Quick Navigation

Report Overview

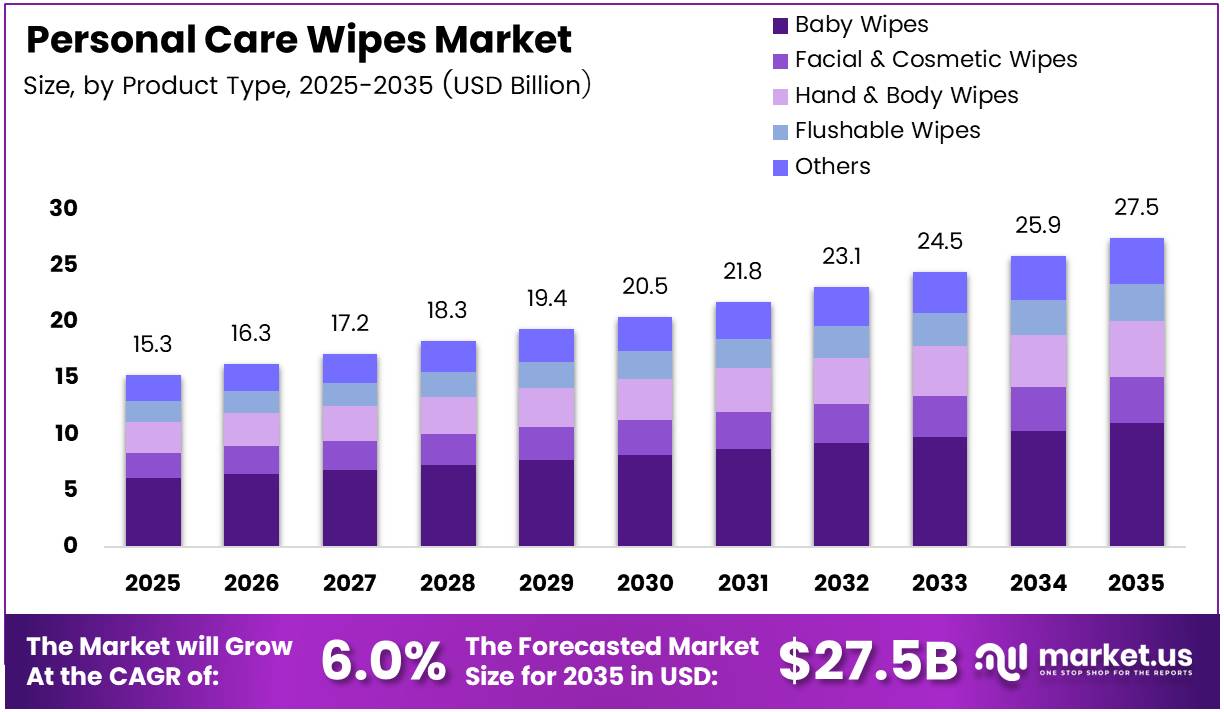

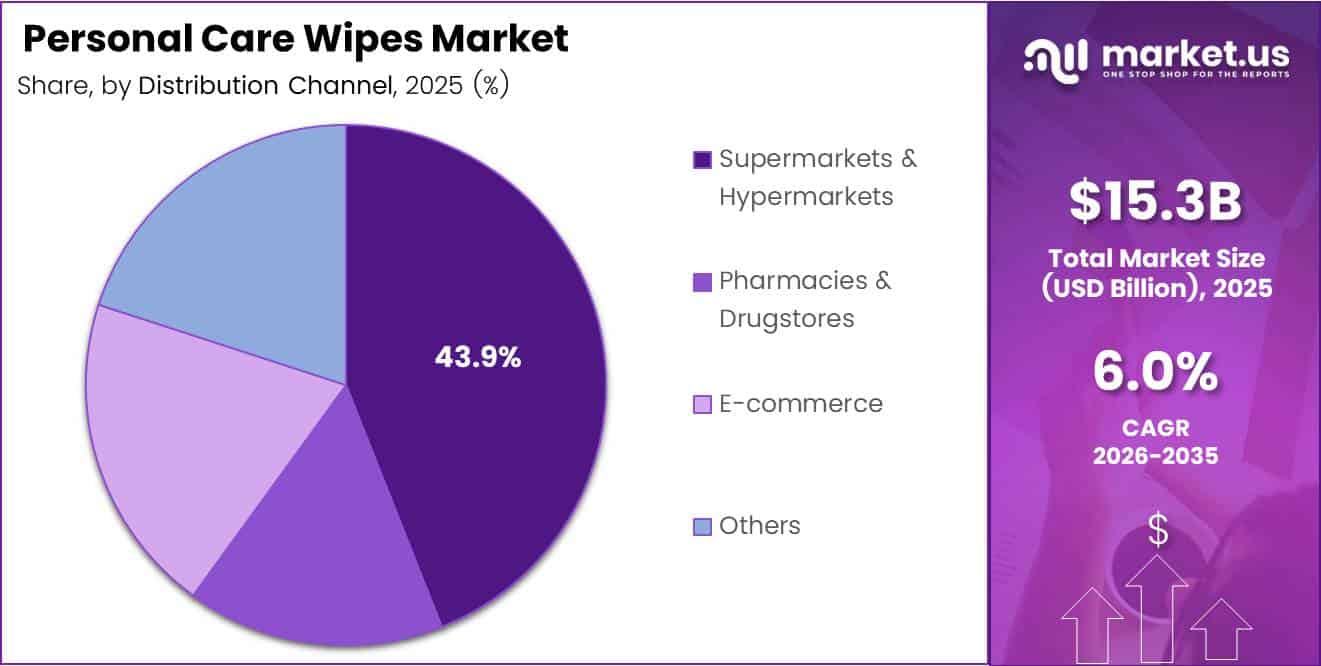

Global Personal Care Wipes Market size is expected to be worth around USD 27.5 Billion by 2035 from USD 15.3 Billion in 2025, growing at a CAGR of 6.0% during the forecast period 2026 to 2035.

Personal care wipes are pre-moistened, single-use nonwoven fabric sheets designed for hygiene, skincare, and cleansing purposes. The product range spans baby wipes, facial wipes, hand and body wipes, and flushable varieties. This breadth of application across age groups and use occasions gives the market a structural resilience that few single-category hygiene products can match.

Urban consumers increasingly treat wipes as a daily essential rather than a convenience backup. Busy commute routines, post-gym hygiene, and travel-format lifestyles have expanded per-capita consumption beyond traditional baby care contexts. This behavioral shift broadens the total addressable market well beyond the infant segment and reduces the market’s historical dependency on birth-rate trends.

Supermarkets and hypermarkets capture 43.9% of distribution, anchoring the market in high-footfall retail channels where impulse and repeat purchases drive volume. However, e-commerce is reshaping replenishment behavior, particularly for subscription formats. Brands that establish direct-to-consumer channels early will carry pricing power and loyalty advantages that shelf-based competitors cannot easily replicate.

Baby wipes lead with 39.7% product share, reflecting persistent caregiver demand for dermatologically safe, dermatologist-tested formulations. However, the facial and cosmetic wipes sub-segment is drawing investment from skincare brands entering the format, which signals a premiumization pathway that could rebalance category margins over the forecast period.

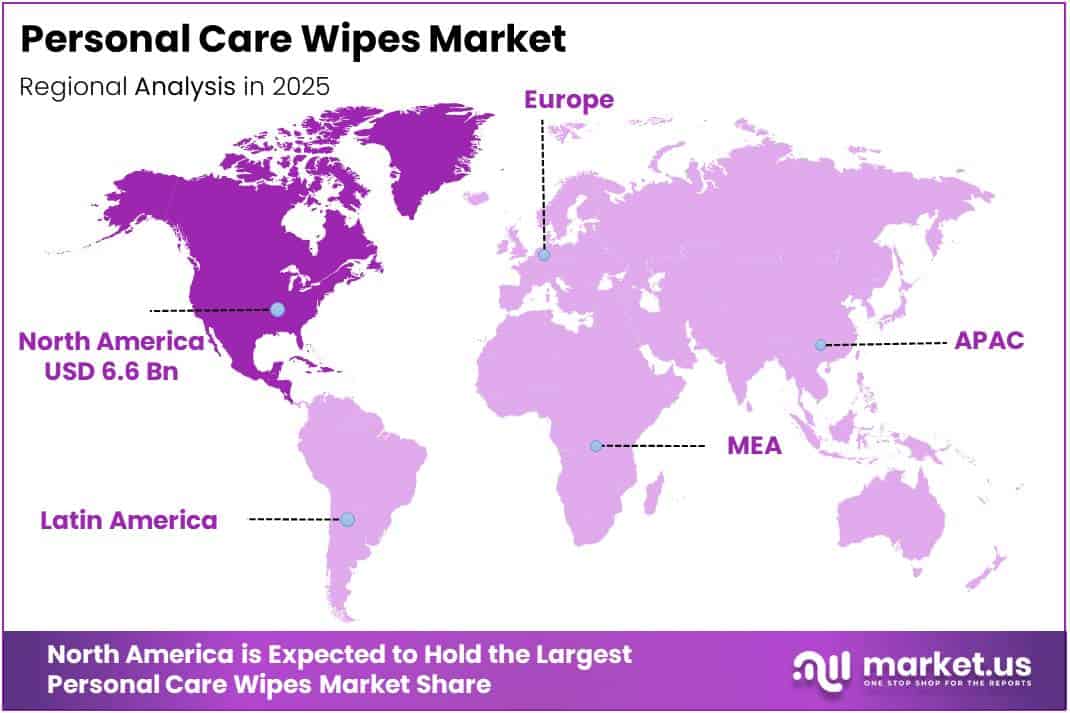

North America holds 43.7% market share, valued at USD 6.6 Billion, supported by mature retail infrastructure and established consumer habits around portable hygiene. In June 2025, TSG Consumer Partners provided a strategic growth investment to Dude Wipes, signaling that institutional capital views the North American market as still underserved in adult personal care formats.

According to a 2025 review published by RWTH Aachen University, approximately 70% of 64 global companies in the diaper and wipe sectors had integrated sustainable practices, including raw material selection, efficiency improvements, and circular economy models. This figure confirms that sustainability has moved from brand positioning to operational standard — companies that have not yet restructured their supply chains face rising compliance and reputational risk.

According to RSC Publishing, on average, 1 gram of wipe can release 56 microfibers into the environment. This data point is reshaping regulatory conversations across Europe and North America, where single-use plastics legislation is tightening. Manufacturers that proactively shift to plant-based and biodegradable fiber blends stand to gain first-mover advantage as compliance thresholds harden across key markets.

Key Takeaways

- The Global Personal Care Wipes Market was valued at USD 15.3 Billion in 2025 and is forecast to reach USD 27.5 Billion by 2035.

- The market is forecast to expand at a CAGR of 6.0% from 2026 to 2035.

- By Product, Baby Wipes lead with a 39.7% market share in 2025.

- By Distribution Channel, Supermarkets and Hypermarkets hold the dominant share at 43.9% in 2025.

- North America dominates the regional landscape with a 43.7% share, valued at USD 6.6 Billion in 2025.

Product Analysis

Baby Wipes dominates with 39.7% due to persistent caregiver demand for dermatologist-tested formulations.

In 2025, Baby Wipes held a dominant market position in the By Product segment of the Personal Care Wipes Market, with a 39.7% share. Caregivers consistently prioritize safety credentials over price, which compresses private-label competition and sustains premium brand pricing. In April 2025, RAAN launched its TruCotton 100% unbleached cotton hypoallergenic baby wipes, reinforcing this safety-led positioning trend.

Facial and Cosmetic Wipes serve as the primary entry point for skincare brands expanding into convenience formats. This sub-segment attracts ingredient-led innovation — vitamin-infused, botanical-extract, and micellar formulations — that commands higher retail price points. Consequently, facial wipes carry stronger gross margins than commodity body wipes and attract disproportionate R&D investment from personal care majors.

Hand and Body Wipes differentiate through functional positioning in workplace, gym, and travel contexts. Their growth relies less on demographic trends and more on behavioral adoption — specifically, the normalization of portable hygiene beyond traditional bathroom settings. This positions hand and body wipes as a volume-growth lever tied to urbanization and mobility patterns rather than population growth.

Flushable Wipes carry the highest regulatory risk within the product portfolio. Multiple countries are tightening flushability certification requirements amid sewer infrastructure concerns. However, Coterie’s June 2025 launch of The Flush Wipe — a certified flushable baby wipe — demonstrates that compliant, premium-positioned products can still access this sub-segment profitably under evolving standards.

Others within the product category — including intimate wipes, antibacterial wipes, and specialty wellness formats — represent the most fragmented sub-segment. However, this fragmentation signals an early-stage premiumization opportunity. Niche positioning around specific skin conditions or lifestyle occasions allows smaller brands to avoid direct competition with category leaders on volume and price.

Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 43.9% due to high-footfall impulse and repeat purchase behavior.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Personal Care Wipes Market, with a 43.9% share. Physical retail visibility drives trial purchases, and the category’s position in personal care aisles alongside complementary hygiene products reinforces basket-building. This channel dominance also gives large-format retailers leverage in shelf-space negotiations with wipe manufacturers.

Pharmacies and Drugstores serve as the trust channel for clinically positioned and sensitive-skin formulations. Consumers purchasing dermatologist-recommended or hypoallergenic variants specifically seek pharmacy endorsement. Therefore, this channel holds structural importance for premium sub-segments — particularly baby wipes, facial wipes, and medicated personal care variants — where healthcare credibility justifies higher price positioning.

E-commerce is restructuring replenishment behavior across the category, particularly for households with young children and for subscription-format products. The channel reduces friction in bulk purchasing and enables direct-to-consumer margin capture. Moreover, digital shelf analytics allow brands to monitor real-time conversion data and adjust product-page content in ways traditional retail cannot support.

Others — including convenience stores, travel retail, and institutional procurement — serve high-velocity, low-consideration purchase occasions. Convenience and travel formats support premium per-unit pricing through pack-size reduction. Institutional channels, covering hospitality and healthcare settings, represent a structurally distinct buyer with volume-driven, specification-led procurement behavior that differs fundamentally from consumer retail dynamics.

Key Market Segments

By Product

- Baby Wipes

- Facial & Cosmetic Wipes

- Hand & Body Wipes

- Flushable Wipes

- Others

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drugstores

- E-commerce

- Others

Drivers

Urban Hygiene Habits and Multipurpose Formulations Accelerate Personal Care Wipes Adoption

Urban consumers no longer treat personal care wipes as a situational backup. Rising awareness of skin health across city populations has repositioned wipes as a daily hygiene staple for commuters, gym users, and office workers. This behavioral normalization expands consumption frequency per household, which directly supports volume growth at the category level.

Manufacturers have responded by developing multipurpose formulations that combine makeup removal, body cleansing, and skin conditioning in a single product. This convergence reduces purchase hesitation by delivering cross-category value. According to RSC Publishing, average microfiber release from personal care wipes accounts for 26–27 mg g⁻¹ of wipes — a figure now driving R&D investment toward cleaner fiber blends that sustain performance while reducing environmental load.

The expansion of skin-friendly, biodegradable ingredients further strengthens the purchase rationale for health-conscious consumers. Botanical actives, aloe vera, and plant-derived surfactants now feature across mass-market and premium product lines. This ingredient transparency signal aligns with broader clean-beauty demand and effectively extends the addressable consumer base beyond the traditional infant care buyer.

Restraints

Environmental Scrutiny of Non-Biodegradable Fibers Creates Compliance and Innovation Pressure

Non-biodegradable plastic fiber content in conventional wipes faces tightening disposal regulations across Europe, the UK, and parts of Asia Pacific. Regulatory restrictions on single-use hygiene products are compelling manufacturers to reformulate material inputs — a process that requires capital investment and supply chain restructuring that smaller producers cannot absorb quickly.

According to RSC Publishing, a single wipe sheet releases 693–1,066 particles when exposed to an aquatic environment. This figure gives regulators a concrete evidence base to justify restrictions, and it is already cited in EU single-use plastics policy discussions. The implication for market participants: brands without a credible biodegradable or flushable-certified product range face both regulatory and retail delisting risk within the forecast period.

Consumer backlash against wipe-related sewer blockages and marine plastic contamination has intensified media scrutiny. However, this pressure creates a bifurcated competitive dynamic — incumbents with R&D resources can convert compliance requirements into product differentiation, while value-segment producers face margin compression as raw material costs rise without corresponding pricing power to offset them.

Growth Factors

Eco-Conscious Innovation and Premium Skincare Integration Open High-Value Market Segments

Compostable and plant-based personal care wipes address the intersection of hygiene demand and environmental responsibility. Brands that achieve recognized compostability certification gain access to a consumer cohort willing to pay a meaningful premium over conventional alternatives. This pricing dynamic improves category margins and reduces the revenue dependency on high-volume, low-margin commodity formats.

Dermatologically tested wipes for sensitive skin represent a clinically credible product tier with strong repeat purchase behavior. Consumers with eczema, rosacea, or allergy-prone skin exhibit low price sensitivity and high brand loyalty once a product proves safe. According to PMC/NIH research, banana fiber nonwoven wet wipes achieved a wet tensile index of 8.59 N·m·kg⁻¹ in the machine direction — exceeding the typical baby wipe benchmark of 3.48 N·m·kg⁻¹ — demonstrating that next-generation plant-based substrates can outperform conventional materials on performance standards.

Travel-friendly mini packs and subscription-based replenishment models create recurring revenue streams that stabilize demand forecasting. In June 2025, Coterie launched The Flush Wipe, a certified flushable baby wipe — a move that confirms premium brands can address regulatory compliance and consumer convenience simultaneously. Subscription models also improve customer lifetime value metrics, a distinction that supports higher direct-to-consumer investment justified by better unit economics.

Emerging Trends

Natural Actives, Alcohol-Free Formulations, and Sustainable Packaging Redefine Wipe Product Standards

Alcohol-free and fragrance-free personal care wipes are gaining formulary preference among dermatologists and pharmacists. This shift reflects documented consumer concern about skin barrier disruption from harsh preservatives. Brands repositioning around alcohol-free credentials access both the sensitive-skin and pediatric segments simultaneously, effectively widening their addressable user base without creating separate SKUs.

The integration of natural extracts — aloe vera, chamomile, and green tea — is moving from a premium differentiation feature to a baseline consumer expectation in facial and cosmetic wipes. Simultaneously, antibacterial and antiviral claims are expanding the functional scope of everyday wipes beyond basic cleansing. According to RSC Publishing, viscose and pulp blended wipes achieve dispersibility of 80–90% within just 150–250 hours under storage conditions — a performance threshold that supports both flushability certification and environmental compliance goals for manufacturers reformulating toward biodegradable materials.

Sustainable packaging — including recyclable outer wraps and refillable formats — is emerging as a secondary purchase driver alongside product formulation. Retailers are actively prioritizing shelf space for wipe brands with verifiable sustainability credentials. Early movers that align packaging formats with retailer ESG commitments gain distribution advantages that compound over time through preferred supplier status and promotional shelf placement.

Regional Analysis

North America Dominates the Personal Care Wipes Market with a Market Share of 43.7%, Valued at USD 6.6 Billion

North America holds 43.7% of the global Personal Care Wipes Market, valued at USD 6.6 Billion in 2025. Mature retail infrastructure, high per-capita hygiene spending, and well-established baby care purchasing habits anchor this dominance. The region’s premium product acceptance also accelerates revenue growth ahead of pure volume trends, sustaining its leadership position even as other markets expand faster in unit terms.

Europe Personal Care Wipes Market Trends

Europe represents the most regulatory-complex operating environment in the global wipes market. EU single-use plastics directives and extended producer responsibility frameworks are compelling manufacturers to reformulate products and packaging at pace. However, this regulatory pressure simultaneously elevates product quality standards, creating barriers that protect compliant incumbents and raise entry costs for lower-specification imports.

Asia Pacific Personal Care Wipes Market Trends

Asia Pacific presents the highest volume expansion potential, driven by rising disposable incomes in China, India, and Southeast Asia and rapidly urbanizing middle-class populations. Per-capita wipe consumption in the region remains significantly below North American and European levels, indicating structural under-penetration. Local manufacturing scale and improving modern retail coverage are closing that gap faster than global macroeconomic conditions might suggest.

Latin America Personal Care Wipes Market Trends

Latin America’s wipes consumption is concentrated in Brazil and Mexico, where modern retail expansion has improved product accessibility in urban centers. However, currency volatility and import cost sensitivity create pricing challenges for premium global brands. Locally manufactured and private-label formats capture volume-oriented demand, while imported premium products serve a narrower but higher-margin urban consumer base.

Middle East and Africa Personal Care Wipes Market Trends

The Middle East and Africa market is bifurcated between GCC nations — where premium hygiene product adoption mirrors European spending patterns — and sub-Saharan Africa, where price accessibility drives purchasing decisions. GCC markets show particular receptivity to antibacterial and travel-format wipes aligned with high-mobility lifestyles. Retail modernization and e-commerce infrastructure development across both sub-regions will progressively expand formal market reach.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Edana operates as the industry’s primary standards-setting body for nonwovens and personal care wipes, positioning it as a structural influencer rather than a direct product competitor. Its role in defining flushability, dispersibility, and sustainability benchmarks means that regulatory and compliance decisions across the wipes sector are shaped by Edana’s technical frameworks. Manufacturers aligned with Edana standards carry a credibility advantage in retail and regulatory conversations.

Diamond Wipes International Inc. strengthened its product portfolio in May 2025 by acquiring certain assets and brands — including Care4 and Ally — from Guy & O’Neill. This move reflects a deliberate consolidation strategy: absorbing established brand equity and distribution relationships rather than building them organically. The acquisition signals Diamond Wipes’ intent to compete across multiple sub-segments simultaneously, reducing revenue concentration risk and increasing shelf footprint.

Medline Industries approaches the personal care wipes market through healthcare and institutional procurement channels, where specification-led buying decisions favor suppliers with clinical credibility and supply chain reliability. This positioning insulates Medline from direct consumer retail competition while securing high-volume, contract-based revenue streams. Its institutional focus also creates a natural adjacency into medical-grade hygiene formats, where margins exceed those of the mass consumer segment.

The Honest Company, Inc. built its competitive positioning on ingredient transparency and clean formulation credentials, targeting health-conscious parents in the baby wipes segment. This brand architecture commands a pricing premium over conventional private-label alternatives and aligns directly with the market’s shift toward dermatologically tested and botanical-ingredient formulations. However, scaling premium positioning without diluting brand trust represents the central tension in its growth strategy.

Key Players

- Edana

- Diamond Wipes International Inc.

- Medline Industries

- The Honest Company, Inc.

- Procter and Gamble Co.

- Edgewell Personal Care Co.

- Johnson & Johnson Services, Inc.

- Pluswipes

- Rockline Industries

- KCWWSkin Inc.

Recent Developments

- December 2024 — 3i Group plc agreed to invest approximately €145 million in WaterWipes UC, signaling strong institutional confidence in premium, natural-ingredient baby wipes and validating the segment’s ability to attract significant growth capital at scale.

- May 2025 — Diamond Wipes International acquired certain assets and brands including Care4 and Ally from Guy & O’Neill, expanding its sub-segment coverage through brand consolidation rather than organic development, and strengthening its multi-category retail presence.

- August 2025 — Vivos Holdings completed its combination with Nice-Pak Products, creating a combined entity with broader manufacturing capabilities and an expanded portfolio across personal care and household wipe formats, reflecting ongoing industry consolidation at the production level.

- June 2025 — Dude Wipes launched LiL’ DUDE Wipes exclusively at Walmart, extending its adult personal care brand equity into the children’s segment and securing a major mass-retail exclusive that provides immediate national distribution scale and consumer trial exposure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 15.3 Billion |

| Forecast Revenue (2035) | USD 27.5 Billion |

| CAGR (2026-2035) | 6.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Baby Wipes, Facial & Cosmetic Wipes, Hand & Body Wipes, Flushable Wipes, Others), By Distribution Channel (Supermarkets & Hypermarkets, Pharmacies & Drugstores, E-commerce, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Edana, Diamond Wipes International Inc., Medline Industries, The Honest Company Inc., Procter and Gamble Co., Edgewell Personal Care Co., Johnson & Johnson Services Inc., Pluswipes, Rockline Industries, KCWWSkin Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |