Quick Navigation

Report Overview

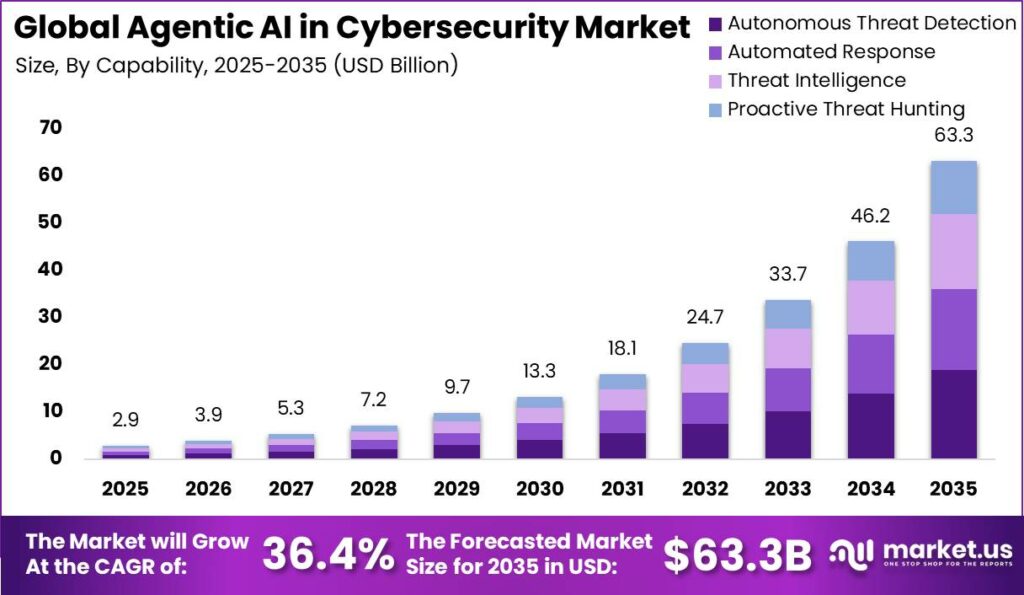

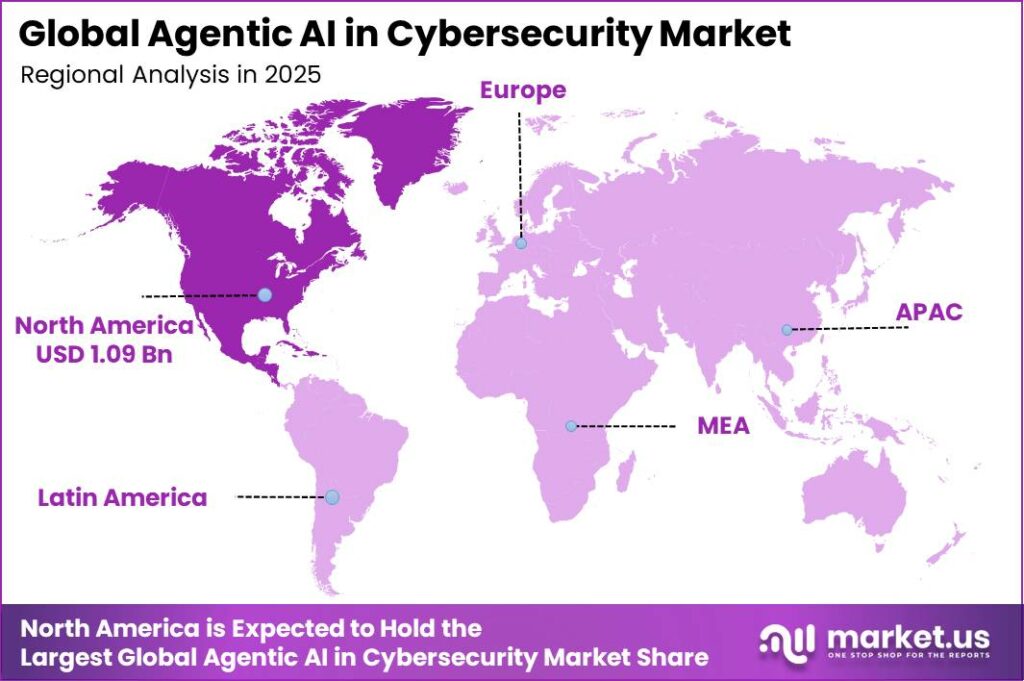

In 2025, the Agentic AI in Cybersecurity Market was valued at USD 2.86 billion and is projected to reach approximately USD 63.2 billion by 2035, growing at a strong 36.4% CAGR during 2026–2035. North America accounted for more than 38.0% of the global market in 2025, generating approximately USD 1.09 billion in revenue, driven by advanced digital infrastructure, high enterprise cybersecurity spending, and early adoption of AI-powered security technologies.

The market is expanding as organizations face a rapidly increasing cyber threat landscape that traditional security teams cannot handle alone. According to the International Telecommunication Union (ITU), around 6 billion people, representing 74% of the global population, used the internet in 2025, while 2.2 billion people remained offline.

This rise in global connectivity is increasing the number of endpoints, data exchanges, and potential attack surfaces, creating greater demand for autonomous cybersecurity solutions. The region’s growth is supported by increasing digital economic activity, with UNCTAD reporting that global trade in goods and services exceeded USD 35 trillion in 2025, while World Bank data shows that the digital economy contributes around 15% of global GDP, equivalent to nearly USD 16 trillion.

Key Takeaway

- The Agentic AI in Cybersecurity Market reached USD 2.86 billion in 2025 and is projected to reach USD 63.29 billion by 2035, growing at a 36.4% CAGR during 2026–2035.

- Autonomous Threat Detection dominated the capability segment with a 30.0% share,

- Cloud-Native deployment led the deployment segment with a 60.0% share, supported by scalable multi-agent cloud and single-tenant cloud security environments.

- SOC Automation held the largest application share at 32.0%

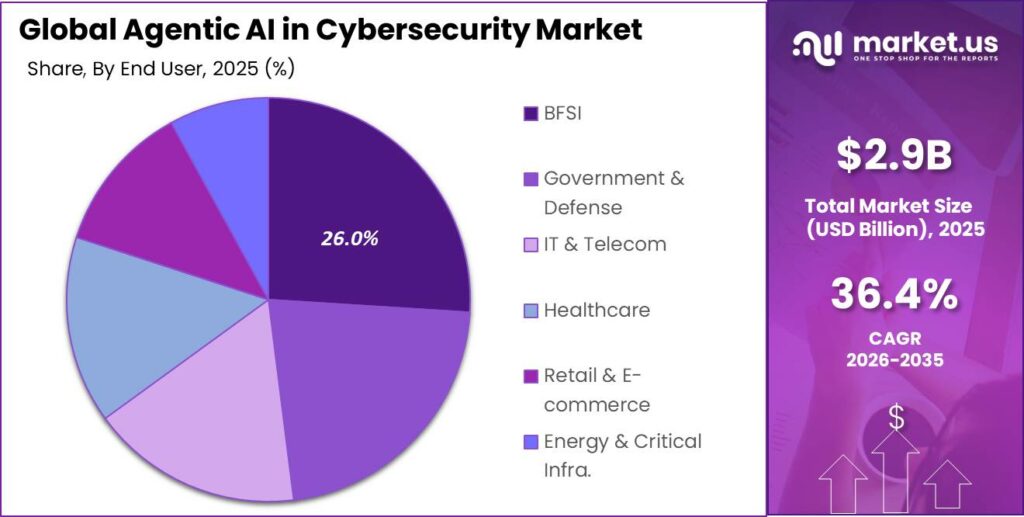

- BFSI was the leading end-user segment with a 26.0% share, supported by rising cybersecurity requirements across financial institutions.

- North America accounted for more than 38.0% of the global market in 2025, generating approximately USD 1.09 billion in revenue.

By Capability

Autonomous Threat Detection accounted for nearly 30% of Agentic AI in Cybersecurity capability spending in 2025, highlighting its critical role in modern security operations. The segment’s dominance is driven by the growing need to identify and respond to cyber threats faster as organizations face rising attack volumes and increasingly complex security risks.

Global cyber incidents are estimated to create around USD 500 billion in annual economic impact, including direct losses, business recovery costs, and additional cybersecurity investments, encouraging enterprises to adopt faster and more automated detection solutions.

Security Operations Centers (SOCs) are also experiencing increasing alert volumes, with organizations handling an average of around 960 alerts per day, while large enterprises manage more than 3,000 alerts daily. Due to limited resources, approximately 40% of security alerts remain uninvestigated, creating demand for AI-powered detection systems that can automatically analyze threats and prioritize critical risks.

Organizations implementing security AI and automation extensively can reduce breach costs by approximately USD 1.9 million per incident and shorten breach lifecycles by 80 days, demonstrating the financial benefits of autonomous detection capabilities.

By Deployment

Cloud-Native deployment accounted for approximately 60% of Agentic AI in Cybersecurity implementations in 2025, reflecting the strong enterprise shift toward cloud-first security architectures. This dominance was driven by rapid workload migration, increasing cloud adoption, and the need for scalable security solutions capable of protecting distributed digital environments.

The International Telecommunication Union (ITU) reported that global internet traffic passing through cloud data centers exceeded 19.5 zettabytes in 2025, increasing from 14.2 zettabytes in 2022. This significant growth highlights the expanding volume of cloud-hosted applications, systems, and data requiring continuous cybersecurity protection.

Cloud-native agentic AI platforms can process petabyte-scale logs, telemetry, and behavioral data, enabling real-time threat correlation, autonomous response, and self-healing capabilities across distributed cloud microservices environments. These capabilities are difficult to achieve with traditional fixed on-premises infrastructure due to scalability and processing limitations.

Furthermore, the Cloud Security Alliance (CSA) indicates that more than 90% of organizations rely on public or hybrid cloud environments for critical applications, increasing security risks at the cloud layer. This is driving enterprises to prioritize cloud-native agentic AI solutions for attack-surface management, AI-driven SIEM, and automated incident response to meet evolving compliance requirements and maintain operational uptime.

By Application

SOC Automation accounted for an estimated 32.0% of the Agentic AI in Cybersecurity Market by application in 2025, highlighting its critical role in addressing the growing gap between increasing cyber threats and limited Security Operations Center (SOC) resources. The segment’s growth is driven by rising cyber risks, cybersecurity skill shortages, and the need for faster automated threat management.

The World Economic Forum reported that 72% of organizations experienced increasing cyber risk, while only 14% believed they had sufficient cybersecurity skills. In addition, nearly 50% of public-sector organizations reported challenges in meeting their cybersecurity staffing goals, creating a significant operational gap. The (ISC)² estimated a global cybersecurity workforce shortage of approximately 4.76 million professionals, making it difficult for organizations to expand SOC teams through traditional hiring approaches.

This workforce shortage is occurring alongside a rapidly increasing threat environment. INTERPOL reported more than 6.5 billion cyber threats detected and mitigated across Asia and the South Pacific in 2024, with DDoS attacks increasing by 92% year-on-year, demonstrating the rising speed and scale of cyberattacks. Industry data also shows that 25–30% of SOC alerts remain uninvestigated, while analyst burnout exceeds 65%, highlighting the limitations of manual security operations.

By End User

The BFSI end-user segment accounted for a dominant 26.0% share of the Agentic AI in Cybersecurity Market in 2025, driven by the sector’s exceptionally high transaction volumes, valuable digital assets, and strict cybersecurity requirements.

The global payments industry processed 3.4 trillion transactions in 2023, generating USD 2.4 trillion in payment revenues, which represented around 35% of total banking revenue. This highlights the critical role of banks and payment providers in managing global digital value flows.

Global wealth reached approximately USD 600 trillion, with a significant share managed through banks, capital markets, and insurers. This large asset base requires continuous protection of customer accounts, trading systems, and policy records against increasingly automated cyber threats.

Key Market Segments

By Capability

- Autonomous Threat Detection

- Real-Time Network Monitoring

- Behavioral Anomaly Detection

- Automated Response

- Incident Auto-Remediation

- Automated Patch Deployment

- Threat Intelligence

- Dark Web Monitoring

- IOC Auto-Correlation

- Proactive Threat Hunting

By Deployment

- Cloud-Native

- Multi-Agent Cloud

- Single-Tenant Cloud

- Hybrid

- On-Premise

By Application

- SOC Automation

- Alert Triage / Management

- Tier-1 Analyst Task Offload

- Vulnerability Management

- Exploit Prediction

- Attack Surface Management

- Fraud & Insider Threat Detection

- Network Defense

By End User

- BFSI

- Government & Defense

- IT & Telecom

- Healthcare

- Hospital SOC Operations

- Medical Device Defense

- Retail & E-commerce

- Energy & Critical Infra.

Market Dynamics

Drivers

| Driver | (~) % CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Threat Velocity & Cost Escalation | +5.8% | Global, North America-led | Short term (≤ 2 years) |

| Autonomous SOC Adoption & Analyst Augmentation | +4.9% | North America, Western Europe | Short term (≤ 2 years) |

| Regulatory Compliance Mandates (EU AI Act, NIS2) | +4.2% | European Union, Global Exporters | Short term (≤ 2 years) |

| Enterprise AI-Security Budget Reallocation | +3.6% | North America, Asia-Pacific | Medium term (2–4 years) |

| AI-Accelerated Threat Actor Sophistication | +3.2% | Global | Short term (≤ 2 years) |

| Cloud-Native & Hybrid Infrastructure Proliferation | +2.8% | North America, APAC, Middle East | Medium term (2–4 years) |

Surging Threat Velocity & Cost Escalation

The root cause is a structural asymmetry between attack economics and legacy defense architectures: annual global cybercrime costs crossed $10.5 trillion in 2025, up from $3 trillion in 2015, with ransomware alone projected to inflict $74 billion in damage in 2026, striking a business or consumer every 2 seconds.

The quantitative mechanism that flows from this is straightforward: enterprise security breach cost analyses published by major technology vendors and cited in World Economic Forum institutional reports documented that the average breach cost reached $4.88 million in 2024, while organizations deploying AI-powered security detected and contained breaches 108 days faster, translating directly into an average $1.76 million per-incident cost saving.

Restraints

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Uncertainty & Fragmented AI Liability Regimes | -3.9% | EU, United States, India | Short term (≤ 2 years) |

| Proprietary Vendor Lock-In & Interoperability Barriers | -3.1% | Global, North America concentrated | Medium term (2–4 years) |

| High Deployment & Integration CapEx | -2.7% | SME Segments, Emerging Markets | Short term (≤ 2 years) |

| Data Sovereignty & Cross-Border AI Processing Bans | -2.3% | EU, India, China, Middle East | Medium term (2–4 years) |

| Board-Level AI Distrust & Human Oversight Mandates | -1.8% | Global, Regulated Industries | Short term (≤ 2 years) |

Regulatory Uncertainty & Fragmented AI Liability Regimes

The root cause is the simultaneous proliferation of materially non-harmonized AI governance frameworks across the market’s largest revenue geographies: the EU AI Act reached full general applicability on 2 August 2026, mandating continuous risk management (Article 9), tamper-evident log retention of at least 6 months (Article 12), human oversight capability (Article 14), and cybersecurity resilience (Article 15) for high-risk systems, with violations carrying penalties of up to €15 million or 3% of global turnover.

Strategically, agentic cybersecurity providers deploying autonomous decision-making agents in EU-facing enterprises must also navigate the GPAI model obligations that became effective 2 August 2025, while simultaneously tracking 59+ new AI regulations introduced in 2024 alone across non-EU jurisdictions, forcing multi-jurisdictional legal compliance overhead that meaningfully delays enterprise deal closure and depresses current-year revenue recognition.

Challenges

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| AI-Skilled Talent Deficit | -3.5% | Global, APAC Acute | Long term (≥ 4 years) |

| Agent Hallucination & False-Positive Risk | -2.9% | Global | Medium term (2–4 years) |

| Adversarial Agent Manipulation | -2.4% | Global, Critical Infrastructure | Long term (≥ 4 years) |

| Legacy SIEM & SOAR Integration Drag | -2.1% | North America, Western Europe | Medium term (2–4 years) |

| Multi-Agent Governance Complexity | -1.8% | Global, Enterprise Segment | Medium term (2–4 years) |

| Compute Cost & Inference Latency | -1.4% | Emerging Markets, Mid-Market | Short term (≤ 2 years) |

AI-Skilled Talent Deficit

The structural vulnerability is a demand-supply asymmetry that has now metastasized into a dual crisis: the global cybersecurity workforce gap reached approximately 4.8 million unfilled roles as of 2025 to 2026, requiring the existing workforce to increase by 87% just to satisfy current organizational demand, while the Asia-Pacific region alone carries a deficit of 3.4 million positions, a figure that grew from 2.7 million the prior year.

The friction this creates for the agentic AI cybersecurity segment is compounded by a skills gap within the gap: leading cybersecurity professional body workforce studies published in 2025 and 2026 confirmed that skills deficits have decisively overtaken headcount shortages as the top workforce problem, with 60% of organizations identifying skills gaps as the greater challenge, and 60% of enterprise security survey respondents specifically citing difficulty finding candidates with AI experience in cybersecurity, up from 57% the prior year.

Quantitatively, organizations with significant security staff shortages carry data breach costs averaging $1.76 million higher than adequately staffed peers, with understaffed firms absorbing an average breach cost of $5.74 million versus $3.98 million for those with adequate teams.

Opportunities

| Opportunity | (~) % CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Agentic MSSP Pricing Model Disruption | +4.6% | North America, Western Europe, APAC | Medium term (2–4 years) |

| OT & ICS Industrial Cybersecurity Expansion | +4.1% | Global, APAC & Europe Industrial Belts | Medium term (2–4 years) |

| Zero Trust Architecture Native Integration | +3.3% | North America, EU | Short term (≤ 2 years) |

| SME & Mid-Market Autonomous SOC Adoption | +2.7% | Global, Emerging Markets | Medium term (2–4 years) |

| Threat-Data Barter & Federated Intelligence Models | +2.1% | North America, EU | Long term (≥ 4 years) |

| Healthcare & Critical Infrastructure Vertical Penetration | +1.9% | North America, EU, Middle East | Medium term (2–4 years) |

Agentic MSSP Pricing Model Disruption

The Agentic AI in Cybersecurity market presents an untapped white-space opportunity rather than an active revenue driver, as major security vendors began integrating agentic capabilities into their platforms in 2025, while managed security service providers (MSSPs) have not yet fully adapted their pricing models.

Emerging opportunities include workflow-execution-based pricing, outcome-based models linked to threats neutralized, compute-based metering, and threat-data-for-services models using anonymized telemetry to improve AI agent performance. These approaches can improve provider economics, with outcome-based execution models estimated to increase effective gross margins by 18 to 25 percentage points at scale.

Only 6% of organizations had fully integrated AI automation across their security environment as of 2026, highlighting a significant adoption gap and conversion opportunity for MSSPs. Contract restructuring, agent-focused service models, and new SLA frameworks could unlock this demand over a 2 to 4-year execution window.

Geopolitical Impact Analysis

Geopolitical tensions are increasingly affecting the cost structure and supply chain stability of Agentic AI in Cybersecurity solutions, especially across critical hardware components such as AI accelerators, secure networking equipment, and computing infrastructure.

WTO data for 2025 indicates that average MFN tariffs on information and communication technology products in major G20 economies are within the 8–12% range, while fabricated metal components linked to steel and aluminum measures face effective rates above 30%. These higher trade costs are increasing expenses for AI security appliances, server racks, chassis, and secure enclosures.

Supply chain disruptions are also creating longer delivery timelines for essential components, including GPUs, high-bandwidth memory (HBM), and trusted platform modules. Security appliances and dedicated inference servers used in SOC environments are experiencing 5–10% higher landed costs. Energy price volatility is adding further pressure on semiconductor and electronics manufacturing.

IEA estimates show wholesale electricity prices in the European Union and United States increased by approximately 30–40% year-on-year in the first half of 2025, while India and Australia recorded 5–15% declines but remained above pre-2022 levels. Since electricity accounts for 20–30% of variable operating costs in semiconductor and electronics facilities, higher energy prices are increasing the cost of AI accelerators and secure computing infrastructure.

Regional Analysis

In 2025, North America dominated the global Agentic AI in Cybersecurity Market, accounting for around 38% of total revenues, equivalent to approximately USD 1.09 billion. The region’s leadership was driven by mature digital infrastructure, a strong concentration of leading AI and cybersecurity vendors, and early enterprise adoption of autonomous, agent-driven security platforms across BFSI, government, technology, and critical infrastructure sectors.

The United States remained the core demand center, supported by aggressive federal cybersecurity initiatives, strong private-sector investment, and increasing adoption of AI-powered security solutions. The U.S. alone contributed well over USD 1.5 billion to broader agentic AI ecosystems in recent base years, reflecting its strong position in AI innovation and cybersecurity spending.

Rising threats, including ransomware and nation-state attacks, encouraged organizations to shift from traditional rule-based and machine learning tools toward continuous, self-learning agentic security operations capable of autonomously detecting, prioritizing, and remediating risks in real time.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Agentic AI in Cybersecurity ecosystem is led by large-scale cybersecurity platforms and AI-focused security providers that are already deploying autonomous security workflows across enterprise environments.

Tier 1 players are estimated to account for around 55–65% of AI-driven security spending, supported by broad customer bases, strong AI capabilities, and integrated security platforms. Tier 2 vendors are expected to capture approximately 15–25% of the market, focusing on specialized autonomous detection, response, and threat intelligence solutions, while the remaining share is distributed among niche providers and internal security tools.

Among Tier 1 leaders, Palo Alto Networks reported fiscal 2025 revenue of USD 9.2 billion, growing 15% year-on-year, supported by AI-enabled platforms such as Cortex XSIAM, which integrates automated detection, threat correlation, and response capabilities.

CrowdStrike continues expanding its AI-driven Falcon platform toward an agentic SOC model, with Q4 FY2026 revenue reaching USD 1.31 billion compared with USD 1.06 billion in Q4 FY2025, and ARR reaching USD 4.24 billion in FY2025.

Microsoft and IBM are also major contributors through their large enterprise security ecosystems. Microsoft supports agentic security workflows through Copilot integrations across Sentinel and Defender, serving 1.4 million security customers and processing 84 trillion threat signals. IBM generated USD 67.5 billion in revenue in 2025, with its generative AI business exceeding USD 12.5 billion, supporting AI-driven security analytics, orchestration, and managed security services.

Tier 2 vendors, including SentinelOne and Darktrace, are focused on autonomous threat detection and response capabilities. SentinelOne reported FY2025 revenue of USD 821.5 million, growing 32%, with ARR of USD 920.1 million, driven by AI-native endpoint, XDR, and automated response solutions. Darktrace continues advancing its self-learning security platform toward more autonomous capabilities across network, cloud, and email protection.

Top Key Players in the Market

- CrowdStrike Holdings

- Palo Alto Networks

- SentinelOne

- Darktrace

- Microsoft Security

- Google Security AI

- IBM Security QRadar

- Vectra AI

- Exabeam

- Cybereason

- Secureworks

- ReliaQuest

Recent Developments

- February 2026 – Palo Alto Networks completed its acquisition of identity security vendor CyberArk in a transaction valued at approximately USD 25 billion, formally integrating the CyberArk Identity Security Platform into Cortex and Strata to secure human, machine and agentic AI identities at scale across global enterprise deployments.

- March 2026 – Google closed its acquisition of Wiz, a leading cloud and AI security platform, in an all-cash deal valued at roughly USD 32 billion, creating a combined multicloud cybersecurity and AI security stack on Google Cloud to protect large-scale AI workloads and agentic AI applications across global cloud environments.

- March 2026 – AWS and NVIDIA expanded their collaboration to support secure deployment of AI and generative AI models, committing to infrastructure for agentic AI environments on AWS that scales from USD 1.65 billion in agentic AI security spending in 2026 toward a projected USD 13.52 billion by 2032, underpinning long-term capacity for AI-driven cybersecurity operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.86 Billion |

| Forecast Revenue (2035) | USD 63.2 Billion |

| CAGR (2026-2035) | 36.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Capability (Autonomous Threat Detection, Automated Response, Threat Intelligence, Proactive Threat Hunting), By Deployment (Cloud-Native, Hybrid, On-Premise), By Application (SOC Automation, Vulnerability Management, Fraud & Insider Threat Detection, Network Defense), By End User (BFSI, Government & Defense, IT & Telecom, Healthcare, Retail & E-commerce, Energy & Critical Infrastructure) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | CrowdStrike Holdings, Palo Alto Networks, SentinelOne, Darktrace, Microsoft Security, Google Security AI, IBM Security QRadar, Vectra AI, Exabeam, Cybereason, Secureworks, ReliaQuest |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |