Quick Navigation

Report Overview

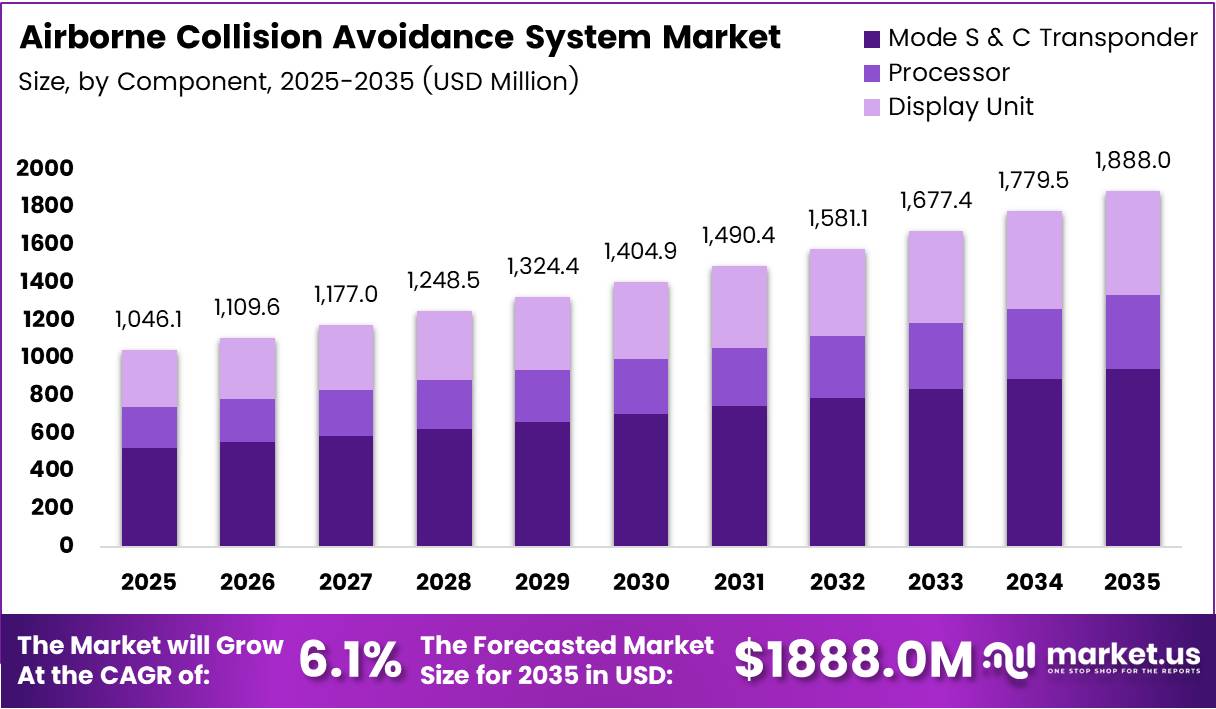

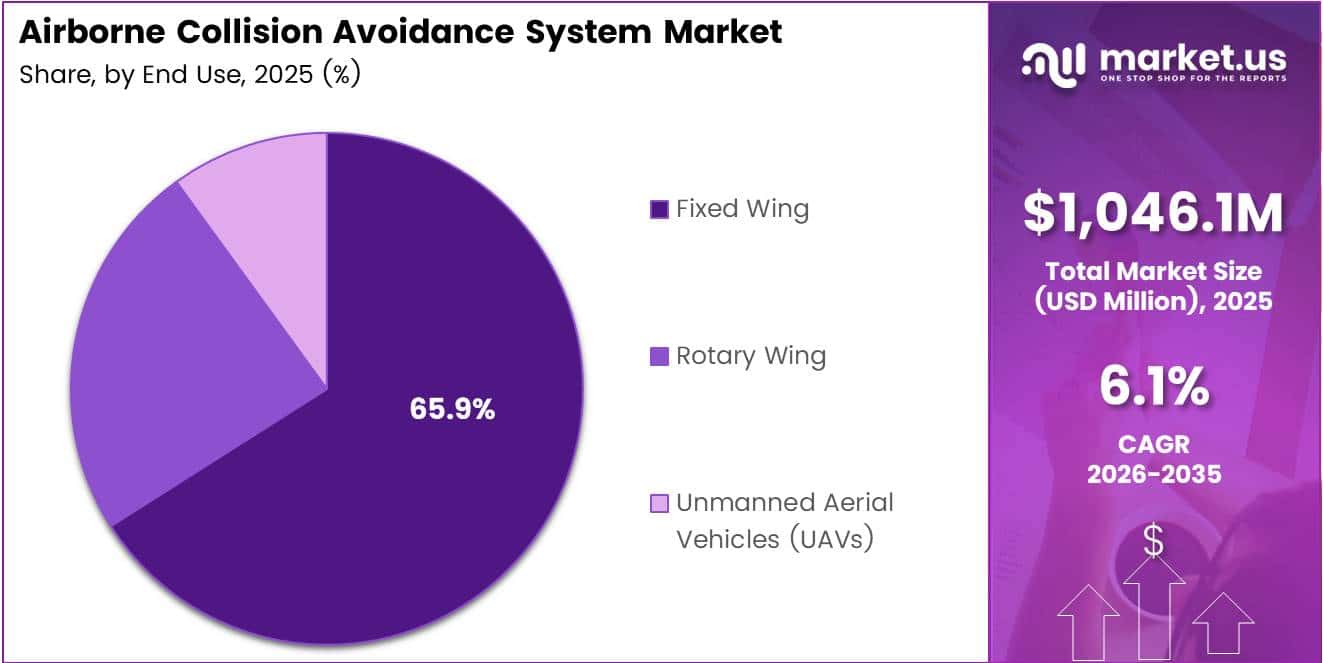

Global Airborne Collision Avoidance System Market size is expected to be worth around USD 1,888.0 Million by 2035 from USD 1,046.1 Million in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

Airborne collision avoidance systems protect aircraft by detecting nearby traffic and issuing resolution advisories to pilots. These systems operate independently of ground-based air traffic control, providing a critical last line of defense against mid-air collisions. Their deployment spans commercial aviation, military aircraft, general aviation, and increasingly, unmanned aerial platforms.

The commercial aviation sector drives the bulk of current demand, as global scheduled operations now exceed 37 million departures annually. Regulatory mandates from ICAO, FAA, and EASA require collision avoidance equipment across most aircraft categories. Consequently, both OEM installations and retrofit programs create sustained revenue streams for system vendors.

Military aviation adds a separate but growing demand layer. Defense agencies worldwide prioritize onboard safety systems as air traffic density increases in shared civil-military airspace. Advanced avionics procurement programs in the US, Europe, and Asia-Pacific now routinely include collision avoidance as a standard requirement rather than an optional upgrade.

The UAV segment signals where the next structural demand shift is occurring. Urban air mobility vehicles, cargo drones, and surveillance UAVs each require collision avoidance solutions tailored to low-altitude, high-density operations. In December 2024, Honeywell Aerospace launched a software-based ACAS X upgrade specifically designed to reduce nuisance alerts in urban air mobility environments, signaling early commercial positioning for this segment.

According to ICAO’s State of Global Aviation Safety 2025 report, the 2024 global accident rate reached 2.56 accidents per million departures — a 36.8% increase from 1.87 per million in 2023. This deterioration in safety metrics directly strengthens the regulatory and operational case for mandatory collision avoidance upgrades across the global fleet.

According to the AIAA Air Traffic Control Quarterly, ACAS X reduces mid-air collision risk by approximately 59% relative to TCAS II, while also reducing overall alert rates by about 50%. These performance gains are not incremental — they represent a generational shift in system capability that makes legacy TCAS II replacement a financially and operationally justified investment for fleet operators.

Key Takeaways

- The global Airborne Collision Avoidance System market was valued at USD 1,046.1 Million in 2025.

- The market is forecast to reach USD 1,888.0 Million by 2035, growing at a CAGR of 6.1%.

- By Type, ACAS I & TCAS I held the dominant share at 56.8% in 2025.

- By Component, Mode S & C Transponder led with a 44.3% share.

- By End Use, Fixed Wing aircraft commanded the largest share at 65.9%.

- By Sales Channel, OEM accounted for 71.2% of total market revenue.

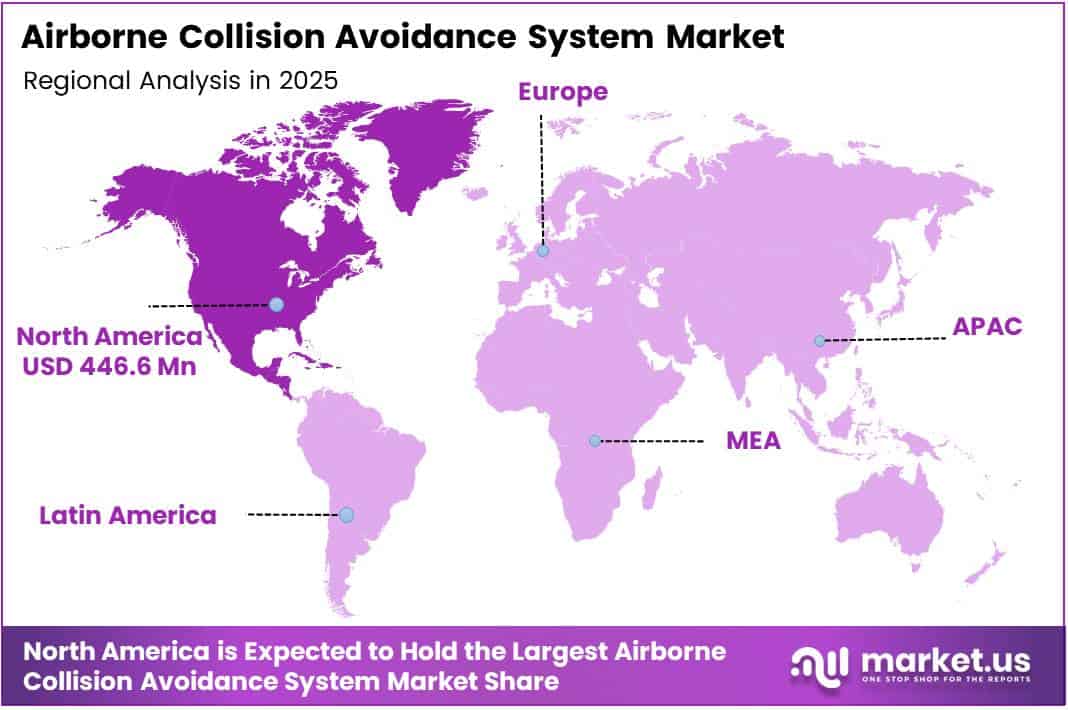

- North America dominated regional markets with a 42.70% share, valued at USD 446.6 Million.

Type Analysis

ACAS I & TCAS I dominates with 56.8% due to widespread mandatory regulatory deployment.

In 2025, ACAS I & TCAS I held a dominant market position in the By Type segment of the Airborne Collision Avoidance System Market, with a 56.8% share. Decades of FAA and ICAO mandates requiring TCAS I across turbine-powered aircraft have created a deeply embedded installed base. Replacement cycles and compliance-driven retrofits sustain revenue well beyond initial OEM installation timelines.

ACAS II & TCAS II carries the highest technical capability among currently certified legacy systems. It issues both traffic advisories and coordinated resolution advisories, making it the required standard for larger commercial aircraft. However, its relative complexity and higher unit cost position it as a premium tier, with adoption concentrated among commercial carriers and larger business aviation operators.

Portable Collision Avoidance System (PCAS) serves as the entry point for general aviation operators who face cost constraints but still require basic traffic awareness. PCAS devices offer subscription-free ADS-B integration and attach to existing cockpit displays. Their lower price point expands the addressable market into light aircraft categories that traditional certified ACAS systems cannot economically serve.

FLARM differentiates through its design for low-altitude, high-density operations involving gliders, light aircraft, and drones. Unlike TCAS-based systems, FLARM uses a proprietary radio protocol optimized for short-range collision risk. Its adoption across European glider clubs and increasingly among drone operators reflects a structural gap in conventional ACAS coverage that FLARM specifically fills.

Component Analysis

Mode S & C Transponder dominates with 44.3% due to universal ATC interrogation compliance requirements.

In 2025, Mode S & C Transponder held a dominant market position in the By Component segment of the Airborne Collision Avoidance System Market, with a 44.3% share. Transponders form the communication backbone of every ACAS installation, enabling both air traffic control surveillance and aircraft-to-aircraft threat detection. Regulatory mandates in controlled airspace make transponder replacement and upgrade a non-discretionary expenditure for operators.

Processor units determine the computational capability of the entire collision avoidance system. As ACAS X adoption advances, processing requirements escalate significantly — the new logic relies on Monte Carlo simulations involving millions of encounter scenarios, demanding substantially more onboard compute power than TCAS II. Vendors supplying high-performance processors for next-generation ACAS installations face a near-term demand window as fleet upgrades accelerate.

Display Unit components translate collision avoidance data into actionable pilot guidance. Modern integrated avionics suites increasingly combine TCAS traffic displays with synthetic vision and terrain awareness on single screens. This consolidation reduces cockpit workload while creating cross-sell opportunities for avionics vendors who control both the display hardware and the underlying ACAS software layer.

End Use Analysis

Fixed Wing dominates with 65.9% due to commercial airline regulatory mandates and fleet scale.

In 2025, Fixed Wing aircraft held a dominant market position in the By End Use segment of the Airborne Collision Avoidance System Market, with a 65.9% share. Commercial airlines operating under ICAO Annex 10 requirements account for the majority of certified ACAS installations globally. The combination of fleet size, mandatory compliance, and regular avionics refresh cycles creates a predictable and large revenue base for system suppliers.

Rotary Wing platforms — including commercial helicopters, offshore transport aircraft, and military rotorcraft — represent a structurally different buyer profile. Helicopter operations frequently occur in low-altitude and uncontrolled airspace where collision risk patterns differ from fixed-wing commercial routes. Suppliers targeting this segment must adapt system sensitivity thresholds and alert logic to rotorcraft-specific flight envelopes.

Unmanned Aerial Vehicles (UAVs) represent the fastest-shifting demand category within end-use segments. Regulatory bodies in the US, EU, and Asia-Pacific are actively developing detect-and-avoid requirements for beyond-visual-line-of-sight drone operations. In January 2025, Garmin International introduced the GTX 345DR transponder-based collision avoidance product specifically targeting the general aviation and UAV markets with integrated dual-link ADS-B capabilities, signaling that major vendors already treat UAVs as a standalone addressable segment.

Sales Channel Analysis

OEM dominates with 71.2% due to factory-installation mandates and long procurement cycles.

In 2025, Original Equipment Manufacturer (OEM) channels held a dominant market position in the By Sales Channel segment of the Airborne Collision Avoidance System Market, with a 71.2% share. Aircraft manufacturers integrate certified ACAS systems at the production stage, locking in vendor relationships for the aircraft’s operational life. This OEM dominance reflects the certification barriers and airframe integration complexity that make post-delivery substitution commercially and technically impractical.

Aftermarket channels serve the global installed base of aircraft requiring system upgrades, regulatory compliance retrofits, or component replacements. As ACAS X certification advances and legacy TCAS II systems approach obsolescence, aftermarket retrofit programs will represent a meaningful revenue expansion. Operators with large mixed-age fleets face mandatory upgrade timelines, creating a structured and time-bound aftermarket demand cycle.

Key Market Segments

By Type

- ACAS I & TCAS I

- ACAS II & TCAS II

- Portable Collision Avoidance System (PCAS)

- FLARM

By Component

- Mode S & C Transponder

- Processor

- Display Unit

By End Use

- Fixed Wing

- Rotary Wing

- Unmanned Aerial Vehicles (UAVs)

By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Drivers

Mandatory Aviation Safety Regulations and Rising Air Traffic Density Compel Fleet-Wide ACAS Adoption

Global air traffic now spans roughly 37 million scheduled commercial departures annually, and congestion in major corridors creates compounding collision exposure. ICAO, FAA, and EASA mandates require certified collision avoidance on turbine-powered commercial and business aircraft. Compliance is non-negotiable — operators who miss retrofit deadlines face grounding orders, making regulatory pressure the single most reliable demand driver in this market.

According to Eurocontrol’s 2025 ACAS Guide, ACAS Xa reduces resolution advisories by approximately 60% compared with TCAS II while maintaining or improving overall safety. This quantifiable performance advantage directly accelerates mandatory upgrade cycles, as regulators can now cite specific metrics when setting transition timelines. Operators cannot argue against safety data of this magnitude when justifying continued use of legacy systems.

In March 2025, Honeywell International and Thales Group collectively captured a 33% market share by launching Software-as-a-Service collision avoidance modules updatable wirelessly without hardware replacement. This model directly addresses the cost objection that historically slowed compliance upgrades among mid-tier operators. By lowering the total cost of compliance, SaaS delivery removes a structural barrier and broadens the eligible buyer pool.

Restraints

High Retrofit Costs and Avionics Integration Complexity Slow Compliance Timelines for Legacy Fleets

Legacy aircraft retrofits require FAA or EASA supplemental type certificates, avionics bay modifications, and wiring harness changes — costs that can reach six figures per aircraft for older platforms. Operators running mixed-age fleets face disproportionate upgrade burdens relative to newer aircraft. This cost structure concentrates retrofit activity among well-capitalized carriers while smaller regional and charter operators delay compliance until regulatory deadlines force action.

According to ICAO’s State of Global Aviation Safety 2025 report, 95 accidents occurred in 2024 among scheduled commercial operations across approximately 37 million departures. The persistence of accidents despite widespread TCAS II deployment reflects a genuine technical gap — legacy systems generate excessive nuisance alerts that erode pilot trust and compliance. Fixing this requires hardware and software upgrades, not just regulatory pressure, which adds complexity and cost to the transition.

Technical integration challenges compound the financial barriers. Older avionics architectures use proprietary data buses and display protocols that are incompatible with modern ACAS X software interfaces. Aircraft manufactured before the 1990s often require full avionics bay redesigns to accommodate updated processors and transponders. This technical depth limits the pool of qualified MRO providers and extends retrofit timelines, creating schedule risk for operators managing fleet availability.

Growth Factors

UAV Detect-and-Avoid Mandates and Next-Generation ACAS X Capabilities Open New Revenue Segments

Regulatory bodies in the US, EU, and Asia-Pacific are advancing detect-and-avoid requirements for UAV beyond-visual-line-of-sight operations. These rules will require collision avoidance certification for commercial cargo drones, surveillance platforms, and urban air mobility vehicles — categories that current TCAS-based systems were not designed to serve. Vendors who certify ACAS X variants for unmanned platforms first will capture early-mover advantages in a segment with no established incumbent.

According to SKYbrary’s 2025 ACAS X summary, FAA evaluations show ACAS Xa improved overall safety by approximately 20% compared with TCAS II and reduced the alerting rate by approximately 65% in US radar-track data. A 65% reduction in alerts means pilots receive fewer false warnings, directly improving response discipline and system trust. Higher trust translates to faster institutional adoption — airlines, militaries, and regulators can justify fleet-wide transitions with confidence in this performance data.

Emerging aviation markets in Southeast Asia, the Middle East, and Africa are expanding commercial fleets from a smaller installed base, which means new aircraft deliveries drive ACAS adoption without the retrofit complexity that constrains mature markets. Additionally, advancements in solid-state radar and AI-assisted data processing are lowering the hardware cost of high-performance ACAS platforms. Together, these factors open addressable markets that were previously cost-prohibitive for smaller operators and developing-region carriers.

Emerging Trends

ACAS X Transition and AI-Based Predictive Logic Redefine Collision Avoidance Performance Standards

The aviation industry is actively transitioning from rule-based TCAS II logic to the probability-based ACAS X framework. ACAS X logic is tuned using Monte Carlo simulations of thousands to millions of randomized aircraft encounters — several orders of magnitude more test cases than the handcrafted scenarios used for TCAS II. This computational depth allows ACAS X to issue more precise, situation-specific advisories rather than conservative default responses that frequently trigger unnecessary maneuvers.

According to SKYbrary, when only one pilot follows the resolution advisory, ACAS Xa still provides approximately 47% greater safety benefit than TCAS II. This robustness under non-ideal compliance conditions is significant — it means the system delivers measurable safety value even in real-world scenarios where crew coordination is imperfect. For regulators and fleet operators, this single metric removes a persistent objection to ACAS X adoption timelines.

AI integration is extending collision avoidance beyond reactive alert systems toward predictive conflict detection. Autonomous and semi-autonomous aircraft require onboard decision logic that does not depend on a human pilot to act on advisories. Vendors developing AI-assisted ACAS variants are positioning for a future where detect-and-avoid functions as an autonomous flight control input rather than a crew notification system — a fundamental shift in system architecture with long-term procurement implications.

Regional Analysis

North America Dominates the Airborne Collision Avoidance System Market with a Market Share of 42.70%, Valued at USD 446.6 Million

North America commanded 42.70% of the global market, valued at USD 446.6 Million in 2025. The FAA’s long-standing TCAS mandates, the presence of the world’s largest commercial aviation infrastructure, and active military avionics modernization programs collectively sustain this leadership position. Moreover, the concentration of major ACAS vendors and certified MRO networks in the US reinforces both supply-side capacity and procurement efficiency.

Europe Airborne Collision Avoidance System Market Trends

Europe holds the second-largest regional position, anchored by EASA’s binding airspace requirements and Eurocontrol’s active role in ACAS X transition planning. The region’s dense controlled airspace and high commercial flight frequency create consistent system demand. Additionally, European defense modernization programs across NATO member states add a parallel military procurement layer that supports regional market depth beyond commercial aviation alone.

Asia Pacific Airborne Collision Avoidance System Market Trends

Asia Pacific is the highest-growth regional market, driven by rapid commercial fleet expansion in China, India, and Southeast Asia. Airlines in these markets are taking new-generation aircraft deliveries with factory-installed ACAS X, bypassing the legacy retrofit cycle entirely. Consequently, Asia Pacific represents the clearest forward-looking demand concentration for OEM-channel ACAS suppliers as fleet sizes continue to scale.

Latin America Airborne Collision Avoidance System Market Trends

Latin America operates a mixed fleet of aging regional aircraft alongside newer narrowbody deliveries, creating a bifurcated market of retrofit demand and new-build OEM installations. Brazil and Mexico anchor regional procurement activity through their national carriers and growing low-cost aviation sectors. However, budget constraints among smaller regional operators limit retrofit conversion rates compared with North American and European peers.

Middle East and Africa Airborne Collision Avoidance System Market Trends

Middle East carriers operate among the world’s most modern fleets, with Gulf-based airlines consistently ordering ACAS-equipped aircraft directly from OEM channels. Africa presents a contrasting picture — fleet modernization programs remain donor-funded or state-financed in many markets, slowing voluntary upgrade adoption. The Middle East’s hub carrier model creates concentrated, high-value procurement activity that partially offsets Africa’s slower adoption pace within the combined regional grouping.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Honeywell International Inc. occupies the strongest commercial position in the ACAS market through its dual control of certified hardware and software upgrade pathways. Its December 2024 ACAS X software upgrade for urban air mobility environments demonstrates deliberate expansion beyond traditional aviation into the UAV and UAM segment — a strategic move that positions Honeywell ahead of pending detect-and-avoid regulations before the competitive window narrows.

Lockheed Martin Corporation approaches the ACAS market from a defense-first posture, supplying collision avoidance systems integrated into military aircraft platforms where mission-critical reliability requirements exceed commercial aviation standards. Its depth in government procurement relationships and classified avionics programs gives Lockheed a durable competitive position in military ACAS that commercial-focused vendors cannot easily replicate through standard certification pathways.

BAE Systems Plc differentiates through its integrated electronic warfare and avionics capabilities, allowing it to bundle collision avoidance functionality within broader mission systems for military customers. This systems integration approach creates higher switching costs than standalone ACAS vendors face, as replacing BAE’s collision avoidance component would require re-certification of interconnected avionics functions — a significant operational and financial deterrent for defense customers.

L3 Technologies, Inc. focuses on the intersection of ACAS hardware manufacturing and avionics integration services, particularly for retrofit programs targeting aging military and government aircraft. Its MRO network and retrofit engineering capabilities address the technical integration complexity that restrains legacy fleet upgrades — making L3 a critical execution partner for operators who face mandatory compliance timelines but lack internal avionics engineering capacity.

Key Players

- Honeywell International Inc.

- Lockheed Martin Corporation

- BAE Systems Plc

- L3 Technologies, Inc.

- Saab Group

- Rockwell Collins Inc.

- Garmin Ltd.

Recent Developments

- January 2025 — Garmin International introduced the GTX 345DR, a new transponder-based collision avoidance product targeting the general aviation and UAV markets. The product integrates dual-link ADS-B “In” capabilities, directly addressing the detect-and-avoid compliance gap in the growing UAV operator segment.

- April 2026 — Market analysis confirmed that ACAS X adoption improved collision avoidance efficiency by 30% over legacy systems. Nearly 60% of commercial fleet upgrades now utilize advanced ACAS X algorithms, indicating that the transition from TCAS II has crossed a majority threshold in active upgrade programs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,046.1 Million |

| Forecast Revenue (2035) | USD 1,888.0 Million |

| CAGR (2026-2035) | 6.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (ACAS I & TCAS I, ACAS II & TCAS II, Portable Collision Avoidance System, FLARM), By Component (Mode S & C Transponder, Processor, Display Unit), By End Use (Fixed Wing, Rotary Wing, Unmanned Aerial Vehicles), By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Honeywell International Inc., Lockheed Martin Corporation, BAE Systems Plc, L3 Technologies Inc., Saab Group, Rockwell Collins Inc., Garmin Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |