Global Abdominal Closure Systems Market By Product Type (Laparoscopic Abdominal Closure Devices and Traction Systems), By Material Type (Absorbable and Non-absorbable), By Application (General Surgery, Gynecology Surgery, Urology Surgery, Oncological Surgery and Others), By End User (Hospitals, Ambulatory Surgical Centers and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181057

- Number of Pages: 330

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

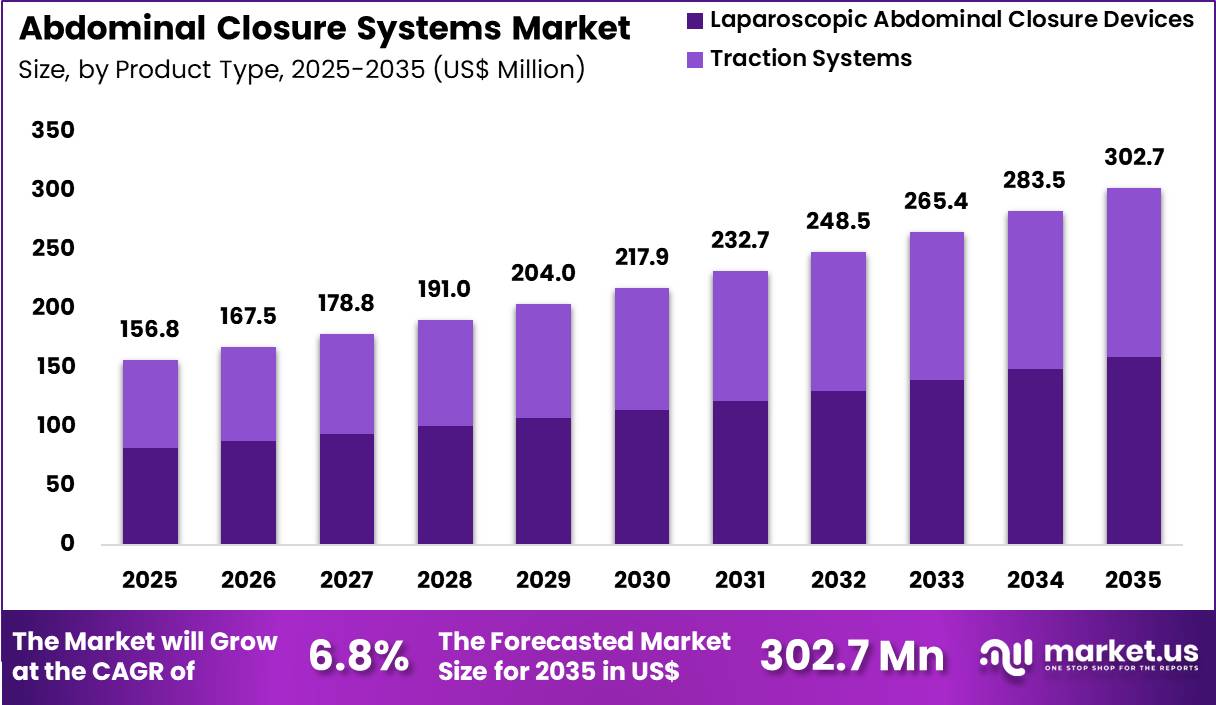

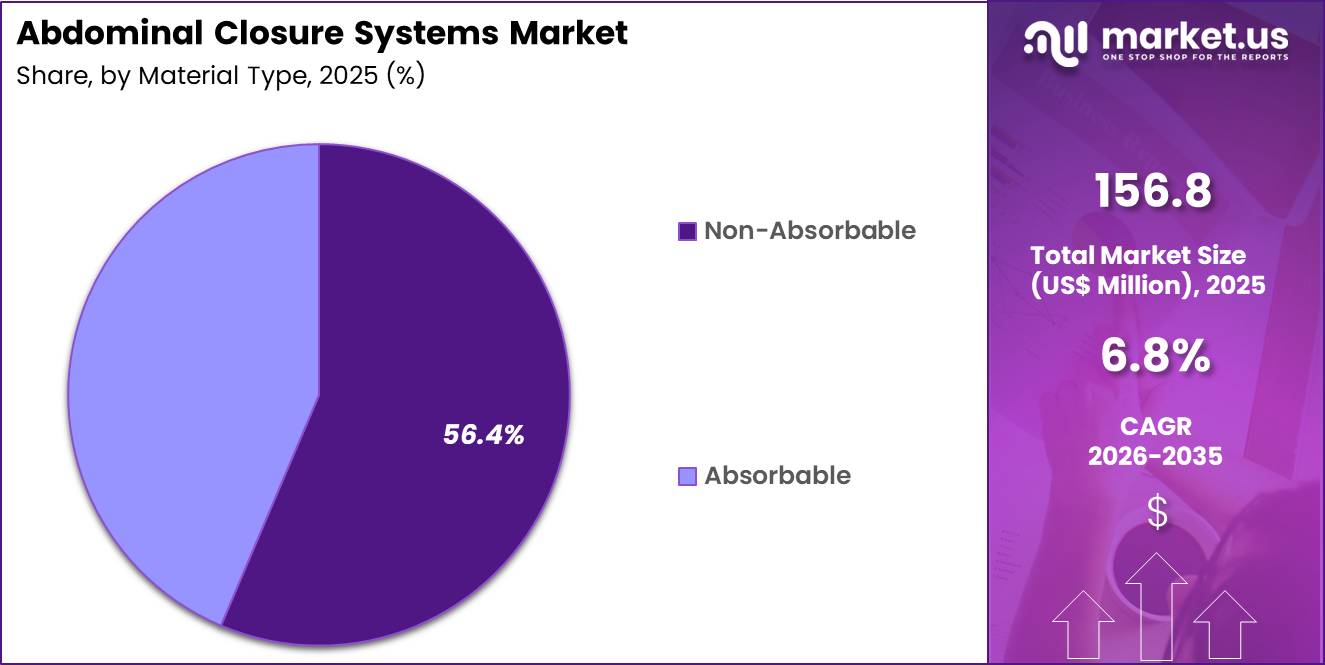

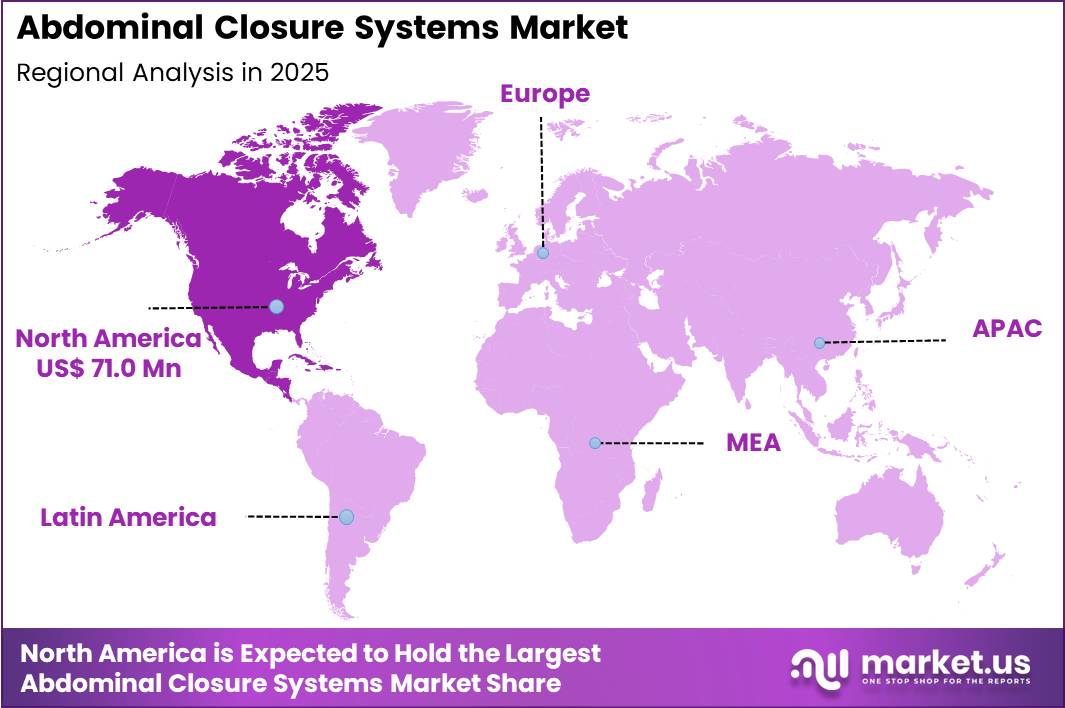

The Global Abdominal Closure Systems Market size is expected to be worth around US$ 302.7 Million by 2035 from US$ 156.8 Million in 2025, growing at a CAGR of 6.8% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 45.3% share with a revenue of US$ 71.0 Million.

Increasing demand for effective abdominal wall closure in complex surgical cases drives the Abdominal Closure Systems market as surgeons seek reliable solutions that minimize complications such as wound dehiscence, incisional hernias, and prolonged hospital stays.

General surgeons increasingly employ continuous suture techniques with slowly absorbable monofilament materials to achieve primary fascial closure after midline laparotomies, distributing tension evenly and reducing the risk of early wound failure in elective and emergency procedures.

These systems support temporary closure in damage-control laparotomy for trauma patients, where surgeons apply negative pressure wound therapy combined with bridging meshes or dynamic retention devices to protect viscera and facilitate delayed definitive closure.

In patients with abdominal sepsis or open abdomen syndrome, clinicians utilize dynamic fascial closure systems that apply regulated, constant tension to gradually approximate the fascial edges, promoting tissue remodeling and enabling higher rates of primary fascial closure without excessive tension on the midline.

These devices also find application in hernia repair and abdominal wall reconstruction, where component separation techniques combined with biologic or synthetic meshes reinforce large defects and restore abdominal wall integrity.

Manufacturers pursue opportunities to develop advanced dynamic closure systems with adjustable tension mechanisms and integrated monitoring, expanding applications in high-risk patients with obesity, poor tissue quality, or intra-abdominal hypertension where traditional static closure often fails.

Developers advance bioresorbable and antimicrobial-coated meshes that integrate with dynamic systems, broadening utility in contaminated fields by reducing infection rates and supporting gradual fascial reapproximation. These innovations facilitate minimally invasive delivery methods that limit additional tissue trauma during closure.

Opportunities emerge in hybrid solutions combining mechanical tension devices with biologic scaffolds to promote native tissue regeneration in chronic or recurrent hernias. Companies invest in evidence-based designs validated through multicenter studies, building surgeon confidence in complex cases.

In February 2026, a collaborative study involving major US surgical centers highlighted the efficacy of dynamic fascial closure systems that utilize constant, regulated tension. According to the study outcomes, these systems facilitate a higher rate of primary closure compared to traditional static methods, particularly in patients with complex abdominal sepsis.

Recent trends emphasize tension-regulated systems and regenerative biomaterials, positioning the market for growth in improved outcomes for high-risk abdominal wall closure scenarios.

Key Takeaways

- In 2025, the market generated a revenue of US$ 156.8 Million, with a CAGR of 6.8%, and is expected to reach US$ 302.7 Million by the year 2035.

- The product type segment is divided into laparoscopic abdominal closure devices and traction systems, with laparoscopic abdominal closure devices taking the lead with a market share of 52.6%.

- Considering material type, the market is divided into absorbable and non-absorbable. Among these, non-absorbable held a significant share of 56.4%.

- Furthermore, concerning the application segment, the market is segregated into general surgery, gynecology surgery, urology surgery, oncological surgery and others. The general surgery sector stands out as the dominant player, holding the largest revenue share of 45.3% in the market.

- The end user segment is segregated into hospitals, ambulatory surgical centers and others, with the hospitals segment leading the market, holding a revenue share of 55.9%.

- North America led the market by securing a market share of 45.3%.

Product Type Analysis

Laparoscopic abdominal closure devices accounted for 52.6% of growth within product type and dominate the abdominal closure systems market due to the rising preference for minimally invasive procedures that require secure trocar and port-site closure.

Surgeons increasingly use these devices because laparoscopic surgery supports smaller incisions, reduced postoperative pain, shorter hospital stay, and faster recovery, which strengthens the clinical shift toward specialized closure tools.

Hospitals and surgical teams also prefer dedicated laparoscopic closure devices because they improve suturing precision in deep abdominal layers and help reduce closure-related complications after port access. The segment is expected to strengthen further as minimally invasive general surgery continues to expand across both elective and emergency settings.

Evidence from clinical literature shows that laparoscopy reduces length of stay and postoperative morbidity compared with open approaches, which directly supports procedure growth and device demand.

Material Type Analysis

Non-absorbable materials accounted for 56.4% of growth within material type and dominate the abdominal closure systems market due to their higher tensile retention and dependable long-term wound support in abdominal wall closure.

Surgeons often prefer non-absorbable options in procedures where fascial integrity and sustained approximation remain critical, especially in patients with elevated intra-abdominal pressure or higher risk of wound failure. This segment is projected to maintain strong growth because abdominal closure continues to prioritize mechanical stability, predictable handling, and secure reinforcement during healing.

Device manufacturers also continue to improve suture and closure material design to support knot security, minimize tissue drag, and improve procedural efficiency in laparoscopic and open-assisted workflows. The segment is likely to benefit from the sustained volume of abdominal surgeries that require durable closure performance in hospitals and high-acuity surgical environments.

Application Analysis

Non-absorbable materials accounted for 56.4% of growth within material type and dominate the abdominal closure systems market due to their higher tensile retention and dependable long-term wound support in abdominal wall closure.

Surgeons often prefer non-absorbable options in procedures where fascial integrity and sustained approximation remain critical, especially in patients with elevated intra-abdominal pressure or higher risk of wound failure. This segment is projected to maintain strong growth because abdominal closure continues to prioritize mechanical stability, predictable handling, and secure reinforcement during healing.

Device manufacturers also continue to improve suture and closure material design to support knot security, minimize tissue drag, and improve procedural efficiency in laparoscopic and open-assisted workflows. The segment is likely to benefit from the sustained volume of abdominal surgeries that require durable closure performance in hospitals and high-acuity surgical environments.

End-User Analysis

Hospitals accounted for 55.9% of growth within end user and dominate the abdominal closure systems market due to their higher surgical volume, broader case complexity, and stronger access to minimally invasive operating infrastructure.

Hospitals manage a large share of both inpatient and ambulatory abdominal procedures, and CDC data on ambulatory surgery showed that hospitals represented 57% of ambulatory surgery visits in the US dataset cited, which supports their procedural concentration relative to many other settings.

This segment is expected to remain dominant because hospitals perform more emergency abdominal procedures, advanced laparoscopic cases, and oncological or multi-specialty surgeries that require reliable closure systems and trained surgical teams.

Hospitals also invest more consistently in laparoscopic platforms, surgical training, and standardized closure protocols, which strengthens device adoption and replacement demand. Their role is likely to stay central as minimally invasive surgery continues to scale across general and specialty abdominal care.

Key Market Segments

By Product Type

- Laparoscopic Abdominal Closure Devices

- Traction Systems

By Material Type

- Absorbable

- Non-absorbable

By Application

- General Surgery

- Gynecology Surgery

- Urology Surgery

- Oncological Surgery

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Others

Drivers

Rising revenue in MedTech segments is driving the market.

The abdominal closure systems market receives substantial propulsion from the consistent expansion observed in broader MedTech portfolios that encompass advanced closure technologies. Johnson & Johnson documented MedTech segment revenue of $27,427 million in 2022. This advanced to $30,400 million in 2023, signifying a 10.9% increase.

In 2024, the segment achieved $31,857 million, reflecting an additional 4.8 percent growth. Such progression illustrates escalating demand for innovative closure solutions in elective and emergency surgical procedures. Healthcare providers increasingly incorporate these systems to mitigate incision-related complications.

The revenue escalation facilitates ongoing enhancements in material science for stronger fascial approximation. Facilities benefit from integrated portfolios that streamline inventory management. This trajectory validates the clinical superiority of next-generation closure devices. Overall, the segment’s financial momentum underpins accelerated adoption across diverse surgical specialties.

Restraints

Currency impacts leading to reported revenue declines is restraining the market.

Braun encountered translational challenges that moderated the visibility of underlying growth in its surgical technologies offerings during the review period. The company recorded sales of €8.5 billion in fiscal year 2022. Sales rose to €8.755 billion in fiscal year 2023, a 3.0% increase. Fiscal year 2024 sales reached €9.137 billion, advancing 4.4 percent from the prior year.

Despite the euro-denominated growth, reported revenue declined by 1.55 percent in U.S. dollar terms for 2024. Adverse exchange rate fluctuations diminished the perceived expansion in international markets. Suppliers adjust pricing models to offset volatility in key currencies.

The restraint influences investor confidence in scaling production for closure system variants. Providers face potential disruptions in budgeting for imported technologies. This dynamic tempers the sector’s overall advancement amid global economic variances.

Opportunities

FDA breakthrough designations for bioabsorbable devices is creating growth opportunities.

Regulatory recognitions for novel materials present compelling avenues for differentiation in abdominal closure innovations. Absolutions Med obtained U.S. Food and Drug Administration breakthrough device designation on January 10, 2024, for its Rebuild bioabsorbable device. This status targets temporary abdominal closure to minimize hernia recurrence risks.

Opportunities emerge for resorbable scaffolds that eliminate removal surgeries and reduce foreign body reactions. Developers can expedite clinical validations through prioritized review pathways. The designation supports integration with existing negative pressure wound therapy systems.

Manufacturers gain competitive edges in tenders emphasizing long-term patient outcomes. Such advancements enable exploration of hybrid constructs for complex ventral hernias. Stakeholders anticipate enhanced reimbursement prospects for breakthrough-eligible products. This framework cultivates sustained investment in degradable polymer technologies.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic shifts influence the abdominal closure systems market through hospital procurement planning, surgical volumes, and budget discipline across operating departments. Inflation raises expenses for sutures, meshes, polymers, sterilization services, and packaging, which increases manufacturing and supply costs.

Higher interest rates tighten capital allocation for healthcare facilities, which slows purchasing decisions for advanced closure devices. Geopolitical tensions interrupt global sourcing of specialty fibers, coatings, and medical-grade materials, creating supply instability.

Current US tariffs on imported surgical materials and device components increase landed costs for distributors and healthcare providers. These pressures can delay inventory replenishment and limit rapid adoption of premium closure technologies in smaller hospitals.

At the same time, manufacturers strengthen domestic production and expand regional supplier networks to secure consistent availability. Growing surgical procedures and demand for improved wound management solutions continue to support steady and confident market growth.

Latest Trends

FDA clearance for automated abdominal wall suturing systems is driving the market.

Suturion AB secured U.S. Food and Drug Administration 510(k) clearance on January 22, 2025, for the SutureTOOL System. This device automates continuous suturing for midline abdominal closure post-laparotomy in adults aged 18 and older. The clearance classifies it under product code OMT for nonabsorbable multifilament sutures.

The system employs Filbloc sutures to achieve uniform tension and reduced operative times. Surgeons benefit from consistent fascial reapproximation in high-tension incisions. The approval demonstrates substantial equivalence to predicate manual techniques without new safety concerns.

Facilities report potential decreases in surgeon fatigue during prolonged procedures. The 2025 milestone aligns with preferences for semi-automated tools in open abdominal surgeries. Early integrations highlight compatibility with standard laparotomy protocols. Overall, this development elevates efficiency standards in closure practices.

Regional Analysis

North America is leading the Abdominal Closure Systems Market

North America accounted for 45.3% of the abdominal closure systems market in 2025 as hospitals and surgical centers increased adoption of advanced wound closure technologies to improve outcomes after major abdominal operations. The region performs a high volume of surgical procedures that require reliable closure solutions to prevent complications such as infection or wound dehiscence.

According to the US Centers for Disease Control and Prevention, about 51.4 million inpatient surgical procedures were performed annually in the United States in recent years, reflecting the substantial clinical demand for surgical closure devices used across multiple specialties.

Surgeons across trauma, oncology, and general surgery increasingly rely on specialized sutures, mesh systems, and negative pressure wound therapy devices to strengthen abdominal wall repair. Rising prevalence of obesity and gastrointestinal disorders has also increased the number of bariatric and abdominal surgeries performed in major medical centers.

Hospitals are integrating advanced biomaterials and antimicrobial sutures that improve tissue healing and reduce postoperative infection risks. Minimally invasive and robotic surgical techniques are also expanding the use of specialized closure devices designed for precision and efficiency.

Academic hospitals and surgical research centers continue to evaluate innovative closure techniques that enhance patient recovery. These factors collectively supported strong expansion of surgical wound closure technologies across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness steady growth during the forecast period as healthcare infrastructure expands and surgical capacity increases across emerging economies. Many countries in the region are strengthening hospital systems and expanding surgical services to meet growing demand from aging populations and rising chronic disease prevalence.

Recent research indicates that the number of abdominal hernia cases in Asia increased from about 3.12 million to 4.26 million over recent years, highlighting the expanding clinical need for effective surgical repair and reliable closure technologies. Hospitals across China, India, Japan, and Southeast Asia are increasing investments in advanced surgical equipment and postoperative care systems.

Surgeons are adopting improved suturing techniques and closure devices that reduce complication rates and support faster recovery after major abdominal procedures. Governments are also promoting national healthcare expansion programs that improve access to surgical care in urban and semi urban populations.

Medical training institutions are strengthening surgical education programs that emphasize modern wound management practices. Regional manufacturers are introducing cost effective biomaterials and closure systems suited to local healthcare budgets.

Growing collaboration between global medical device companies and regional hospitals is accelerating technology transfer and clinical adoption. These developments are expected to support continued growth of surgical wound closure technologies throughout Asia Pacific.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Abdominal Closure Systems market pursue expansion through continuous innovation in surgical sutures, mesh materials, and wound closure technologies that improve healing outcomes after abdominal procedures. Companies collaborate closely with surgeons and healthcare institutions to develop advanced closure solutions that reduce infection risk and enhance post-operative recovery.

They also expand manufacturing capacity and strengthen distribution partnerships with hospitals and surgical centers to widen product accessibility. Johnson & Johnson, through its Ethicon division, represents a major player in the Abdominal Closure Systems market and operates as a global healthcare company headquartered in New Jersey that develops surgical sutures, staplers, and wound closure technologies used in operating rooms worldwide.

The company focuses on research-driven product development and surgeon training programs to support safer surgical procedures. Competitors also pursue regulatory approvals, new product launches, and clinical collaborations to strengthen adoption of next-generation abdominal closure solutions across healthcare systems.

Top Key Players

- Medtronic plc

- Johnson & Johnson (Ethicon)

- 3M Company

- B. Braun Melsungen AG

- Teleflex Incorporated

- Smith & Nephew plc

- Baxter International Inc.

- Integra LifeSciences Corporation

- Essity AB

- Abbott Laboratories

- ACell Inc.

- neoSurgical Ltd.

- CooperSurgical, Inc.

- Golden Stapler Surgical Co., Ltd.

- Pride Medical Equipment

Recent Developments

- In January 2025, Absolutions Med announced that its Rebuild Bioabsorbable device, which received FDA breakthrough designation, entered broader clinical validation phases. According to recent reports, the device is specifically engineered for abdominal wall closure to significantly minimize the long-term risks of incisional hernias in high-risk patient populations.

- In May 2025, Solventum (formerly 3M Health Care) introduced updated clinical protocols for its AbThera Advance open abdomen negative pressure therapy system. As per recent clinical summaries, these updates focus on improving the medial tension required for primary fascia closure, aiming to reduce the duration of open abdomen management in trauma cases.

Report Scope

Report Features Description Market Value (2025) US$ 156.8 Million Forecast Revenue (2035) US$ 302.7 Mllion CAGR (2026-2035) 6.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Laparoscopic Abdominal Closure Devices and Traction Systems), By Material Type (Absorbable and Non-absorbable), By Application (General Surgery, Gynecology Surgery, Urology Surgery, Oncological Surgery and Others), By End User (Hospitals, Ambulatory Surgical Centers and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Medtronic plc, Johnson & Johnson (Ethicon), 3M Company, B. Braun Melsungen AG, Teleflex Incorporated, Smith & Nephew plc, Baxter International Inc., Integra LifeSciences Corporation, Essity AB, Abbott Laboratories, ACell Inc., neoSurgical Ltd., CooperSurgical, Inc., Golden Stapler Surgical Co., Ltd., Pride Medical Equipment. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Abdominal Closure Systems MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Abdominal Closure Systems MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Medtronic plc

- Johnson & Johnson (Ethicon)

- 3M Company

- B. Braun Melsungen AG

- Teleflex Incorporated

- Smith & Nephew plc

- Baxter International Inc.

- Integra LifeSciences Corporation

- Essity AB

- Abbott Laboratories

- ACell Inc.

- neoSurgical Ltd.

- CooperSurgical, Inc.

- Golden Stapler Surgical Co., Ltd.

- Pride Medical Equipment

Our Clients

- 181057

- March 2026