminophylline API capacity, largely installed between the late 1990s and early 2010s, continues to constrain efficiency versus modern continuous or intensified manufacturing systems. These legacy facilities typically carry 8 to 12 % higher unit conversion costs and 3 to 5 days longer cycle times per lot, driven by less efficient process control and older equipment design.

Process variability further compounds inefficiency, with methylxanthine batch yields fluctuating by 2 to 3 % points around target assay. This leads to conservative overages, rework, and scrap rates of 1 to 2 % of annual output. In a market of roughly USD 300 to 330 million growing at approximately 2 %, these inefficiencies translate into about a 1 % point drag on effective growth capacity due to margin compression and constrained production flexibility.

Compliance requirements add another layer of cost pressure. GMP upgrades for HVAC, solvent recovery, and data integrity typically require USD 3 to 5 million per site over 3 to 5 years, discouraging full capacity utilization, often capped at 75 to 80 %, and limiting responsiveness to demand spikes.Industry response is gradually shifting toward hybrid manufacturing models, combining continuous processing, PAT enabled real time monitoring, and multi product platforms, to reduce cycle times by 20 to 30 % and improve yields. However, full modernization is likely to take 2 to 4 years, keeping legacy batch infrastructure a persistent near term constraint.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Aging batch API capacity | -1.0% | North America, EU, India | Medium term (2-4 years) |

| Quality & transparency burden | -0.9% | Global hospital channels | Medium term (2-4 years) |

| Legacy therapy positioning | -0.8% | North America, EU, Japan | Long term (≥ 4 years) |

| Volatile essential drug logistics | -1.1% | North America, EU, LMICs | Short term (≤ 2 years) |

| Skilled respiratory care gap | -0.7% | LMICs, rural high-income | Long term (≥ 4 years) |

Restraints

Shift to Inhaled Bronchodilators and Guideline Driven Constraint on Aminophylline

Asthma and COPD treatment pathways have progressively shifted toward inhaled therapies, short and long acting beta agonists, long acting muscarinic antagonists, and inhaled corticosteroids, as first line standards of care. As a result, aminophylline has been largely relegated to second line or adjunctive use in many guideline driven systems, limiting its clinical role despite rising global respiratory disease prevalence.

Evidence from COPD exacerbation trials showing limited incremental benefit and higher adverse event risk versus placebo has reinforced this positioning. At the same time, major public health efforts to expand access to essential inhaled medicines, especially in low resource settings, have further concentrated spending toward inhaled regimens.

In high income markets, roughly 70 to 80 % of maintenance bronchodilation expenditure is now directed to inhaled therapies.This shift reduces aminophylline utilization primarily to acute severe asthma settings requiring hospital oversight and intravenous administration, capping prescription volumes and narrowing its addressable market.

Although inhaled therapies may carry higher per dose pricing, they deliver better safety and lower downstream healthcare utilization, making them more favorable under cost effectiveness and reimbursement frameworks.Overall, the evolving guideline landscape and treatment mix shift likely reduce aminophylline growth potential by approximately 0.9 % points, with the strongest impact in North America, Western Europe, and advanced APAC markets where guideline adherence is highest.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Narrow therapeutic index & safety concerns | -1.3% | North America, EU, high-regulation APAC | Medium term (2-4 years) |

| Shift to inhaled bronchodilators & guidelines | -0.9% | Global, esp. OECD and tier-1 EMs | Long term (≥ 4 years) |

| Episodic injectable shortages & fragile manufacturing base | -0.8% | North America, EU, selective LMIC | Short–Medium term (≤ 4 years) |

| Tight hospital formulary & payer cost-containment | -1.0% | North America core, EU, GCC | Medium term (2-4 years) |

| Aging production assets & limited new CapEx | -0.7% | Global API corridors (India, China), EU | Long term (≥ 4 years) |

Opportunitys

Emergency Respiratory and Neonatal Care Bundles for Aminophylline

Aminophylline remains a niche therapy in acute hospital settings such as severe asthma, COPD exacerbations, and neonatal apnea, but its commercial role is constrained by fragmented procurement and low generic pricing. Today, it is typically used as part of broader emergency respiratory care rather than as a structured, protocol driven product, limiting its share of total episode level spending.

The opportunity lies in shifting from standalone drug sales to bundled, protocolized care packages. In this model, aminophylline is embedded within standardized hospital pathways that include dosing algorithms, monitoring protocols, staff training, and clinical decision support systems.

This allows manufacturers to reposition the product as part of a managed care solution rather than a commodity input.Such bundling can support 20 to 30 % price premiums by reducing variability and improving clinical consistency, while also increasing utilization by an estimated 25 to 35 % in participating hospitals.

Standardization improves inventory predictability and can lower logistics and working capital costs by 5 to 10 %, potentially improving EBIT margins by 200 to 300 basis points on these product lines.If adopted in roughly 10 to 15 % of tertiary hospitals across major regions by 2032, these bundled models could generate USD 300 to 500 million in incremental revenue and add approximately 1.2 % points to aminophylline market CAGR by 2035, compared with a purely transactional generic pricing model.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Cosmeto-medical cellulite & fat contouring | +2.0% | North America, EU, East Asia | Medium term (2-4 years) |

| Topical combination weight management | +1.5% | North America, EU, GCC, East Asia | Medium term (2-4 years) |

| Novel inhalation & IV delivery platforms | +1.8% | North America core, EU, APAC emerging | Long term (≥ 4 years) |

| Emergency respiratory & neonatal care bundles | +1.2% | North America, EU, LATAM, APAC | Short term (≤ 2 years) |

| Digital therapeutics–linked dosing optimization | +1.0% | North America, EU, Developed APAC | Long term (≥ 4 years) |

| Government-backed stockpiles & countermeasures | +1.0% | North America, EU, Selected APAC | Medium term (2-4 years) |

Geopolitical Impact Analysis

Tariff pressures and trade disruptions driving supply chain friction for generic molecules.

Tariff pressures and global trade disruptions are creating measurable supply chain friction across the aminophylline market, particularly affecting the economics of generic pharmaceutical manufacturing. As an off-patent molecule, Aminophylline relies heavily on globally distributed Active Pharmaceutical Ingredient (API) supply chains, with key upstream manufacturing hubs concentrated in Asia, especially China and India.

Any escalation in trade tensions or tariff structures increases input cost volatility, which can ultimately be transmitted through finished-dose manufacturers into hospital procurement systems that operate under tightly controlled budget frameworks.

In addition to trade-related cost pressures, broader geopolitical instability is reshaping pharmaceutical distribution networks across multiple regions. Disruptions in Eastern Europe and parts of Central Asia have altered established sourcing and logistics pathways, requiring suppliers to reconfigure distribution strategies for continuity of supply.

While these geopolitical developments do not fundamentally restrict market availability, they introduce persistent uncertainty in pricing, procurement planning, and long-term contracting. As a result, manufacturers and healthcare systems are increasingly prioritizing multi-source API procurement strategies and supply chain diversification to strengthen resilience and reduce exposure to regional trade shocks.

Regional Analysis

North America Held the Largest Share of the Global Aminophylline Market

In 2025, North America dominated the global Aminophylline market, holding about 47.2% of total global revenue at US$150.85 million. This leadership position is underpinned by the FDA-approved status of aminophylline for reversible airway obstruction confirming its continued regulatory standing and hospital formulary eligibility across U.S. and Canadian healthcare systems by NIH.

The United States maintains the world’s largest concentration of COPD and asthma patients. North America’s market share is expected to moderate gradually across the forecast period as clinical guideline evolution progressively reduces aminophylline’s use in high-income country COPD and asthma management protocols.

The Europe region represents the second largest regional market, due to its well-established hospital formulary status in Western Europe, as well as the ongoing utility in Eastern Europe despite lagging guidelines. The fastest growing regional market is the Asia Pacific region, fueled by increasing disease burden in China, India, and Southeast Asia, along with the cost benefits of aminophylline compared with expensive inhaled medications.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Global Aminophylline Market is characterised by a fragmented competitive structure with no single manufacturer commanding a dominant global share across all formulation types, geographies, and channel segments. Aminophylline is an off-patent, genericised molecule manufactured by a large number of branded and generic pharmaceutical companies across North America, Europe, India, and China.

At the branded product tier, Pfizer Inc., Bayer AG, and Merck KGaA maintain established positions through long-standing institutional formulary approvals and reference product status in hospital pharmacy procurement. Hikma Pharmaceuticals PLC a leading global injectable generics manufacturer with commercial operations across North America, Europe, and MENA confirmed continued strong injectables portfolio demand across its hospital channel in April 2026.

Indian manufacturers including Sun Pharmaceutical Industries, Cipla, Dr. Reddy’s Laboratories, Aurobindo Pharma, Amneal Pharmaceuticals, and Glenmark Pharmaceuticals represent the most cost-competitive manufacturing base globally, supplying both domestic Indian hospital demand and international export markets across Asia, Africa, and Latin America.

Sandoz AG (Novartis group generics), Teva Pharmaceutical Industries, and Hikma Pharmaceuticals compete across North American and European generic injectable and oral aminophylline segments. The overall market rewards manufacturing cost efficiency, regulatory approval breadth across multiple geographies, and hospital channel distribution capability competitive advantages available to both large multinational generics firms and smaller regional manufacturers.

Top Key Players

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Hikma Pharmaceuticals PLC

- Sandoz AG (Novartis group generics)

- Merck KGaA

- Bayer AG

- Sun Pharmaceutical Industries Ltd.

- Cipla Ltd.

- Reddy’s Laboratories Ltd.

- Amneal Pharmaceuticals LLC

- Aurobindo Pharma Ltd.

- Glenmark Pharmaceuticals Ltd.

- Omega Laboratories

- ACTIZA Pharmaceutical Pvt. Ltd.

- TORQUE Pharmaceuticals Pvt. Ltd.

- Others

Key Development

- March 2025 – Sun Pharmaceutical Industries Ltd. announced the acquisition of Checkpoint Therapeutics for approximately USD 355 million. The acquisition strengthens Sun Pharma’s innovative oncology portfolio and expands its specialty pharmaceutical business, reinforcing the company’s long-term strategy of broadening its global branded medicines pipeline.

- June 2026 – Pfizer Inc. entered into a strategic licensing and development agreement with Innovent Biologics valued at up to USD 10.5 billion. The collaboration focuses on advancing multiple oncology programs and reflects Pfizer’s continued investment in expanding its innovative drug development pipeline.

- In April 2025- Sandoz advanced its broader hospital and respiratory generics strategy after its spin‑off from Novartis, yet there were no announcements of collaborations, M&A, or launches focused specifically on aminophylline, which remains one of many mature injectable respiratory therapies in its catalog.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 319.6 Million |

| Forecast Revenue (2035) | US$ 393.4 Million |

| CAGR (2026-2035) | 2.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Indication (COPD, Asthma / Bronchial Asthma, Infant / Neonatal Apnea, Other Bronchospasm / Others), By Route (Parenteral, Oral Tablets / Capsules, Oral Solutions, Other Injectable Routes), By Product Type (Branded Aminophylline Products, Generic Aminophylline Products, API), By Channel (Hospital Pharmacies, Retail Pharmacies, Online, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Pfizer Inc., Teva Pharmaceutical Industries Ltd., Hikma Pharmaceuticals PLC, Sandoz AG (Novartis group generics), Merck KGaA, Bayer AG, Sun Pharmaceutical Industries Ltd., Cipla Ltd., Dr. Reddy’s Laboratories Ltd., Amneal Pharmaceuticals LLC, Aurobindo Pharma Ltd., Glenmark Pharmaceuticals Ltd., Omega Laboratories, ACTIZA Pharmaceutical Pvt. Ltd., TORQUE Pharmaceuticals Pvt. Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |