Quick Navigation

Overview

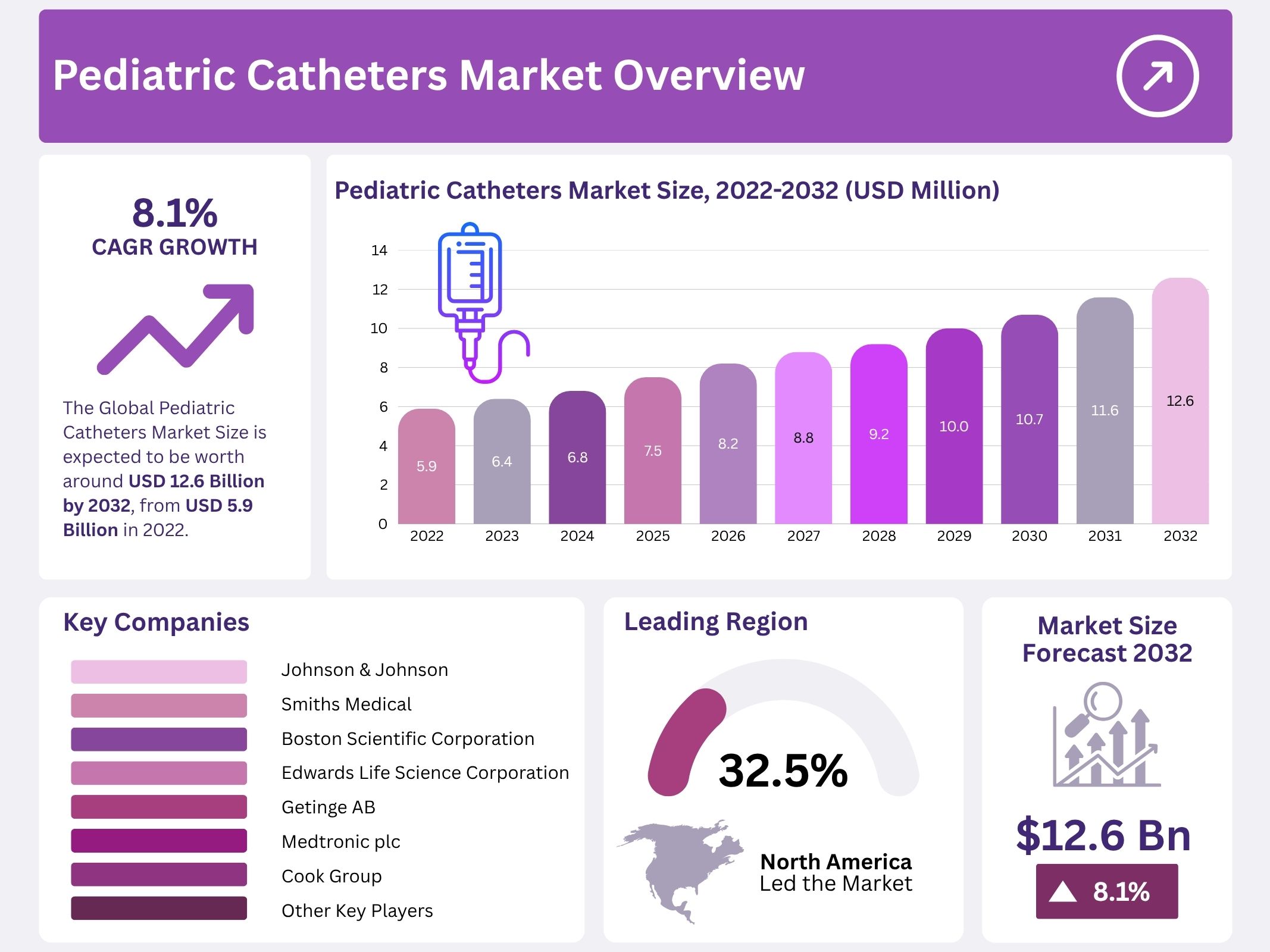

The Global Pediatric Catheters Market is projected to reach nearly USD 12.6 billion by 2032, rising from USD 5.9 billion in 2022. Growth is expected to proceed at a CAGR of 8.1% during the assessment period. The expansion of this market has been supported by a rising burden of congenital and chronic conditions among infants and children. Increased detection of cardiac defects, urinary tract disorders, neurological issues and complications linked to preterm births has elevated the use of catheter-based management. Early diagnosis through improved screening systems has further strengthened demand across hospitals and pediatric specialty units.

The availability of advanced neonatal and pediatric intensive care services has also influenced market expansion. Higher numbers of preterm and low-birth-weight infants have increased utilization of catheters for ventilation support, fluid administration, nutrition and monitoring. NICUs and PICUs rely heavily on catheter-based solutions for continuous care, contributing to stable demand. The steady rise in pediatric admissions requiring critical care intervention has reinforced the role of catheters as essential clinical tools in emergency and long-term treatment pathways.

Technological progress in catheter design and material science has improved safety and patient comfort. The adoption of biocompatible polymers, hydrophilic coatings and flexible silicone-based structures has reduced the risk of infection and minimized complications. Miniaturized designs suited to pediatric anatomy have enhanced placement accuracy and clinical outcomes. These advancements have encouraged healthcare providers to shift toward premium devices, leading to higher product adoption in both developed and emerging regions.

Safety-focused innovation continues to be a significant driver. Concerns regarding catheter-associated infections have supported the demand for antimicrobial coatings and closed-system products. Regulatory guidelines promoting sterile procedures and standardized catheter management have increased hospital compliance with high-quality devices. This emphasis on infection prevention has improved clinician confidence and contributed to consistent market growth across acute care and specialty settings.

Growing volumes of pediatric surgical and interventional procedures have further supported demand. Catheters are widely used in cardiology, urology, oncology and minimally invasive surgeries for diagnostic and therapeutic applications. Parallel investments in pediatric healthcare infrastructure in emerging economies have increased access to advanced products. Expanded training programs for clinicians have improved placement techniques and reduced complications, supporting broader adoption of specialized pediatric catheter solutions.

Key Takeaways

- The market is projected to expand at an 8.1% CAGR, with valuation expected to rise from USD 5.9 billion in 2022 to USD 12.6 billion by 2032.

- Growth is being supported by rising cases of neurological disorders and congenital heart defects, which continue to elevate the need for pediatric catheter procedures.

- Increasing global prevalence of urological diseases, particularly urinary tract infections, has been identified as a key factor strengthening overall catheter utilization.

- Expansion is being constrained by high treatment costs and limited reimbursement structures, which place financial pressure on providers and families seeking pediatric interventions.

- Polyvinyl chloride catheters maintain a 52.2% share, attributed to material suitability, safety profile, and widespread acceptance in pediatric clinical applications.

- Cardiovascular catheters hold a leading 41.1% share, supported by the high incidence of congenital heart anomalies requiring precision-focused diagnostic and therapeutic procedures.

- Hospitals and clinics represent 32.5% of demand, supported by increased adoption of intravascular ultrasound systems and broader availability of specialized pediatric care.

- Market opportunity is reinforced by rising research investments, expanding patient education initiatives, and the development of advanced catheter-related software applications.

- Adoption of modern design and manufacturing technologies is becoming more prominent worldwide, enhancing product performance and aligning with evolving pediatric clinical requirements.

- North America leads with 32.5% market share, followed by Europe, while Asia-Pacific is expected to accelerate due to higher healthcare investment and modernization.

Regional Analysis

North America maintained a notable position in the global pediatric catheters market. The region accounted for a 32.5% revenue share in 2022. This growth was supported by a rise in hospital-acquired infections. The presence of an advanced healthcare system further strengthened regional demand. Increased adoption of specialized pediatric devices also influenced market expansion. The overall development of clinical infrastructure improved access to catheterization procedures. These factors collectively reinforced the dominant market position of North America during the forecast period.

Europe was projected to secure the second-largest revenue share in the pediatric catheters market. Favorable reimbursement structures improved accessibility to pediatric catheterization. A continuous rise in inpatient procedures contributed to market growth. Higher hospitalization rates for chronic illnesses supported the demand for pediatric catheter solutions. The region’s established medical facilities enabled broader adoption of catheter technologies. Supportive regulatory frameworks further encouraged product usage. These combined elements strengthened Europe’s market performance throughout the assessment period.

Asia-Pacific was anticipated to witness substantial revenue generation in 2022. The rising burden of congenital heart defects increased the need for pediatric catheter procedures. Higher prevalence of structural anomalies in middle- and low-income settings supported market demand. Expanding public healthcare investment enhanced treatment capacity. Private sector participation also stimulated technological adoption. Growing awareness of pediatric intervention procedures improved utilization rates. These trends collectively positioned Asia-Pacific as a major contributor to global pediatric catheter market growth.

Segmentation Analysis

The pediatric catheters market has been segmented by material type. Polyvinyl chloride accounted for the largest revenue share of 52.2% in 2022. This growth has been attributed to its smooth insertion surface and flexible structure, which reduce irritation compared with other materials. Demand has been supported by rising urinary complications in children. Polyurethane catheters held the second-largest share. Their strength, toughness, and biocompatibility supported stable adoption during the historical period. These characteristics are expected to maintain consistent use across pediatric applications.

The market has been further segmented by product type. Cardiovascular catheters dominated with a revenue share of 41.1% in 2022. This leadership has been driven by the high incidence of congenital heart defects and the availability of a broad range of interventional devices. The urology segment is projected to grow at the fastest rate during the forecast period. Growth is being supported by rising cases of bladder and kidney disorders. Catheters used in urology procedures vary by age group, which increases product demand.

The end-user landscape shows clear concentration in hospitals and clinics. This segment accounted for the highest revenue share in 2022. Increased adoption of intravascular ultrasound systems and wider access to pediatric diagnostic services supported this position. Hospitals and clinics typically manage a broad range of urologic and cardiovascular conditions, which increases catheter usage. Ambulatory surgical centers are expected to expand at a moderate CAGR of 4.6 percent. Their growth is supported by rising outpatient procedures and improvements in pediatric surgical capabilities.

Key Market Segments

By Type

- Polyvinyl Chloride

- Silicone Catheter

- Polyurethane Catheter

- Other Types

By Product

- Cardiovascular

- Urology

- Neurovascular

- Specialty

- Other Products

By End-User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Other End-Users

Key Players Analysis

The pediatric catheters market is shaped by a broad set of global and regional manufacturers. The competitive landscape has been influenced by steady improvements in design quality, safety performance, and clinical efficiency. Large medical technology firms have expanded their pediatric portfolios to maintain strong market positions. Companies such as Johnson & Johnson, Smiths Medical, and Boston Scientific Corporation have strengthened their presence through continuous product development supported by significant research investments.

Product innovation has remained a central strategy across the industry. Advancements in minimally invasive technologies and biocompatible materials have been prioritized to address rising clinical needs in neonatal and pediatric care. Organizations like Edwards Life Science Corporation, Getinge AB, and Medtronic plc have focused on improved catheter durability and precision. Their efforts have contributed to increased adoption of advanced solutions in healthcare settings, supporting long term market expansion.

The competitive environment has also been defined by investments in manufacturing capabilities and broader distribution networks. Key participants have expanded production infrastructures to ensure stable supply and compliance with international standards. Companies including Cook Group, Flexicare Medical Ltd., and C.R. Bard, Inc. have reinforced their global footprint through enhanced operational efficiency. These initiatives have supported greater accessibility of specialized pediatric catheter products across developed and emerging markets.

Collaborations with healthcare providers, regulatory advancements, and strategic acquisitions have further strengthened market positions. Firms have aligned their product strategies with evolving clinical protocols to maintain relevance in specialized pediatric procedures. Major players such as Koninklijke Philips N.V., Abbott, B. Braun Melsungen AG, and Cardinal Health have broadened their offerings through targeted portfolio expansion. These actions, combined with contributions from various other competitors, continue to support stable and diversified market growth.

Market Key Players

- Johnson & Johnson

- Smiths Medical

- Boston Scientific Corporation

- Edwards Life Science Corporation

- Getinge AB

- Medtronic plc

- Cook Group

- Flexicare Medical Ltd.

- C.R. Bard, Inc.

- Koninklijike Philips N.V.

- Abbott

- B. Braun Melsungen AG

- Cardinal Health

- Other Key Players

Conclusion

The pediatric catheters market is expected to advance steadily as healthcare systems continue to strengthen early diagnosis and treatment for infants and children. Demand has been supported by rising cases of congenital and chronic conditions, wider access to intensive care units, and ongoing improvements in catheter design. Increased focus on safe materials, infection control, and precision-based procedures has encouraged the use of modern devices in hospitals and specialty centers. Progress in pediatric care, together with greater investment in healthcare infrastructure, is expected to sustain adoption. As clinical needs grow, the market is likely to benefit from continued innovation and broader availability of specialized catheter solutions.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Foley Catheter Market || Neurovascular Catheters Market || Microcatheter Market || APAC Transcatheter Aortic-Valve Replacement Market || Catheter Related Bloodstream Infection Market || Catheter Market || Coil Transcatheter Embolization and Occlusion Devices Market || Switzerland Coil Transcatheter Embolization and Occlusion Devices Market || Transcatheter Embolization And Occlusion Devices Market || Central Venous Catheter Market