Global Aircraft Data Management Market Size, Share, Growth Analysis By Component (Hardware, Software), By Type (Flight Control, Engine Control, Utility Control, Others), By Aircraft (Fixed Wing, Rotary Wing, Unmanned Aerial Vehicle (UAV)), By End-User (Commercial, Military, Civil), By Point of Sale (OEM, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 184109

- Number of Pages: 370

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

Global Aircraft Data Management Market size is expected to be worth around USD 17.0 Billion by 2035 from USD 9.1 Billion in 2025, growing at a CAGR of 6.4% during the forecast period 2026 to 2035.

Aircraft data management covers the systems and software that capture, process, store, and transmit operational data across every phase of flight. This includes flight data recorders, engine health monitoring units, avionics data buses, and the ground-side platforms that turn raw telemetry into actionable maintenance and safety intelligence.

The market sits at the intersection of two structural forces: tightening regulatory mandates and the commercial pressure to reduce unscheduled maintenance costs. Airlines and defense operators no longer treat data management as a compliance checkbox. They treat it as a revenue-protection tool — one that directly determines aircraft availability and operational cost per seat mile.

Regulatory bodies on both sides of the Atlantic are accelerating this transition. EASA and FAA digital compliance rules now require structured data collection and audit-ready storage across commercial fleets. These mandates are not guidance — they carry certification consequences, which means operators must invest regardless of budget cycles.

Connected aircraft ecosystems now generate terabytes of data per flight across engine sensors, avionics systems, and cabin networks. The volume of data produced per aircraft has grown beyond what legacy ground data units can process efficiently, creating structural demand for cloud-based platforms and high-speed onboard recorders. On April 1, 2026, Airbus merged its Navblue navigation services unit with its Skywise digital platform to form a single end-to-end aviation digital services company — a signal that integrated data management is becoming a core product, not a peripheral one.

According to the IATA 2025 Annual Safety Report, released March 9, 2026, the global aviation accident rate improved to 1.32 accidents per million flights in 2025, down from 1.42 in 2024. Fatal accident probability also shifted from one in every 3.5 million flights between 2012–2016 to one in every 5.6 million flights between 2021–2025. This improvement is directly attributed to data-driven safety management — confirming that investment in aircraft data infrastructure produces measurable safety outcomes, not just operational efficiency gains.

According to EASA, over 92% of European operators above the regulatory FDMA threshold had implemented flight data monitoring systems by 2023. EASA now requires operators to collect 60–80% of flight data for safety audits, which is driving fleet-wide upgrades from legacy recorders to cloud-capable FDM platforms. This compliance pressure creates a predictable, recurring procurement cycle that benefits both OEM hardware suppliers and software analytics vendors.

Low-cost carrier expansion compounds this demand further. As LCC fleets scale across Asia Pacific and the Middle East, each new aircraft added to a managed fleet represents an incremental data management contract — for onboard hardware, ground analytics software, and integration services. The installed-base economics of this market strongly favor vendors with platform-level solutions over point-product suppliers.

Key Takeaways

- The global Aircraft Data Management Market was valued at USD 9.1 Billion in 2025 and is forecast to reach USD 17.0 Billion by 2035, at a CAGR of 6.4%.

- By Component, Hardware leads with a 62.5% market share, reflecting the installed-base dominance of onboard data acquisition and recording units.

- By Type, Flight Control systems hold the largest share at 38.1%, driven by mandatory digital compliance requirements for flight data recording.

- By Aircraft, Fixed Wing platforms account for 54.8% of the market, supported by large commercial airline fleets and regulatory mandates.

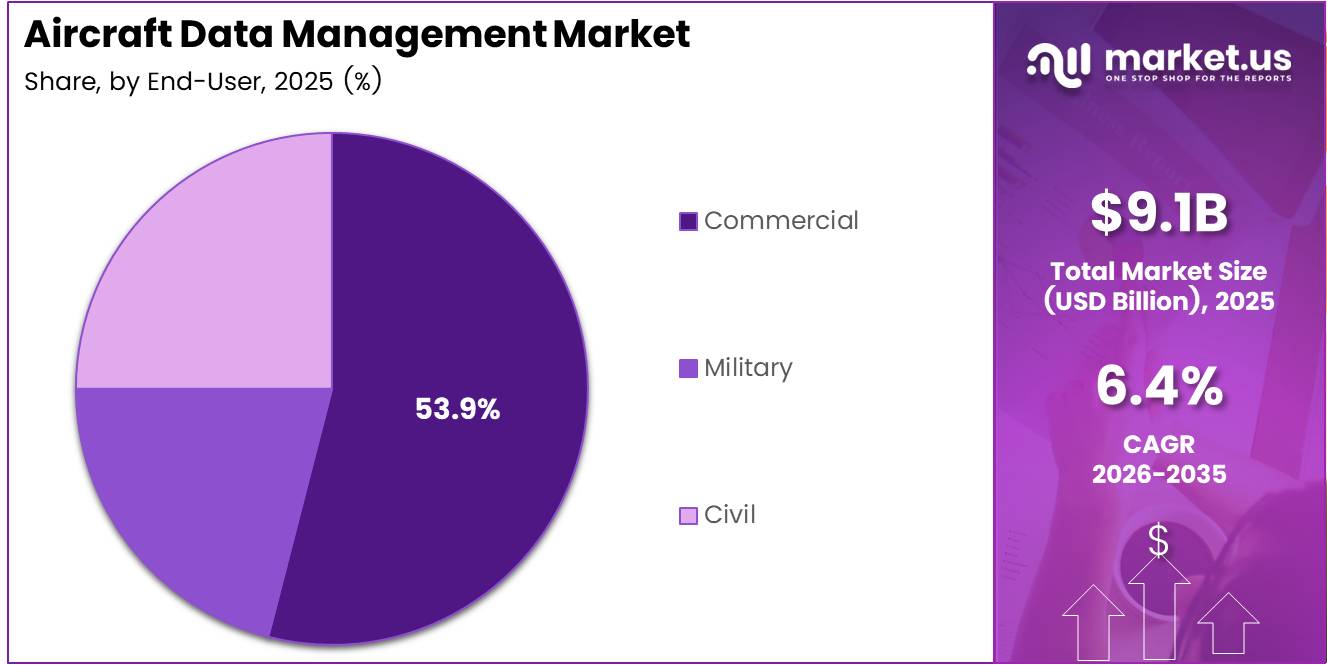

- By End-User, Commercial operators hold 53.9% share, as airline fleet expansion and FDMA compliance obligations drive consistent procurement.

- By Point of Sale, OEM channels represent 67.2% of market revenue, reflecting the preference for factory-integrated data management systems.

- North America dominates with a 43.50% share, valued at approximately USD 3.9 Billion, underpinned by FAA mandates and a mature aerospace procurement base.

Product Analysis

Hardware dominates with 62.5% due to mandatory onboard recording compliance requirements.

In 2025, Hardware held a dominant market position in the By Component segment of the Aircraft Data Management Market, with a 62.5% share. Onboard data acquisition units, flight data recorders, and cockpit voice recorders represent non-negotiable compliance items under FAA and EASA rules. This regulatory lock-in creates a durable revenue base that software vendors cannot displace — only augment.

Software carries the highest margin profile within this segment and serves as the primary vector for recurring revenue. Airlines increasingly invest in analytics platforms that translate raw recorder output into predictive maintenance triggers and fuel optimization signals. However, software adoption scales with fleet size, meaning growth concentrates among large network carriers and MRO integrators rather than smaller operators.

Type Analysis

Flight Control systems dominate with 38.1% due to mandatory digital flight data recording mandates.

In 2025, Flight Control systems held a dominant market position in the By Type segment of the Aircraft Data Management Market, with a 38.1% share. Regulatory requirements under FAA and EASA frameworks mandate structured data capture from flight control surfaces on all commercial aircraft. This positions flight control data management as a baseline procurement item across every new aircraft delivery and major retrofit program.

Engine Control data systems serve as the primary input layer for predictive maintenance pipelines. Engine health monitoring generates the highest data density of any aircraft subsystem, making it the segment most directly linked to MRO cost reduction programs. Airlines running advanced engine analytics consistently report lower time-on-wing loss and fewer unscheduled removals, which raises the commercial case for engine data investment.

Utility Control data management covers hydraulics, pneumatics, electrical systems, and environmental controls. This segment differentiates through integration complexity — utility systems span multiple suppliers and aircraft generations, making standardized data collection technically demanding. Operators managing mixed fleets face the highest integration costs in this category.

Others in the By Type segment encompasses cabin systems, navigation data, and communications logging. According to the British Journal of Multidisciplinary Studies (April 2025), airlines implementing digital twin technology across multiple data types documented maintenance cost reductions averaging 28.5%, with operational availability rising up to 37.2% for wide-body aircraft. This finding underscores the value of treating multi-type data as a unified input rather than managing each system in isolation.

Aircraft Analysis

Fixed Wing aircraft dominate with 54.8% due to large commercial fleet volumes and compliance obligations.

In 2025, Fixed Wing aircraft held a dominant market position in the By Aircraft segment of the Aircraft Data Management Market, with a 54.8% share. Commercial narrowbody and widebody fleets represent the largest installed base for data management hardware and software. Each aircraft delivers a multi-decade data management revenue stream — from OEM installation through successive avionics upgrades and recorder replacements.

Rotary Wing platforms serve specialized defense, offshore energy, and emergency services operators with distinct data requirements. Rotorcraft generate vibration-intensive operational profiles that place unique demands on data acquisition hardware. Defense procurement cycles and long platform lifespans create retrofit opportunities as aging helicopter fleets migrate from legacy data units to digital systems.

Unmanned Aerial Vehicle (UAV) platforms represent the fastest-expanding aircraft category for data management investment. UAV data requirements differ structurally from manned aircraft — real-time telemetry, mission data logging, and regulatory compliance for BVLOS operations all demand dedicated data management architectures. As civil and defense UAV fleets scale, this segment will absorb an increasing share of software and edge-computing investment.

End-User Analysis

Commercial operators dominate with 53.9% due to fleet scale and mandatory FDMA compliance obligations.

In 2025, Commercial operators held a dominant market position in the By End-User segment of the Aircraft Data Management Market, with a 53.9% share. Airline fleet expansion — particularly among low-cost carriers in Asia Pacific and the Middle East — multiplies data management procurement at scale. Each new aircraft added to a managed fleet generates incremental hardware, software, and integration spending across the asset’s operational life.

Military end-users prioritize data security, mission-specific data acquisition, and compliance with defense airworthiness standards. Military procurement cycles differ from commercial aviation — contracts tend to be larger, longer-term, and tied to specific platform programs. The Curtiss-Wright HSDR-2512 high-speed Ethernet recorder, introduced in December 2024 with capacity for up to 180 terabytes of flight test data, reflects the data intensity demands emerging from advanced defense flight test programs.

Civil aviation — covering business jets, air ambulance, and government transport — occupies a distinct buyer profile. These operators require data management solutions scaled to smaller fleet sizes and lower regulatory complexity than commercial carriers. However, increasing adoption of EASA-aligned safety frameworks in civil aviation is narrowing the gap between civil and commercial compliance requirements.

Point of Sale Analysis

OEM channels dominate with 67.2% due to factory-integration preference and certification efficiency.

In 2025, OEM channels held a dominant market position in the By Point of Sale segment of the Aircraft Data Management Market, with a 67.2% share. Aircraft manufacturers and Tier 1 avionics integrators embed data management systems during production, giving operators a certified, fully integrated solution from day one. This dramatically reduces the cost and schedule risk of post-delivery integration — a strong structural incentive that sustains OEM channel dominance across fleet types.

Aftermarket channels serve retrofit demand across aging fleets that require upgrades to meet new regulatory recording standards. The FAA’s 25-hour cockpit voice and flight data recording mandate creates a finite but high-value retrofit wave across the existing U.S. commercial and business aviation fleet. Aftermarket vendors that hold multiple type certifications across major aircraft families hold a structural advantage in capturing this wave before it consolidates around a small number of approved suppliers.

Key Market Segments

By Component

- Hardware

- Software

By Type

- Flight Control

- Engine Control

- Utility Control

- Others

By Aircraft

- Fixed Wing

- Rotary Wing

- Unmanned Aerial Vehicle (UAV)

By End-User

- Commercial

- Military

- Civil

By Point of Sale

- OEM

- Aftermarket

Drivers

FAA and EASA Digital Compliance Mandates Force Fleet-Wide Data Infrastructure Upgrades

Regulatory bodies are no longer setting advisory targets for flight data management — they are enforcing structural compliance obligations. Over 75 major U.S. airlines participated in the FAA’s Flight Operational Quality Assurance (FOQA) program as of 2024, contributing to a 42% reduction in serious incidents over the past decade. This outcome demonstrates that mandated data collection directly translates into measurable safety performance — reinforcing the regulatory case for continued program expansion.

EASA’s requirements compel operators to collect between 60 and 80% of flight data for safety audits, which effectively forces airlines running older recording infrastructure to upgrade to cloud-capable FDM platforms. These are not discretionary budget decisions — non-compliance carries certification consequences that ground aircraft. This dynamic creates a structurally inelastic demand cycle for hardware suppliers and data platform vendors operating in certified aviation environments.

In November 2024, Honeywell and Curtiss-Wright jointly launched the Connected Recorder-25, a cockpit voice and flight data recorder built specifically for compliance with the FAA’s new 25-hour recording mandate. The product initially targeted Boeing 737, 767, and 777 aircraft, with Airbus A320-family certification planned for the first half of 2025. A compliance deadline driving two major suppliers to co-develop a dedicated product confirms the commercial scale of this regulatory demand wave.

Restraints

Non-Standard Data Formats and Retrofit Costs Create Integration Barriers Across Mixed Fleets

Aircraft data management faces a fundamental interoperability problem. Different OEMs output flight data in proprietary formats that are not natively compatible with centralized airline analytics platforms. Carriers operating mixed fleets — which includes most major global airlines — must either invest in expensive format translation middleware or accept fragmented data visibility across their fleet. Neither outcome supports the seamless data pipelines that predictive maintenance requires.

The cost of retrofitting older aircraft with modern digital data units compounds this barrier. Delta Air Lines’ APEX program demonstrated the scale of what deferred investment costs an airline: maintenance-related cancellations fell from over 5,600 annually in 2010 to just 55 — a reduction of approximately 99% — after targeted fleet-wide modernization. The savings were substantial, but reaching that outcome required sustained capital commitment over multiple years, a threshold that constrains smaller carriers and regional operators.

For airlines operating aircraft types older than 15 years, hardware retrofit projects frequently encounter airframe structural constraints that limit sensor placement and data bus access. These physical limitations force engineering workarounds that increase project cost and timeline. Combined with the integration complexity of multi-OEM fleets, this creates a two-tier market where large network carriers accelerate digitization while smaller fleets lag — limiting the total addressable market for advanced analytics vendors in the near term.

Growth Factors

Digital Twin Platforms and Cloud Analytics Unlock New MRO Revenue Streams and Retrofit Demand

Digital twin adoption is producing economics that compress the business case for aircraft data investment. According to IJMRET (2025), digital twin technology decreases unplanned downtime by an average of 35% — approximately 7.5 hours per 1,000 flying hours — and cuts annual maintenance expenditures by USD $200,000 to $250,000 per aircraft, with 92% predictive accuracy in failure detection. These figures reframe data management from an operating cost to a capital-efficient asset protection tool.

Cloud-based flight data monitoring enables real-time airworthiness analytics that were previously impossible under ground-only data transfer architectures. Airlines that migrate to cloud-native FDM platforms gain the ability to trigger maintenance actions while aircraft are still in flight, reducing turnaround time at destination airports. Qantas demonstrated the revenue scale of this capability — integrating FDMA with real-time alert systems reduced engine failure incidents by 15% and generated AI-assisted fuel savings of approximately USD $92 million annually.

Blockchain-based traceability systems represent an adjacent growth vector within MRO supply chains. Counterfeit aircraft parts remain a structural cost and safety risk for operators globally. Blockchain ledgers that link component provenance to flight data records reduce the verification burden on MRO providers and create a defensible audit trail for regulators. This application draws on the same data infrastructure that supports flight monitoring — extending the return on investment for airlines that have already built structured data pipelines.

Emerging Trends

Satellite Broadband, Edge Computing, and AI Interfaces Redefine How Aircraft Generate and Deliver Data

Satellite broadband connectivity is displacing legacy ACARS systems as the primary channel for high-volume flight data offload. ACARS bandwidth constraints — designed for short text transmissions — cannot support the data volumes that modern avionics, engine sensors, and cabin systems generate per flight. Satellite L-band and Ka-band networks now offer the throughput required to transfer operational data in near real-time, enabling ground teams to act on flight data before aircraft arrive at the gate.

Edge computing onboard aircraft is shifting data processing from the ground to the aircraft itself. Rather than transmitting raw sensor streams for ground-side analysis, onboard processing units now filter, compress, and flag anomalies before transmission. Delta Air Lines’ FDMA deployment — which analyzes data from over 100,000 flights annually and has driven a 15% reduction in unscheduled maintenance on its Airbus A350 fleet — illustrates the operational value of combining onboard intelligence with cloud-scale analytics platforms. According to IATA’s 2025 Annual Safety Report, GNSS jamming events impacting aircraft rose 67% in 2025 compared to 2023, while GPS spoofing incidents increased 193%. These threat vectors make onboard anomaly detection — not just ground-side analysis — a functional safety requirement, not an optional upgrade.

Natural language interfaces for pilot access to technical aircraft logs represent an early but structurally significant trend. Pilots and ground engineers currently retrieve maintenance data through menu-driven avionics interfaces that were not designed for rapid fault interrogation. NLP-based query tools that surface relevant log entries in plain language reduce diagnostic time and lower the skill barrier for first-line maintenance checks. Aircraft health management systems that integrate multi-sensor data from engines, airframe, and avionics into a single coherent view are the enabling architecture for these interfaces — and are now entering service across newer widebody platforms.

Regional Analysis

North America Dominates the Aircraft Data Management Market with a Market Share of 43.50%, Valued at USD 3.9 Billion

North America holds a 43.50% share of the global Aircraft Data Management Market, valued at USD 3.9 Billion in 2025. The FAA’s FOQA program, 25-hour recording mandate, and established defense procurement infrastructure create a dense, compliance-driven demand base. The concentration of major OEM suppliers, MRO integrators, and avionics technology developers in the U.S. further reinforces this region’s structural advantage in both revenue capture and product development.

Europe Aircraft Data Management Market Trends

Europe represents the second-largest regional market, supported by EASA’s mandatory FDMA compliance framework, which had achieved over 92% operator adoption by 2023. Germany, France, and the UK concentrate the majority of European aerospace manufacturing and MRO activity, creating co-located supply and demand for data management solutions. EASA’s ongoing push to expand data collection requirements is driving cloud platform upgrades across the European carrier base.

Asia Pacific Aircraft Data Management Market Trends

Asia Pacific delivers the strongest fleet-growth dynamics of any region, as low-cost carrier expansion in India, Southeast Asia, and China multiplies the installed base of aircraft requiring data management systems. Each new aircraft entering service in this region represents a long-duration data management revenue opportunity. IndiGo’s FDMA deployment across its fleet, which achieved a 25% improvement in pilot behavior monitoring, illustrates the operational maturity emerging among leading Asia Pacific carriers.

Middle East and Africa Aircraft Data Management Market Trends

The Middle East operates some of the world’s largest wide-body fleets through Gulf carriers, creating concentrated demand for engine health monitoring and flight data analytics on long-haul operations. Africa’s commercial aviation sector is at an earlier stage of regulatory alignment with ICAO data management standards, but growing bilateral safety agreements are accelerating compliance investment. OEM-channel installations dominate procurement in both sub-regions due to the prevalence of new-aircraft orders over retrofit programs.

Latin America Aircraft Data Management Market Trends

Latin America’s aircraft data management market reflects a mix of fleet renewal and regulatory catch-up dynamics. Brazil and Mexico anchor regional demand through their national carriers and growing LCC sectors, while smaller markets are at earlier stages of FDMA implementation. Regional aviation authorities are progressively aligning with ICAO Safety Management System standards, which will expand compliance-driven procurement across the region’s mid-tier carrier base over the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Honeywell International Inc. occupies a uniquely integrated position in this market, supplying both the onboard data acquisition hardware and the ground-side analytics platforms that airlines use to act on that data. This vertical footprint means Honeywell benefits from procurement at both the OEM installation stage and subsequent software upgrade cycles. Its co-development of the Connected Recorder-25 with Curtiss-Wright demonstrates the company’s strategy of anchoring compliance-driven hardware upgrades to its broader connected aircraft software ecosystem.

RTX Corporation approaches aircraft data management through its Collins Aerospace division, which integrates avionics systems, data concentrators, and flight management computers across commercial and military platforms. RTX’s strength lies in platform-level integration — its avionics systems are embedded in aircraft that will generate data management revenue for decades. This long-duration installed-base exposure makes RTX less dependent on short-cycle procurement and more aligned with the steady replacement and upgrade economics of the market.

Thales Group competes through a combination of flight data monitoring software, avionics integration, and cybersecurity capabilities — a combination that positions it well as aircraft connectivity increases the data security surface area. Thales serves both commercial and defense operators globally, giving it regulatory exposure across EASA, FAA, and bilateral aviation authority frameworks simultaneously. This multi-jurisdiction compliance capability reduces the geographic concentration risk that affects smaller vendors in this space.

BAE Systems plc focuses its aircraft data management capabilities primarily on defense platforms, where data security, mission-specific acquisition standards, and long platform lifespans create a distinct competitive environment from commercial aviation. BAE’s defense orientation insulates it from commercial airline budget cycles while exposing it to defense appropriations risk. Its positioning in flight test instrumentation and military aircraft health management systems aligns directly with the growing defense UAV and next-generation combat aircraft data requirements emerging across NATO member nations.

Key Players

- Honeywell International Inc.

- RTX Corporation

- Thales Group

- BAE Systems plc

- Safran SA

- General Electric Company

- Curtiss-Wright Corporation

- Saab AB

- Leonardo S.p.A.

- Elbit Systems Ltd.

- L3Harris Technologies, Inc.

- Mercury Systems, Inc.

- Avidyne Corporation

- Northrop Grumman Corporation

- General Dynamics Corporation

Recent Developments

- March 2025 — Curtiss-Wright won a $50 million contract from the U.S. Naval Air Systems Command to supply high-speed data acquisition systems and flight test instrumentation products for the Special Flight Test Instrumentation Pool. Work runs through January 2030, establishing a long-duration revenue line in defense flight test data management.

- December 2024 — Curtiss-Wright introduced the HSDR-2512 airborne high-speed Ethernet data recorder, capable of storing up to 180 terabytes of flight test data at 16.5 gigabytes per second across twelve 10 Gigabit Ethernet inputs. The product targets the most demanding aerospace flight test environments where legacy recorders cannot meet data throughput requirements.

- April 1, 2026 — Airbus merged its Navblue navigation services division with its Skywise digital platform to form a unified end-to-end aviation digital services company. The Skywise platform has connected almost 12,000 aircraft since its 2017 launch, and the merger positions Airbus to offer integrated navigation, fleet operations, and predictive maintenance data services through a single commercial offering.

- 2024 — IndiGo Airlines implemented flight data monitoring and analysis across its full fleet, achieving a 25% improvement in pilot behavior monitoring and stronger compliance with standard flight parameters. The deployment demonstrates how FDMA investment at scale translates into measurable safety and operational performance outcomes for high-frequency, high-cycle LCC operations.

- 2024 — Lufthansa Technik’s use of FDMA insights reduced Aircraft on Ground (AOG) events by 20% while contributing fuel savings of up to 5%, per an IATA operational safety report. This outcome confirms that data-driven MRO decisions deliver both reliability and fuel economics simultaneously — a dual return that strengthens the investment case for FDMA platform upgrades across European MRO operators.

- April 2025 — A field study of 180 commercial aircraft equipped with digital twin technology found that predictive maintenance algorithms achieved 92.5% accuracy in identifying component failures an average of 18.7 days in advance. The study, published in the British Journal of Multidisciplinary Studies, documented an 84.6% reduction in AOG incidents compared to equivalent fleets operating without digital twin capability.

Report Scope

Report Features Description Market Value (2025) USD 9.1 Billion Forecast Revenue (2035) USD 17.0 Billion CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Hardware, Software), By Type (Flight Control, Engine Control, Utility Control, Others), By Aircraft (Fixed Wing, Rotary Wing, Unmanned Aerial Vehicle (UAV)), By End-User (Commercial, Military, Civil), By Point of Sale (OEM, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Honeywell International Inc., RTX Corporation, Thales Group, BAE Systems plc, Safran SA, General Electric Company, Curtiss-Wright Corporation, Saab AB, Leonardo S.p.A., Elbit Systems Ltd., L3Harris Technologies, Inc., Mercury Systems, Inc., Avidyne Corporation, Northrop Grumman Corporation, General Dynamics Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Aircraft Data Management MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Aircraft Data Management MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Honeywell International Inc.

- RTX Corporation

- Thales Group

- BAE Systems plc

- Safran SA

- General Electric Company

- Curtiss-Wright Corporation

- Saab AB

- Leonardo S.p.A.

- Elbit Systems Ltd.

- L3Harris Technologies, Inc.

- Mercury Systems, Inc.

- Avidyne Corporation

- Northrop Grumman Corporation

- General Dynamics Corporation

Our Clients

- 184109

- Apr 2026