Quick Navigation

Report Overview

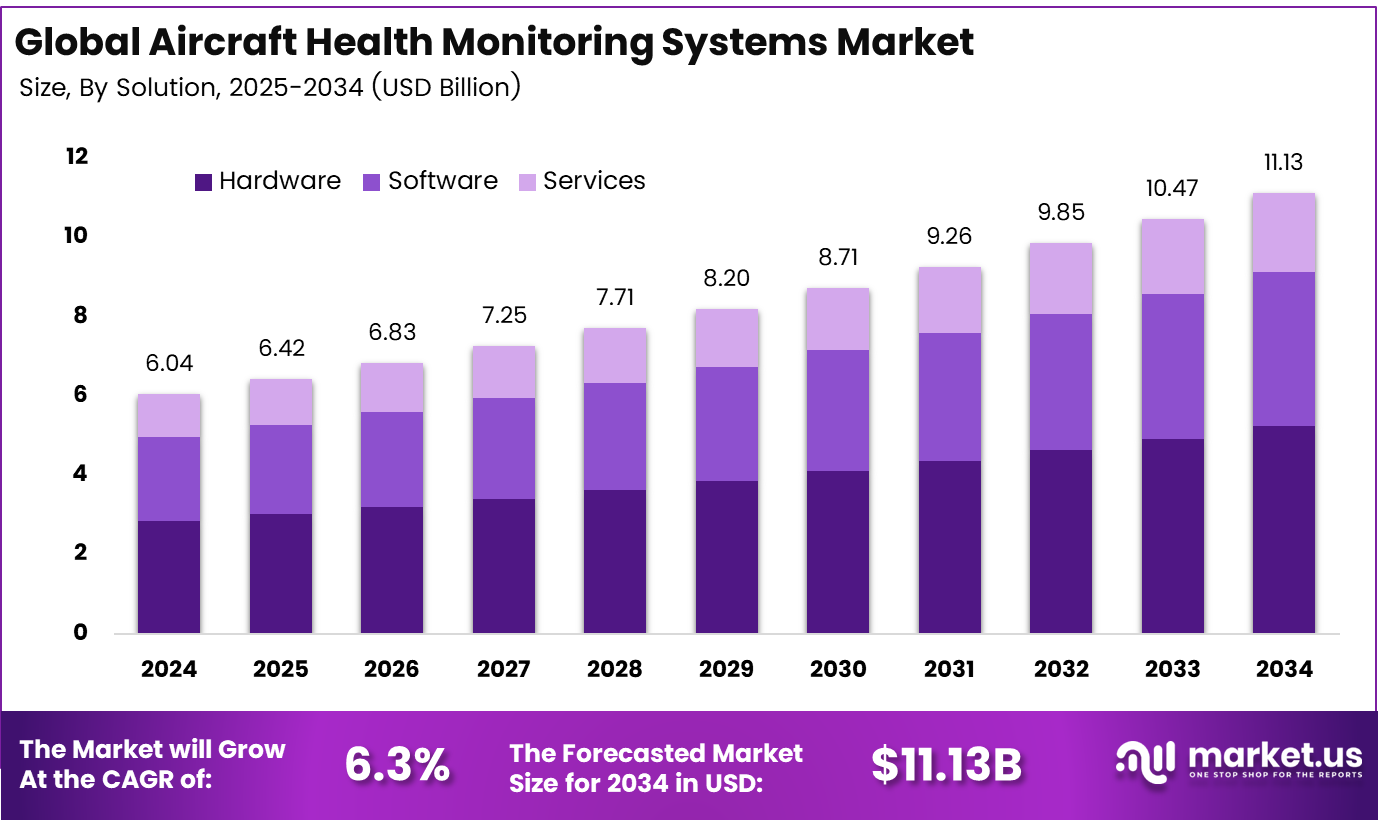

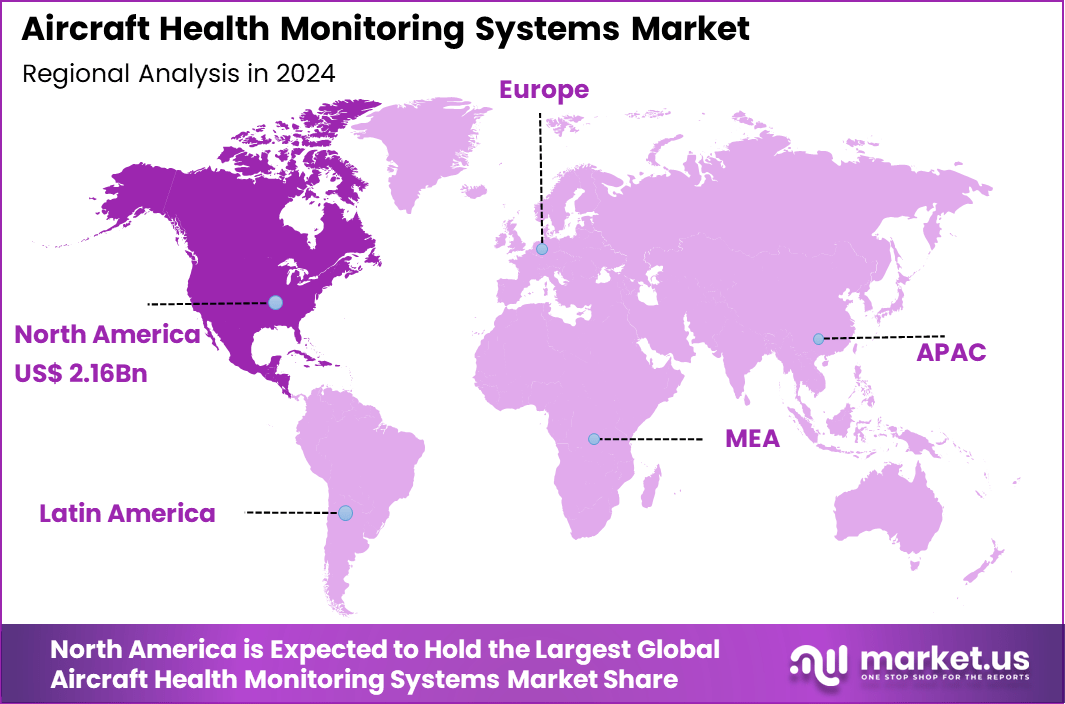

The Global Aircraft Health Monitoring Systems Market size is expected to be worth around USD 11.13 Billion By 2034, from USD 6.04 billion in 2024, growing at a CAGR of 6.3% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 36% share, with USD 2.17 billion in revenue.

The Aircraft Health Monitoring Systems (AHMS) market represents a dynamic and rapidly evolving sector within the aviation industry, focused on the real-time surveillance and management of an aircraft’s operational health. These systems are designed to collect, analyze, and transmit critical data related to the performance and condition of various aircraft components, enabling predictive maintenance and early fault detection.

By shifting maintenance programs from reactive to proactive frameworks, AHMS not only enhances operational efficiency but also significantly improves safety standards. This market growth is propelled by the increasing sophistication of modern aircraft, rising air traffic demands, and the critical need to minimize unscheduled downtime in the aviation sector.

Key drivers behind AHMS growth include escalating air traffic volumes and stringent safety regulations. The rising demand for predictive maintenance capabilities is prompting industry players to adopt real-time diagnostics and anomaly detection tools. Innovations in lightweight wireless sensors have further lowered integration barriers, enabling broader deployment of AHMS technologies.

Scope and Forecast

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.04 Bn |

| Forecast Revenue (2034) | USD 11.13 Bn |

| CAGR (2025-2034) | 6.3% |

| Largest market in 2024 | North America [36% market share] |

Key Insight Summary

- By solution, Hardware accounted for 47% share, highlighting strong demand for sensors and embedded monitoring devices.

- By installation, On-board systems dominated with 63% share, driven by the need for real-time data acquisition and analysis during flight operations.

- By system, Engine Health Monitoring led the market with 42% share, as engine reliability remains critical to safety and cost efficiency.

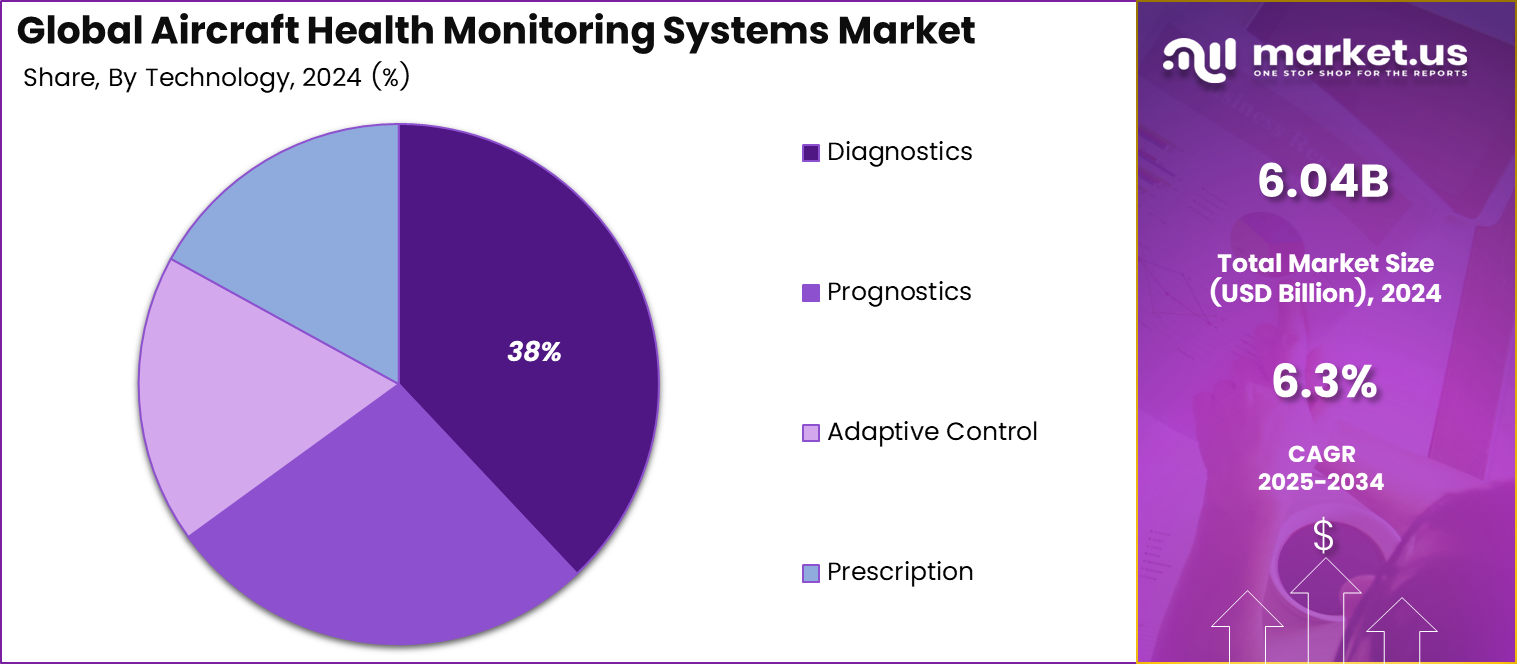

- By technology, Diagnostics held 38% share, reflecting its vital role in detecting faults and enabling timely corrective actions.

- By end-user, Airlines dominated with 52% share, underscoring their need to optimize fleet availability, reduce downtime, and improve safety compliance.

- In 2024, North America led the market with over 36% share, generating about USD 2.16 billion, supported by a large commercial and defense aircraft fleet and advanced maintenance infrastructure.

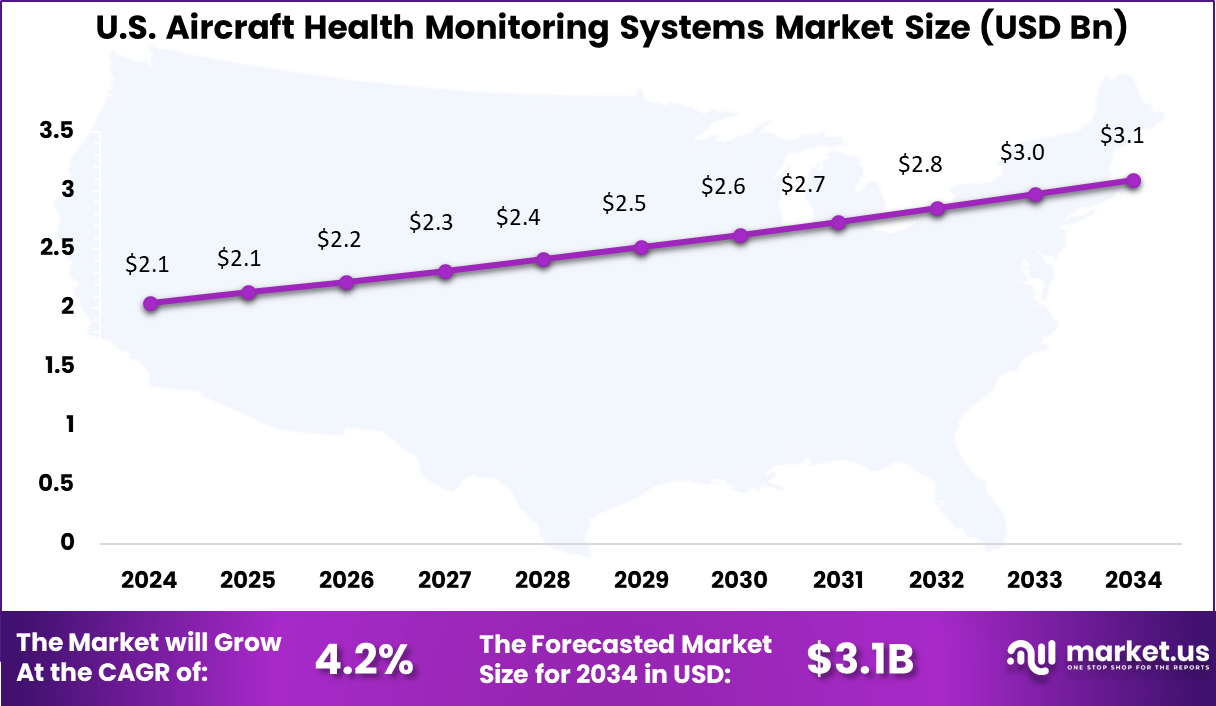

- The United States alone contributed nearly USD 2.05 billion, with a projected 4.2% CAGR, reflecting ongoing investments in fleet modernization and maintenance technologies.

Analysts’ Viewpoint

Technology adoption within the AHMS market is characterized by the integration of several advanced components. Artificial intelligence plays a central role by interpreting sensor data to detect anomalies and forecast potential component failures. Wireless sensor networks facilitate the continuous collection of high-volume data from varied aircraft systems, while cloud computing enables scalable data processing and analytics.

In particular, Integrated Vehicle Health Management (IVHM) systems, which unify data from engines, avionics, and structural components, exemplify this integration trend and drive deeper insights into aircraft health. These technological advancements not only elevate the capabilities of monitoring systems but also reduce operational costs by empowering airlines with actionable intelligence.

The key reasons behind adopting Aircraft Health Monitoring Systems extend beyond safety enhancements. Operators gain the ability to perform condition-based maintenance, which avoids unnecessary part replacements and reduces maintenance labor and inventory costs. Real-time health data allows for swift decision-making during flight, improving operational flexibility and reducing schedule disruptions.

Investment opportunities in the AHMS market are significant and multifaceted. The continuous growth of the global aviation fleet, combined with ongoing modernization efforts, ensures sustained capital demand for advanced health monitoring technologies. Opportunities exist in the development of AI-powered diagnostic tools, sensor innovations, and data analytics platforms tailored for aerospace applications.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 36% share and holding USD 2.16 billion in revenue. This leadership can be attributed to the region’s strong presence of commercial aviation operators and military aircraft programs, alongside stringent regulatory frameworks emphasizing real-time safety monitoring.

The Federal Aviation Administration (FAA) and related bodies have pushed for early fault detection systems and predictive maintenance technologies, making Aircraft Health Monitoring Systems (AHMS) an integral part of fleet operations. Additionally, the mature infrastructure and high investment in aerospace R&D in countries like the United States continue to support innovation in sensor technologies and data analytics for aircraft diagnostics.

US Market Size

The U.S. Aircraft Health Monitoring Systems Market was valued at USD 2.1 billion in 2024 and is anticipated to reach approximately USD 3.1 billion by 2034, expanding at a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2025 to 2034.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Solution Analysis

In 2024, The Hardware segment held a dominant market position, capturing a 47% share of the Global Aircraft Health Monitoring Systems Market. This dominance is due to the essential role hardware components, such as sensors, avionics, and diagnostic devices, play in collecting real-time data for aircraft health monitoring. These hardware components are crucial for monitoring critical aircraft systems, enabling early detection of faults and ensuring efficient performance. The growth in fleet modernization and the need for more accurate diagnostics further drive the demand for sophisticated hardware solutions.

For Instance, in February 2024, a new project focused on insulation monitoring for aircraft electrical systems was announced through CORDIS. The project aims to integrate advanced hardware solutions into Aircraft Health Monitoring Systems (AHMS) to ensure the reliability of electrical insulation in aircraft.

Installation Analysis

In 2024, the On-board segment held a dominant market position, capturing a 63% share of the Global Aircraft Health Monitoring Systems Market. This dominance is due to the growing need for real-time monitoring and diagnostics directly on the aircraft, allowing for immediate detection of potential issues and minimizing downtime. On-board systems enable continuous health checks of critical components during flight, enhancing safety and operational efficiency. The integration of advanced sensors and predictive maintenance technologies further supports the increasing reliance on on-board health monitoring solutions.

For instance, in March 2021, GPMS (Global Tracking and Monitoring Solutions) announced an STC (Supplemental Type Certificate) for its predictive health and usage monitoring system, Foresight MX, on the Bell 212 and 412 helicopters. This on-board installation of the Foresight MX system enables real-time monitoring of critical aircraft systems, providing predictive maintenance insights.

System Analysis

In 2024, the Engine Health Monitoring segment held a dominant market position, capturing a 42% share of the Global Aircraft Health Monitoring Systems Market. This dominance is due to the critical role engines play in aircraft safety and performance. It provides real-time data on engine conditions, allowing for early detection of anomalies and preventing potential failures. As airlines focus on reducing maintenance costs and improving operational efficiency, these systems offer significant value by enabling predictive maintenance and enhancing engine reliability.

For Instance, in September 2023, Airbus introduced its Skywise Health Monitoring (S.HM) system for the A220 aircraft, extending its digital health monitoring solutions across its commercial fleet. This cloud-based platform provides real-time monitoring and predictive maintenance capabilities, leveraging Airbus’s Skywise data platform.

Technology Analysis

In 2024, the Diagnostics segment held a dominant market position, capturing a 38% share of the Global Aircraft Health Monitoring Systems Market. This dominance is due to the increasing reliance on advanced diagnostic tools to monitor aircraft systems and identify potential issues. Diagnostic systems provide real-time insights into the health of various components, enabling early detection of faults and reducing the risk of unplanned maintenance. With the growing emphasis on safety, efficiency, and predictive maintenance, diagnostic technologies have become essential for optimizing aircraft operations.

For Instance, in May 2024, FLYHT Aerospace Solutions partnered with MBS Electronic Systems GmbH to enable a data loading solution that complies with new security requirements. This collaboration enhances FLYHT’s capabilities in real-time aircraft health monitoring and data management.

End-User Analysis

In 2024, the Airlines segment held a dominant market position, capturing a 52% share of the Global Aircraft Health Monitoring Systems Market. This dominance is due to airlines’ increasing focus on reducing operational costs, improving safety, and enhancing fleet management. The ability to implement predictive maintenance through AHMS allows airlines to minimize unscheduled downtimes, optimize maintenance schedules, and ensure the reliability of their aircraft fleets. As airlines continue to prioritize operational efficiency and cost reduction, the demand for advanced health monitoring systems has surged.

For Instance, in December 2023, Boeing highlighted enhancements to its Airplane Health Management (AHM) system, focusing on predictive maintenance capabilities. The system utilizes onboard sensors to capture data, analyze information remotely, and alert operators to potential issues, thereby optimizing maintenance schedules and reducing downtime.

Key Market Segments

By Solution

- Hardware

- Sensors

- Avionics

- Flight Data Management Systems

- Connected Aircraft Solutions

- Grund Servers

- Software

- Onboard Software

- Diagnostic Flight Data Analysis

- Prognostics Flight Data Analysis Software

- Services

By Installation

- On-board

- On-Ground

By System

- Engine Health Monitoring

- Structure Health Monitoring

- Component Health Monitoring

By Technology

- Diagnostics

- Prognostics

- Adaptive Control

- Prescription

By End-User

- Airlines

- OEMs

- MROs

Market Dynamics

Emerging Trend - AI & Machine Learning Integration

The most prominent shift occurring in the aircraft health monitoring sector stems from the adoption of artificial intelligence and machine learning. These technologies are transforming how aircraft maintenance is handled.

By processing massive amounts of sensor data collected during flights, predictive analytics can now flag performance anomalies and potential failures before they escalate. This leap to smart diagnostics is reducing both downtime and maintenance costs, fostering a move from reactive repairs to genuinely predictive maintenance strategies.

Driver - Demand for Predictive Maintenance

A core force behind the increasing use of aircraft health monitoring systems is the growing need for proactive, rather than reactive, maintenance methods. Airlines and operators are prioritizing safety, reliability, and efficiency as air traffic expands globally.

Predictive maintenance enabled by these systems lowers the risk of unexpected breakdowns, minimizes flight disruptions, and ensures passenger safety. The real-time insights derived from continuous monitoring allow for well-timed interventions, preventing costly issues before they affect operations.

Restraint -High Implementation Costs

The path to modern aircraft health monitoring is not without hurdles. One significant barrier is the high upfront cost of integrating advanced monitoring systems. These investments cover new sensors, digital platforms, system installations, and regular upgrades. For smaller operators or those with older fleets, this financial burden can slow or outright limit system adoption, especially since ongoing costs such as maintenance and staff training further add up.

Opportunity - Uptake in Predictive Maintenance for Drones

A fresh growth area is the application of health monitoring systems to unmanned aerial vehicles and drones. With their growing presence in commercial, defense, and public services, the need to ensure drone reliability and longevity is greater than ever.

Health monitoring technologies are evolving to provide lightweight, intelligent solutions for drones, supporting advanced diagnostics for missions in diverse and often challenging environments. This segment is primed for rapid development as regulations become stricter and operational volumes rise.

Challenge - Integrating with Legacy Aircraft

Many airlines operate fleets containing older aircraft that lack modern digital infrastructure. Retrofitting these planes with cutting-edge health monitoring systems poses technical and financial challenges.

Modifying existing structures to support new sensors and processing capabilities can be costly and complex, often resulting in project delays and compatibility issues. These integration problems make it difficult for operators to uniformly upgrade their fleets, thus limiting the full potential benefits of new monitoring technologies.

Key Player Analysis

Leading aircraft OEMs such as Airbus SE and The Boeing Company have played a central role in advancing aircraft health monitoring systems (AHMS). Their integration of real-time diagnostics and predictive analytics into new-generation aircraft has set benchmarks for the aviation industry. These players focus on digital twins, IoT integration, and smart maintenance alerts.

Prominent engine and avionics providers like GE Aviation, Rolls-Royce, and Collins Aerospace have invested in health monitoring solutions tailored for propulsion systems and critical aircraft components. These firms have enabled condition-based maintenance through sensors and cloud-based analytics.

Honeywell International Inc. and Meggitt PLC are also contributing to onboard diagnostics, enhancing fuel efficiency, and reducing unscheduled maintenance events. Their expertise in integrating software with legacy platforms continues to support fleet operators in meeting stringent safety and compliance standards.

Specialized solution providers such as FLYHT Aerospace Solutions Ltd, Curtiss-Wright Corporation, and Ultra Electronics Group offer advanced monitoring platforms that emphasize real-time data acquisition and fault detection. Meanwhile, Safran and Esterline Technologies Corporation are focusing on modular AHMS solutions compatible with civil and military aircraft. These players enhance situational awareness and contribute to quicker turnaround times for aircraft.

Top Key Players Covered

- Airbus SE

- The Boeing Company

- GE Aviation

- Collins Aerospace (United Technologies Corporation)

- Honeywell International Inc.

- Meggitt PLC

- Rolls-Royce

- FLYHT Aerospace Solutions Ltd

- Curtiss-Wright Corporation

- Safran

- Esterline Technologies Corporation

- Ultra Electronics Group

- Other Key Players

Recent Developments

- In March 2025, the European Defence Agency (EDA) initiated a research project focused on Prognostic Health Management (PHM) to monitor and predict the health of aircraft batteries. Targeting hybrid aircraft and UAVs, the project aims to extend battery lifespan and ensure reliable performance by forecasting safe usage limits and minimizing the risk of system failure.

- In April 2025, the Indian Air Force (IAF) invited industrial collaboration to develop a real-time in-flight health monitoring system, reinforcing its adoption of advanced technologies to protect aircrew in high-stress operational environments.

- In July 2024, Rolls-Royce finalized a TotalCare service agreement with Vietjet for 40 Trent 7000 engines powering 20 Airbus A330neo aircraft. Initially revealed during the Singapore Airshow in February, this agreement builds on Vietjet’s existing TotalCare support and shifts maintenance risk and time-on-wing accountability to Rolls-Royce, ensuring operational continuity.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.04 Billion |

| Forecast Revenue (2034) | USD 11.13 Billion |

| CAGR (2025-2034) | 6.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Solution (Hardware (Sensors, Avionics, Flight Data Management Systems, Connected Aircraft Solutions, Grund Servers), Software (Onboard Software, Diagnostic Flight Data Analysis, Prognostics Flight Data Analysis Software), Services), By Installation (On-board, On-Ground), By System (Engine Health Monitoring, Structure Health Monitoring, Component Health Monitoring), By Technology (Diagnostics, Prognostics, Adaptive Control, Prescription), By End-User (OEMs, Airlines, MROs) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Airbus SE, The Boeing Company, GE Aviation, Collins Aerospace (United Technologies Corporation), Honeywell International Inc., Meggitt PLC, Rolls-Royce, FLYHT Aerospace Solutions Ltd, Curtiss-Wright Corporation, Safran, Esterline Technologies Corporation, Ultra Electronics Group, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |