Quick Navigation

Overview

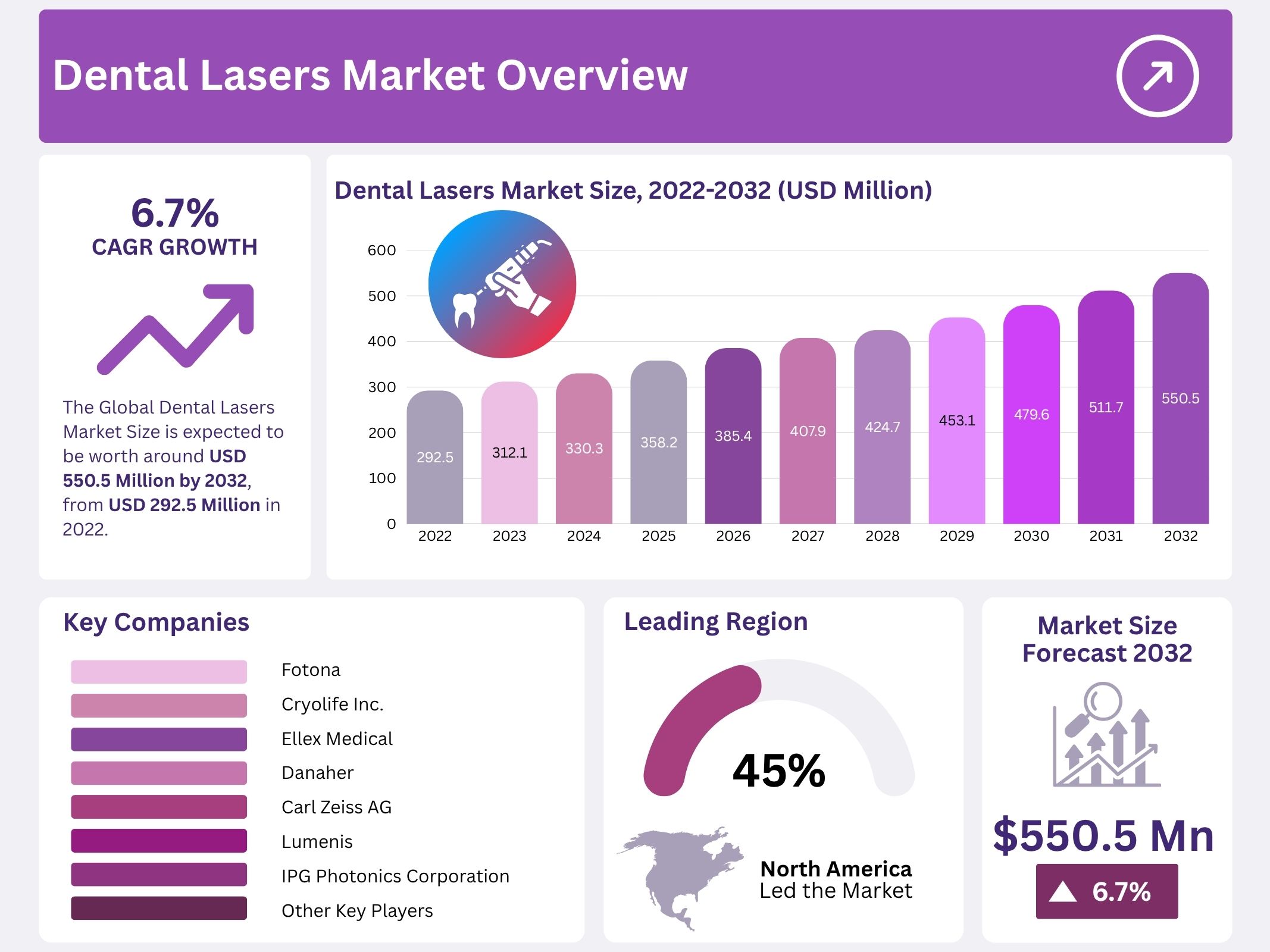

The global dental lasers market was valued at USD 292.5 million in 2022 and is projected to reach approximately USD 550.5 million by 2032, growing at a CAGR of 6.7% from 2023 to 2032. Growth is primarily driven by the increasing burden of oral diseases, the adoption of minimally invasive dental procedures, and technological innovations. Rising awareness of preventive dentistry and expanding dental infrastructure further enhance market prospects globally.

The increasing prevalence of oral disorders such as dental caries, periodontitis, and gingivitis has accelerated the demand for advanced dental treatments. According to the World Health Organization, oral diseases affect around 3.5 billion people worldwide. Dental lasers enable efficient management of soft and hard tissue conditions through precise, non-invasive procedures. This technology supports faster healing, less discomfort, and improved treatment outcomes, which makes it a preferred option in modern dentistry.

Patient preference for minimally invasive and pain-free treatments has strengthened the demand for dental lasers. These systems reduce bleeding, minimize anesthesia needs, and lower the risk of bacterial contamination. Their integration into clinical practice, especially in developed regions, reflects the growing emphasis on patient comfort and operational efficiency. Additionally, aesthetic dentistry—such as tooth whitening and gum contouring—has expanded the use of lasers due to their precision and superior cosmetic results.

Technological advancements have significantly enhanced the performance and accessibility of dental lasers. Modern systems now feature wavelength optimization for specific tissues, portable designs for small clinics, and integration with digital imaging systems. These developments have reduced procedural time, improved diagnostic accuracy, and supported data-driven treatment planning. The convergence of laser technology with artificial intelligence and digital dentistry is expected to further streamline operations and clinical outcomes.

Furthermore, rising investment in dental infrastructure and an expanding base of trained professionals are fueling market expansion. Educational institutions increasingly include laser dentistry in their curriculum, promoting wider clinical acceptance. The ageing global population and growing preventive care awareness are also increasing demand for laser-based dental solutions. Environmental advantages, such as reduced aerosol generation and minimal waste, enhance the appeal of these systems, aligning with sustainability and infection control standards.

Key Takeaways

- In 2022, the global dental lasers market was valued at approximately USD 292.5 million, reflecting growing adoption of advanced dental technologies.

- The market is forecasted to reach around USD 550.5 million by 2032, indicating robust expansion across various dental applications worldwide.

- A compound annual growth rate (CAGR) of 6.7% is projected for the period between 2023 and 2032, reflecting steady market momentum.

- The market is segmented into product type, application, and end-user categories, each contributing distinctively to overall industry growth.

- Soft tissue dental lasers are anticipated to experience the fastest growth rate among product types due to increasing use in minimally invasive treatments.

- The oral surgery segment is projected to dominate the application category, driven by growing demand for precision-based and painless procedures.

- Dental clinics represent the largest end-user group, owing to rising patient visits and higher adoption of laser-based dental treatments.

- Increasing demand for non-invasive and painless dental procedures is a key driver fueling the expansion of the dental lasers market.

- Rising elderly population and growing prevalence of edentulous conditions are significantly contributing to the market’s upward trajectory.

- High equipment costs and limited availability of skilled professionals are major challenges restricting wider adoption of dental lasers.

- The COVID-19 pandemic disrupted dental practices globally, but the market is currently witnessing gradual recovery and renewed procedural demand.

- North America continues to hold a substantial market share, supported by advanced healthcare infrastructure and favorable reimbursement policies.

Regional Analysis

The soft tissue segment is anticipated to witness the fastest growth in the market. This expansion is driven by the increasing number of soft tissue operations, where diode lasers are primarily utilized. Diode laser therapy is preferred due to its portability, cost-effectiveness, and ease of use. These advantages have led to greater adoption by surgeons seeking precision and convenience. The rising preference for minimally invasive procedures and growing disposable incomes are also expected to accelerate the segment’s growth during the forecast period.

The all-tissue segment is projected to record notable growth owing to its versatility and clinical benefits. All-tissue laser devices are effective in treating various oral cavity issues and offer superior performance compared to traditional equipment. Their multifunctional nature and reduced treatment discomfort enhance patient satisfaction. Moreover, by eliminating the need for needles, drilling sounds, and post-operative pain, these devices are becoming increasingly favored in modern dental practices. Such advantages are anticipated to strengthen product adoption in the near future.

The growing comfort and precision associated with all-tissue laser devices are attracting substantial investor interest. These devices enhance patient experience by minimizing pain and anxiety during dental procedures. Additionally, they enable dentists to perform operations more efficiently and safely. Investors are expected to fund product innovations that further simplify device handling and improve treatment outcomes. Consequently, the all-tissue laser category is likely to experience sustained growth as both patients and practitioners seek advanced, patient-friendly dental solutions.

Based on applications, the oral surgery segment is expected to dominate the market due to the rising prevalence of oral disorders such as gum disease, tooth decay, and oral cancer. Among end-users, dental clinics represent the largest market share owing to the increasing use of lasers for minimally invasive and efficient treatments. The wide availability of dental laser products and supportive reimbursement policies further stimulate adoption. These factors collectively contribute to the growing preference for laser technologies in clinical dental practices worldwide.

Segmentation Analysis

The soft tissue segment is anticipated to witness the fastest growth in the market. This expansion is driven by the increasing number of soft tissue operations, where diode lasers are primarily utilized. Diode laser therapy is preferred due to its portability, cost-effectiveness, and ease of use. These advantages have led to greater adoption by surgeons seeking precision and convenience. The rising preference for minimally invasive procedures and growing disposable incomes are also expected to accelerate the segment’s growth during the forecast period.

The all-tissue segment is projected to record notable growth owing to its versatility and clinical benefits. All-tissue laser devices are effective in treating various oral cavity issues and offer superior performance compared to traditional equipment. Their multifunctional nature and reduced treatment discomfort enhance patient satisfaction. Moreover, by eliminating the need for needles, drilling sounds, and post-operative pain, these devices are becoming increasingly favored in modern dental practices. Such advantages are anticipated to strengthen product adoption in the near future.

The growing comfort and precision associated with all-tissue laser devices are attracting substantial investor interest. These devices enhance patient experience by minimizing pain and anxiety during dental procedures. Additionally, they enable dentists to perform operations more efficiently and safely. Investors are expected to fund product innovations that further simplify device handling and improve treatment outcomes. Consequently, the all-tissue laser category is likely to experience sustained growth as both patients and practitioners seek advanced, patient-friendly dental solutions.

Based on applications, the oral surgery segment is expected to dominate the market due to the rising prevalence of oral disorders such as gum disease, tooth decay, and oral cancer. Among end-users, dental clinics represent the largest market share owing to the increasing use of lasers for minimally invasive and efficient treatments. The wide availability of dental laser products and supportive reimbursement policies further stimulate adoption. These factors collectively contribute to the growing preference for laser technologies in clinical dental practices worldwide.

Key Market Segments

Based on Product

- Soft Tissue Dental Lasers

- Dental Welding Lasers

- All Tissue Dental Lasers

- Other products

Based on Application

- Conservative Dentistry

- Endodontic Treatment

- Oral Surgery

- Implantology

- Peri-Implantitis

- Periodontics

- Tooth Whitening

- Other Applications

Based on End-User

- Hospitals

- Dental Clinics

- Other End-Users

Key Players Analysis

The dental lasers market is characterized by the presence of several established players, including Biolase, Inc., Dentsply Sirona, Danaher, and Fotona D.D. These companies focus on continuous innovation and strategic alliances to enhance their market position. Biolase Inc. has introduced the Epic Pro laser system designed for superior performance in soft tissue management. The technology integrates an intelligent temperature monitoring feature, ensuring consistent and predictable outcomes, which positions the company as a pioneer in advanced dental laser innovation.

Leading manufacturers such as Danaher, Carl Zeiss AG, and Koninklijke Philips N.V. emphasize expanding their dental product portfolios through mergers, acquisitions, and product diversification. Dentsply Sirona continues to strengthen its presence with advanced laser systems supporting precision dentistry. Similarly, Fotona’s research-driven innovations contribute significantly to the market by offering high-performance laser systems that address both soft and hard tissue applications. These companies’ strategies enhance clinical efficiency and patient comfort, thereby increasing adoption across dental practices globally.

The competitive landscape also includes emerging manufacturers such as AMD Lasers, Gigaalaser, and Han’s Laser Technology Industry Group Co., Ltd., which focus on affordability and technological differentiation. Shenzhen Mindray Bio-Medical Electronics Co., Ltd. and IPG Photonics Corporation leverage technological expertise to offer energy-efficient and compact laser solutions. These players are actively targeting developing economies, aiming to expand accessibility and affordability of dental laser treatments. Their efforts contribute to the rapid penetration of dental laser systems across varied clinical settings.

Furthermore, regional and niche players like Den-Mat Holdings L.L.C., R.C. Laser GmbH, and Sisma SpA are investing in product customization and clinician training programs. Their focus lies in providing specialized laser systems designed for specific dental procedures. Strategic collaborations with distributors and clinics are strengthening their market presence. Collectively, these players contribute to an increasingly competitive and innovation-driven environment, where technological advancements and clinical efficiency remain key determinants of market leadership.

- Shenzhen Mindray Bio-Medical Electronics Co. Ltd.

- Fotona

- Cryolife Inc.

- Ellex Medical

- Danaher

- Carl Zeiss AG

- Lumenis

- IPG Photonics Corporation

- Koninklijke Philips N.V.

- Dentsply Sirona

- AMD Lasers Inc.

- Biolase Inc.

- The Yoshida Dental MFG. Co. Ltd.

- Gigaalaser

- A.O. Group Inc.

- Kavo Dental

- Han’s Laser Technology Industry Group Co. Ltd.

- R.C. Laser Gmbh

- Den-Mat Holdings L.L.C.

- Sisma SpA

Conclusion

The dental lasers market is expanding steadily due to growing awareness of oral health and the shift toward pain-free, minimally invasive treatments. Advancements in laser technology have improved treatment accuracy, patient comfort, and clinical efficiency, leading to higher adoption across dental practices. Increasing demand for aesthetic and preventive dentistry further supports market growth. Key manufacturers are focusing on innovation and training to enhance accessibility and performance of laser systems. Despite challenges such as high equipment costs and skill shortages, the market outlook remains positive. Rising investments, ageing populations, and technological integration are expected to strengthen the global adoption of dental lasers in the coming years.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Dental Equipment Market | Dental Prosthetics Market | Dental Services Market | Dental Burs Market | Dental X-ray Market | Dental Turbines Market | Dental Loupe Market | Dental Syringes Market | Dental Anesthesia Market | Dental Tourism Market | Dental Implant Market | Dental Braces Market