Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Material Type Analysis

- Function / Application Analysis

- Thickness Analysis

- End User Analysis

- Key Market Segments

- Market Dynamics

- Drivers

- Restraints

- Challenges

- Opportunities

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

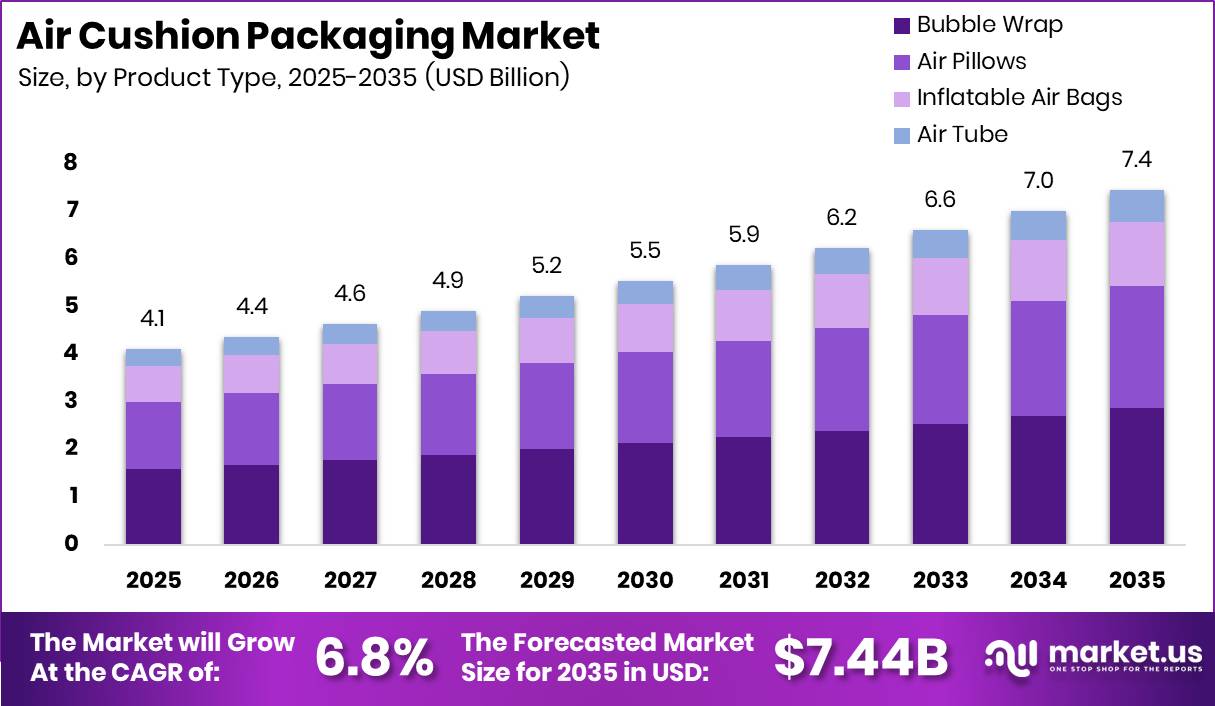

Global Air Cushion Packaging Market size is expected to be worth around USD 7.44 Billion by 2035 from USD 4.12 Billion in 2025, growing at a CAGR of 6.8% during the forecast period 2026 to 2035. This trajectory reflects the structural weight that e-commerce fulfillment and damage-control logistics place on lightweight protective solutions.

The air cushion packaging market covers inflatable protective packaging formats used to prevent product damage during storage and shipment. These formats include bubble wrap, air pillows, inflatable air bags, and air tubes. Buyers span e-commerce retailers, electronics manufacturers, pharmaceutical distributors, automotive suppliers, and logistics operators. This reflects how broadly protective void-fill demand has embedded itself across supply chains.

Key Takeaways

- Market value in 2025 stands at USD 4.12 Billion, forecast to reach USD 7.44 Billion by 2035.

- The market grows at a CAGR of 6.8% from 2026 to 2035.

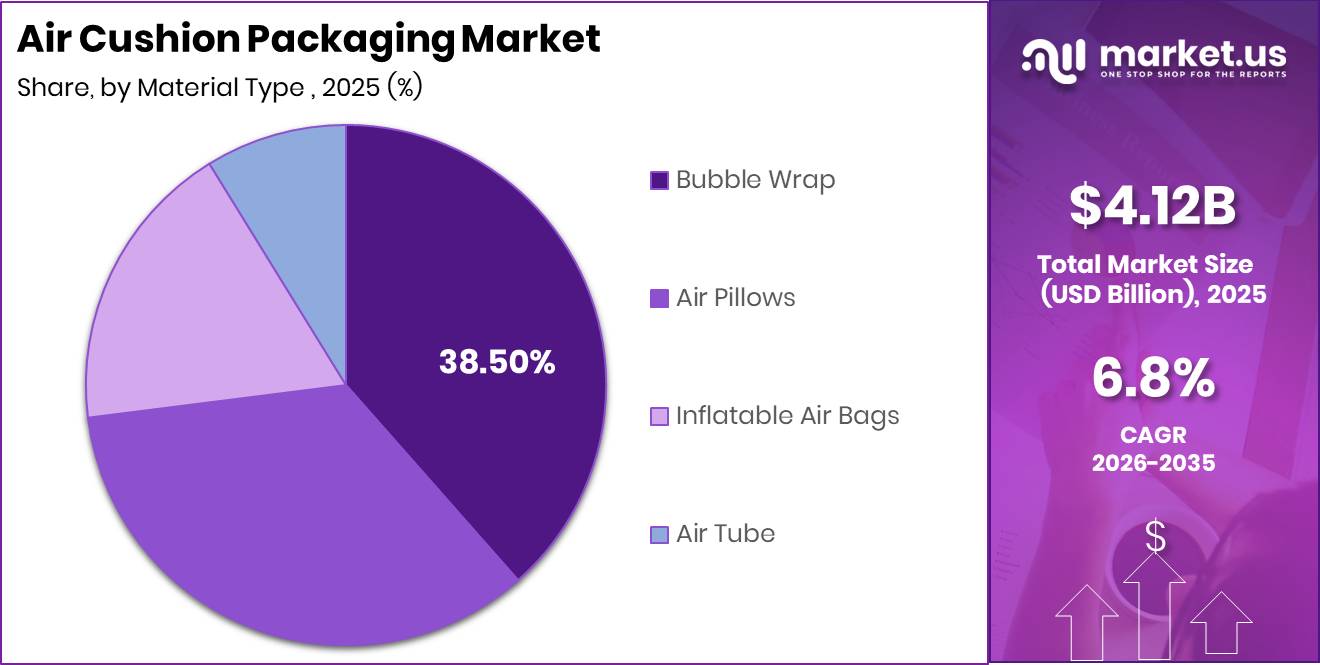

- Bubble Wrap dominates the By Product Type segment with a 38.50% share.

- LDPE dominates the By Material Type segment with a 45.00% share.

- Void Fill dominates the By Function / Application segment with a 42.60% share.

- The 30 to 60 Microns thickness tier dominates the By Thickness segment with a 52.40% share.

- E-Commerce and Retail dominates the By End User segment with a 44.20% share.

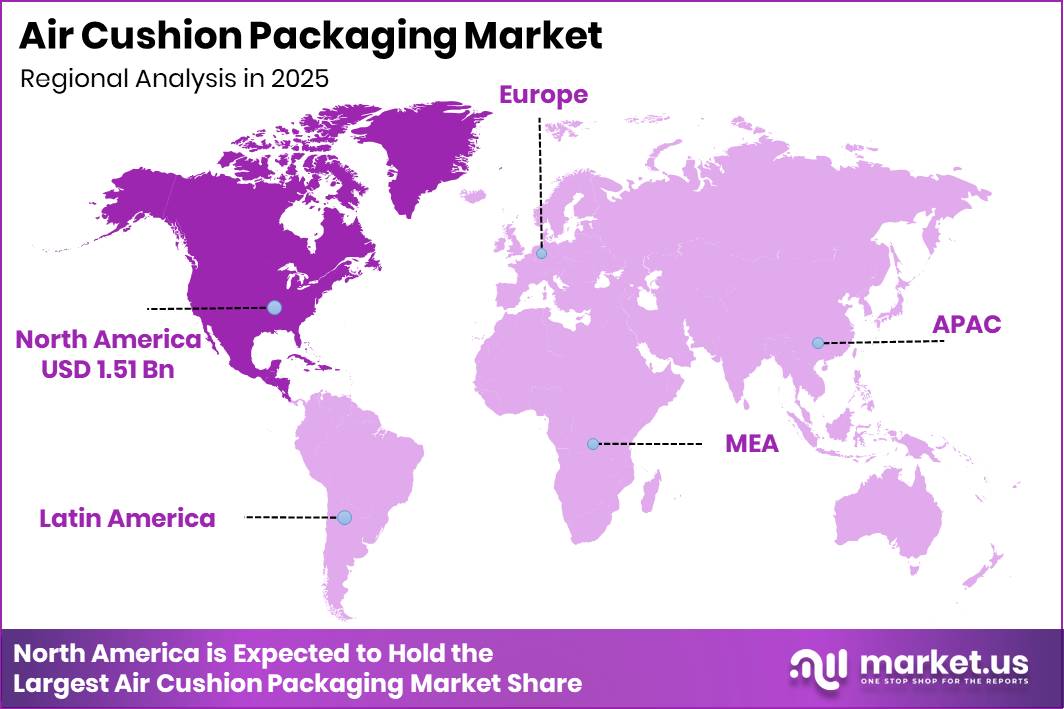

- North America leads all regions with a 36.80% market share, valued at USD 1.51 Billion.

Government policy is reshaping how air cushion suppliers design and position their products. The EU’s Packaging and Packaging Waste Regulation entered into force in February 2025, with broad application beginning in August 2026. E-commerce and transport packaging will face an empty-space ratio cap of 50% from 1 January 2030. This shifts spend toward right-sized cushion dispensing and mono-material films.

Data from DS Smith’s Material Change Index shows the study analyzed 1,500 food and beverage products across major European retailers to assess packaging substitution opportunities. DS Smith found that 51% of plastic food packaging formats assessed could be minimized or replaced with alternative materials. This scale of substitution assessment signals that air cushion vendors operating in food-adjacent sectors face intensifying pressure to reformulate or certify materials ahead of European compliance windows.

Product Type Analysis

Bubble Wrap dominates with 38.50% due to universal compatibility across product categories.

In 2025, Bubble Wrap held a dominant market position in the By Product Type segment of the Air Cushion Packaging Market, with a 38.50% share. Bubble wrap’s surface-contact protection suits fragile items across e-commerce, electronics, and retail channels. Vendors that maintain bubble wrap as a primary SKU capture the broadest buyer base before specialty formats capture niche volume.

Air Pillows represent the second-largest sub-segment with a 34.50% share. Air pillows are the preferred void-fill format for automated fulfillment centers because on-demand inflation machines reduce warehousing footprint. As per our research, Pregis AirSpeed® Renew air cushion films contain a minimum of 30% post-consumer recycled content, giving distributors a compliance-ready product as EPR rules tighten. Buyers seeking machine-compatible recyclable options will accelerate air pillow adoption over bubble wrap in regulated markets.

Inflatable Air Bags hold an 18.20% share in the By Product Type segment. Air bags serve blocking and bracing applications where items require fixed-position immobilization inside cartons. This functional specificity makes air bags a harder-to-substitute format, even as sustainability pressure pushes buyers toward lighter-weight alternatives. Vendors offering certified inflatable air bags retain a defensible position in electronics and automotive shipments.

Air Tube holds the remaining 8.80% share. Air tubes serve edge and corner protection applications where surface wrapping formats cannot conform. This niche role limits volume but supports premium pricing due to format specificity and lower substitution risk.

Material Type Analysis

LDPE dominates with 45.00% due to processing flexibility and broad machine compatibility.

In 2025, LDPE held a dominant market position in the By Material Type segment of the Air Cushion Packaging Market, with a 45.00% share. LDPE’s low sealing temperature and film flexibility make it the default film input across most inflatable cushion machine platforms. Converters that source LDPE at scale retain a cost-per-meter advantage that newer bio-based entrants cannot yet match.

HDPE holds a 22.40% share of the By Material Type segment. HDPE films provide higher tensile strength at thinner gauges, which reduces material consumption per cushion without sacrificing burst resistance. This positions HDPE as the preferred material for high-throughput operations where film efficiency directly affects line cost. Buyers managing large-volume automated pack stations increasingly specify HDPE to reduce per-unit material spend.

Polyethylene Blends account for a 18.60% share. PE blend films allow converters to balance cost, seal performance, and limited recyclability compliance within a single structure. This flexibility makes blends a transitional format as buyers move toward mono-material recyclable structures under EPR frameworks. Suppliers that master blend formulation will bridge the gap between conventional film buyers and regulated-market accounts.

Bio-Based and Biodegradable Films hold 8.80% and Recycled Content Films hold 5.20%, together representing the remaining share. These formats carry price premiums and require certified supply chains, limiting current volumes. However, as regulatory timelines compress toward 2030, their combined addressable pool will expand among brand-owner accounts in Europe and Japan.

Function / Application Analysis

Void Fill dominates with 42.60% due to universal applicability in e-commerce carton packing.

In 2025, Void Fill held a dominant market position in the By Function / Application segment of the Air Cushion Packaging Market, with a 42.60% share. Void fill commands this share because nearly every parcel shipped in an oversized carton requires dead-space elimination to prevent product movement. Suppliers that optimize for on-demand void-fill inflation speed hold a direct throughput advantage in high-volume fulfillment environments.

Blocking and Bracing, Wrapping, Edge and Corner Protection, and Cushioning each represent distinct functional applications within the remaining share of the segment. Blocking and bracing serves industrial and automotive shipments where load immobilization is the primary requirement. Wrapping and cushioning address fragile consumer goods, while edge and corner protection serves electronics and appliance formats where point-impact damage is the primary risk. Vendors that offer a full-function portfolio across these applications reduce buyer switching costs and deepen account retention.

Thickness Analysis

30 to 60 Microns dominates with 52.40% due to balanced protection and material efficiency.

In 2025, the 30 to 60 Microns tier held a dominant market position in the By Thickness segment of the Air Cushion Packaging Market, with a 52.40% share. This gauge range delivers sufficient cushioning for most e-commerce categories without excess resin consumption. Buyers operating high-throughput lines standardize on this tier to balance protection performance and per-unit film cost across their product mix.

Less than 30 Microns and Above 60 Microns each serve defined applications at the extremes of the thickness spectrum. Sub-30-micron films target cost-sensitive, lightweight shipments where minimum protection is acceptable. Above-60-micron formats serve heavy or high-value goods where superior burst resistance justifies higher material cost. These flanking segments are structurally smaller but support differentiated pricing strategies for vendors that invest in multi-gauge film lines.

End User Analysis

E-Commerce and Retail dominates with 44.20% due to parcel volume and void-fill intensity.

In 2025, E-Commerce and Retail held a dominant market position in the By End User segment of the Air Cushion Packaging Market, with a 44.20% share. Parcel output from online retail generates the highest per-order void-fill demand of any end-user category. Suppliers that secure preferred-vendor agreements with major fulfillment operators lock in recurring film volume before competitors can bid on the same programs.

Consumer Electronics and Appliances, Pharmaceuticals and Healthcare, Automotive, Logistics, and Others each represent addressable end-user pools beyond the e-commerce core. Electronics and appliances require precision cushioning formats to protect high-value items against transit shock. Pharma and healthcare shipments demand certified protective materials that meet product integrity and traceability requirements. Automotive and logistics users prioritize blocking and bracing performance over cost, creating a durable premium pocket for specialized suppliers.

Key Market Segments

By Product Type

- Bubble Wrap

- Air Pillows

- Inflatable Air Bags

- Air Tube

By Material Type

- LDPE (Low-Density Polyethylene)

- HDPE (High-Density Polyethylene)

- Polyethylene (PE) Blends

- Bio-Based / Biodegradable Films

- Recycled Content Films

By Function / Application

- Void Fill

- Blocking and Bracing

- Wrapping

- Edge and Corner Protection

- Cushioning

By Thickness

- Less than 30 Microns

- 30 to 60 Microns

- Above 60 Microns

By End User

- E-Commerce and Retail

- Consumer Electronics and Appliances

- Pharmaceuticals and Healthcare

- Automotive

- Logistics (Transport, Shipping and Warehousing)

- Others

By Distribution Channel

- Direct Sales / B2B

- Online Retail / E-Commerce

- Distributors and Wholesalers

- Retail Stores

Market Dynamics

Market Opportunity Analysis - Underserved end users and emerging regions offer targeted entry points for air cushion suppliers

Pharmaceuticals and Healthcare represent an underexploited end-user pool within the By End User segment. Air cushion packaging penetration in this category remains limited compared to e-commerce, yet medical device and drug shipments demand certified protective formats with traceable material content. Suppliers that develop pharma-compliant air cushion film certifications can access a premium buyer segment with lower price sensitivity and longer contract cycles than e-commerce accounts.

The Above 60 Microns thickness tier sits at the lower end of current volume share within the By Thickness segment. However, this gauge serves high-value electronics and automotive shipments where damage costs outweigh material premiums. Vendors investing in multi-gauge film lines can capture this underserved tier and price at a structural premium relative to the dominant 30 to 60 micron standard format.

Latin America and Middle East and Africa remain structurally underpenetrated relative to their e-commerce growth trajectories. Brazil and Mexico anchor the Latin America opportunity, with expanding online retail networks creating consistent void-fill demand. GCC logistics hubs present a parallel opportunity tied to high-throughput regional distribution, where air cushion machine placements by early-mover vendors will define long-term supply relationships before local competitors scale.

By contrast, Bio-Based and Biodegradable Films hold only an 8.80% share of the By Material Type segment today, but face the largest structural uplift from regulatory timelines compressing toward 2030. Suppliers that achieve certified bio-based or compostable film qualification before European and Japanese compliance deadlines arrive will access a switchover pool that incumbent LDPE-focused vendors cannot serve without retooling their film lines.

Technology and Innovation Landscape - Film efficiency, recycled-content engineering, and machine scalability define the competitive edge

Sealed Air’s Extreme Efficiency film technology delivers 40% more film length per roll than traditional inflatable air pillow film rolls. This improvement directly reduces roll-change frequency and downtime in high-throughput fulfillment operations. Vendors that offer higher meters-per-roll ratios lower their effective cost per cushion for buyers and create a measurable operational efficiency argument that competitors with standard roll formats cannot match.

Storopack’s AIRplus® 100% Recycled air cushion technology achieves a film composition of 99% air and only 1% film material, minimizing raw material consumption per cushion. RecyClass certification verifies the use of up to 100% recycled material in these films, providing buyers with third-party validated material credentials. Storopack AIRplus® 100% Recycled film production generates 30% fewer greenhouse gas emissions than virgin-material air pillow production, a figure that directly supports corporate carbon-reduction procurement criteria.

Storopack’s AIRmove² 50% Recycled film reduces fossil-resource consumption by approximately 39% versus the standard film while maintaining equivalent cushioning performance. A single roll of AIRmove² 50% Recycled film contains 435 meters of film, reducing roll-change frequency and improving line uptime. This combination of sustainability credentials and operational efficiency positions the format as a transition product for buyers moving from virgin-material films toward fully recycled structures without sacrificing pack-line throughput.

Storopack’s AIRmove® air cushion system produces 3.5 meters of air cushion film per minute and is designed for packaging operations handling up to 20 packages per day. The AIRmove² scales this to 500 packages per day, giving vendors a machine portfolio that addresses SME micro-fulfillment centers and enterprise fulfillment hubs within a single product family. This scalability means suppliers can onboard small accounts and grow with them as their shipment volumes expand, reducing churn risk across the customer lifecycle.

Drivers

The EU’s Packaging and Packaging Waste Regulation entered into force in February 2025, with broad application beginning in August 2026. The regulation is designed to make packaging recyclable by 2030 while reducing unnecessary packaging volume. E-commerce and transport packaging will face an empty-space ratio cap of 50% from 1 January 2030, which directly targets air cushion usage patterns in oversized cartons.

This cap does not simply destroy demand. It redirects spend toward right-sized carton design, better-calibrated cushion dispensing, mono-material films, and protective systems that can prove both damage prevention and regulatory fit. Storopack became the first manufacturer to commercialize an air pillow film made from 100% recycled material sourced from both post-consumer and post-industrial waste streams, establishing a supply-side reference point for what compliance-ready film looks like. Storopack also set a target to manufacture at least 50% of its internally produced protective packaging from recycled or renewable raw materials by 2025. Vendors that cannot match this standard will lose bids to compliant competitors.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce shipment growth lifts void-fill demand | +1.5% | North America core, Western Europe, India, Southeast Asia | Short term (≤ 2 years) |

| EU packaging rules force redesign of protective formats | +1.3% | EU core, UK spill-over, export-led APAC supply chains | Medium term (2-4 years) |

| Recycled-content and EPR compliance reshape film sourcing | +0.9% | EU, India, North America branded accounts | Medium term (2-4 years) |

| Automated pack stations expand on-demand air cushion use | +1.0% | North America, Germany, Benelux, Japan, China coastal hubs | Short term (≤ 2 years) |

| Damage-control economics support lightweight cushioning | +1.1% | North America, EU, China, Australia | Short term (≤ 2 years) |

| Plastic-to-paper substitution changes product mix, not protection demand | +0.6% | North America, EU, developed APAC | Medium term (2-4 years) |

Restraints

The most immediate commercial restraint for the air cushion packaging market is polymer input instability. Air pillows and inflatable void-fill formats remain heavily dependent on LLDPE and LDPE films whose costs move sharply with upstream feedstock, energy, and freight disruptions. Public price references in 2026 show LLDPE at roughly USD 1.08/kg in North America, USD 2.26/kg in Europe, and USD 1.28/kg in Northeast Asia. These inter-regional gaps weaken standardized global sourcing strategies.

Resin typically represents the dominant share of film input cost. Even a USD 100 to 200/ton movement compresses converter margins by more than 100 basis points when customer contracts reset only quarterly or semi-annually. Amazon reported that since 2024 it has removed plastic air pillows from all delivery packaging globally, reducing total plastic packaging by 16.4%. Amazon also reported eliminating 95% of plastic air pillows across North America, avoiding nearly 15 billion plastic air pillows annually. This buyer-side substitution compounds the margin pressure converters already face from resin volatility, slowing bid conversion and reducing order frequency across major accounts.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resin cost volatility | -1.4% | North America, EU, APAC core | Short term |

| Compliance cost escalation | -1.7% | EU, UK, Canada | Medium to Long term |

| Empty-space regulation risk | -0.9% | EU, advanced APAC | Medium to Long term |

| Margin pressure at converters | -1.1% | North America, EU | Medium term |

| Freight and lead-time instability | -0.6% | Global trade corridors | Short term |

| Shift to fiber alternatives | -0.8% | EU, North America | Medium to Long term |

Challenges

Air cushion packaging remains structurally exposed to resin cost turbulence because the product is still predominantly film-based and closely linked to polyethylene inputs. Global plastics production keeps upstream supply-demand balancing sensitive to energy, petrochemical outages, and inventory cycles. Converters can face 10 to 20% raw-material price swings within a planning cycle, compressing gross margins by 150 to 300 basis points if pass-through lags by one quarter.

This margin compression raises safety-stock requirements from roughly 3 weeks to 5 to 7 weeks and increases working-capital intensity for film inventory by about 8 to 12% during volatile procurement periods. The drag weakens forecasting accuracy and encourages buyers to stagger purchase commitments. Producers must offset this through multi-source resin strategies, indexed pricing models, thinner-gauge engineering, and higher machine efficiency per meter of film consumed to retain competitive positioning.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Resin price instability | -1.1% | North America, EU, Northeast Asia | Medium term (2-4 years) |

| Limited circular film availability | -0.9% | EU, UK, Canada, Japan | Long term (≥ 4 years) |

| Automation talent bottleneck | -0.8% | North America core, Western Europe, developed APAC | Medium term (2-4 years) |

| Cross-border fulfillment volatility | -0.8% | EU trade corridors, US import networks, APAC export hubs | Medium term (2-4 years) |

| Recyclability compliance complexity | -0.7% | EU regulatory hubs, UK, Canada, Australia | Long term (≥ 4 years) |

| Bio-material performance gap | -0.6% | EU, Japan, premium North America accounts | Medium term (2-4 years) |

Opportunities

Compostable and bio-based air cushion formats represent a future opportunity rather than a current market driver. Most of the existing market still runs on conventional polyethylene structures. The EU’s updated packaging rules entered into force in February 2025 and are designed to cut packaging waste, improve recyclability, and push packaging toward stricter design standards by 2030 and 2035. Storopack AIRplus® Bio Home Compostable film achieves at least 90% degradation within 365 days under home-composting conditions, demonstrating a certified product benchmark for this category.

This creates a premiumization lane where suppliers could secure 8% to 15% average selling price uplift, 300 to 500 basis points of gross margin expansion, and access to a new addressable revenue pool tied to sustainability-led SKU conversion. Food delivery, beauty, health products, and premium D2C categories are not yet fully penetrated by air cushion vendors, offering first-mover positions for suppliers that complete resin reformulation and machine compatibility adaptation before competitors do.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Compostable film conversion | +1.8% | EU, UK, North America, Japan | Medium term (2 to 4 years) |

| Fulfillment software integration | +1.5% | North America, EU, China, India | Short term (≤ 2 years) |

| Closed-loop recovery systems | +1.2% | EU core, UK, North America | Medium term (2 to 4 years) |

| Cold-chain and medical expansion | +1.0% | North America, EU, developed APAC | Long term (≥ 4 years) |

| SME and emerging-market penetration | +0.9% | India, ASEAN, LatAm, Africa | Long term (≥ 4 years) |

| Packaging-as-a-service monetization | +0.8% | Global enterprise and 3PL hubs | Medium term (2 to 4 years) |

Regional Analysis

North America Dominates the Air Cushion Packaging Market with a Market Share of 36.80%, Valued at USD 1.51 Billion

North America holds a 36.80% share of the global air cushion packaging market, valued at USD 1.51 Billion in 2025. The region’s dominance reflects a mature e-commerce infrastructure, high automated fulfillment penetration, and aggressive retailer-led sustainability commitments. According to Sealed Air, 55% of consumers expect brands to prioritize sustainable packaging, a figure that reinforces why major North American retailers are restructuring their protective packaging programs.

Europe represents the second most structurally significant regional market for air cushion packaging. The EU’s PPWR, which entered into force in February 2025, creates an immediate compliance driver for protective packaging reformulation across the continent. Vendors that can supply certified recyclable or mono-material air cushion films will gain preferred-vendor status with European brand owners before the August 2026 broad application deadline compresses lead times.

Asia Pacific is the fastest-expanding regional pool for air cushion packaging demand. E-commerce shipment volumes in China, India, and Southeast Asia create sustained void-fill requirements that outpace most other regions in unit growth. However, price sensitivity in emerging APAC markets limits adoption of premium sustainable films, meaning volume growth will concentrate in standard LDPE and PE blend formats for the near term.

Latin America and the Middle East and Africa each represent earlier-stage market pools where air cushion adoption tracks e-commerce infrastructure development. Brazil and Mexico anchor Latin America as the primary demand centers, driven by expanding online retail networks. GCC logistics hubs and South Africa’s growing organized retail sector offer longer-term entry points for suppliers willing to invest in distribution before volume matures.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Sealed Air Corporation holds a structural advantage in the air cushion packaging market through its broad portfolio of recycled-content inflatable films. Sealed Air’s recycled-content inflatable air pillows contain at least 95% recycled content, including 55% post-consumer recycled material, while its BUBBLE WRAP® Inflatable Cushioning product delivers 80% recycled content with full protective performance. In September 2025, Sealed Air introduced the AUTOBAG® 850HB with approximately two-minute changeovers between paper and poly materials, allowing fulfillment centers to switch packaging formats without additional equipment. These combined positions create a defensible account base among sustainability-led enterprise buyers.

Pregis Corporation competes on high-PCR film performance, targeting procurement programs where recycled content minimums are contractually specified. Pregis AirSpeed® HC Renew PCR inflatable cushioning film contains 80% post-consumer recycled content, while Pregis AirSpeed® Renew air cushion films deliver a minimum of 30% PCR content. This tiered portfolio lets Pregis address both premium sustainability accounts and cost-sensitive buyers within a single product family. However, Pregis’s competitive position depends on its ability to scale PCR resin sourcing as EPR rules raise minimum recycled content thresholds across key markets.

Key Players

- Sealed Air Corporation

- Pregis Corporation

- Smurfit Kappa Group Plc

- Storopack Hans Reichenecker GmbH

- Automated Packaging Systems

- FP International

- Intertape Polymer Group (IPG)

- Berry Global Group Inc.

- 3M Company

- Polyair Inter Pack Inc.

- Ranpak Holdings Corp.

- Abriso N.V.

- Airwave Packaging LLC

- Veritiv Corporation

- Shandong Xinniu Packaging

Recent Developments

- September 2025 – Sealed Air launched the AUTOBAG® 850HB Hybrid Bagging Machine, a new automated packaging system that runs both paper and poly mailers on a single platform, expanding its protective packaging and fulfillment portfolio.

- February 2025 – Storopack launched AIRfiber®, a paper-based air pillow solution featuring a water-soluble inner coating that enables recycling within standard paper waste streams while maintaining protective performance of conventional air cushions.

- February 2025 – Storopack commercialized AIRfiber® air pillows carrying the “Made for Recycling” certification under DIN EN 13430, expanding its sustainable air-cushion packaging portfolio with a certified recyclable format.

- October 2025 – Ranpak commercially launched FillPak® Mini, its smallest paper-based void-fill converter, designed for space-constrained packing stations and protective packaging applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.12 Billion |

| Forecast Revenue (2035) | USD 7.44 Billion |

| CAGR (2026-2035) | 6.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Bubble Wrap, Air Pillows, Inflatable Air Bags, Air Tube); By Material Type (LDPE, HDPE, Polyethylene PE Blends, Bio-Based / Biodegradable Films, Recycled Content Films); By Function / Application (Void Fill, Blocking and Bracing, Wrapping, Edge and Corner Protection, Cushioning); By Thickness (Less than 30 Microns, 30 to 60 Microns, Above 60 Microns); By End User (E-Commerce and Retail, Consumer Electronics and Appliances, Pharmaceuticals and Healthcare, Automotive, Logistics, Others); By Distribution Channel (Direct Sales / B2B, Online Retail / E-Commerce, Distributors and Wholesalers, Retail Stores) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Sealed Air Corporation, Pregis Corporation, Smurfit Kappa Group Plc, Storopack Hans Reichenecker GmbH, Automated Packaging Systems, FP International, Intertape Polymer Group (IPG), Berry Global Group Inc., 3M Company, Polyair Inter Pack Inc., Ranpak Holdings Corp., Abriso N.V., Airwave Packaging LLC, Veritiv Corporation, Shandong Xinniu Packaging |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |