Quick Navigation

Report Overview

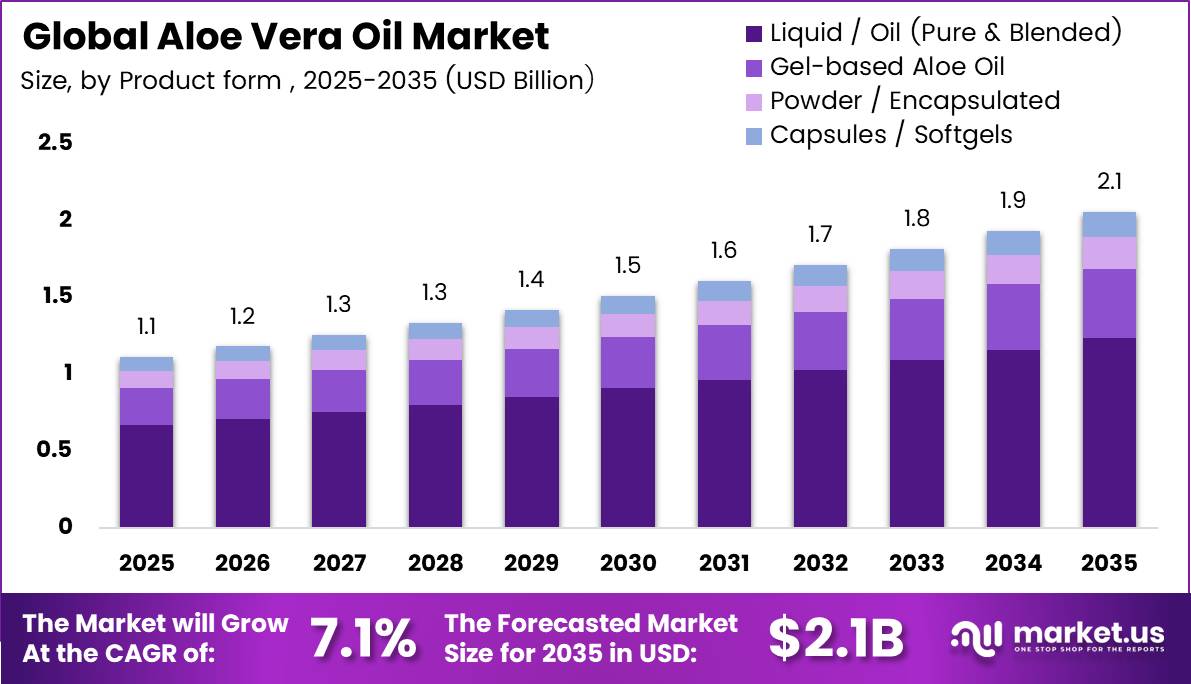

Global Aloe Vera Oil Market size is expected to be worth around USD 2.19 Billion by 2035 from USD 1.18 Billion in 2025, growing at a CAGR of 7.1% during the forecast period 2026 to 2035. This trajectory places aloe vera oil among the faster-growing botanical ingredient categories in personal care and wellness globally.

The aloe vera oil market encompasses liquid, gel-based, powdered, and encapsulated oil formats derived from Aloe barbadensis leaf. These formats serve cosmetics, pharmaceuticals, food and beverages, aromatherapy, and animal care end markets. Suppliers range from raw leaf processors to finished personal care formulators operating across conventional and certified organic supply chains.

Key Takeaways

- Aloe Vera Oil Market size in 2025 stands at USD 1.18 Billion, reaching USD 2.19 Billion by 2035 at a CAGR of 7.1%.

- Liquid/Oil (Pure and Blended) dominates the By Product Form segment with a 60.00% share.

- Conventional cultivation dominates the By Nature segment with a 65.00% share.

- Cosmetics and Personal Care dominates the By Application segment with a 35.00% share.

- Mid-Range pricing dominates the By Price Range segment with a 42.00% share.

- Bottles dominate the By Packaging Type segment with a 48.00% share.

- Offline channels dominate the By Distribution Channel segment with a 63.00% share.

- North America leads all regions with a 34.50% market share, valued at USD 0.382 Billion in 2025.

According to the National Center for Complementary and Integrative Health, aloe vera-derived ingredients see extensive use in topical skin care products for soothing and moisturizing applications. This positions aloe vera oil as a functional active, not a commodity filler. Formulators that build documented efficacy claims around soothing and moisturization unlock premium channel access and stronger buyer retention.

As reported by the NSF, aloe vera ingredients are widely incorporated across cosmetics, lotions, soaps, and personal care products under recognized commercial standards. This broad formulation footprint creates recurring procurement demand across multiple product categories. Brands that standardize aloe oil sourcing protocols reduce reformulation risk and gain supply chain predictability.

Data from USDA AMS shows certified organic personal care manufacturing is expanding its use of botanical ingredients including aloe vera. Simultaneously, the FDA has flagged regulatory restrictions on therapeutic and organic claims for aloe-based cosmetic products. This means compliance-ready aloe oil suppliers that align with USDA and FDA labeling guidance hold a structural sourcing advantage over undocumented competitors.

Product Form Analysis

Liquid / Oil (Pure and Blended) dominates with 60.00% due to versatile cosmetic and nutraceutical formulation compatibility.

In 2025, Liquid / Oil (Pure and Blended) held a dominant market position in the By Product Form segment of the Aloe Vera Oil Market, with a 60.00% share. This format serves the widest range of end-use applications, from facial serums and body oils to nutraceutical blends. The NSF confirms aloe vera ingredients are integrated into clean-label botanical personal care formulations across multiple product formats, reinforcing liquid oil’s broad commercial utility and consistent reformulation demand.

Gel-based Aloe Oil held a 22.00% share in the By Product Form segment. This format appeals to after-sun, soothing, and dermatological applications where texture and skin feel matter to end consumers. Brands targeting sensitive-skin or post-procedure recovery categories use gel-based formats to differentiate on sensory experience and position within dermocosmetic price tiers.

Powder / Encapsulated formats held a 10.00% share. This format serves nutraceutical manufacturers, functional food producers, and private-label supplement brands requiring stable, shelf-stable aloe actives. Encapsulation extends ingredient shelf life and simplifies dosing, making this format attractive for contract manufacturers supplying capsule and tablet production lines.

Capsules / Softgels held the remaining 8.00% share. This format addresses the ingestible wellness segment, including health drinks, nutraceutical capsules, and dietary supplement product lines. Brands in this tier face rising compliance demands for food-grade purity and traceability, which raises entry barriers but rewards suppliers holding credible certification documentation.

Nature Analysis

Conventional dominates with 65.00% due to broader leaf supply availability and lower unit cost.

In 2025, Conventional cultivation held a dominant market position in the By Nature segment of the Aloe Vera Oil Market, with a 65.00% share. This dominance reflects large-scale leaf sourcing from India, Latin America, and China where non-certified farming infrastructure is well established. USDA AMS data confirms that certified organic personal care manufacturing is expanding botanical ingredient use, which means conventional suppliers face intensifying competitive pressure from certified alternatives as premium brand demand shifts.

Organic / Certified Organic held the remaining 35.00% share. The NSF’s NSF/ANSI 305 standard governs organic ingredient requirements in personal care, and certification activity under this standard is increasing. Suppliers that achieve and maintain NSF/ANSI 305 compliance gain shelf access in premium EU, North American, and APAC channels that require auditable organic credentials as a base procurement requirement.

Application Analysis

Cosmetics and Personal Care dominates with 35.00% due to high-volume use across skincare, haircare, and color cosmetics.

In 2025, Cosmetics and Personal Care held a dominant market position in the By Application segment of the Aloe Vera Oil Market, with a 35.00% share. The NCCIH confirms aloe vera oil is widely positioned around skin-soothing and moisturizing benefits in commercial formulations. This positioning supports inclusion in moisturizers, face serums, after-sun gels, scalp treatments, and body oils, covering the full personal care product architecture and generating recurring ingredient procurement demand.

Pharmaceuticals and Healthcare represents the next significant application tier. This segment spans wound healing formulations, anti-inflammatory topical drugs, dermatological prescriptions, and OTC ointments. NSF’s organic personal care standards confirm expanded aloe vera oil applications in certified formulations including therapeutic-adjacent products, which signals growing pharmacy channel penetration for high-specification aloe oil grades.

Food and Beverages serves functional food ingredient, nutraceutical capsule, and health drink applications. This segment competes with the encapsulated product form tier and demands food-grade extraction and purity documentation. Brands entering this segment face higher compliance costs, but the recurring subscription nature of wellness supplement purchasing reduces demand volatility versus personal care.

Aromatherapy and Wellness, and Animal Care / Veterinary hold the remaining application share collectively. Aromatherapy covers massage oils, spa treatments, and diffuser blends. Animal care addresses pet grooming oils and veterinary topical applications. Both segments operate at lower volumes but provide margin diversification opportunities for suppliers seeking to reduce concentration risk in the cosmetics channel.

Price Range Analysis

Mid-Range (USD 10 to 30 / 100ml) dominates with 42.00% due to broad consumer accessibility and branded product alignment.

In 2025, Mid-Range pricing held a dominant market position in the By Price Range segment of the Aloe Vera Oil Market, with a 42.00% share. This tier captures the largest addressable consumer base across health and beauty retail, pharmacy, and online channels. Brands operating in this range balance quality positioning with mainstream price accessibility, making it the primary battleground for private-label and established natural brand competition.

Mass / Economy (Below USD 10 / 100ml), Premium (USD 30 to 60 / 100ml), and Ultra-Premium / Clinical Grade (Above USD 60 / 100ml) collectively hold the remaining share. Premium and Ultra-Premium tiers are smaller by volume but generate higher per-unit revenue. Clinical grade products targeting pharmacy and dermatologist channels command pricing power tied directly to documentation quality and compliance certifications.

Packaging Type Analysis

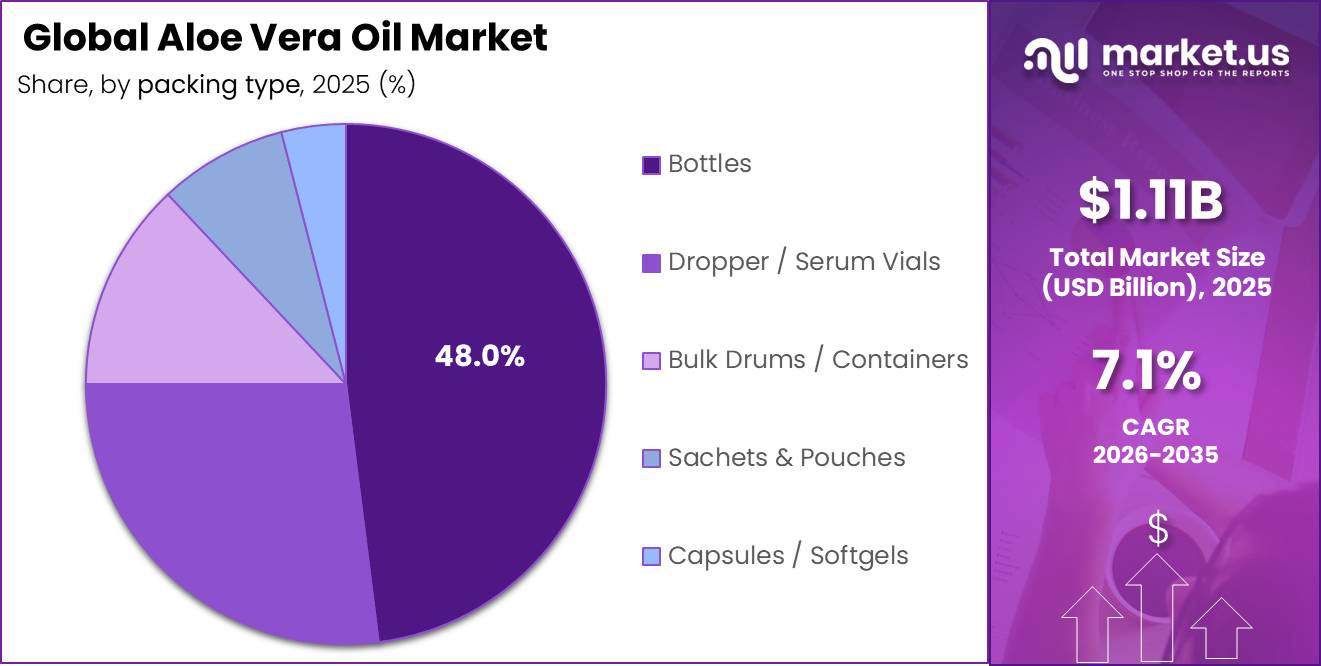

Bottles dominate with 48.00% due to consumer familiarity and compatibility across retail and online formats.

In 2025, Bottles held a dominant market position in the By Packaging Type segment of the Aloe Vera Oil Market, with a 48.00% share. Bottles serve both retail shelf display and e-commerce fulfillment requirements effectively. This format supports brand visibility on physical shelves while meeting dimensional and leak-resistance requirements for online distribution, giving it structural relevance across both the offline and online sales channels.

Dropper / Serum Vials held a 27% share. This format supports the premium serum and facial oil categories where precise dosing and clinical visual cues reinforce premium price positioning. Bulk Drums / Containers held 13%, serving B2B ingredient suppliers and contract manufacturers requiring large-volume inputs. Sachets and Pouches held 8%, while Capsules / Softgels held 4.00% as a packaging format for ingestible aloe products.

Distribution Channel Analysis

Offline dominates with 63.00% due to entrenched retail infrastructure across pharmacy, specialty, and supermarket channels.

In 2025, Offline held a dominant market position in the By Distribution Channel segment of the Aloe Vera Oil Market, with a 63.00% share. Supermarkets, specialty health and beauty stores, pharmacies, and spa and salon supply distributors collectively anchor offline volume. Institutional B2B sales to ingredient suppliers also contribute significantly. Products meeting NSF/ANSI 305 organic requirements gain preferential placement in specialty retail chains such as Holland and Barrett and GNC.

Online held a 37.00% share. Brand-owned D2C websites, e-commerce marketplaces including Amazon and iHerb, social commerce platforms, and subscription wellness services drive this segment. Online channels reduce geographic barriers for niche aloe oil brands and enable direct consumer relationships, which lower customer acquisition costs over time compared with wholesale-dependent offline distribution strategies.

Key Market Segments

By Product Form / Type

- Liquid / Oil (Pure and Blended)

- Gel-based Aloe Oil

- Powder / Encapsulated

- Capsules / Softgels

By Nature / Cultivation Method

- Conventional

- Organic / Certified Organic

By Application / End Use

- Cosmetics and Personal Care

- Skincare

- Moisturizers and face serums

- After-sun and soothing gels

- Anti-aging creams and lotions

- Body oils and massage oils

- Haircare

- Scalp treatments and hair oils

- Shampoos and conditioners

- Hair growth serums

- Color cosmetics (makeup base, primers)

- Nail care

- Skincare

- Pharmaceuticals and Healthcare

- Wound healing and burn treatment formulations

- Anti-inflammatory topical drugs

- Dermatological prescriptions

- OTC ointments and creams

- Food and Beverages

- Functional food ingredient

- Nutraceutical capsules and softgels

- Health drinks and smoothies

- Aromatherapy and Wellness

- Massage therapy oils

- Spa and wellness treatments

- Diffuser blends

- Animal Care / Veterinary

- Pet grooming oils

- Veterinary topical applications

By Price Range

- Mass / Economy (Below USD 10 / 100ml)

- Mid-Range (USD 10 to 30 / 100ml)

- Premium (USD 30 to 60 / 100ml)

- Ultra-Premium / Clinical Grade (Above USD 60 / 100ml)

By Packaging Type

- Bottles

- Dropper / Serum Vials

- Bulk Drums / Containers

- Sachets and Pouches

- Capsules / Softgels

By Distribution Channel

- Offline

- Supermarkets and Hypermarkets

- Specialty Health and Beauty Stores (Holland and Barrett, GNC)

- Pharmacies and Drug Stores

- Departmental Stores

- Spa and Salon Supply Distributors

- Institutional / B2B Sales (ingredient suppliers to manufacturers)

- Online

- Brand-owned D2C websites

- E-commerce marketplaces (Amazon, Flipkart, iHerb)

- Social commerce (Instagram, TikTok Shop)

- Subscription wellness platforms

Regional Analysis

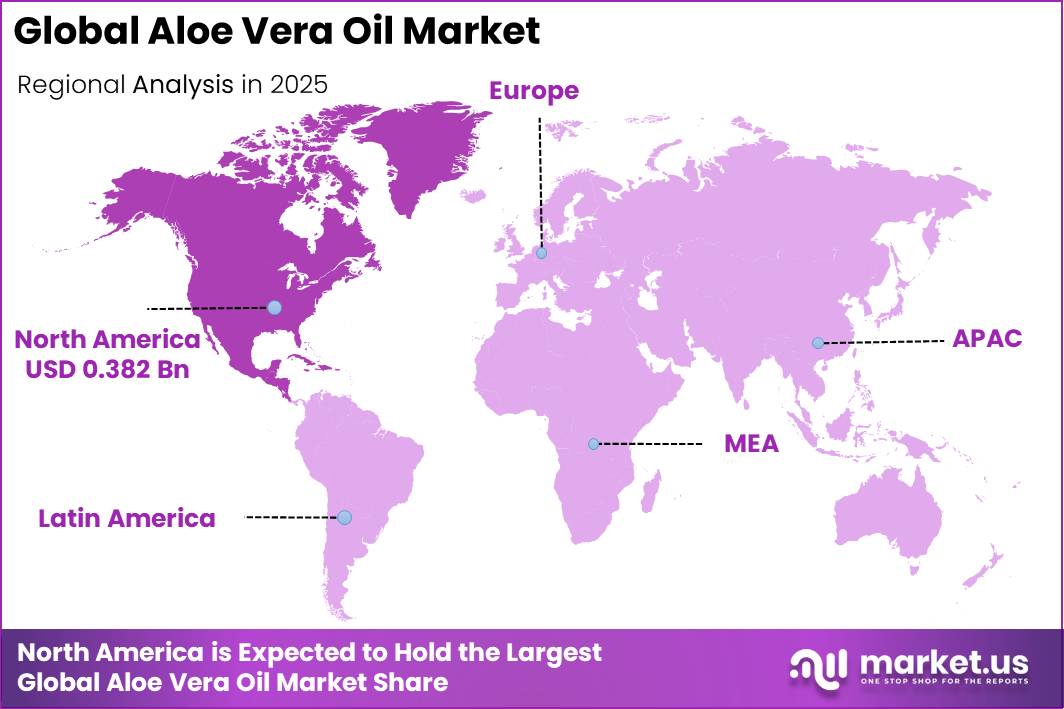

North America Dominates the Aloe Vera Oil Market with a Market Share of 34.50%, Valued at USD 0.382 Billion

North America holds the largest regional share at 34.50%, valued at USD 0.382 Billion in 2025. The United States drives this position through high consumer spending on natural personal care, established pharmacy retail infrastructure, and large-scale B2B ingredient procurement by multinational personal care manufacturers. Regulatory frameworks from the FDA and California Proposition 65 shape formulation choices and create compliance-driven differentiation among aloe oil suppliers serving this market.

Europe represents the second major regional market for aloe vera oil. EU cosmetic ingredient regulations, COSMOS certification requirements, and the microplastics phase-out actively push personal care brands toward documented botanical emollients including aloe oil. This regulatory pressure rewards suppliers with full traceability documentation and allergen screening, raising the cost of entry but lifting average selling prices for compliant aloe oil grades sold into European premium and mid-range channels.

Asia Pacific serves as both a major consumption market and the primary production base for aloe vera oil globally. China, India, Japan, and South Korea drive consumption across cosmetics, nutraceuticals, and functional food categories. India and China anchor leaf supply with large dryland cultivation areas supporting raw material availability for both domestic processing and export to European and North American buyers requiring volume at competitive leaf costs.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

Aloe vera oil demand is pulled by a broad reformulation cycle in beauty and personal care. Buyers now require natural-origin inputs with full technical dossiers covering origin, extraction method, contaminant screens, allergen statements, and stability data. CBI’s 2026 guidance explicitly requires CoA, SDS, traceability documents, microbiological testing, and at least one third-party efficacy or stability proof to accelerate buyer onboarding. This converts aloe oil from a simple botanical into a documentation-backed functional active.

This shift lifts unit economics in favor of suppliers selling standardized oil with anti-inflammatory, soothing, and moisturization claims into facial care, scalp oils, sun care, and body repair formats. Average selling price resilience improves and formulary penetration expands in premium channels. The effect is strongest in North America, Europe, and premium APAC beauty markets where procurement rewards auditable natural inputs over unverified low-cost substitutes.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label skincare substitution into aloe oil actives | +1.9% | North America core, EU core, APAC premium urban | Short term (≤ 2 years) |

| COSMOS/Ecocert traceability and audited natural-ingredient sourcing | +1.4% | EU core, UK, North America premium, Japan, South Korea | Medium term (2-4 years) |

| Microplastics phase-out lifting demand for botanical emollients and sensory substitutes | +1.2% | EU core, UK spill-over, developed APAC | Medium term (2-4 years) |

| Cultivation economics in India and other dryland belts supporting leaf availability | +1.0% | India core, Latin America supply base, Africa emerging | Short term (≤ 2 years) |

| Premiumization in scalp care, after-sun, and dermo-cosmetic formats | +1.6% | North America, EU, Gulf, APAC corridors | Short term (≤ 2 years) |

| Regulatory scrutiny on ingredient quality pushing refined, decolorized, specification-led oils | +0.9% | United States, EU, export-oriented APAC | Medium term (2-4 years) |

Restraints

Toxicology concerns around non-decolorized aloe whole-leaf extracts create risk aversion among large finished-product brands, especially in the United States. California Proposition 65 listed non-decolorized whole-leaf aloe following National Toxicology Program findings of intestinal tumors in rodents. Risk managers at multinational personal care and OTC brands apply conservative umbrella standards across entire ingredient families, triggering additional toxicology reviews and supplier qualification requirements for aloe-containing oil formulations.

This friction operates at three levels. Product-development lead times stretch by 3 to 6 months when aloe oil formulations require extra toxicology reviews. Large retailers may avoid complex aloe variants to minimize on-shelf Prop 65 warning label exposure. Internal portfolio reviews can redirect R&D budgets from aloe-centric lines toward lower-risk botanical oils such as jojoba, sunflower, or argan. This toxicology overhang can shave roughly 1.9 percentage points from achievable growth in North America and parts of the EU.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicology and Prop-65 overhang on aloe extracts | -1.9% | North America core, EU | Long term |

| Regulatory tightening in cosmetics actives | -1.4% | EU, UK, North America | Medium term |

| Volatile aloe leaf supply and farm-gate pricing | -1.6% | India, China, Mexico, LATAM, Africa | Short term |

| Quality variation and adulteration in aloe oil | -1.2% | APAC corridors, export hubs | Medium term |

| High refinement and compliance costs for food-grade oil | -1.0% | EU, North America, Japan | Long term |

| Slow innovation and limited differentiated IP in aloe oil formats | -0.8% | Global | Medium term |

Challenges

Aloe vera oil processing is heavily concentrated in small and mid-sized Asia-Pacific units running fragmented cold-press and infusion lines. These facilities typically operate at 45 to 65% utilization and below 2,000 to 3,000 tons per year of combined plant oil throughput. Batch changeover times of 4 to 8 hours for line sanitation and allergen risk controls can erase 10 to 15% of theoretical monthly capacity, compressing available output when global brand demand spikes.

International buyers now request multi-year contracts with minimum annual volumes of 50 to 300 tons of consistent-specification aloe oils. This forces brand owners to multisource from 5 to 10 suppliers instead of 2 to 3, stretching lead times by 5 to 10 days per order cycle. Strategic mitigation requires processing alliances that bring plant throughput to at least 8,000 to 10,000 tons per year and inline monitoring systems that can reduce batch rejection rates from 4 to 6% down to 1 to 2%.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile aloe leaf supply | -1.4% | India, China, Latin America | Medium term (2-4 years) |

| Fragmented cold-press capacity | -1.1% | Asia-Pacific processing hubs | Medium term (2-4 years) |

| Inconsistent oil quality specs | -0.9% | EU regulatory hubs, North America core | Long term (≥ 4 years) |

| Natural input cost swings | -1.2% | Global, esp. APAC and EU | Short term (≤ 2 years) |

| Regulatory and claims ambiguity | -0.8% | EU, North America, high-income APAC | Long term (≥ 4 years) |

| Limited formulation expertise | -0.7% | Emerging brands in APAC, LATAM, MEA | Medium term (2-4 years) |

Opportunities

Aloe vera oil today is sold predominantly as a generic natural emollient. The white space lies in repositioning it into microbiome-safe, barrier-repair dermacosmetics with clinically framed claims, premium pricing, and regimen-based recurring revenue. EU compliance is tightening on ingredient naming, allergens, and nanomaterial handling, raising barriers for undifferentiated sellers but creating pricing power for scaled brands that build compliant, dermatologist-backed platforms early.

A credible upside case of 200 to 300 basis points of faster category growth exists for companies that convert aloe oil from a single SKU ingredient play into a 4 to 6 SKU barrier line spanning cleanser, serum, scalp treatment, baby care, and post-procedure balm. Premium derma positioning can lift gross margins by roughly 800 to 1,200 basis points versus commodity personal care oils. The monetizable white space is strongest in the EU, US, Japan, and South Korea where early compliance adaptation before July 2026 INCI enforcement can create a 12 to 24 month shelf-access advantage.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Microbiome-led derma lines | +2.4% | EU, North America, Japan, South Korea | Short term |

| Ingestible beauty extensions | +2.1% | North America core, EU, China, Japan | Medium term |

| Clinical OTC adjacency | +1.7% | North America, EU, GCC, Australia | Medium term |

| Premium traceable sourcing | +1.5% | EU, UK, North America | Short term |

| Social commerce DTC acceleration | +1.9% | China, US, Southeast Asia, GCC | Short term |

| Roll-up of niche botanicals | +2.8% | EU, India, US, Latin America | Long term |

Key Company Insights

Forever Living Products International, Inc. built its market position on vertically integrated aloe cultivation, processing, and direct sales distribution across more than 160 countries. This vertical structure gives the company cost control from leaf to shelf. However, heavy reliance on a multi-level marketing distribution model creates brand perception risks in markets where regulatory scrutiny of MLM structures is rising, particularly the EU and China.

Aloecorp, Inc. operates as a dedicated aloe ingredient supplier focused on supplying standardized aloe vera raw materials to personal care, food, and nutraceutical manufacturers. The FDA has flagged regulatory restrictions on therapeutic and organic claims for aloe-based products, and NSF certification activity for organic personal care is increasing. Aloecorp’s ingredient-supplier positioning means it benefits when brand customers require compliant, documented aloe oil inputs to satisfy retailer and regulatory demands.

Key Players

- Forever Living Products International, Inc.

- Aloecorp, Inc.

- Terry Laboratories, Inc.

- Aloe Laboratories, Inc. (Harmony Green Co. Ltd.)

- Lily of the Desert

- Herbalife Nutrition Ltd.

- Patanjali Ayurved Limited

- Foodchem International Corporation

- Pharmachem Laboratories, Inc.

- NatureAloe (Natural Aloe Costa Rica S.A.)

- NOW Foods

- GOODMAN International (Aloe Vera Australia)

- Aloe Plus Lanzarote S.L.

- L’Oréal S.A. (La Roche-Posay / Garnier)

- Aloe Jaumave S.A. de C.V.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.18 Billion |

| Forecast Revenue (2035) | USD 2.19 Billion |

| CAGR (2026-2035) | 7.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Form / Type (Liquid / Oil Pure and Blended, Gel-based Aloe Oil, Powder / Encapsulated, Capsules / Softgels); By Nature / Cultivation Method (Conventional, Organic / Certified Organic); By Application / End Use (Cosmetics and Personal Care, Pharmaceuticals and Healthcare, Food and Beverages, Aromatherapy and Wellness, Animal Care / Veterinary); By Price Range (Mass / Economy, Mid-Range, Premium, Ultra-Premium / Clinical Grade); By Packaging Type (Bottles, Dropper / Serum Vials, Bulk Drums / Containers, Sachets and Pouches, Capsules / Softgels); By Distribution Channel (Offline, Online) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Forever Living Products International Inc., Aloecorp Inc., Terry Laboratories Inc., Aloe Laboratories Inc. (Harmony Green Co. Ltd.), Lily of the Desert, Herbalife Nutrition Ltd., Patanjali Ayurved Limited, Foodchem International Corporation, Pharmachem Laboratories Inc., NatureAloe (Natural Aloe Costa Rica S.A.), NOW Foods, GOODMAN International (Aloe Vera Australia), Aloe Plus Lanzarote S.L., L’Oréal S.A. (La Roche-Posay / Garnier), Aloe Jaumave S.A. de C.V. |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Aloe Vera Oil Market size was USD 283 Million by 2023, growing at a CAGR of 7.20%.

The Global Aloe Vera Oil Market size is growing at a CAGR of 7.20% during the forecast period from 2023 to 2032.

The Global Aloe Vera Oil Market size is expected to be worth around USD 567.2 Million by 2032 during the forecast period from 2023 to 2032.