Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- China AI Microcontrollers Market

- Product Analysis

- Technologies Analysis

- Sales Channel Analysis

- End-Use Industry Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

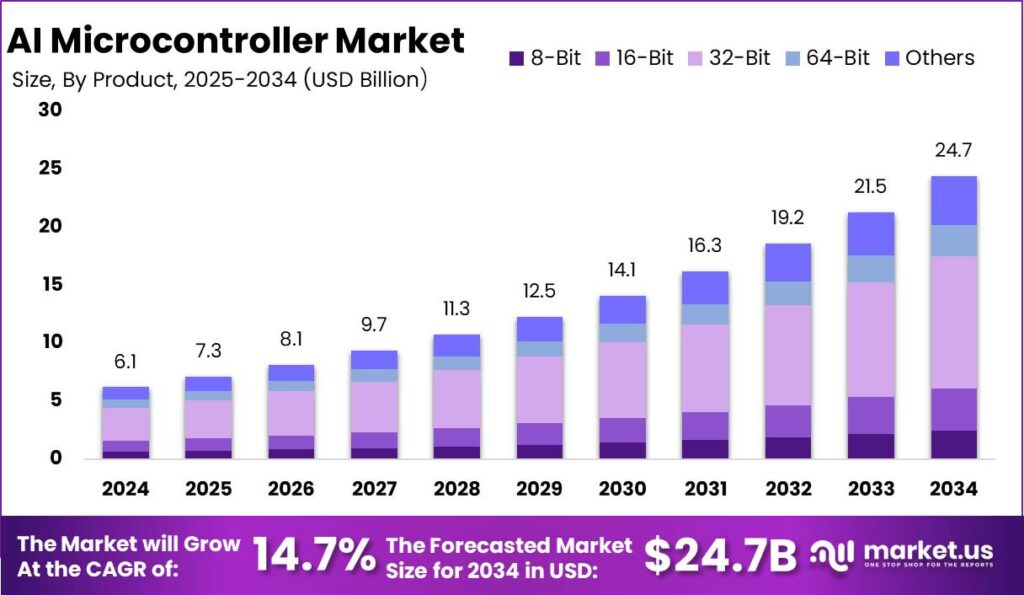

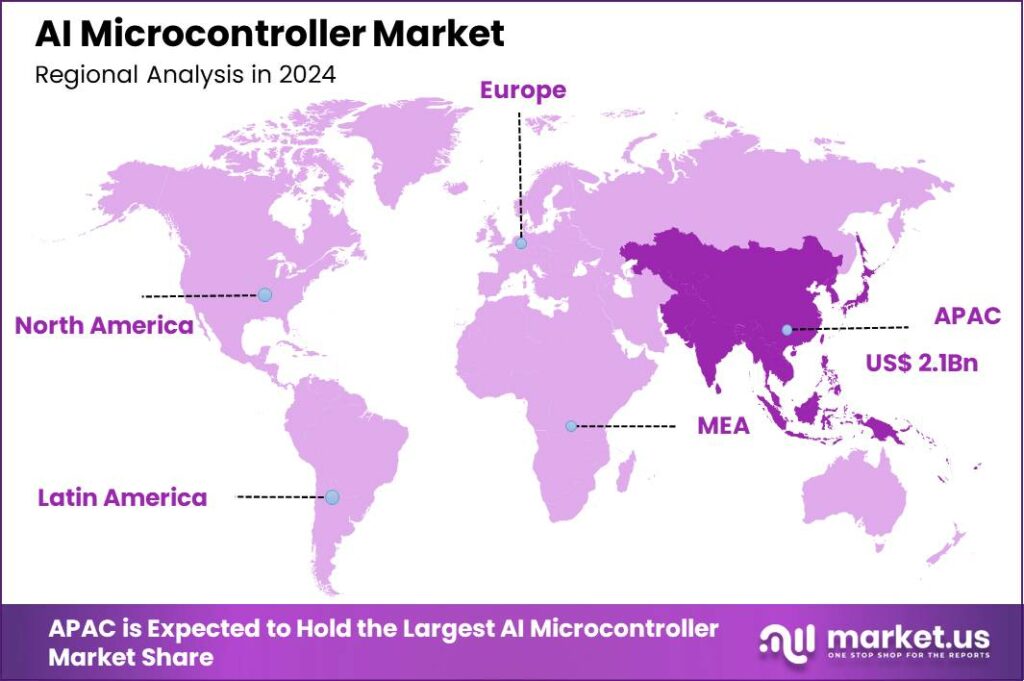

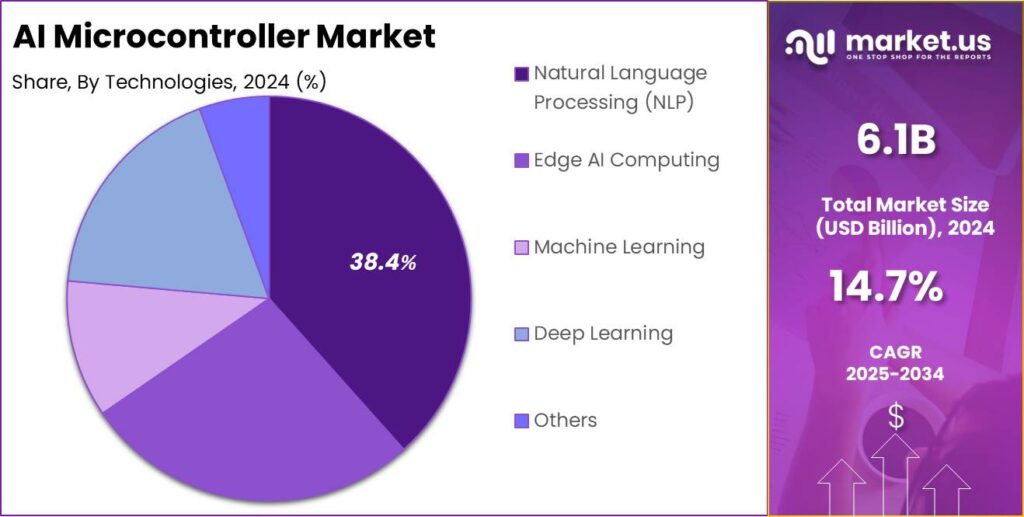

The AI Microcontroller Market size is expected to be worth around USD 24.7 Billion By 2034, from USD 6.1 billion in 2024, growing at a CAGR of 14.7% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 34.7% share, holding USD 2.1 Billion revenue.

The AI microcontroller market is experiencing significant growth, driven by the increasing integration of AI capabilities into various consumer and industrial products. This trend is propelled by the demand for devices that can process data locally, enhancing performance and privacy. The market is characterized by rapid technological advancements, with companies developing microcontrollers that offer higher processing power and energy efficiency.

The primary drivers of the AI microcontroller market include the growing demand for intelligent, autonomous devices, which require real-time processing capabilities. Increased adoption of IoT technologies, along with advancements in edge computing, has created a significant demand for AI-powered devices that can process data locally.

Key Takeaways

- The AI microcontroller market is expected to reach a value of approximately USD 24.7 billion by 2034, up from USD 6.1 billion in 2024, with a compound annual growth rate (CAGR) of 14.7% from 2025 to 2034.

- In 2024, the Asia-Pacific (APAC) region led the market, accounting for over 34.7% of the total share, generating USD 2.1 billion in revenue.

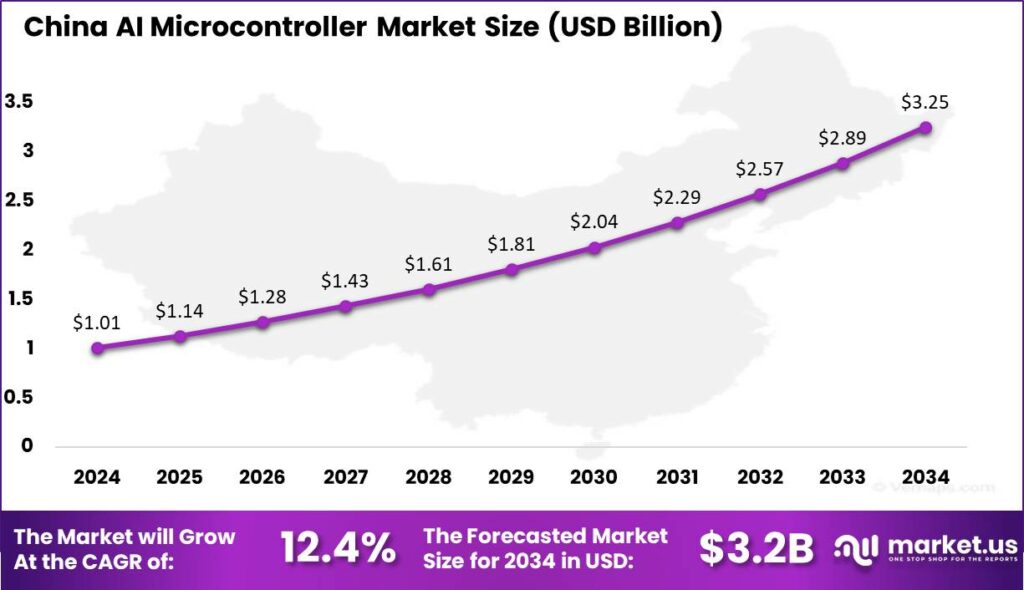

- China’s AI microcontroller market, specifically, was valued at USD 1.01 billion in 2024, growing at a CAGR of 12.4%.

- The 32-bit segment dominated the market in 2024, holding more than 46.7% of the share.

- Regarding applications, the Natural Language Processing (NLP) segment led the market with a share of over 38.4%.

- Direct sales channels also remained dominant in 2024, capturing more than 54.5% of the overall market share.

- In terms of end-use industries, the consumer electronics sector was the largest contributor, accounting for more than 36.5% of the total market share.

Analysts’ Viewpoint

Demand for AI microcontrollers is expanding across several industries. In the consumer electronics sector, smart devices such as smartphones, smart home appliances, and wearables are increasingly using AI microcontrollers to enhance their functionality, offering features such as voice recognition and adaptive user interfaces.

The automotive industry is also a significant contributor, with AI microcontrollers playing a crucial role in the development of electric vehicles (EVs) and autonomous driving systems. Investing in AI microcontrollers presents numerous opportunities. As more industries embrace automation, smart technologies, and edge computing, companies that provide AI-powered hardware solutions are poised for significant growth.

Recent technological advancements in AI microcontrollers include the development of more energy-efficient processors and the integration of advanced AI algorithms directly into the chip architecture. The ability to run complex machine learning models directly on the device, without the need for a cloud connection, has revolutionized various industries, making it possible for devices to make decisions faster and more reliably.

China AI Microcontrollers Market

The China AI Microcontroller Market size was exhibited at USD 1.01 Billion in 2024 with CAGR of 12.4%. This robust expansion can be attributed to several factors, including China’s significant advancements in artificial intelligence (AI) technology and the increased integration of AI systems across various industries.

The demand for microcontrollers embedded with AI capabilities is rising due to the country’s emphasis on innovation and the growing need for smarter, more efficient electronic systems. One of the key drivers behind this growth is China’s strong focus on becoming a global leader in AI development.

The government has implemented numerous policies and initiatives to encourage the development of AI technologies, which, in turn, fosters demand for AI-driven hardware such as microcontrollers. The rise of smart devices, IoT (Internet of Things) applications, and automation systems in sectors such as automotive, healthcare, and manufacturing is further fueling this demand.

Furthermore, the competitive landscape in China is supported by both domestic companies and international players. Local manufacturers have been quick to innovate and adapt to the growing AI trend, providing affordable and advanced microcontroller solutions.

In 2024, APAC held a dominant market position, capturing more than a 34.7% share, with a revenue of USD 2.1 billion in the AI microcontroller market. This substantial share can be attributed to the region’s robust technological advancements and high adoption rates of AI technologies across various industries, particularly in countries such as China, Japan, and South Korea.

APAC continues to be a global leader due to its large-scale manufacturing capabilities, strong research and development (R&D) infrastructure, and the presence of key players driving innovation in AI hardware. The increasing demand for automation in industries such as automotive, consumer electronics, and industrial applications has significantly contributed to the growth of the AI microcontroller market in the region.

Furthermore, governments in APAC countries have been heavily investing in smart infrastructure and AI-based solutions, creating a favorable environment for market expansion. The proliferation of the Internet of Things (IoT) devices, coupled with the region’s growing focus on artificial intelligence, has further solidified APAC’s position as a market leader.

Product Analysis

In 2024, the 32-bit segment held a dominant market position, capturing more than a 46.7% share of the AI microcontroller market. The widespread adoption of 32-bit microcontrollers can be attributed to their balanced performance, power efficiency, and versatility across a wide range of applications.

With significant improvements in processing capabilities, 32-bit microcontrollers are able to handle complex AI tasks, such as machine learning inference and sensor data processing, which are essential for IoT devices, robotics, and industrial automation.

The 32-bit architecture provides a favorable trade-off between performance and cost. It offers superior processing power compared to 8-bit and 16-bit microcontrollers while remaining more energy-efficient and affordable than 64-bit options. This combination makes 32-bit microcontrollers highly attractive for cost-sensitive applications where high performance is required but with limited power consumption.

Additionally, the growing demand for edge computing and real-time AI processing has further strengthened the position of 32-bit microcontrollers. With their ability to execute complex algorithms in real-time, these microcontrollers are increasingly being integrated into embedded systems that need local AI decision-making capabilities without relying on cloud processing.

The wide availability of development tools and software frameworks tailored for 32-bit systems has also enhanced their adoption, facilitating easier integration into new and existing technologies. The dominance of the 32-bit segment is expected to continue as the need for smart, connected devices increases.

Technologies Analysis

In 2024, the Natural Language Processing (NLP) segment held a dominant market position, capturing more than 38.4% of the AI microcontroller market share. This dominance can be attributed to the growing reliance on voice-activated technologies and automated customer service solutions across a wide range of industries.

NLP enables devices to interpret and respond to human language, making it an essential component in products such as virtual assistants, chatbots, and smart speakers. As consumer demand for seamless, voice-driven interactions increases, the adoption of NLP in microcontrollers is accelerating.

The rise of NLP technologies is closely tied to the expansion of smart home devices, mobile applications, and customer service automation. With advancements in speech recognition, sentiment analysis, and language translation, NLP is becoming a critical feature for many edge AI applications.

Microcontrollers equipped with NLP capabilities enable real-time language processing directly on devices, which reduces the dependency on cloud-based processing and enhances user experience by minimizing latency. This is particularly important for time-sensitive applications where immediate responses are necessary.

Moreover, the integration of NLP with machine learning algorithms has driven further market growth. Machine learning enhances NLP’s ability to understand context, nuance, and intent, which is crucial for applications in healthcare, retail, and finance.

For instance, in healthcare, NLP-enabled microcontrollers can assist in real-time transcription and analysis of medical conversations, while in retail, they can power personalized customer interactions. As the scope of NLP applications continues to widen, the demand for AI microcontrollers capable of handling these complex tasks is expected to rise.

Sales Channel Analysis

In 2024, the Direct Sales segment held a dominant market position in the AI microcontroller market, capturing more than 54.5% of the overall share. This substantial market dominance can be attributed to several key factors that contribute to the preference for direct sales channels in the AI microcontroller sector.

Direct sales enable manufacturers to establish closer relationships with their customers, allowing for tailored solutions and greater customization of microcontroller systems. These direct interactions also foster better customer support, which is essential for the technically complex nature of AI microcontroller products.

The direct sales model also offers manufacturers a more efficient route to market, reducing the reliance on intermediaries. By selling directly to customers, companies can maintain greater control over pricing, product positioning, and promotional strategies. Additionally, the growing emphasis on high-performance, application-specific AI microcontrollers, which require detailed technical understanding, makes direct engagement more favorable.

Buyers typically seek specialized products and solutions, making the personalized approach of direct sales more appealing compared to generalized retail or distributor offerings. Another significant advantage of direct sales is the potential for improved customer feedback and product innovation. As manufacturers deal directly with customers, they can gain invaluable insights into market needs, challenges, and future trends.

End-Use Industry Analysis

In 2024, the Consumer Electronics segment held a dominant market position in the AI microcontroller market, capturing more than 36.5% of the total market share. This growth can be attributed to the increasing demand for AI-powered devices such as smartphones, smart TVs, wearables, and home automation systems.

The integration of artificial intelligence (AI) into consumer electronics has enhanced device functionality, enabling advanced features like voice recognition, predictive behavior, and personalized experiences. Additionally, the growing adoption of the Internet of Things (IoT) and smart home ecosystems has further propelled the market demand for AI microcontrollers.

For instance, in smart appliances, AI can enable energy optimization, enhance user interaction through natural language processing, and even automate routine tasks. This shift toward more intelligent devices has made AI microcontrollers a key component in modern consumer electronics, contributing significantly to the segment’s market share.

The consumer electronics sector is also benefiting from the constant innovation and enhancement of AI capabilities, which drive the demand for microcontrollers with increased processing power and lower energy consumption. This trend is expected to continue, as the growing reliance on AI-powered functionalities across a broad range of devices makes microcontrollers indispensable for both new product development and upgrades of existing technologies.

Key Market Segments

By Product

- 8-Bit

- 16-Bit

- 32-Bit

- 64-Bit

- Others

By Technologies

- Edge AI Computing

- Natural Language Processing (NLP)

- Machine Learning

- Deep Learning

- Others

By Sales Channel

- Direct Sales

- Distributors & Resellers

- Online Sales

By End-Use Industry

- Consumer Electronics

- Automotive

- Industrial Automation

- Healthcare

- Retail & E-Commerce

- Aerospace & Defense

- Others (Agriculture, etc.)

Driver

Rising Demand for IoT Devices

The increasing integration of the Internet of Things (IoT) into everyday life is a significant driver for the growth of AI microcontrollers. As IoT devices proliferate in both consumer and industrial sectors, the need for powerful, low-power, and intelligent processing units has escalated. AI microcontrollers, which combine traditional microcontroller functionality with machine learning (ML) capabilities, enable edge devices to process data locally, reducing latency and bandwidth usage.

A major advantage of AI microcontrollers is their ability to perform tasks like voice recognition, image processing, and predictive maintenance, all without needing constant cloud interaction. For example, in smart home devices, AI microcontrollers can enable voice assistants to respond instantly to commands or even predict user behaviors based on past interactions.

Restraint

Power Consumption and Heat Dissipation Issues

Despite the growing popularity of AI microcontrollers, one significant restraint is the challenge of power consumption and heat dissipation. AI-driven tasks, especially those involving machine learning or real-time data processing, require substantial computational power, which in turn leads to higher energy consumption.

While traditional microcontrollers are optimized for low-power consumption, integrating AI capabilities often demands more processing resources, which can strain battery-operated or energy-efficient devices. This issue becomes even more critical in applications like wearable devices, where maintaining a small form factor while ensuring long battery life is a top priority.

In IoT devices, excessive power usage can lead to frequent recharging or larger, bulkier batteries, compromising the portability and convenience of the device. Additionally, the increased processing power required for AI tasks generates more heat, which, if not effectively managed, can degrade the performance and longevity of the device.

Opportunity

AI Microcontrollers in Autonomous Vehicles

One of the most exciting opportunities for AI microcontrollers lies in the rapidly growing autonomous vehicle market. These vehicles rely on a combination of sensors, cameras, radar, and machine learning algorithms to navigate and make real-time decisions. AI microcontrollers, integrated into vehicle control systems, can enhance the processing power needed to handle the massive amount of data these systems generate.

For autonomous vehicles, AI microcontrollers are crucial in performing tasks such as object detection, path planning, and decision-making in real-time. The ability to process data locally, without needing to send it to the cloud for analysis, reduces latency and allows for quicker decision-making, which is essential for safety in autonomous driving.

The opportunity in this space is significant as automotive manufacturers and tech companies increasingly invest in AI to enable full autonomy. As these technologies mature, AI microcontrollers will play a key role in ensuring that vehicles can operate independently, respond to changing road conditions, and interact with other vehicles and infrastructure in a safe and efficient manner.

Challenge

Complexity of Software Development

One of the biggest challenges in deploying AI microcontrollers is the complexity of software development. AI systems require a combination of algorithms, machine learning models, and hardware optimizations, all of which need to work seamlessly together. Developing this software stack is often a time-consuming and resource-intensive process.

For companies, the lack of standardized tools and platforms for developing AI-based systems can further complicate the development process. Additionally, developers must ensure that the algorithms used are optimized for the limited resources available on microcontrollers, such as memory and processing power. This requires deep expertise in both AI and embedded systems design.

Furthermore, since AI microcontrollers often perform tasks in real-time, the software must also be optimized for speed and reliability, adding another layer of complexity. The challenge is not only to develop robust AI models but to ensure they are both efficient and capable of operating within the constraints of low-power, resource-limited hardware.

Growth Factors

Increased Adoption of Smart Devices

The growth of AI microcontrollers is being significantly driven by the widespread adoption of smart devices across multiple sectors. These devices, ranging from home automation systems to wearable gadgets, rely heavily on efficient, intelligent microcontroller units to perform complex tasks with minimal power consumption. As consumers and businesses embrace the benefits of connected devices, the demand for smarter, more efficient AI microcontrollers has surged.

One of the most important factors fueling this growth is the advancement in artificial intelligence and machine learning technologies. As AI algorithms become more refined and adaptable, they can be implemented on smaller and less powerful devices, such as microcontrollers. This enables edge computing, where data is processed locally rather than being sent to a cloud server, improving response times and reducing the dependency on constant internet connectivity.

Emerging Trends

AI Integration at the Edge

One of the most prominent emerging trends in the microcontroller industry is the increasing integration of AI at the edge. Traditionally, computing systems relied on cloud computing to process large datasets, with the data sent back and forth between devices and cloud servers.

However, as data generation increases exponentially, especially in IoT and smart device applications, the need for faster data processing has led to a shift toward edge computing. This means that AI processing is being done directly on devices rather than in centralized data centers, reducing latency and bandwidth use.

AI microcontrollers are at the heart of this trend, enabling real-time decision-making by performing complex computations locally. For instance, in autonomous vehicles, AI microcontrollers help process sensor data, interpret images, and detect obstacles without relying on cloud-based processing.

Business Benefits

Improved Operational Efficiency and Cost Savings

One of the key business benefits of integrating AI microcontrollers into products and systems is the significant improvement in operational efficiency and cost savings. By empowering devices to process data locally and make decisions without relying on a central server or human intervention, businesses can automate processes, streamline operations, and reduce overhead costs.

For example, in industrial applications, AI microcontrollers can be used for predictive maintenance. By continuously monitoring machinery performance and analyzing sensor data in real-time, AI microcontrollers can identify potential issues before they lead to expensive breakdowns or downtime.

This predictive capability not only extends the lifespan of equipment but also reduces the costs associated with emergency repairs and unplanned maintenance. For businesses, this means less operational disruption and lower maintenance expenses, ultimately contributing to the bottom line.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

NXP Semiconductors has been actively enhancing its position in the AI microcontroller market through strategic acquisitions. In February 2025, NXP agreed to acquire Kinara, a company specializing in edge AI processors, for $307 million. This acquisition is expected to close in the first half of 2025, subject to customary closing conditions, including regulatory clearances.

AMD has been making significant strides in the AI microcontroller market through strategic acquisitions and product innovations. In December 2023, AMD launched the MI300 series chips, which quickly achieved $1 billion in sales. These chips are part of AMD’s new AI portfolio, including the Ryzen AI 300 series, Instinct MI325X accelerators, and MI350 graphics processing units.

Intel has been actively developing AI microcontroller solutions to compete with industry leaders. In December 2023, Intel unveiled Gaudi3, an AI chip designed for generative AI software, with plans for launch in 2024.This move signifies Intel’s commitment to advancing AI technologies and enhancing its presence in the AI microcontroller market.

Top Key Players in the Market

- Nvidia Corporation

- Advanced Micro Devices, Inc. (AMD)

- Alphabet Inc.

- Microsoft Corporation

- Qualcomm Incorporated

- STMicroelectronics NV

- Texas Instruments Incorporated

- Infineon Technologies AG

- NXP Semiconductors

- Others

Recent Developments

- In January 2025, Nvidia launched the “Orin-2” AI microcontroller, a significant upgrade to their earlier models, designed to optimize edge computing for autonomous vehicles and robotics. The chip incorporates enhanced AI processing capabilities, reducing latency and improving energy efficiency.

- In December 2024, AMD acquired a small AI microcontroller startup, “Neurolink Systems,” to enhance its capabilities in low-power AI processing. This acquisition is expected to bolster AMD’s position in edge computing and IoT solutions, with a focus on accelerating AI adoption in embedded systems.

- In November 2024, Alphabet entered a strategic partnership with NXP Semiconductors to co-develop AI microcontrollers specifically designed for smart home devices. These microcontrollers will integrate Google’s AI capabilities with NXP’s embedded solutions to drive the next generation of smart appliances.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.1 Bn |

| Forecast Revenue (2034) | USD 24.7 Bn |

| CAGR (2025-2034) | 14.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (8-Bit, 16-Bit, 32-Bit, 64-Bit, Others), By Technologies (Edge AI Computing, Natural Language Processing (NLP), Machine Learning, Deep Learning, Others), By Sales Channel (Direct Sales, Distributors & Resellers, Online Sales), By End-Use Industry (Consumer Electronics, Automotive, Industrial Automation, Healthcare, Retail & E-Commerce, Aerospace & Defense,Others (Agriculture, etc.)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Nvidia Corporation, Advanced Micro Devices, Inc. (AMD), Alphabet Inc., Microsoft Corporation, Qualcomm Incorporated, STMicroelectronics NV, Texas Instruments Incorporated, Infineon Technologies AG, NXP Semiconductors, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |