Quick Navigation

Report Overview

The Global LendTech Market size is expected to be worth around USD 145.1 Billion By 2034, from USD 15.7 Billion in 2024, growing at a CAGR of 24.90% during the forecast period from 2025 to 2034. In 2024, North America accounted for over 38% of the total LendTech market share, equating to a revenue of approximately USD 5.9 billion.

LendTech, short for Lending Technology, refers to the use of technology to streamline and improve the lending process. This includes digital platforms, artificial intelligence (AI), machine learning (ML), blockchain, and other advanced tools that enhance how financial institutions and fintech companies assess creditworthiness, manage risk, and offer loans.

The LendTech market is rapidly growing, encompassing platforms like peer-to-peer lending, online loans, mortgage tech, and microfinancing. It attracts startups, fintechs, and large financial institutions aiming to innovate, reduce costs, and enhance customer experiences. The market evolves quickly due to shifting regulations, consumer preferences, and tech advancements.

Key drivers of LendTech markrt growth include consumer demand for faster, more convenient loan platforms and the shift to digital-first experiences. Advancements in AI and data analytics have improved credit risk assessments, making them more accurate and efficient. By leveraging alternative data sources, LendTech companies can provide loans to individuals and businesses that are often underserved by traditional banks.

According to Market.us, Global FinTech industry is expected to see tremendous growth. The market size is projected to reach around $1,382 billion by 2034, up from $234.6 billion in 2024, representing a CAGR of 19.40% during the forecast period from 2025 to 2034. In 2024, North America is expected to hold a dominant share of the market, contributing more than 39.7%, with total revenues projected at $93.1 billion.

Based data from EmilyJane, the average lending firm spends $1 million annually on software and data. This investment comes in light of the fact that current lending processes often have a lengthy funding period, typically taking 45-60+ days to complete.

In the broader landscape of LendTech, companies like LendingClub are making significant strides. LendingClub, a recognized leader in the space, serves over 10 million members and has facilitated more than $100 billion in loans. In 2022 alone, the company reported a revenue of $1.3 billion, marking a 20% growth from the previous year.

The FinTech industry as a whole is booming, with more than 100,000 apps available on platforms like Google Play and the Apple App Store. This growth reflects the increasing adoption of technologies like AI and machine learning, which are being used to streamline processes such as customer identity verification and securing critical loan documents.

In the UK, a concerning trend is emerging in the payday loan sector. Approximately 67% of payday loan borrowers and 49% of short-term installment borrowers are considered over-indebted, significantly higher than the 15% of the general UK adult population facing similar financial stress.

Key Takeaways

U.S. LendTech Market Size

The U.S. LendTech market is projected to reach a value of $5.6 billion by 2024, reflecting a robust compound annual growth rate (CAGR) of 22.8%. This rapid expansion highlights the increasing demand for innovative financial solutions that streamline the lending process.

LendTech, combining lending and technology, is transforming the financial ecosystem by driving efficiency, accessibility, and customer-focused services. The market grows with rising demand for digital lending platforms and the integration of AI, machine learning, and blockchain, improving credit assessment and risk management.

This market is also benefiting from the broader shift toward digital financial services, which is reshaping traditional lending models. More lenders are embracing technology-driven solutions to improve operational efficiency, reduce costs, and meet the evolving needs of borrowers. Additionally, regulatory changes and the growing interest in fintech solutions are playing a significant role in driving LendTech innovation.

In 2024, North America held a dominant position in the global LendTech market, accounting for over 38% of the total market share, which equates to a revenue of approximately USD 5.9 billion. The region leads due to advanced tech infrastructure, high fintech adoption, and strong regulatory support for digital services.

The U.S. market stands out as a key driver, with growing digital lending players and the rise of alternative lending platforms. Tech-savvy consumers and businesses in North America foster LendTech innovation, with AI, machine learning, and blockchain enhancing customer experience and lending processes.

One key factor contributing to North America’s dominance is the well-developed financial ecosystem, where established institutions and fintech startups work synergistically to provide a wide range of digital lending solutions. Additionally, the region’s relatively relaxed regulatory environment for fintech startups, paired with government initiatives that encourage innovation, has made it a hub for LendTech development.

North America offers significant growth potential in lending, driven by rising demand for fast, flexible credit and streamlined business financing. Venture capital supports LendTech startups, fostering innovation and rapid scaling. With ongoing advancements in digital lending technology, the region is set to maintain its market leadership.

Component Analysis

In 2024, the Solution segment of the LendTech market held a dominant position, capturing over 68% of the market share. This can be primarily attributed to the increasing reliance on automated tools and platforms that streamline the entire lending process.

Solutions such as loan origination systems, credit scoring platforms, and automated underwriting tools have become crucial for lenders aiming to enhance efficiency and reduce operational costs. These solutions not only make the loan approval process faster but also reduce human error, leading to a more reliable and cost-effective experience for both lenders and borrowers.

AI and machine learning are key drivers of the Solution segment’s dominance, enhancing credit assessment and risk management. These technologies enable faster data processing and improved decision-making, allowing lenders to offer personalized, inclusive loan options by assessing creditworthiness beyond traditional scores.

Another factor contributing to the Solution segment’s strong performance is the demand for end-to-end digital platforms. In an increasingly digital-first world, borrowers and lenders alike are gravitating toward solutions that offer seamless, all-in-one platforms for loan application, approval, disbursement, and management.

Type Analysis

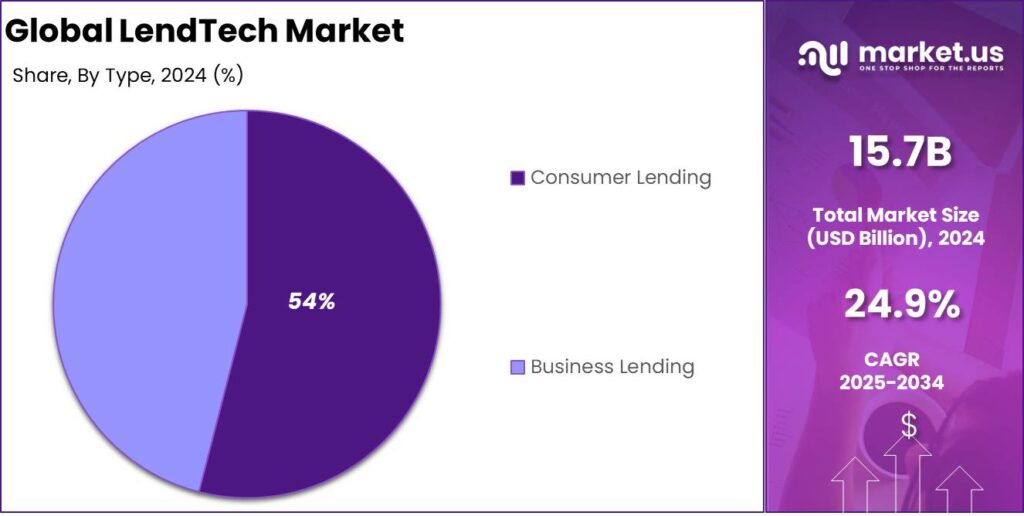

In 2024, the Consumer Lending segment held a dominant market position, capturing more than 54% of the total LendTech market share. This segment’s leadership can be attributed to the increasing demand for personal loans, mortgages, home loans, auto loans, student loans, and credit cards, which have become more accessible through digital platforms.

The growing preference for faster, more convenient lending solutions has encouraged both consumers and lenders to embrace digital-first approaches, particularly in personal and auto loan segments. Consumer lending, with its broad application to daily financial needs, remains the cornerstone of the LendTech market.

The Personal Loans sub-segment has experienced significant growth, largely due to the rising consumer desire for quick access to funds without the need for a traditional bank. Online platforms are providing a simpler and more transparent alternative to the conventional borrowing process, eliminating the need for excessive paperwork and long wait times.

Another major driver within the Consumer Lending segment is the growing demand for Mortgages and Home Loans. As homebuyers increasingly turn to digital platforms for competitive mortgage rates and simplified loan processes, the role of LendTech in transforming the home financing landscape becomes clearer.

Enterprise Size Analysis

In 2024, the Small and Medium Enterprises (SMEs) segment of the LendTech market held a dominant position, capturing more than 51% of the total market share. This significant share can be attributed to the growing need for flexible and accessible lending solutions among SMEs, which are often underserved by traditional financial institutions.

LendTech platforms are transforming SME financing by offering faster approvals, competitive interest rates, and more flexible credit requirements than traditional banks. As SMEs drive economic growth, their rising demand for financial support makes them a key segment in the LendTech market.

The rise of digital lending platforms tailored specifically for SMEs has enabled them to access funding more efficiently, without the long waiting periods or complex paperwork associated with conventional bank loans. These platforms leverage cutting-edge technologies like AI and machine learning to assess credit risk and provide personalized loan offerings.

This level of customization has greatly appealed to small business owners who may lack the credit history or collateral required for traditional loans, further driving the growth of the LendTech market in this segment. Moreover, the ease of access to capital allows SMEs to invest in growth opportunities, technology upgrades, and workforce expansion.

End-User Analysis

In 2024, the Banks segment held a dominant market position, capturing more than 57% of the global LendTech market share. This leadership can be attributed to the established infrastructure, robust financial backing, and customer trust that banks have cultivated.

Banks, leveraging their deep customer insights and extensive lending history, utilize advanced technologies to optimize lending processes, boost customer experience, and strengthen risk management. The integration of AI, machine learning, and blockchain enables more personalized, efficient, and secure lending solutions, solidifying their market position.

Banks’ significant market share is also attributed to their regulatory expertise and robust compliance systems, allowing them to navigate complex lending regulations. By investing in digital platforms and automation, they’ve reduced operational costs and accelerated loan origination processes.

Banks’ ability to utilize large-scale data analytics for credit risk assessment has reinforced their dominance. By analyzing vast transactional and behavioral data, they can more accurately evaluate creditworthiness, reducing defaults and boosting profitability. As they refine digital strategies and customer-centric offerings, banks are poised to maintain their leadership in the LendTech market.

Key Market Segments

By Component

- Solution

- Services

By Type

- Consumer Lending

- Personal Loans

- Mortgages and Home Loans

- Auto Loans

- Student Loans

- Credit Cards

- Business Lending

- Business Loans

- Commercial Loans

- Invoice Loans

- Trade Finance

- Equipment Financing

By Enterprise Size

- SMEs (Small and Medium Enterprizes)

- Large Enterprizes

By End-User

- Banks

- Credit Unions

- Non-banking Financial Companies

Driver

Growth in Digital Lending Adoption

One of the key drivers in the LendTech industry is the rapid growth of digital lending adoption. The increasing shift toward online platforms and mobile apps has made borrowing and lending more accessible, especially for consumers who previously faced challenges in securing loans through traditional banks.

In addition, with the rise of fintech startups and tech-savvy banks, many consumers are now looking for faster, more efficient ways to access loans. They’re increasingly opting for digital-first solutions that offer personalized options based on data analytics and AI-driven algorithms.

This growing trend has made digital lending a popular choice across different segments, from personal loans to business financing, pushing LendTech companies to innovate continuously. Financial inclusion is empowering more individuals and small businesses, driving the growth of the LendTech market.

Restraint

Regulatory Challenges

Regulatory challenges remain a major restraint for the LendTech industry. As digital lending models grow rapidly, they often operate in a regulatory gray area, which can vary significantly across different regions and countries. In many markets, governments have yet to establish clear and standardized regulations that govern digital lending practices.

Companies operating in multiple regions may struggle to comply with local laws while maintaining a seamless customer experience across borders. In addition, regulatory bodies are frequently tightening rules to protect consumers, which could increase the cost and complexity of compliance. These challenges may discourage new entrants into the LendTech space or slow the growth of existing players who must navigate complex legal frameworks.

Opportunity

Expanding Financial Inclusion

An emerging opportunity within the LendTech market is the ability to increase financial inclusion for underserved populations.Traditional banks often neglect remote individuals or those without credit access due to location, history, or socio-economic status. LendTech platforms, however, use data-driven credit scoring and digital solutions to reach these underserved groups.

By integrating alternative data sources such as mobile phone usage, social media activity, and transaction histories, LendTech companies can assess creditworthiness in a more inclusive manner. This opens up new lending opportunities for millions of unbanked or underbanked people worldwide, particularly in emerging markets. The ability to offer micro-loans or small-ticket loans through mobile apps also allows individuals to access capital for personal or business needs.

Challenge

Cybersecurity Risks

As the LendTech sector continues to scale, one of its biggest challenges is the increasing risk of cybersecurity breaches. The reliance on digital platforms to process sensitive financial data makes LendTech companies attractive targets for cybercriminals. Data breaches, identity theft, and fraud are serious risks that can undermine consumer trust and damage a company’s reputation.

With the digital lending process involving a substantial amount of personal and financial information, companies must implement robust cybersecurity measures to protect their clients. This includes securing databases, encryption, multi-factor authentication, and monitoring systems for suspicious activity. However, as cyber threats evolve, it becomes increasingly difficult for companies to stay ahead of potential risks.

Emerging Trends

One emerging trend in LendTech is the growing use of AI for credit scoring. Instead of relying on traditional credit scores, lenders are now using AI algorithms to analyze a broader range of data points, such as spending patterns and social media activity.

Another trend is the increasing use of blockchain for transparent and secure lending. Blockchain’s decentralized nature helps reduce fraud and increases trust in the loan process by providing a clear, immutable record of transactions.

The rise of “embedded finance” is also influencing the LendTech sector. Lending services are increasingly integrated into non-financial apps, simplifying loan access for consumers. In the future, lenders may partner with e-commerce sites or apps to offer real-time loans based on transaction history.

The concept of “open banking” is gaining traction, where third-party providers access customer financial data with their consent to offer more personalized lending options. This can increase competition and innovation in the lending space, benefitting both consumers and lenders.

Business Benefits

- Enhanced Customer Experience: With streamlined processes and faster approvals, customers experience a smoother and more transparent lending journey. LendTech platforms allow clients to apply for loans from the comfort of their homes, improving customer satisfaction.

- Data-Driven Decisions: LendTech platforms leverage big data and AI to assess creditworthiness more accurately. Businesses can offer personalized loan products based on a deeper understanding of customer behavior, reducing the risk of defaults.

- Better Risk Management: LendTech solutions provide advanced risk assessment tools, helping businesses predict and mitigate potential risks. With real-time data analysis and better insights, companies can identify red flags early, avoiding costly mistakes.

- Compliance & Regulation Management: LendTech tools help businesses stay compliant with ever-changing financial regulations. Automated tracking and reporting ensure that companies meet industry standards without manual oversight.

- Access to New Markets: By offering digital lending solutions, LendTech allows companies to reach underserved markets, including those in remote or developing regions. This opens up new revenue streams and customer bases that were previously difficult to tap into.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Several key players in LendTech Market have been instrumental in shaping its growth and development.

Nelito Systems Ltd. is a prominent player in the LendTech space, providing innovative software solutions for financial institutions. The company specializes in offering end-to-end solutions that improve banking operations, particularly in lending. Nelito’s core offerings include loan origination systems, loan servicing, and core banking solutions that enable financial institutions to offer faster and more accurate loan processing.

Tavantas is a growing name in the LendTech industry, specializing in digital lending solutions that cater to both traditional financial institutions and emerging fintech companies. Their products offer seamless integration, automation, and user-friendly interfaces that significantly enhance the loan application process.

Visa, Inc., one of the global leaders in digital payments, has also made significant strides in the LendTech sector. While Visa is primarily known for its payment processing systems, the company’s venture into digital lending solutions has been transformative. Through various partnerships and innovations, Visa has developed products that streamline credit and loan processes for both consumers and financial institutions.

Top Key Players in the Market

- Nelito Systems Ltd.

- Tavantas

- Visa, Inc.

- Pegasystems Inc.

- Roostify, Inc.

- Finastra

- Nelito Systems Pvt. Ltd.

- Newgen Software Technologies Limited

- American Express Company

- Fiserv, Inc.

- Q2 Software, Inc.

- Nelito Sysrems Pvt Ltd.

- Other Key Players

Top Opportunities Awaiting for Players

- Digitization of Loan Processes: By leveraging AI, machine learning, and automation, players can create a smoother customer experience, reduce operational costs, and improve loan approval times. The ongoing shift towards digital financial services in both developed and emerging markets creates substantial growth potential.

- Embedded Lending Solutions: LendTech companies can tap into this trend by offering embedded lending solutions providing loans directly within non-financial platforms. By integrating lending into a customer’s journey, businesses can enhance customer engagement, drive sales, and provide tailored financial products. This creates new revenue streams while ensuring a deeper connection with users.

- Alternative Credit Scoring Models: LendTech players have a significant opportunity to develop and deploy alternative credit scoring systems, using data from social media activity, transaction histories, and even alternative behavior metrics. This will enable lenders to assess creditworthiness for a broader customer base, reducing financial exclusion and opening up new markets.

- Partnerships with Traditional Banks: There is growing potential for collaboration between LendTech startups and traditional financial institutions. By forming strategic partnerships, LendTech companies can leverage the infrastructure, trust, and customer base of established players while offering advanced technologies and innovative products in return.

- Sustainability-Focused Lending: LendTech companies can capitalize on this trend by offering green loans, sustainable financing options, and eco-friendly investment opportunities. By aligning financial products with sustainability goals, LendTech companies can attract a loyal customer base while promoting environmental responsibility.

Recent Developments

- In October 2024, Tavant launched LO.ai, an AI-powered product designed to enhance the efficiency of loan officers and borrowers. This product aims to reduce loan manufacturing costs and improve loan pull-through rates by automating training and providing tools that increase borrower confidence.

- In November 2024, Moody’s Corporation has acquired Numerated Growth Technologies to enhance its LendTech solutions, expanding the capabilities of its Lending Suite. This move will provide customers across asset classes with even more powerful risk data and analytics.

- In February 2025, Newgen Software’s commercial lending solution was implemented by Massachusetts’ Enterprise Bank. This solution streamlines multiple lending processes on a low-code platform, enhancing efficiency and customer service.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 15.7 Bn |

| Forecast Revenue (2034) | USD 145.1 Bn |

| CAGR (2025-2034) | 24.90% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Solution, Services), By Type (Consumer Lending (Personal Loans, Mortgages and Home Loans, Auto Loans, Student Loans, Credit Cards), Business Lending (Business Loans, Commercial Loans, Invoice Loans, Trade Finance, Equipment Financing), By Enterprise Size (SMEs (Small and Medium Enterprizes), Large Enterprizes), By End-User (Banks, Credit Unions, Non-banking Financial Companies) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Nelito Systems Ltd., Tavantas, Visa, Inc., Pegasystems Inc., Roostify, Inc., Finastra, Nelito Systems Pvt. Ltd., Newgen Software Technologies Limited, American Express Company, Fiserv, Inc., Q2 Software, Inc., Nelito Sysrems Pvt Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |